Asia Pacific Food Additives Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD6214

December 2024

99

About the Report

Asia Pacific Food Additives Market Overview

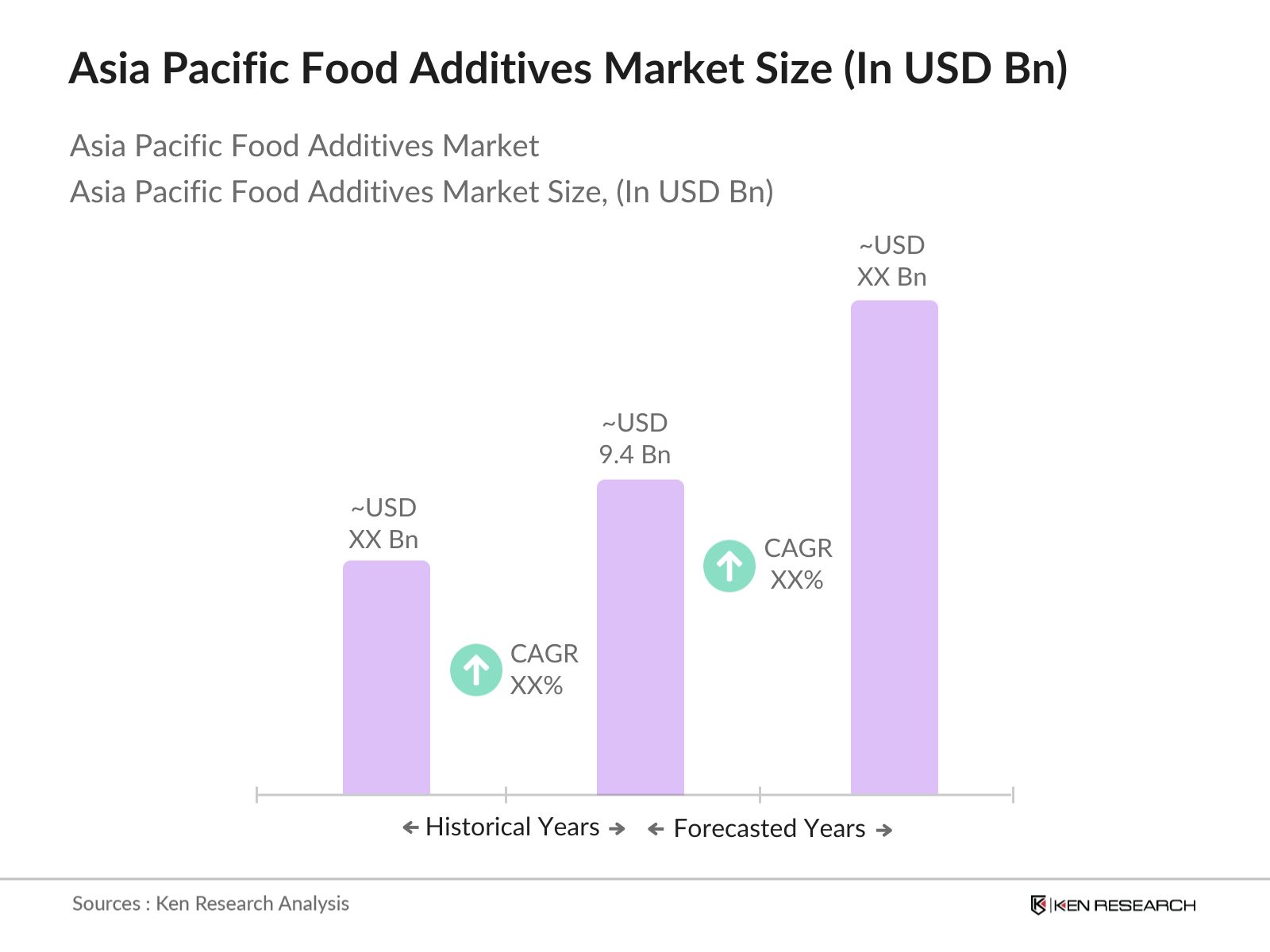

- The Asia Pacific Food Additives Market is valued at USD 9.4 billion, based on a five-year historical analysis. This growth is primarily driven by the increasing demand for processed foods across the region, which has led to a need for food additives that enhance the flavour, appearance, and shelf life of these products. Additionally, the rising health consciousness among consumers has increased demand for natural additives, driving market growth further.

- China, India, and Japan dominate the Asia Pacific Food Additives Market due to their large food processing industries, which cater to both domestic and international demand. Chinas dominance stems from its large-scale production facilities and high consumer base, while Japans leadership is influenced by advanced technologies and stringent food safety regulations. India, on the other hand, benefits from a growing population and increasing urbanization, further boosting the demand for processed and packaged foods.

- Food safety regulations across the Asia Pacific region are tightening, with government bodies like the Food Safety and Standards Authority of India (FSSAI) implementing stringent guidelines on additive use. In 2023, FSSAI introduced stricter controls on additives used in infant foods and beverages, ensuring higher safety and compliance standards. These regulations are mirrored in other countries such as China and South Korea, where food safety laws mandate regular inspections and certifications for additives used in food production, supporting the safer use of additives.

Asia Pacific Food Additives Market Segmentation

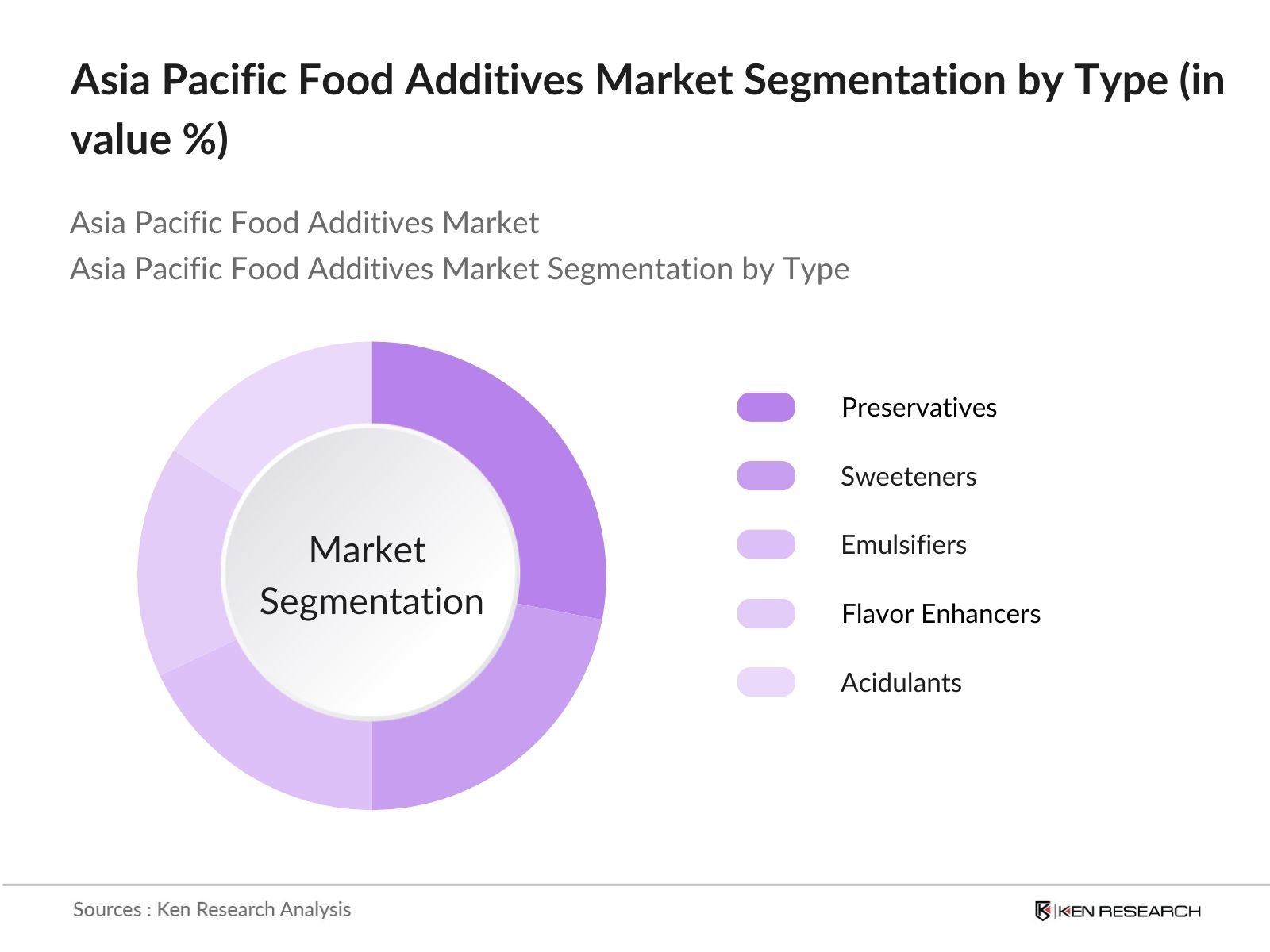

- By Type: The Asia Pacific Food Additives Market is segmented by type into Preservatives, Sweeteners, Emulsifiers, Flavour Enhancers, and Acidulants. Recently, Preservatives have a dominant market share under this segmentation, as they play a crucial role in extending the shelf life of processed foods, which are in high demand in the region. The expanding food processing industry, coupled with the rising consumption of ready-to-eat products, has driven the demand for preservatives.

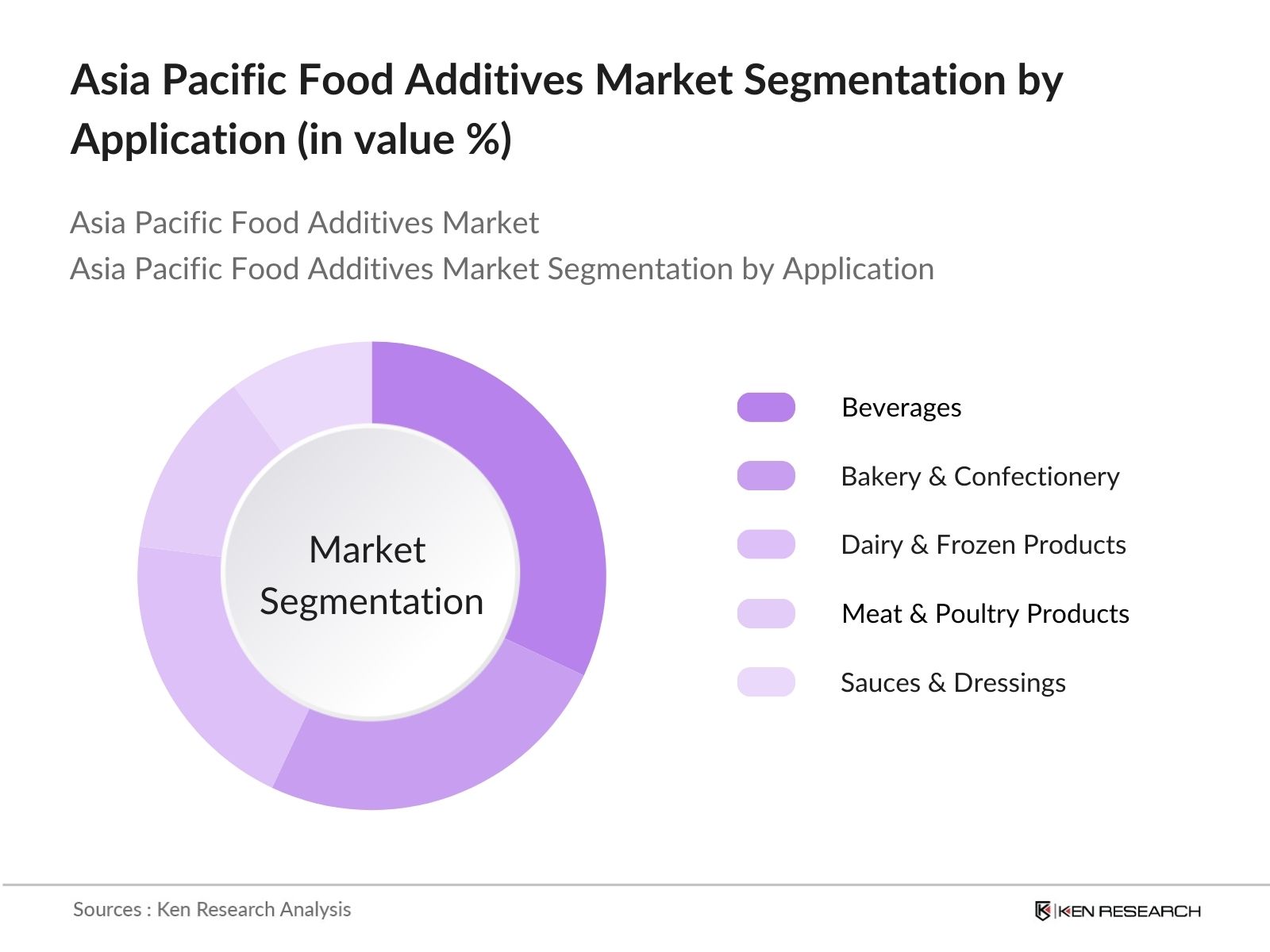

- By Application: The market is also segmented by application into Beverages, Bakery & Confectionery, Dairy & Frozen Products, Meat & Poultry Products, and Sauces & Dressings. Beverages hold the largest market share in this category, driven by the rising consumption of functional drinks, energy drinks, and ready-to-drink beverages. The regions hot and humid climate, coupled with changing consumer preferences, has contributed to the higher consumption of beverages, which in turn increases the need for additives that enhance flavour, texture, and appearance.

Asia Pacific Food Additives Market Competitive Landscape

The Asia Pacific Food Additives Market is dominated by a few key players, including major global and regional companies. These companies have influence on the market due to their established distribution networks, strong research and development capabilities, and ability to innovate with new food additive products that align with consumer trends.

Company Name | Establishment Year | Headquarters | No. of Employees | Revenue (USD Bn) | Product Portfolio | Market Position | R&D Investment | Manufacturing Facilities | Distribution Network |

Archer Daniels Midland (ADM) | 1902 | Chicago, USA | - | - | - | - | - | - | - |

Cargill, Inc. | 1865 | Minnesota, USA | - | - | - | - | - | - | - |

Kerry Group | 1972 | Tralee, Ireland | - | - | - | - | - | - | - |

BASF SE | 1865 | Ludwigshafen, Germany | - | - | - | - | - | - | - |

Givaudan | 1895 | Vernier, Switzerland | - | - | - | - | - | - | - |

Asia Pacific Food Additives Market Analysis

Asia Pacific Food Additives Market Growth Drivers

- Rising Processed Food Demand: The demand for processed foods in the Asia Pacific region is on a substantial rise, driven by rapid urbanization, a growing middle-class population, and shifting consumer lifestyles. Countries like China and India have witnessed a sharp increase in processed food consumption, with processed food imports in India increasing to $1.2 billion in 2022. Similarly, Chinas food processing sector generated around $1.85 trillion in revenues in 2022. This growth is further fueled by busy consumer lifestyles and a higher inclination towards convenience foods. The expansion of supermarkets and hypermarkets across APAC has made processed foods more accessible.

- Health-Conscious Consumer Trends: The shift toward health-conscious consumption is becoming increasingly pronounced in the Asia Pacific market. In Japan, health and wellness food product sales reached $55 billion in 2023. In Australia, 68% of consumers indicated a preference for healthier food alternatives, which has led to the demand for food additives that reduce sugar and salt content. Furthermore, the rise of functional foods, including additives that provide additional health benefits such as vitamins and minerals, is contributing to this market growth, as consumers are more aware of food labels and the ingredients they consume.

- Advances in Additive Technologies: The Asia Pacific food additives market is benefiting from technological advancements in additive production, particularly in areas such as microbial fermentation and enzyme-based additives. South Korea's food industry has invested over $500 million in R&D for advanced additives between 2022 and 2023. Additionally, China is focusing on producing bio-based additives through advanced fermentation technologies, further pushing innovation in this sector. These innovations help improve food shelf-life, taste, and texture, while aligning with consumer preferences for natural ingredients.

Asia Pacific Food Additives Market Challenges

- Regulatory Compliance Complexity: Navigating the complex regulatory landscape in the Asia Pacific region remains a major challenge for the food additives industry. For example, there are over 1,000 individual food safety regulations in place across Southeast Asian countries. In 2023, companies spent an estimated $1.3 billion complying with various regulatory requirements, including the need for certifications and product reformulations. Differences in food additive standards between markets, such as those in Japan and China, further complicate the ability of companies to launch products across multiple countries seamlessly.

- Raw Material Price Volatility: The food additives industry in Asia Pacific faces major challenges due to volatile raw material prices. The price of raw materials such as sugar, oil, and natural colours saw fluctuations of over 15% in 2023, primarily due to geopolitical tensions and supply chain disruptions. For example, palm oil prices, a key ingredient in many emulsifiers, increased from $900 to $1,200 per metric ton between 2022 and 2023. Such price volatility affects the production costs of food additives, leading to lower profit margins for manufacturers.

Asia Pacific Food Additives Market Future Outlook

Over the next five years, the Asia Pacific Food Additives Market is expected to show robust growth, driven by rising consumer demand for processed foods, increasing health awareness, and continuous innovations in natural additives. Growth in urbanization and the expansion of e-commerce platforms are also likely to contribute to market expansion, with major players investing heavily in research and development to meet changing consumer preferences and comply with stringent regulatory standards.

Asia Pacific Food Additives Market Opportunities

- Growth in Natural Food Additives Demand: Natural food additives are gaining momentum as consumers increasingly favour clean-label products across the Asia Pacific region. The demand for natural preservatives like rosemary extract and plant-based colorants like beetroot has surged, particularly in countries such as Australia and Japan. In 2023, the market for natural food colorants in Asia Pacific reached $1.5 billion, with double-digit growth in sectors like dairy and bakery. The trend is propelled by consumer awareness of health and wellness and the preference for organic and minimally processed foods.

- Innovations in Food Preservation Additives: The need to extend the shelf life of processed foods without compromising safety or quality is driving innovation in food preservation additives. In 2023, Japan and China invested a combined $200 million in developing next-generation preservatives such as antimicrobial peptides and enzyme inhibitors. These innovations aim to reduce reliance on synthetic preservatives while maintaining food quality, particularly for perishable goods like dairy and seafood. Southeast Asian markets, including Thailand and Vietnam, are also seeing rising demand for advanced preservation technologies in food exports.

Scope of the Report

By Type | Preservatives Sweeteners Emulsifiers Flavor Enhancers Acidulants |

By Source | Synthetic Natural |

By Application | Beverages Bakery & Confectionery Dairy & Frozen Products Meat & Poultry Products Sauces & Dressings |

By Functionality | Flavouring Agents Colouring Agents Preservative Agents Nutritional Additives |

By Region | China India Japan Australia & New Zealand Southeast Asia |

Products

Key Target Audience

Food and Beverage Manufacturers

Processed Food Producers

Natural and Organic Product Manufacturers

Food Additive Suppliers

Banks and Financial Institutions

Government and Regulatory Bodies (Food Safety and Standards Authority of India, Chinese Food and Drug Administration)

Investors and Venture Capitalist Firms

Supermarket and Hypermarket Chains

Food Technology Startups

Companies

Players Mentioned in the Report

Archer Daniels Midland (ADM)

Cargill, Inc.

Kerry Group

BASF SE

Givaudan

Tate & Lyle

Ajinomoto Co., Inc.

Ingredion Incorporated

DSM Nutritional Products

Chr. Hansen Holding A/S

Table of Contents

1. Asia Pacific Food Additives Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Market CAGR and Growth Trends)

1.4. Market Segmentation Overview

2. Asia Pacific Food Additives Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Food Additives Market Analysis

3.1. Growth Drivers

3.1.1. Rising Processed Food Demand

3.1.2. Health-Conscious Consumer Trends

3.1.3. Government Regulations on Food Quality

3.1.4. Advances in Additive Technologies

3.2. Market Challenges

3.2.1. Regulatory Compliance Complexity

3.2.2. Raw Material Price Volatility

3.2.3. Consumer Mistrust Towards Synthetic Additives

3.3. Opportunities

3.3.1. Growth in Natural Food Additives Demand

3.3.2. Innovations in Food Preservation Additives

3.3.3. Expansion into Emerging Markets in Southeast Asia

3.4. Trends

3.4.1. Shift Toward Clean Label Ingredients

3.4.2. Increase in Plant-Based Additives

3.4.3. Rise of Microbial and Enzyme-based Additives

3.5. Government Regulations

3.5.1. Food Safety and Standards Authority Regulations

3.5.2. Banned Substance Lists (APAC-specific)

3.5.3. Import/Export Policies for Additives

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia Pacific Food Additives Market Segmentation

4.1. By Type (In Value %)

4.1.1. Preservatives

4.1.2. Sweeteners

4.1.3. Emulsifiers

4.1.4. Flavour Enhancers

4.1.5. Acidulants

4.2. By Source (In Value %)

4.2.1. Synthetic

4.2.2. Natural

4.3. By Application (In Value %)

4.3.1. Beverages

4.3.2. Bakery & Confectionery

4.3.3. Dairy & Frozen Products

4.3.4. Meat & Poultry Products

4.3.5. Sauces & Dressings

4.4. By Functionality (In Value %)

4.4.1. Flavouring Agents

4.4.2. Colouring Agents

4.4.3. Preservative Agents

4.4.4. Nutritional Additives

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia & New Zealand

4.5.5. Southeast Asia

5. Asia Pacific Food Additives Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Archer Daniels Midland (ADM)

5.1.2. Cargill, Incorporated

5.1.3. Kerry Group

5.1.4. BASF SE

5.1.5. Givaudan

5.1.6. Tate & Lyle

5.1.7. Ajinomoto Co., Inc.

5.1.8. Ingredion Incorporated

5.1.9. DSM Nutritional Products

5.1.10. Chr. Hansen Holding A/S

5.1.11. DuPont

5.1.12. Corbion N.V.

5.1.13. Sensient Technologies Corporation

5.1.14. Lonza Group

5.1.15. International Flavors & Fragrances (IFF)

5.2. Cross Comparison Parameters (Product Portfolio, Manufacturing Facilities, Research & Development Investments, Supply Chain Network, Revenue, Market Position, Product Innovation, Distribution Network)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Private Equity and Venture Capital Funding

5.8. Government Grants and Support Programs

6. Asia Pacific Food Additives Market Regulatory Framework

6.1. Food Additive Regulation Standards (Specific to APAC countries)

6.2. Compliance and Certification Processes

6.3. Import and Export Laws for Food Additives

7. Asia Pacific Food Additives Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Food Additives Future Market Segmentation

8.1. By Type (In Value %)

8.2. By Source (In Value %)

8.3. By Application (In Value %)

8.4. By Functionality (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Food Additives Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

DisclaimerContact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involved mapping the stakeholder ecosystem within the Asia Pacific Food Additives Market. Extensive desk research utilizing secondary and proprietary databases was conducted to gather information on key market variables, such as product innovation and regulatory frameworks.

Step 2: Market Analysis and Construction

This phase involved compiling historical data on market penetration and revenue generation. A thorough assessment of food additives role in various food segments helped in constructing accurate market forecasts. Service quality statistics were also evaluated for validation purposes.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were tested through interviews with industry experts using computer-assisted telephone interviews (CATI). These consultations provided financial and operational insights, further refining the data gathered in the previous steps.

Step 4: Research Synthesis and Final Output

The final step involved direct engagement with food additive manufacturers, providing detailed insights into market dynamics, consumer preferences, and product performance. This ensured a comprehensive and validated report on the Asia Pacific Food Additives Market.

Frequently Asked Questions

01. How big is the Asia Pacific Food Additives Market?

The Asia Pacific Food Additives Market is valued at USD 9.4 billion, driven by the growing demand for processed foods, health-conscious consumers, and the rising popularity of natural additives.

02. What are the challenges in the Asia Pacific Food Additives Market?

Key challenges in the Asia Pacific Food Additives Market include regulatory compliance across different countries, raw material price volatility, and consumer scepticism towards synthetic additives. The market also faces logistical challenges due to diverse regional preferences.

03. Who are the major players in the Asia Pacific Food Additives Market?

Key players in the Asia Pacific Food Additives Market include Archer Daniels Midland (ADM), Cargill, Kerry Group, BASF SE, and Givaudan. These companies dominate the market due to their extensive product portfolios, strong distribution networks, and investment in innovation.

04. What are the growth drivers of the Asia Pacific Food Additives Market?

The Asia Pacific Food Additives Market is driven by rising urbanization, increased demand for processed and convenience foods, consumer interest in healthier products, and technological innovations in food preservation and flavouring.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.