Asia Pacific Fuel Cell Vehicle Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD4847

December 2024

90

About the Report

Asia Pacific Fuel Cell Vehicle Market Overview

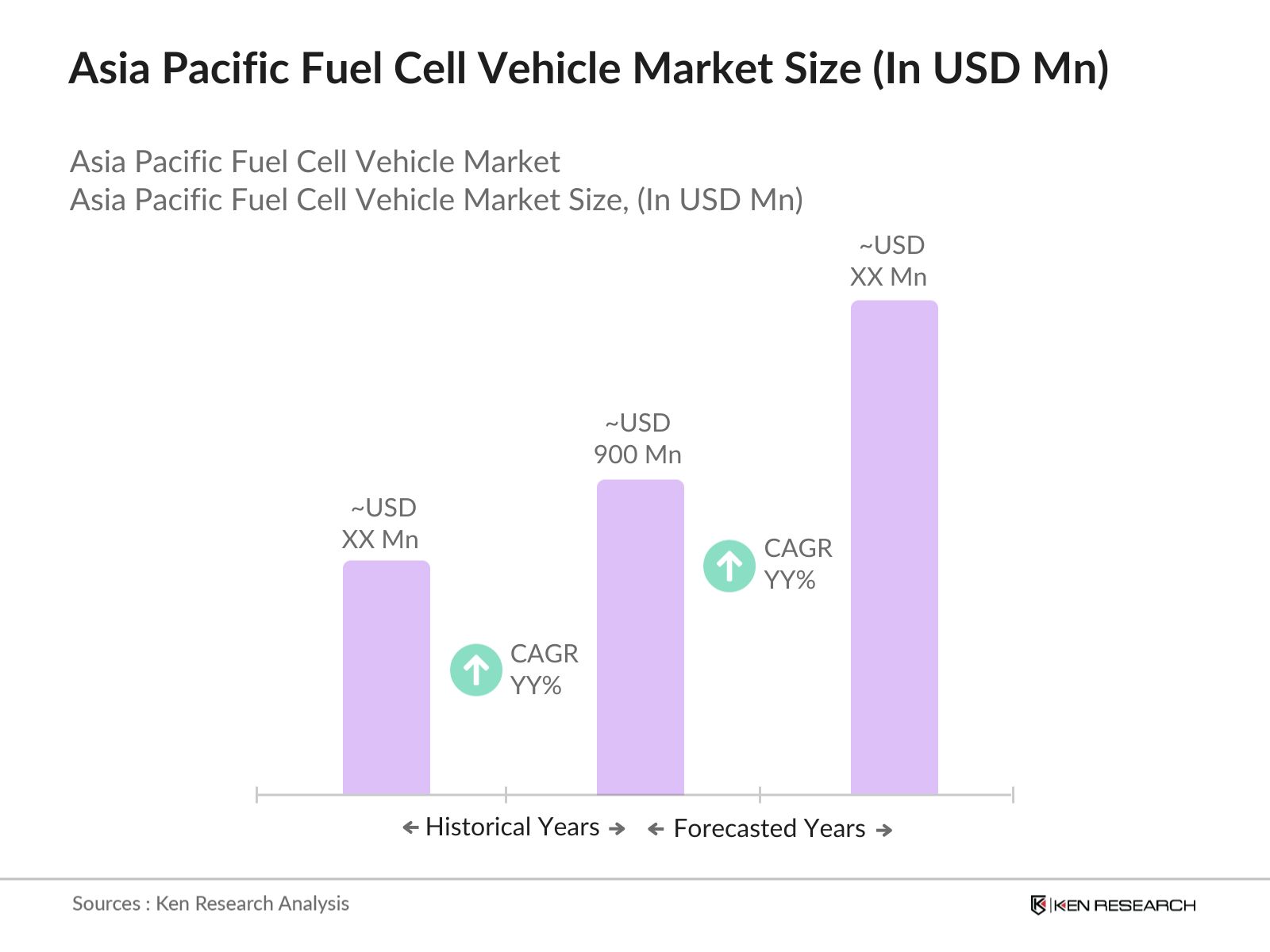

- The Asia Pacific fuel cell vehicle (FCV) market, valued at USD 900 million, has shown robust growth driven by increasing government support, stringent emission regulations, and advancements in hydrogen infrastructure. Nations across the region are making significant investments to promote hydrogen as a clean fuel alternative, with Japan, South Korea, and China at the forefront, pushing for zero-emission solutions in the transportation sector.

- In Asia Pacific, Japan, China, and South Korea lead the market. Japan and South Korea benefit from strong government backing, tax incentives, and a well-established hydrogen infrastructure. China, the largest automotive market, has rapidly advanced hydrogen-powered transportation with significant government subsidies and plans to build extensive refueling networks.

- Japans 2024 roadmap allocated JPY 2 trillion (USD 14.1 billion) for hydrogen development, including fuel cell technology. The roadmap aims for 800,000 FCVs on the road by 2030, supporting the automotive sector through policy and financial incentives.

Asia Pacific Fuel Cell Vehicle Market Segmentation

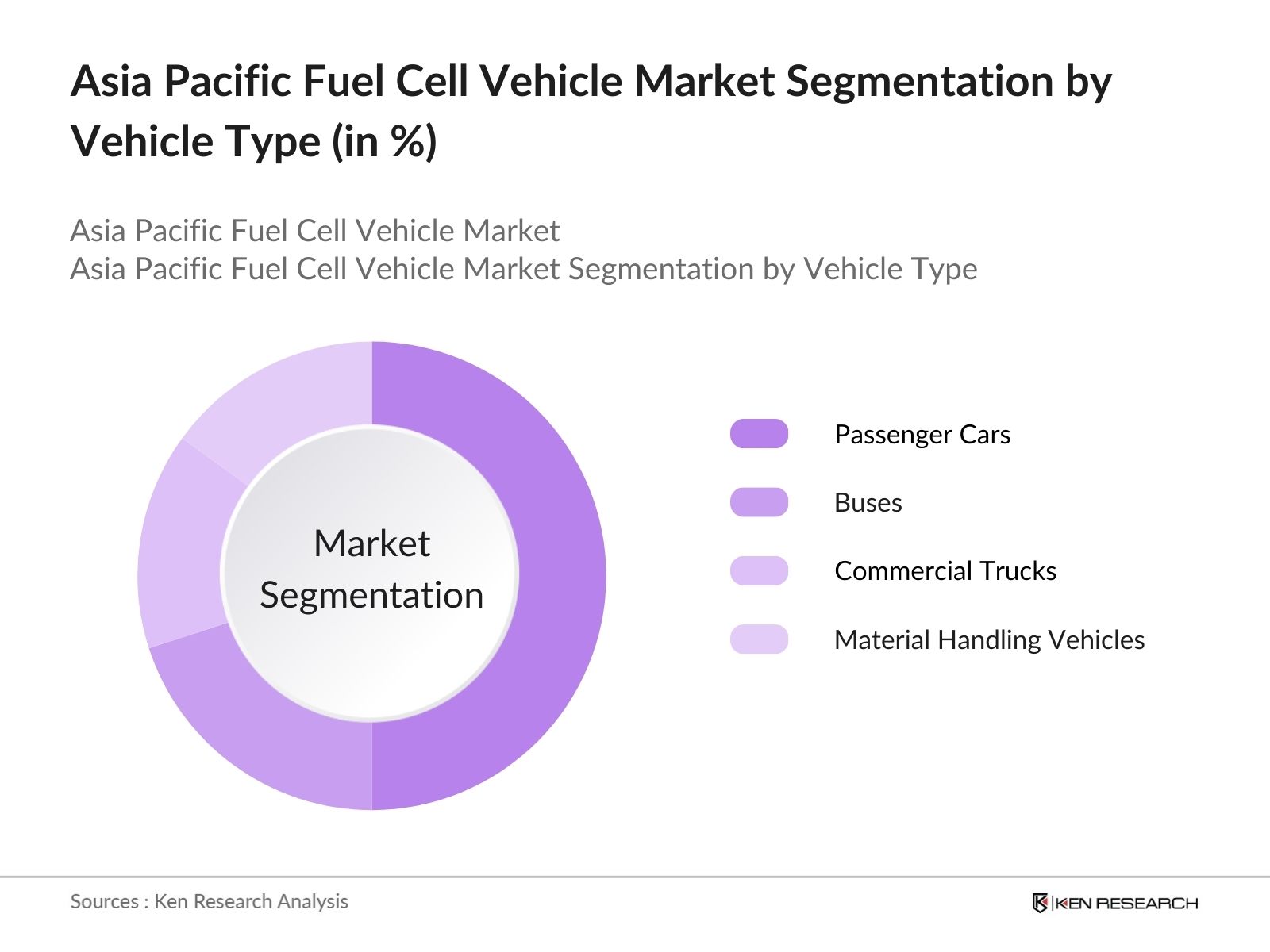

By Vehicle Type: The market is segmented by vehicle type into passenger cars, buses, commercial trucks, and material handling vehicles. Recently, passenger cars have claimed the dominant market share under vehicle type due to rising consumer interest in sustainable personal transportation and advancements in fuel cell technology making it more accessible for everyday use. Japanese brands, like Toyota and Honda, have been pioneers in producing fuel cell passenger cars, contributing to the segments strong position in the market.

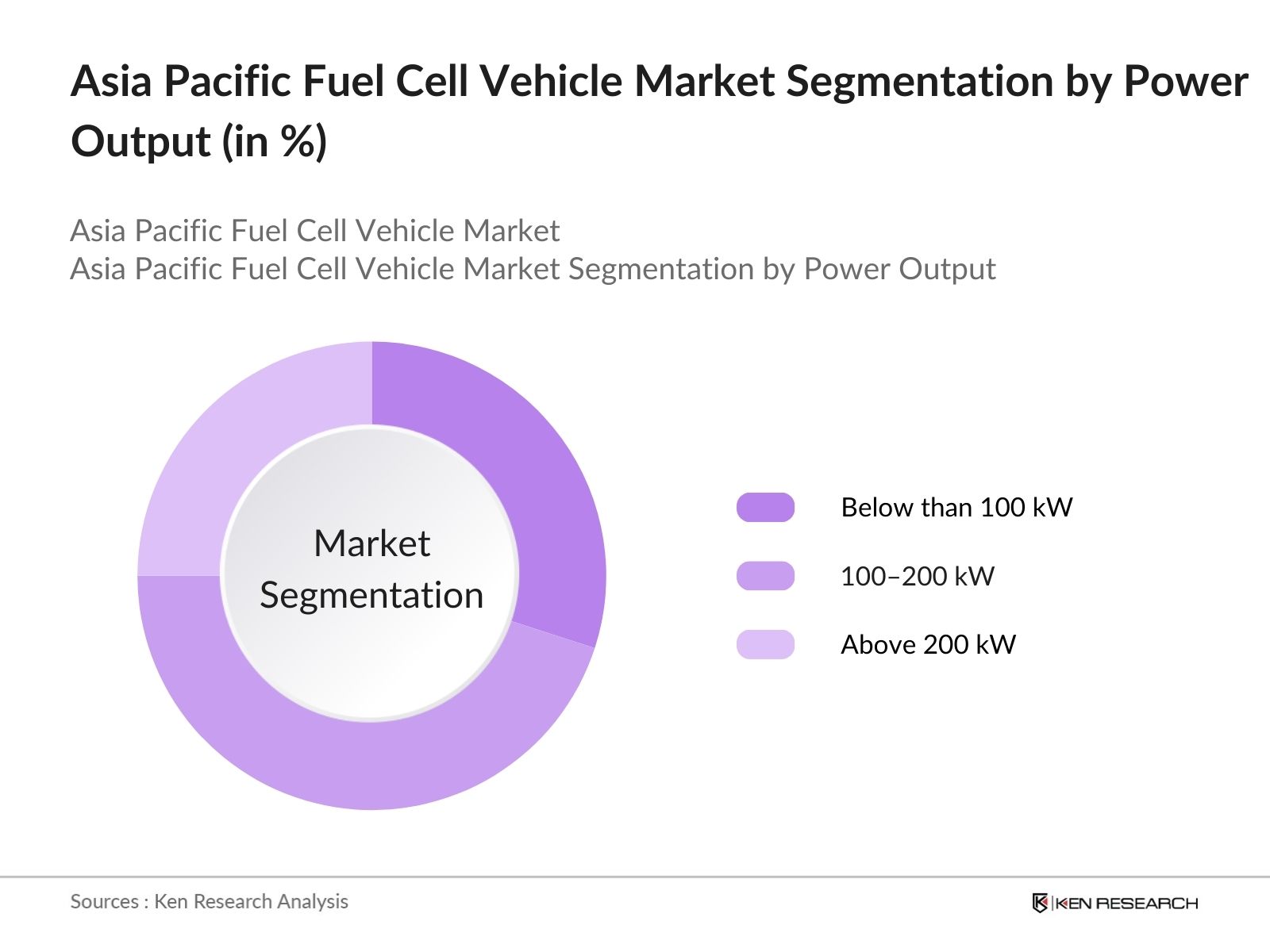

By Power Output: The market is also segmented by power output into below 100 kW, 100-200 kW, and above 200 kW. The 100-200 kW segment holds a leading market share due to its suitability for both passenger and commercial vehicles. This range meets the power needs of most fuel cell passenger vehicles and urban buses, making it versatile and practical for mass adoption. The 100-200 kW power output also aligns well with current infrastructure capabilities, making it highly marketable.

Asia Pacific Fuel Cell Vehicle Market Competitive Landscape

The market is dominated by a few major players, including Toyota, Hyundai, and Honda, which have spearheaded the development of hydrogen-powered vehicles in the region. These brands leverage their established manufacturing infrastructure, research capabilities, and government support to strengthen their market position.

Asia Pacific Fuel Cell Vehicle Market Analysis

Market Growth Drivers

- Government Subsidies and Funding Support: In 2024, Japan allocated approximately JPY 200 billion towards hydrogen and fuel cell technology initiatives, including vehicle infrastructure development. This funding aims to boost fuel cell vehicle (FCV) adoption through tax incentives and purchase rebates. Similarly, China announced RMB 8 billion in subsidies to support FCV manufacturers, creating robust demand.

- Expansion of Hydrogen Refueling Infrastructure: Japan's Ministry of Economy, Trade and Industry (METI) has set a target to increase the number of hydrogen refueling stations to 320 by 2025, compared to the existing 160 stations in 2024. South Korea also aims to install over 310 hydrogen stations by 2025, investing approximately KRW 500 billion. This infrastructure expansion is expected to facilitate wider adoption of FCVs.

- Energy Security and Environmental Mandates: As part of energy diversification efforts, South Korea imported 6.7 million metric tons of hydrogen in 2024. By transitioning to domestically-produced green hydrogen for FCVs, the government aims to cut down on crude oil imports by about 4 million barrels annually. Australia has also launched initiatives to harness hydrogen as a fuel source, projecting it could reduce greenhouse gas emissions by 35 million metric tons by 2028.

Market Challenges

- High Production Costs of Fuel Cells: FCVs cost around 30-40% more than conventional vehicles due to the high price of platinum required in fuel cell manufacturing. In 2024, platinum prices averaged around $950 per ounce, leading to higher component costs that limit FCV affordability and widespread adoption.

- Limited Hydrogen Supply Chain: Japans hydrogen supply capacity stands at 1.2 million metric tons in 2024, barely sufficient to meet projected demand. South Korea also reported a hydrogen shortfall of around 500,000 metric tons. Establishing reliable production and distribution channels is critical to supporting the regional FCV market.

Asia Pacific Fuel Cell Vehicle Market Future Outlook

Over the next five years, the Asia Pacific fuel cell vehicle industry is anticipated to experience substantial growth, driven by continuous government incentives, increasing investment in hydrogen refueling infrastructure, and growing consumer demand for zero-emission vehicles.

Future Market Opportunities

- Expansion of Green Hydrogen Production Facilities: Japan and Australia are projected to increase their hydrogen production capacity by 10 million metric tons by 2028. This growth will reduce reliance on imported hydrogen, ensuring a stable supply chain for FCV markets and enabling more consistent production.

- Government-Mandated Emission Reduction Goals: South Korea plans to mandate emission reduction targets across its automotive industry, aiming to decrease fossil-fuel-powered vehicle sales by 40% by 2029. This policy shift is expected to propel the adoption of FCVs as cleaner alternatives.

Scope of the Report

|

Vehicle Type |

Passenger Cars |

|

Power Output |

Below 100 kW |

|

Fuel Type |

Hydrogen Fuel Cells |

|

Technology |

Proton Exchange Membrane Fuel Cells (PEMFC) |

|

Region |

China |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Fuel Cell Vehicle Manufacturers

Hydrogen Fuel Suppliers

Automotive Component Suppliers

Infrastructure Developers

Government and Regulatory Bodies (e.g., Ministry of Transport, Department of Energy)

Research and Development Institutions

Investor and Venture Capitalist Firms

Environmental Policy Makers

Companies

Players Mentioned in the Report:

Toyota Motor Corporation

Hyundai Motor Company

Honda Motor Co., Ltd.

Ballard Power Systems

Plug Power Inc.

Nikola Corporation

General Motors

Bosch Mobility Solutions

Bloom Energy

Daimler AG

Table of Contents

1. Asia Pacific Fuel Cell Vehicle Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics Overview (Market Demand Drivers, Technological Advancements)

1.4. Market Segmentation Overview

2. Asia Pacific Fuel Cell Vehicle Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Government Policies, Technology Innovations, Milestone Adoptions)

3. Asia Pacific Fuel Cell Vehicle Market Analysis

3.1. Growth Drivers

3.1.1. Emissions Regulations

3.1.2. Technological Advancements in Hydrogen Fuel Cells

3.1.3. Rising Investments in Green Mobility

3.1.4. Government Incentives and Subsidies

3.2. Market Challenges

3.2.1. High Production and Maintenance Costs

3.2.2. Limited Hydrogen Refueling Infrastructure

3.2.3. Competition from Battery Electric Vehicles (BEVs)

3.2.4. Consumer Awareness and Acceptance

3.3. Opportunities

3.3.1. Expansion in Emerging Markets

3.3.2. Increasing Collaborations for Infrastructure Development

3.3.3. Potential for Fuel Cell Integration in Heavy-Duty Vehicles

3.3.4. Enhanced Hydrogen Storage Solutions

3.4. Trends

3.4.1. Development of Compact Fuel Cells

3.4.2. Rise of Fuel Cell Vehicles in Public Transportation

3.4.3. Growing Focus on Hybrid Fuel Cell Systems

3.4.4. Increasing Adoption of Zero Emission Technologies

3.5. Government Regulations

3.5.1. Emission Reduction Targets

3.5.2. Safety Standards for Fuel Cell Vehicles

3.5.3. Hydrogen Infrastructure Policies

3.5.4. National and Regional Initiatives

3.6. Competitive Landscape

3.7. Porter’s Five Forces Analysis

3.8. Stakeholder Ecosystem Analysis

4. Asia Pacific Fuel Cell Vehicle Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Cars

4.1.2. Buses

4.1.3. Commercial Trucks

4.1.4. Material Handling Vehicles

4.2. By Power Output (In Value %)

4.2.1. Below 100 kW

4.2.2. 100-200 kW

4.2.3. Above 200 kW

4.3. By Fuel Type (In Value %)

4.3.1. Hydrogen Fuel Cells

4.3.2. Methanol Fuel Cells

4.4. By Technology (In Value %)

4.4.1. Proton Exchange Membrane Fuel Cells (PEMFC)

4.4.2. Solid Oxide Fuel Cells (SOFC)

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Australia

4.5.5. Southeast Asia

5. Asia Pacific Fuel Cell Vehicle Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Toyota Motor Corporation

5.1.2. Hyundai Motor Company

5.1.3. Honda Motor Co., Ltd.

5.1.4. Daimler AG

5.1.5. Nissan Motor Corporation

5.1.6. Ballard Power Systems

5.1.7. Cummins Inc.

5.1.8. Plug Power Inc.

5.1.9. Nikola Corporation

5.1.10. General Motors (GM)

5.1.11. Audi AG

5.1.12. BMW AG

5.1.13. Bosch Mobility Solutions

5.1.14. Bloom Energy

5.1.15. FAW Group

5.2. Cross Comparison Parameters (Market Position, Product Portfolio, Regional Presence, Revenue Streams, Technological Partnerships, R&D Investments, Production Capacity, Strategic Collaborations)

5.3. Market Share Analysis

5.4. Strategic Initiatives and Innovations

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Joint Ventures and Collaborations

5.8. Government Incentives

5.9. Private and Public Funding Analysis

6. Asia Pacific Fuel Cell Vehicle Market Regulatory Framework

6.1. Hydrogen Fuel Standards and Regulations

6.2. Vehicle Safety Standards

6.3. Environmental Compliance

6.4. Certification Processes

7. Asia Pacific Fuel Cell Vehicle Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Growth Drivers

8. Asia Pacific Fuel Cell Vehicle Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Power Output (In Value %)

8.3. By Fuel Type (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Fuel Cell Vehicle Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Market Entry Strategies

9.3. Key Distribution Channels

9.4. Identifying White Space Opportunities

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial step involves building a comprehensive ecosystem map encompassing the primary stakeholders within the Asia Pacific fuel cell vehicle market. Through rigorous desk research, both proprietary and public databases are used to gather essential industry-level data, aiming to outline the core variables that affect market dynamics.

Step 2: Market Analysis and Construction

This stage compiles historical data on the Asia Pacific fuel cell vehicle market, analyzing key metrics such as market penetration, adoption rates, and revenue streams across different regions. Additionally, fuel cell technology adoption in heavy-duty versus passenger segments is assessed to provide reliable revenue projections.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses developed during the initial stages are validated through consultations with industry experts, conducted via structured interviews. Feedback from fuel cell vehicle manufacturers and hydrogen infrastructure developers helps refine and corroborate data accuracy.

Step 4: Research Synthesis and Final Output

The final phase consolidates data obtained through interactions with stakeholders, validating market segmentation and analyzing consumer behavior trends. This ensures a comprehensive, validated analysis for the Asia Pacific fuel cell vehicle market.

Frequently Asked Questions

01. How big is the Asia Pacific Fuel Cell Vehicle Market?

The Asia Pacific fuel cell vehicle market is valued at USD 900 million, driven by strong government support, emission regulations, and advancements in hydrogen refueling infrastructure.

02. What are the challenges in the Asia Pacific Fuel Cell Vehicle Market?

Challenges in the Asia Pacific fuel cell vehicle market include high production costs, limited hydrogen refueling stations, competition from electric vehicles, and the need for increased consumer awareness about hydrogen technology.

03. Who are the major players in the Asia Pacific Fuel Cell Vehicle Market?

Key players in the Asia Pacific fuel cell vehicle market include Toyota, Hyundai, Honda, Ballard Power Systems, and Plug Power, which dominate through extensive R&D investment, strategic partnerships, and a strong focus on hydrogen infrastructure.

04. What are the growth drivers of the Asia Pacific Fuel Cell Vehicle Market?

Growth in the Asia Pacific fuel cell vehicle market is driven by favorable government policies, advancements in hydrogen fuel cell technology, and an increasing focus on sustainable transportation solutions, especially in Japan, South Korea, and China.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.