Asia Pacific Lithium-Ion Battery Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD4342

October 2024

96

About the Report

Asia Pacific Lithium- Ion Battery Market Overview

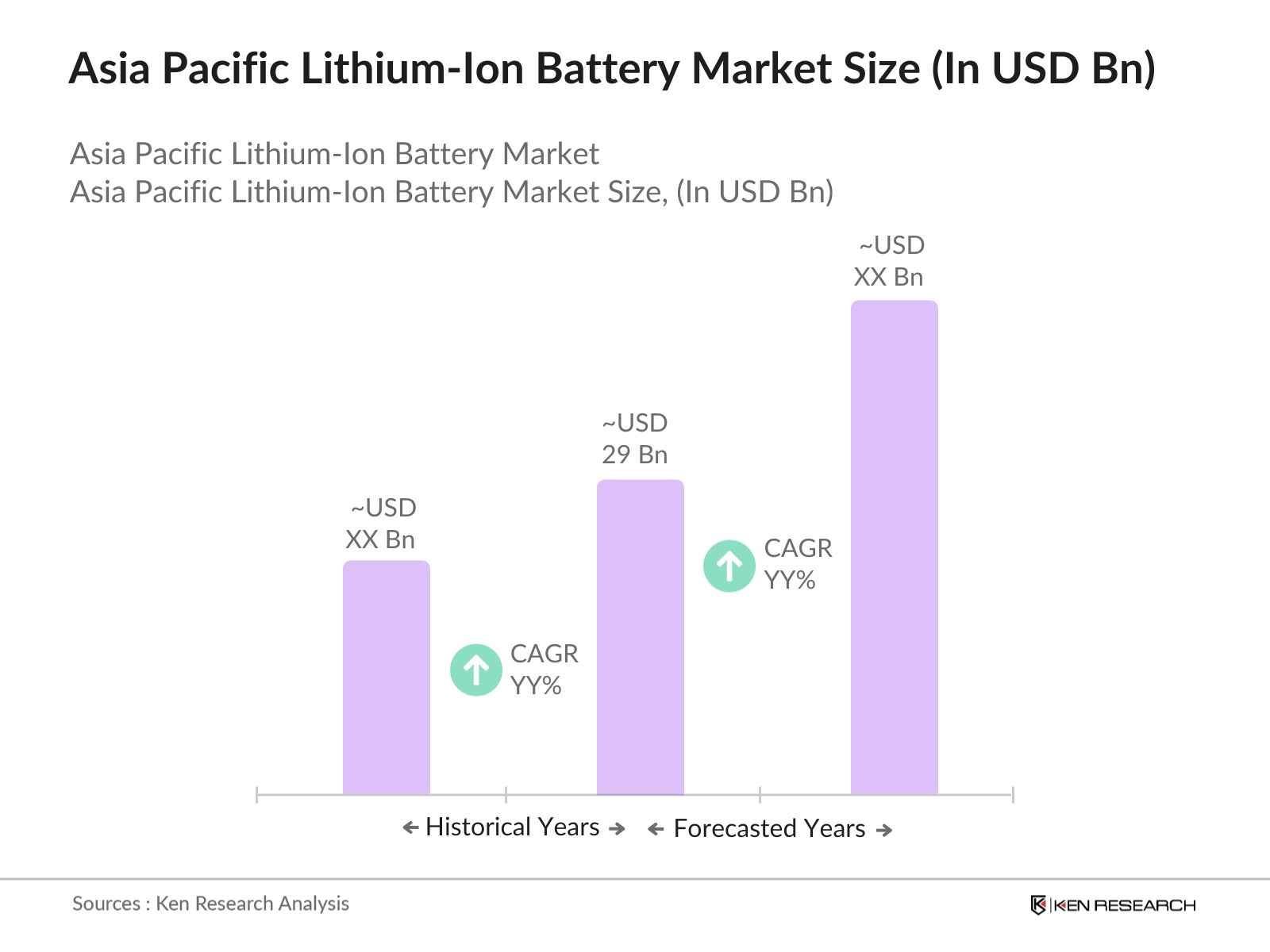

- The Asia Pacific lithium-ion battery market is valued at USD 29 billion based on a five-year historical analysis. This market size is primarily driven by the exponential demand for electric vehicles (EVs) and the increasing need for energy storage solutions in both renewable energy and consumer electronics sectors. The region's technological advancements in battery performance, including improvements in energy density and efficiency, have further fueled market growth.

- China, Japan, and South Korea dominate the market due to their leadership in battery manufacturing, research and development, and advanced supply chain management. Chinas dominance is bolstered by its vast EV production and raw material access, while Japan and South Korea benefit from strong technological expertise and established brands such as Panasonic and LG Energy Solution.

- Chinas government has aggressively supported the growth of the market through its National New Energy Vehicle (NEV) program. By 2024, the program had helped increase the number of EVs to over 7 million on Chinese roads. Additionally, the government has invested in subsidies and grants to promote the development of local battery manufacturers and create a self-sufficient lithium-ion battery supply chain.

Asia Pacific Lithium-Ion Battery Market Segmentation

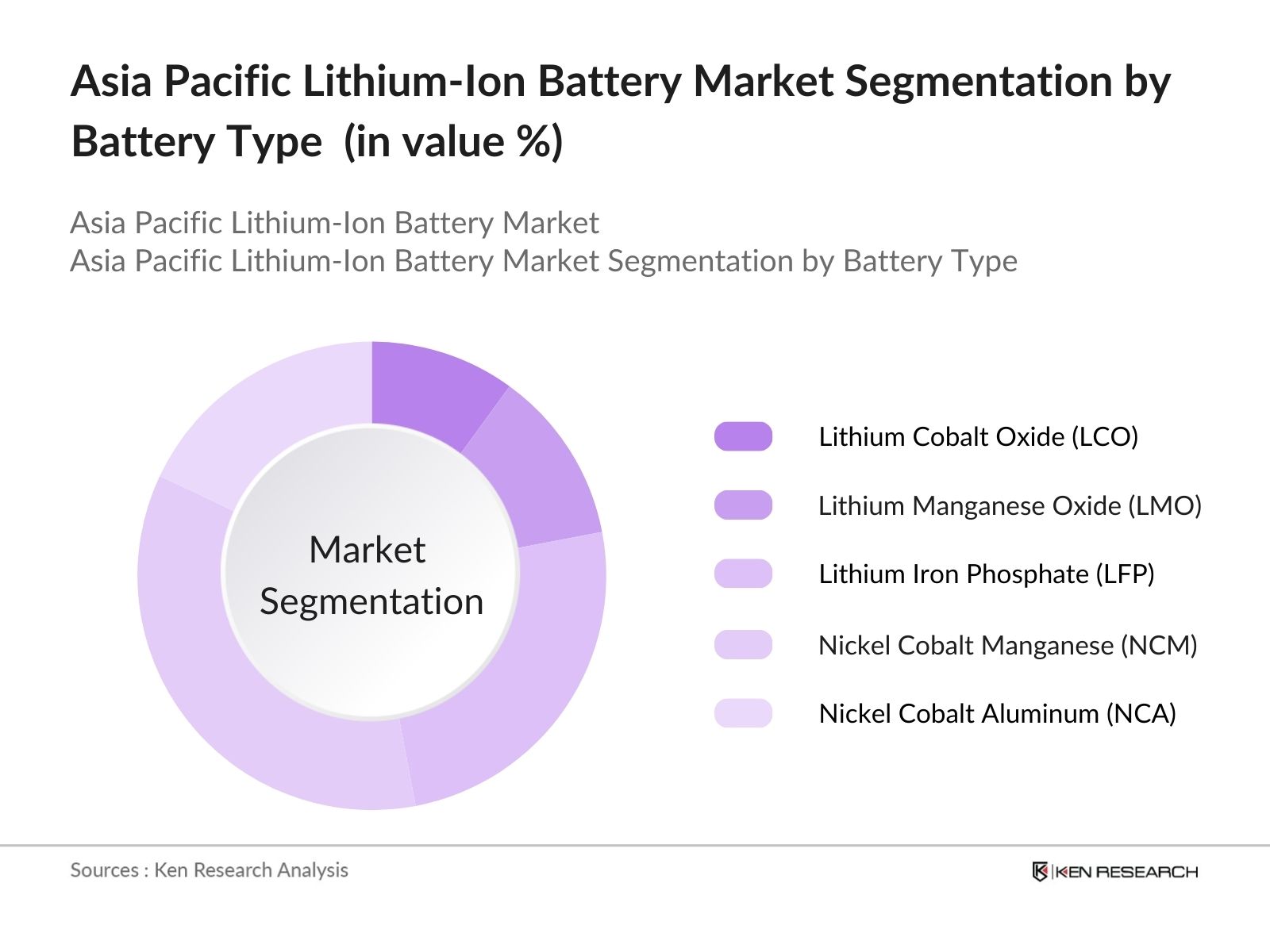

By Battery Type: The market is segmented by battery type into Lithium Cobalt Oxide (LCO), Lithium Manganese Oxide (LMO), Lithium Iron Phosphate (LFP), Nickel Cobalt Manganese (NCM), and Nickel Cobalt Aluminum (NCA). Nickel Cobalt Manganese (NCM) batteries have gained a dominant market share under the segmentation by battery type. This is due to their balanced performance in terms of energy density, cost-effectiveness, and durability. NCM batteries are widely used in electric vehicles and energy storage systems, as they provide an ideal balance between range and charging time, making them popular for use in consumer electronics and high-performance EVs.

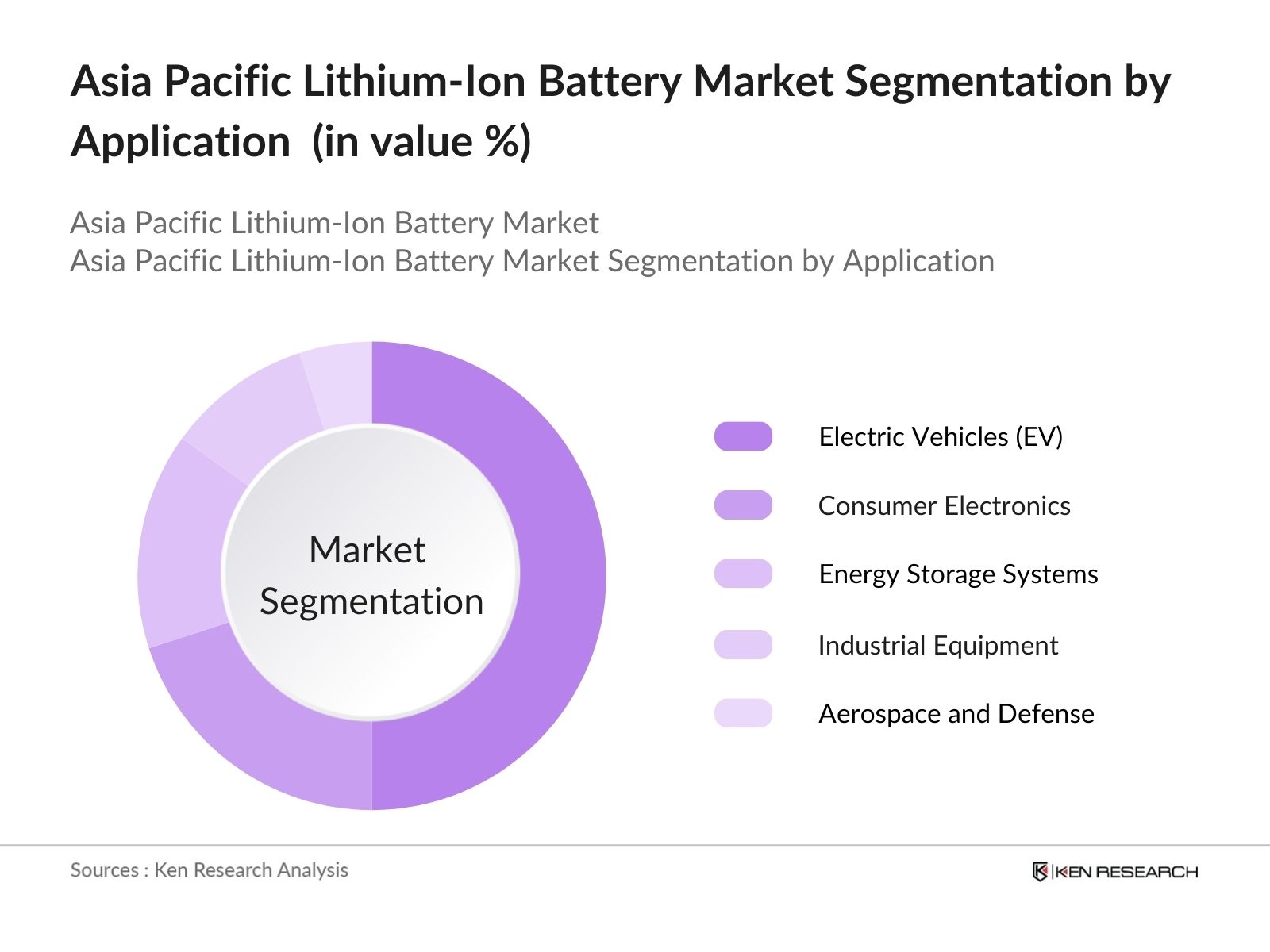

By Application: The market is further segmented by application into Electric Vehicles, Consumer Electronics, Energy Storage Systems, Industrial Equipment, and Aerospace and Defense. The Electric Vehicles (EV) sub-segment holds the largest share in the market under the application segmentation. This dominance is attributed to the rapid electrification of the automotive sector across the Asia Pacific region, especially in China and India. Government mandates for reducing CO2 emissions, coupled with generous EV subsidies, have accelerated the adoption of lithium-ion batteries in the transportation sector.

Asia Pacific Lithium-Ion Battery Market Competitive Landscape

The market is dominated by several key players with a influence over the markets supply chain, technological innovation, and raw material sourcing. These players range from global giants to regional manufacturers who have heavily invested in R&D and large-scale battery production facilities.

|

Company Name |

Establishment Year |

Headquarters |

Battery Technology Innovation |

Global Production Capacity |

Raw Material Sourcing |

EV Market Penetration |

Manufacturing Costs |

R&D Investments |

|

Panasonic Corporation |

1918 |

Osaka, Japan |

||||||

|

LG Energy Solution |

1947 |

Seoul, South Korea |

||||||

|

Contemporary Amperex Technology Co. |

2011 |

Ningde, China |

||||||

|

BYD Co., Ltd. |

1995 |

Shenzhen, China |

||||||

|

Samsung SDI |

1970 |

Seoul, South Korea |

Asia Pacific Lithium-ion Battery Market Analysis

Market Growth Drivers

- Electric Vehicle (EV) Adoption Surge: The rise in electric vehicle (EV) adoption across Asia-Pacific is a major driver for the market. In 2024, China alone registered over 7 million electric cars, and countries like India and Japan are seeing rapid growth in EV sales. The Asia-Pacific region is a global hub for EV production, with companies like BYD and Tesla manufacturing large volumes of electric vehicles. This surge is increasing demand for lithium-ion batteries, with EVs accounting for a significant portion of battery consumption in the region.

- Renewable Energy Integration: Governments across Asia-Pacific are promoting renewable energy sources such as solar and wind power, driving the demand for energy storage solutions. India's renewable energy sector is experiencing rapid growth, with a record16.4 GWof capacity added in the first seven months of 2024. The country aims for500 GWof non-fossil fuel capacity by 2030, necessitating annual additions of50 GWto meet this target. The adoption of energy storage technologies in off-grid and rural areas is further accelerating the market growth.

- Growing Consumer Electronics Market: Asia-Pacifics rapidly expanding consumer electronics market is a significant growth driver for lithium-ion batteries. In 2024, smartphones, tablets, and laptops were shipped across the region, with China, South Korea, and India being the largest producers. These devices require high-performance and long-lasting battery solutions, further boosting the demand for lithium-ion batteries. Additionally, the rise in smart appliances and personal electronic devices is increasing the demand for compact, efficient batteries, especially in high-density urban areas.

Market Challenges

- Limited Infrastructure for Charging Stations: The lack of adequate infrastructure for EV charging stations in the Asia-Pacific region is hindering the growth of the lithium-ion battery market. India, for example, had fewer than 15,000 public charging stations in 2024, a shortfall compared to the rapidly increasing number of EVs on the road. Similarly, in Southeast Asia, the absence of standardized charging networks has slowed the adoption of electric vehicles and, consequently, the demand for lithium-ion batteries.

- Environmental Concerns and Recycling Issues: Lithium-ion batteries pose environmental challenges due to the toxic materials used in their production and disposal. In 2024, the region generated over 500,000 metric tons of lithium-ion battery waste, primarily from discarded electronics and electric vehicle batteries. The lack of effective recycling infrastructure has led to environmental concerns and increased pressure on governments to introduce stricter regulations.

Asia Pacific Lithium-Ion Battery Market Future Outlook

Over the next five years, the Asia Pacific lithium-ion battery industry is expected to witness growth driven by the rapid expansion of the electric vehicle sector, increasing investments in renewable energy storage, and ongoing advancements in battery technologies.

Future Market Opportunities

- Advancements in Solid-State Batteries: Over the next five years, solid-state batteries will likely replace traditional lithium-ion batteries in certain applications, due to their higher energy density, enhanced safety features, and faster charging capabilities. By 2028, major manufacturers such as Panasonic and Toyota are expected to mass-produce these batteries, with Japan and South Korea leading the technological advancements in this field. This shift will enable longer-range electric vehicles and improve energy storage efficiency for renewable energy projects.

- Increase in Battery Recycling Initiatives: By 2028, Asia-Pacific will see a rise in battery recycling initiatives to address environmental concerns and raw material shortages. Countries like China and South Korea are expected to introduce stricter regulations on battery waste management, coupled with incentives for recycling companies. The lithium-ion battery recycling market is anticipated to grow rapidly, with new facilities being established in key regions, including Australia and India, to recover valuable materials from used batteries.

Scope of the Report

|

Battery Type |

Lithium Cobalt Oxide (LCO) Lithium Manganese Oxide (LMO) Lithium Iron Phosphate (LFP) Nickel Cobalt Manganese (NCM) Nickel Cobalt Aluminum (NCA) |

|

Application |

Electric Vehicles Consumer Electronics Energy Storage Systems Industrial Equipment Aerospace and Defense |

|

Capacity |

Less than 10 kWh 10-50 kWh 50-100 kWh More than 100 kWh |

|

Power Density |

Less than 150 Wh/kg 150-200 Wh/kg 200-300 Wh/kg More than 300 Wh/kg |

|

Region |

China Japan South Korea India Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Electric Vehicle Manufacturers

Renewable Energy Companies

Battery Manufacturers

Energy Storage Solution Providers

Government and Regulatory Bodies (Ministry of New and Renewable Energy, National Development and Reform Commission - China)

Investments and Venture Capitalist Firms

Transportation and Logistics Providers

Companies

Players Mentioned in the Report:

Panasonic Corporation

LG Energy Solution

Contemporary Amperex Technology Co. (CATL)

BYD Co., Ltd.

Samsung SDI

SK Innovation Co., Ltd.

Toshiba Corporation

Envision AESC Group

GS Yuasa Corporation

EVE Energy Co., Ltd.

Farasis Energy

A123 Systems LLC

Sila Nanotechnologies

Amperex Technology Limited (ATL)

Leclanch SA

Table of Contents

1. Asia Pacific Lithium-Ion Battery Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Lithium-Ion Battery Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Lithium-Ion Battery Market Analysis

3.1. Growth Drivers

3.1.1. Electric Vehicle Adoption (EV Demand, EV Penetration, EV Infrastructure Development)

3.1.2. Renewable Energy Integration (Energy Storage Demand, Grid Modernization)

3.1.3. Government Incentives and Policies (Subsidies, Emission Norms)

3.1.4. Consumer Electronics Growth (Mobile Devices, Portable Power Banks)

3.2. Market Challenges

3.2.1. High Raw Material Prices (Lithium, Cobalt)

3.2.2. Recycling Challenges (End-of-Life Battery Management)

3.2.3. Supply Chain Constraints (Raw Material Sourcing, Logistics)

3.3. Opportunities

3.3.1. Technological Advancements (Solid-State Batteries, Fast Charging Technology)

3.3.2. Expansion in Industrial Energy Storage (Commercial and Residential Solutions)

3.3.3. Cross-Sector Collaborations (Energy Sector, EV OEMs, and Battery Producers)

3.4. Trends

3.4.1. Focus on Battery Energy Density (Improved Energy-to-Weight Ratio)

3.4.2. Development of Second-Life Batteries (Repurposing Used Batteries)

3.4.3. Investments in Battery Manufacturing (Gigafactories, Domestic Production Initiatives)

3.5. Government Regulation

3.5.1. Regional Battery Manufacturing Policies (Asia Pacific Domestic Policies)

3.5.2. Emission Control Regulations (EV Incentive Schemes)

3.5.3. Renewable Energy Mandates (Energy Storage Targets, Grid Requirements)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Asia Pacific Lithium-Ion Battery Market Segmentation

4.1. By Battery Type (In Value %)

4.1.1. Lithium Cobalt Oxide (LCO)

4.1.2. Lithium Manganese Oxide (LMO)

4.1.3. Lithium Iron Phosphate (LFP)

4.1.4. Nickel Cobalt Manganese (NCM)

4.1.5. Nickel Cobalt Aluminum (NCA)

4.2. By Application (In Value %)

4.2.1. Electric Vehicles

4.2.2. Consumer Electronics

4.2.3. Energy Storage Systems

4.2.4. Industrial Equipment

4.2.5. Aerospace and Defense

4.3. By Capacity (In Value %)

4.3.1. Less than 10 kWh

4.3.2. 10-50 kWh

4.3.3. 50-100 kWh

4.3.4. More than 100 kWh

4.4. By Power Density (In Value %)

4.4.1. Less than 150 Wh/kg

4.4.2. 150-200 Wh/kg

4.4.3. 200-300 Wh/kg

4.4.4. More than 300 Wh/kg

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Rest of APAC

5. Asia Pacific Lithium-Ion Battery Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Panasonic Corporation

5.1.2. LG Energy Solution

5.1.3. Contemporary Amperex Technology Co., Limited (CATL)

5.1.4. BYD Co., Ltd.

5.1.5. Samsung SDI Co., Ltd.

5.1.6. SK Innovation Co., Ltd.

5.1.7. Toshiba Corporation

5.1.8. Envision AESC Group

5.1.9. A123 Systems LLC

5.1.10. GS Yuasa Corporation

5.1.11. EVE Energy Co., Ltd.

5.1.12. Farasis Energy

5.1.13. Sila Nanotechnologies

5.1.14. Amperex Technology Limited (ATL)

5.1.15. Leclanch SA

5.2 Cross Comparison Parameters

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Asia Pacific Lithium-Ion Battery Market Regulatory Framework

6.1 Battery Disposal and Recycling Standards

6.2 Safety Regulations (Transport, Usage)

6.3 Environmental Regulations (CO2 Emissions, Waste Management)

6.4 Certification Requirements (ISO, IEC Standards)

7. Asia Pacific Lithium-Ion Battery Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Lithium-Ion Battery Future Market Segmentation

8.1. By Battery Type (In Value %)

8.2. By Application (In Value %)

8.3. By Capacity (In Value %)

8.4. By Power Density (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Lithium-Ion Battery Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In the initial phase, we constructed an ecosystem map of the Asia Pacific lithium-ion battery market, identifying key stakeholders such as battery manufacturers, raw material suppliers, and government regulatory bodies. Desk research was conducted using secondary and proprietary databases to gather industry-level information.

Step 2: Market Analysis and Construction

The historical data analysis phase involved compiling market penetration and revenue generation data for different product types and applications. Furthermore, insights into the supply chain and raw material pricing trends were evaluated.

Step 3: Hypothesis Validation and Expert Consultation

Through computer-assisted telephone interviews (CATIs) with industry experts from major companies, key market assumptions were validated. This process included insights from battery technology researchers, EV manufacturers, and material suppliers.

Step 4: Research Synthesis and Final Output

The final step included direct interaction with battery manufacturers to gather granular insights into production capacity, sales performance, and R&D investments. This comprehensive data was synthesized to provide a validated and accurate market analysis.

Frequently Asked Questions

01. How big is the Asia Pacific Lithium-Ion Battery Market?

The Asia Pacific lithium-ion battery market is valued at USD 29 billion, driven by the widespread adoption of electric vehicles and renewable energy storage solutions across key countries like China, Japan, and South Korea.

02. What are the challenges in the Asia Pacific Lithium-Ion Battery Market?

The primary challenges in the Asia Pacific lithium-ion battery market include rising raw material costs (particularly for lithium and cobalt), the need for sustainable recycling solutions, and the pressure to innovate within a highly competitive landscape.

03. Who are the major players in the Asia Pacific Lithium-Ion Battery Market?

Key players in the Asia Pacific lithium-ion battery market include Panasonic, LG Energy Solution, CATL, BYD, and Samsung SDI. These companies are dominant due to their advanced battery technology, strong production capacities, and strategic alliances with automotive and energy companies.

04. What are the growth drivers of the Asia Pacific Lithium-Ion Battery Market?

Growth in the Asia Pacific lithium-ion battery market is primarily driven by increasing electric vehicle adoption, government regulations promoting battery recycling and sustainability, and advancements in battery energy density and efficiency.

05. What is the future of the Asia Pacific Lithium-Ion Battery Market?

The Asia Pacific lithium-ion battery market is expected to witness growth, particularly in electric vehicles and renewable energy storage applications, driven by government incentives and ongoing technological advancements in solid-state battery technology.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.