Asia Pacific Lithium Iron Phosphate Battery Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD3887

December 2024

94

About the Report

Asia Pacific Lithium Iron Phosphate Battery Market Overview

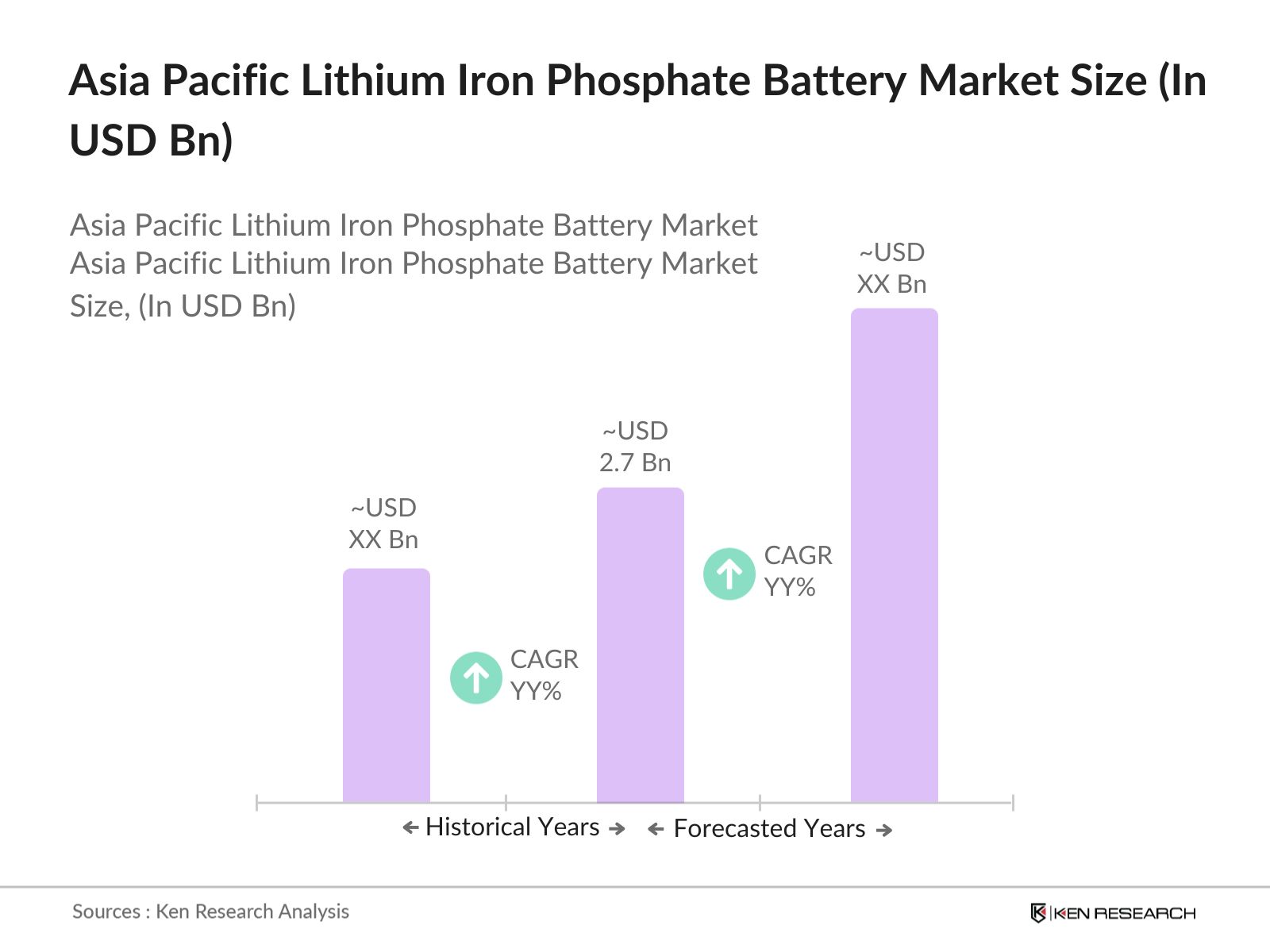

- The Asia Pacific Lithium Iron Phosphate Battery market is valued at USD 2.7 billion, driven primarily by the surging demand in the electric vehicle (EV) sector, energy storage systems, and industrial applications. Key factors such as technological advancements, cost-effectiveness, and the stable chemistry of LFP batteries compared to other lithium-ion chemistries have bolstered their adoption.

- China and Japan dominate the market, leveraging their advanced battery manufacturing ecosystems and the significant government backing for EV and energy storage initiatives. Chinas substantial investments in domestic EVs and its leading position in renewable energy production create a strong demand for LFP batteries, while Japans focus on industrial and renewable energy storage solutions further cements its position as a market leader.

- The Chinese government has mandated battery recycling regulations, allocating 1 billion in 2024 to encourage LFP recycling projects. These policies are set to improve the environmental sustainability of battery production, lowering costs for raw material imports by promoting the use of recycled materials.

Asia Pacific Lithium Iron Phosphate Battery Market Segmentation

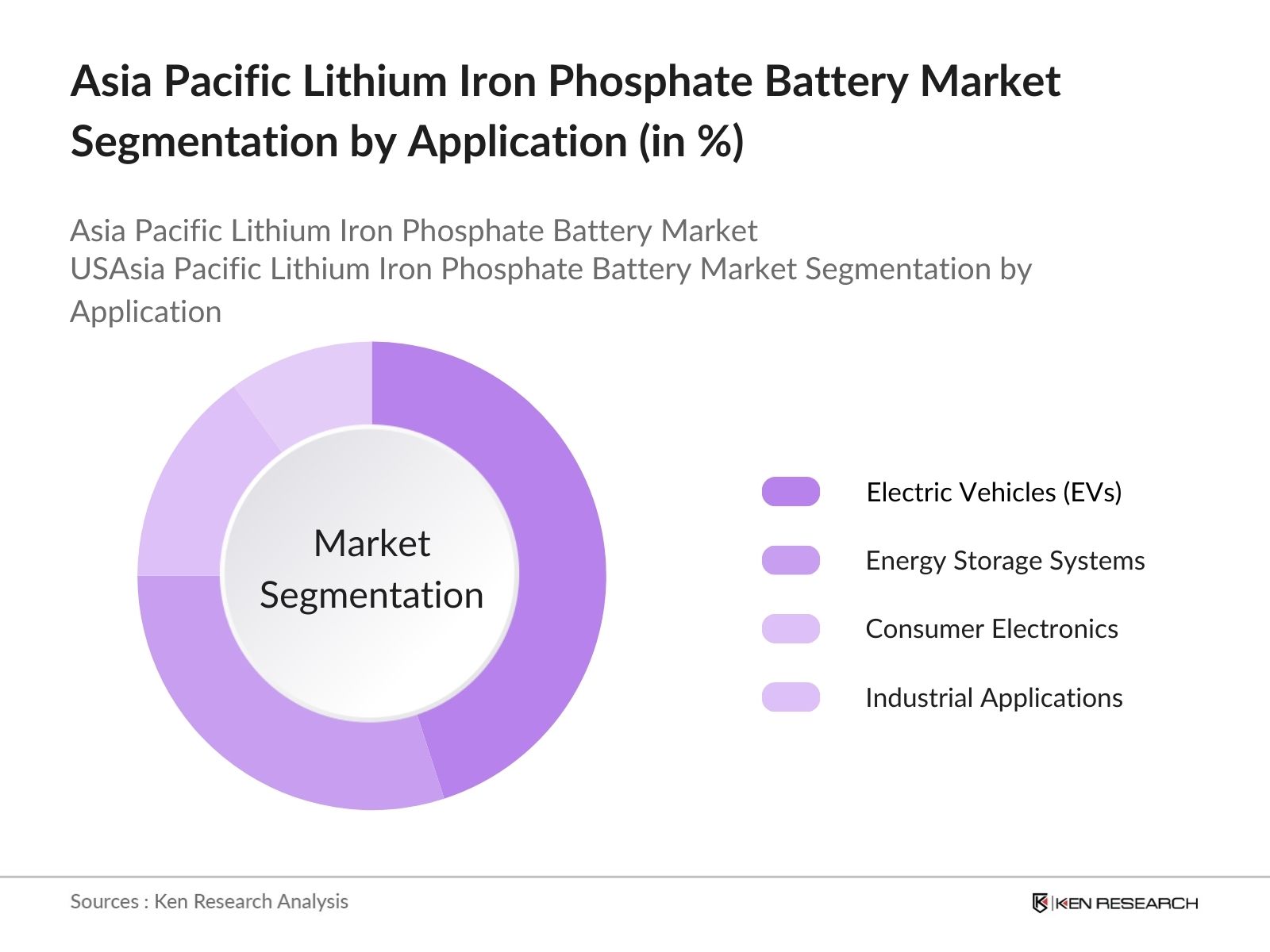

By Application: The market is segmented by application into Electric Vehicles (EVs), Energy Storage Systems (ESS), Consumer Electronics, and Industrial Applications. Currently, the EV segment dominates due to the rising number of electric vehicles on the roads, especially in China and Japan. The high energy efficiency, cost-effectiveness, and environmental advantages of LFP batteries make them the preferred choice for EV applications across the region, supported by favorable government policies and incentives in countries like China.

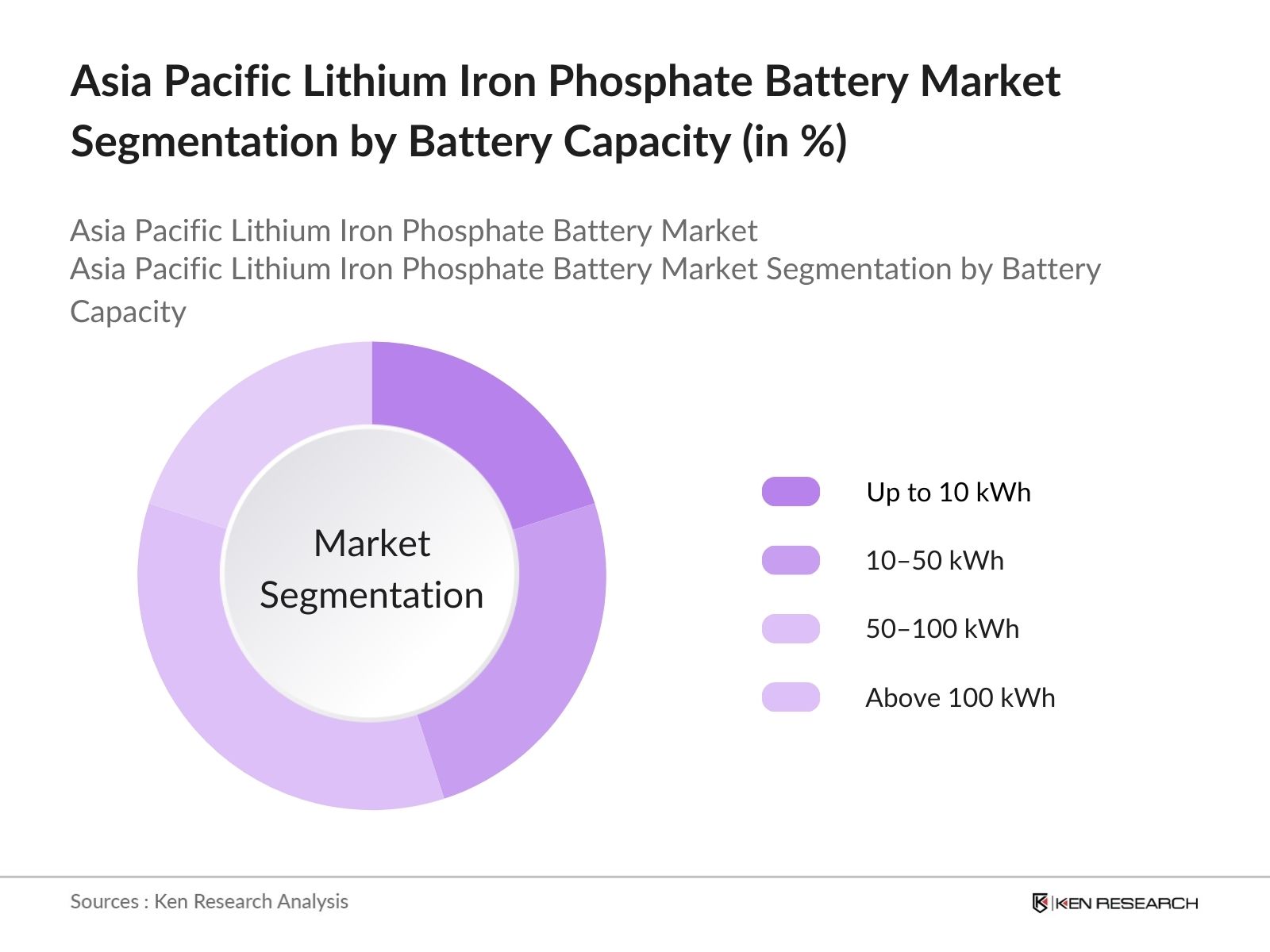

By Battery Capacity: The market is further segmented by battery capacity into Up to 10 kWh, 1050 kWh, 50100 kWh, and Above 100 kWh. Batteries in the 50100 kWh category hold the largest share, driven by the high demand in commercial EVs and large-scale energy storage projects. This capacity range strikes a balance between power output and durability, making it highly suitable for mid-size to heavy-duty electric vehicles and medium-sized renewable energy storage projects.

Asia Pacific Lithium Iron Phosphate Battery Market Competitive Landscape

The market is dominated by a few key players, including major battery manufacturers from China, Japan, and South Korea. Companies such as CATL and BYD in China, and Panasonic and LG Chem in Japan and South Korea, are leading due to their strong production capacities, R&D investments, and strategic partnerships with automotive and industrial companies.

Asia Pacific Lithium Iron Phosphate Battery Market Analysis

Market Growth Drivers

- Surge in Electric Vehicle (EV) Production Across Key Asia-Pacific Economies: The Asia Pacific region is witnessing a significant increase in EV production, with China leading the industry. In 2024, Chinas EV production is expected to reach approximately 8 million units, driven by governmental incentives and an expanding charging infrastructure.

- Expansion of Renewable Energy Storage Projects: Energy storage systems (ESS) that utilize LFP batteries are seeing notable growth as renewable energy adoption rises. Japan, for example, has allocated around 100 billion ($674 million USD) in 2024 to support renewable energy storage projects, which prominently feature LFP technology due to its reliability and lifespan

- Support for Decentralized Energy Projects in Southeast Asia: Southeast Asia is heavily investing in decentralized energy solutions, especially in Indonesia, where the government plans to deploy 500 MW of distributed renewable energy systems by 2025. LFP batteries are preferred for their low-cost scalability and safety in isolated locations, supporting demand for these batteries in residential and industrial energy storage.

Market Challenges

- High Cost of Raw Materials and Supply Chain Constraints: The cost of raw materials required for LFP batteries, such as lithium and iron, remains volatile. For example, in 2024, lithium prices reached approximately $70,000 per ton due to supply shortages, which challenges LFP battery manufacturers in the region. Dependence on imported raw materials, especially from Australia and Latin America, adds further cost pressures.

- Environmental Concerns Regarding Mining Practices: Environmental impacts of lithium extraction pose regulatory challenges in the Asia-Pacific. For instance, in 2024, the Philippines introduced stringent environmental standards, adding compliance costs to lithium mining projects that feed the battery sector. Such regulatory actions are increasing operating costs for LFP battery suppliers, impacting profitability.

Asia Pacific Lithium Iron Phosphate Battery Market Future Outlook

Over the next five years, the Asia Pacific LFP Battery Industry is anticipated to experience substantial growth, spurred by the continuous rise in demand for EVs, ongoing expansion of renewable energy projects, and advancements in battery technology.

Future Market Opportunities

- Increased Adoption of LFP Batteries in Public Transportation Fleets: By 2029, cities across the Asia-Pacific, especially in China and Japan, are expected to integrate over 50,000 electric buses using LFP batteries due to government commitments to reduce urban air pollution. LFPs durability and cost advantages make it ideal for public transport applications, where reliability and cost savings are crucial.

- Growth in Renewable Energy-Driven Energy Storage Demand: By 2028, it is projected that Japan and South Korea will add an additional 15 GW of ESS capacity, largely powered by LFP batteries, to support grid stability. This shift is fueled by stringent emissions targets and high renewable energy adoption.

Scope of the Report

|

Type |

Portable Batteries |

|

Application |

Automotive |

|

Power Capacity |

016,250 mAh |

|

Voltage |

Up to 12V |

|

Region |

China |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Electric Vehicle Manufacturers

Renewable Energy Providers

Battery Manufacturing Companies

Automotive OEMs

Energy Storage Solution Providers

Government and Regulatory Bodies (e.g., Ministry of Industry and Information Technology, China; Ministry of Economy, Trade, and Industry, Japan)

Investors and Venture Capitalist Firms

Telecommunications and Consumer Electronics Companies

Companies

Players Mentioned in the Report:

CATL

BYD

Panasonic Corporation

LG Chem

Samsung SDI

A123 Systems LLC

Toshiba Corporation

Sony Energy Devices Corporation

Wanxiang Group Corporation

E-One Moli Energy Corp

Table of Contents

1. Asia Pacific Lithium Iron Phosphate Battery Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Asia Pacific Lithium Iron Phosphate Battery Market Size (In USD Million)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Asia Pacific Lithium Iron Phosphate Battery Market Analysis

3.1 Growth Drivers (e.g., EV adoption, renewable energy storage)

3.2 Market Challenges (e.g., high costs, supply chain issues)

3.3 Opportunities (e.g., smart grid integration, fast-charging tech)

3.4 Trends (e.g., battery recycling, EV collaboration)

3.5 Government Regulations (e.g., emission targets, safety standards)

3.6 SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7 Stakeholder Ecosystem (e.g., manufacturers, suppliers, regulators)

3.8 Porter’s Five Forces Analysis (competition, supplier power)

3.9 Competitive Landscape (key players and strategies)

4. Asia Pacific Lithium Iron Phosphate Battery Market Segmentation

4.1 By Type (e.g., portable, stationary)

4.2 By Application (e.g., automotive, energy storage, electronics)

4.3 By Power Capacity (e.g., 0–16,250 mAh, 50,001–100,000 mAh)

4.4 By Voltage (e.g., up to 12V, 36V–48V, above 48V)

4.5 By Region (e.g., China, Japan, India, South Korea, Australia)

5. Asia Pacific Lithium Iron Phosphate Battery Market Competitive Analysis

5.1 Detailed Profiles of Major Companies (e.g., BYD, CATL, LG Chem)

5.2 Cross Comparison Parameters (e.g., revenue, R&D investment, market share)

5.3 Market Share Analysis (e.g., dominant players by region)

5.4 Strategic Initiatives (e.g., product launches, partnerships)

5.5 Mergers and Acquisitions (e.g., industry consolidation trends)

5.6 Investment Analysis (e.g., venture capital, government grants)

5.7 Venture Capital Funding (e.g., emerging battery tech startups)

5.8 Government Grants (e.g., incentives for battery innovation)

5.9 Private Equity Investments (e.g., growth funding for LFP battery firms)

6. Asia Pacific Lithium Iron Phosphate Battery Market Regulatory Framework

6.1 Environmental Standards (e.g., sustainability compliance)

6.2 Compliance Requirements (e.g., safety regulations)

6.3 Certification Processes (e.g., quality and performance standards)

7. Asia Pacific Lithium Iron Phosphate Battery Future Market Size (In USD Million)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Asia Pacific Lithium Iron Phosphate Battery Future Market Segmentation

8.1 By Type

8.2 By Application

8.3 By Power Capacity

8.4 By Voltage

8.5 By Country

9. Asia Pacific Lithium Iron Phosphate Battery Market Analysts Recommendations

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This phase involves mapping the entire ecosystem within the Asia Pacific LFP Battery Market, focusing on manufacturers, end-users, and government bodies. Secondary research from reputable databases and proprietary sources was conducted to isolate critical market factors influencing battery demand and usage.

Step 2: Market Analysis and Construction

Historical data on LFP battery production, application sectors, and revenues were collected and analyzed to identify patterns and growth trajectories. In addition, market penetration rates and product adoption statistics were assessed to build reliable market forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions were verified through discussions with key stakeholders and industry experts, including representatives from major LFP battery companies. These insights were instrumental in refining market estimates and aligning them with industry realities.

Step 4: Research Synthesis and Final Output

The final phase involved detailed interviews with battery manufacturers and energy providers to validate findings. This step confirmed the accuracy of projections, and the report was further validated through a bottom-up analysis to ensure comprehensive and reliable insights.

Frequently Asked Questions

01. How big is the Asia Pacific Lithium Iron Phosphate Battery Market?

The Asia Pacific Lithium Iron Phosphate Battery Market is valued at USD 2.7 billion, primarily driven by the electric vehicle and energy storage sectors, with significant contributions from China and Japan.

02. What are the main challenges in the Asia Pacific LFP Battery Market?

Key challenges in the Asia Pacific Lithium Iron Phosphate Battery Market include the high initial investment costs for production, supply chain constraints, and competition from other lithium-ion chemistries like nickel-cobalt-manganese (NCM) batteries.

03. Who are the major players in the Asia Pacific LFP Battery Market?

Key players in the Asia Pacific Lithium Iron Phosphate Battery Market include CATL, BYD, Panasonic Corporation, LG Chem, and Samsung SDI, who dominate due to extensive R&D investments and large-scale production capacities.

04. What are the growth drivers for the Asia Pacific LFP Battery Market?

The Asia Pacific Lithium Iron Phosphate Battery Market is driven by increased adoption of electric vehicles, expanding renewable energy storage solutions, and supportive government policies across major countries in the Asia Pacific region.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.