Asia Pacific Locomotive Industry Outlook to 2030

Region:Asia

Author(s):Sanjna

Product Code:KROD3337

November 2024

93

About the Report

Asia Pacific Locomotive Industry Overview

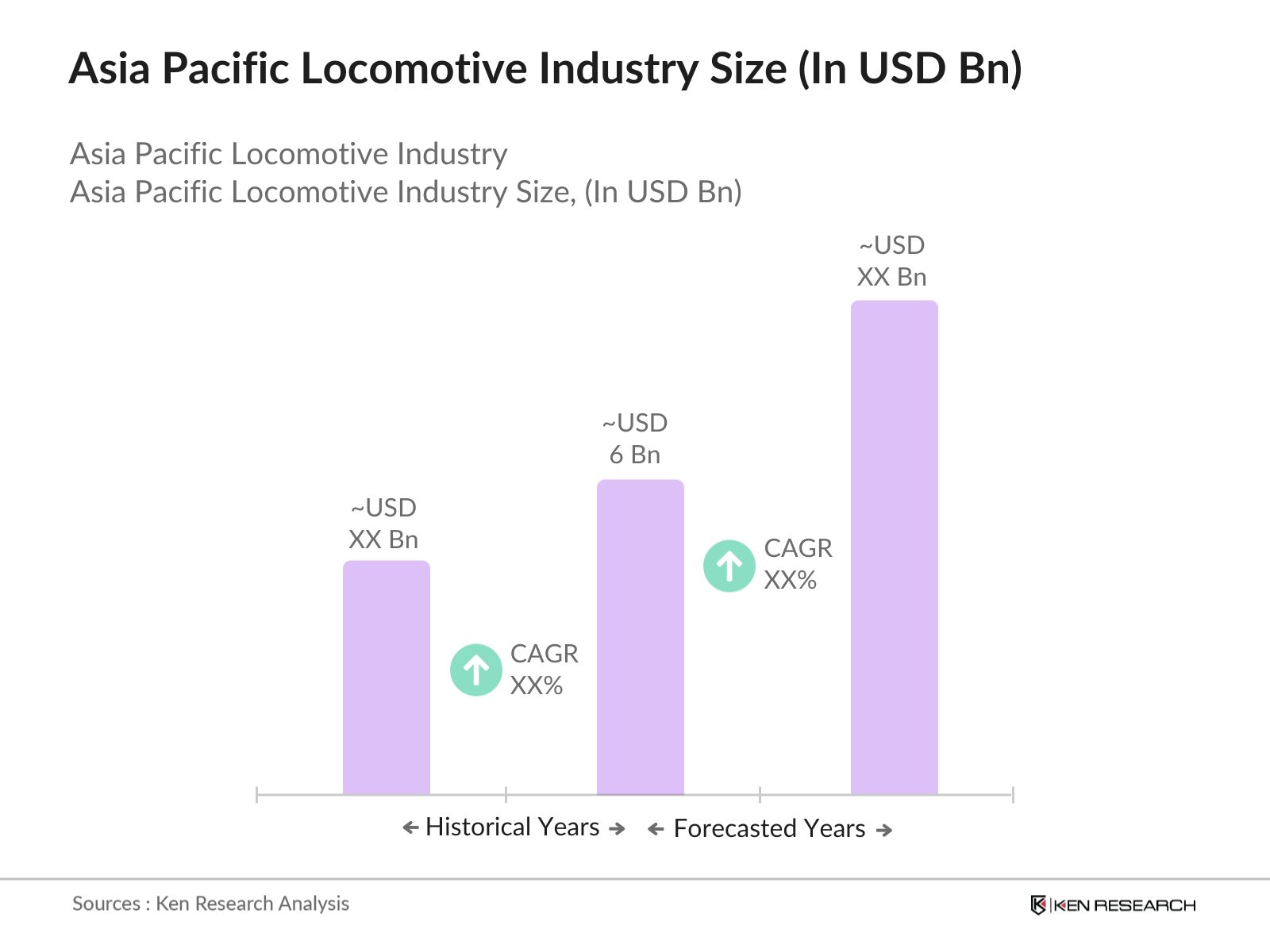

- The Asia Pacific locomotive industry is valued at USD 6 billion, driven by substantial Investments in railway infrastructure and the rapid shift toward electrification. The region is witnessing a growing demand for energy-efficient and environmentally sustainable locomotives, particularly in response to strict emission regulations. Urbanization and industrial expansion have further fueled the growth of freight and passenger rail services, contributing to the significant expansion of the market.

- Countries like China, India, and Japan dominate the Asia Pacific locomotive market. China leads due to its extensive rail network and high government spending on rail infrastructure development, while India is catching up with several modernization projects. Japan, with its advanced high-speed rail systems, maintains its dominance in passenger transport locomotives. These countries benefit from robust government policies, infrastructure investments, and technological advancements, making them key players in the market.

- The Asia Pacific region has implemented strict emission controls to reduce the environmental impact of rail transport. As of November 2023,, 60,814 km of broad-gauge network has been electrified, with 39,013 km electrified since April 2014 China's "Blue Sky Defense" plan includes reducing railway sector CO2 emissions by 12 million tons annually as part of its Paris Agreement commitment. These regulations push manufacturers to innovate and adopt cleaner locomotive technologies.

Asia Pacific Locomotive Industry Segmentation

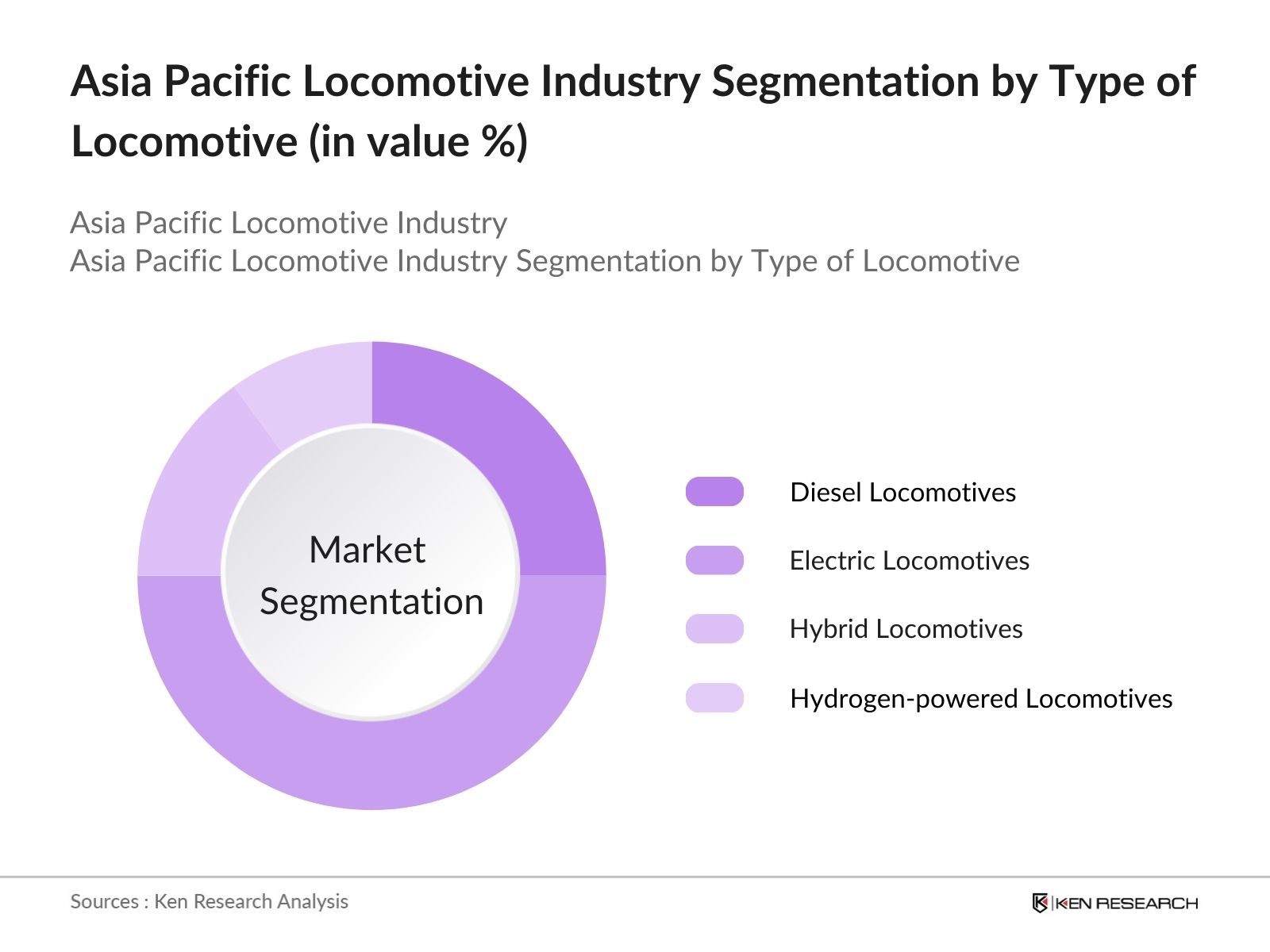

By Type of Locomotive: The Asia Pacific locomotive market is segmented by type into diesel, electric, hybrid, and hydrogen-powered locomotives. Recently, electric locomotives have dominated the market share under this segmentation, driven by increased governmental efforts to reduce carbon emissions and dependence on fossil fuels. Electric locomotives are favored for their efficiency, low operational costs, and the availability of renewable energy options. Countries like China and India are heavily investing in the electrification of their rail networks, contributing to the rise of this segment.

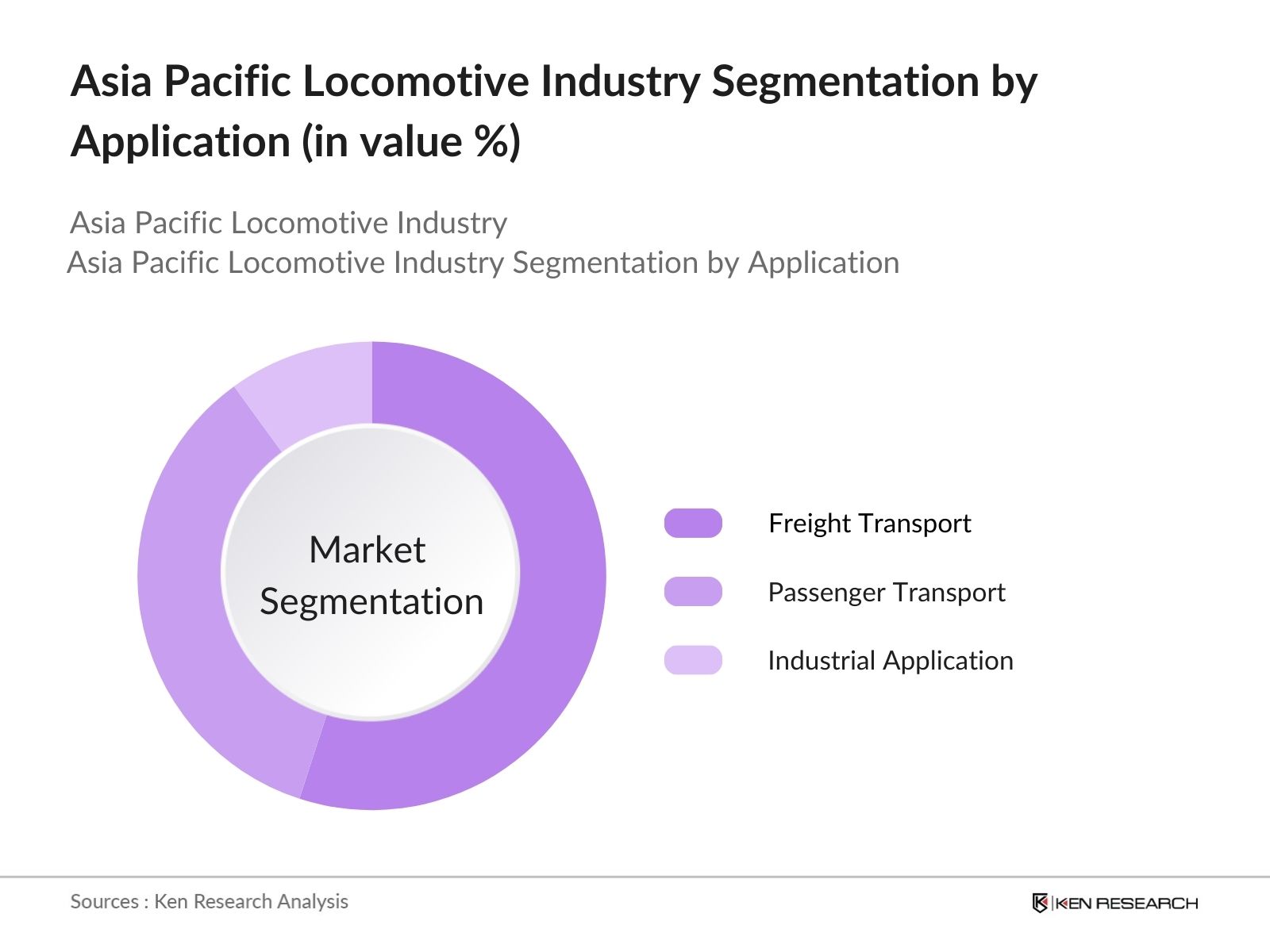

By Application: The market is further segmented by application into freight transport, passenger transport, and industrial applications. Freight transport holds a dominant market share within this segment due to the increased demand for transporting goods across industrialized regions. The expansion of e-commerce, coupled with government efforts to modernize freight corridors, has led to a surge in demand for freight locomotives. Additionally, the cost-efficiency and large-scale capacity of freight trains make them a preferred choice for businesses in logistics and supply chain management.

Asia Pacific Locomotive Industry Competitive Landscape

The Asia Pacific locomotive market is dominated by a mix of local and global players, with leading companies competing on technological innovation, environmental sustainability, and extensive railway network projects. Companies like CRRC Corporation and GE Transportation lead the market through advanced locomotive manufacturing capabilities and collaborations with national governments. Local players benefit from their established presence and strategic government partnerships.

|

Company Name |

Establishment Year |

Headquarters |

No. of Employees |

Key Contracts |

Green Technology Initiatives |

Annual Revenue |

Investments in R&D |

Market Share |

Strategic Alliances |

|

CRRC Corporation |

2015 |

Beijing, China |

- |

- |

- |

- |

- |

- |

- |

|

GE Transportation |

1892 |

Chicago, USA |

- |

- |

- |

- |

- |

- |

- |

|

Alstom |

1928 |

Saint-Ouen, France |

- |

- |

- |

- |

- |

- |

- |

|

Siemens Mobility |

1847 |

Munich, Germany |

- |

- |

- |

- |

- |

- |

- |

|

Kawasaki Heavy Industries |

1896 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

- |

Asia Pacific Locomotive Industry Analysis

Growth Drivers

- Expansion of Freight Transportation: The Asia Pacific region has seen significant growth in freight transportation due to increasing industrial activity and trade. Indian Railways achieved a freight loading of approximately903 billion net tonne kilometers (NTKMs)in the financial year 2022-23, which translates to about0.9 trillion ton-kilometers. With rapid industrialization in countries like India, Indonesia, and Vietnam, the demand for rail freight services is expected to remain strong. This expansion is fueled by government investments in port-to-rail connections and transcontinental trade routes.

- Rapid Urbanization and Intercity Connectivity: Urbanization in Asia Pacific has grown rapidly, with countries like China reaching an urbanization rate of 65% in 2023, while India stands at 36%. This growth drives the need for better intercity rail connectivity. In Southeast Asia, cities like Jakarta, Bangkok, and Ho Chi Minh City are expanding their urban rail networks, enhancing regional connectivity. The surge in middle-class populations and increased mobility between cities necessitate faster, more efficient transportation solutions, with rail transport becoming a key part of regional and national infrastructure projects.

- Investment in Railway Infrastructure: Governments across Asia Pacific have made substantial investments in railway infrastructure. In India, the government has indeed committed$10 billion to modernize its national railway system. This investment includes initiatives for new high-speed corridors and electrification projects, aimed at transforming the Indian Railways into a more efficient and modern transport system. Similarly, Japan and South Korea have allocated funds to improve both freight and passenger rail networks, demonstrating the region's focus on expanding rail infrastructure for economic development.

Challenges

- High Initial Capital Investment: Indias dedicated freight corridors, under construction since 2013, are expected to cost $12 billion by the time of completion. Similarly, Japans maglev high-speed rail project has already surpassed $50 billion in investment. This high CAPEX limits the pace of new railway developments, especially in emerging economies where public funds and private investment are harder to secure.

- Stringent Emission Regulations: Several countries in Asia Pacific have tightened emission regulations in response to global climate change concerns. Japan and South Korea have implemented stringent Tier 4 emission standards for new diesel locomotives, requiring a 50% reduction in nitrogen oxide (NOx) and particulate matter (PM) emissions compared to older models. These regulations increase the cost of adopting compliant technologies and add to the financial burden of operators.

Asia Pacific Locomotive Industry Future Outlook

The Asia Pacific locomotive market is expected to grow significantly over the next five years due to continued government investments in railway infrastructure and the increasing demand for low-emission transportation solutions. Governments in the region are actively working on electrification and modernization projects to improve the efficiency of rail networks, both for freight and passenger transport. The rise in cross-border trade and regional connectivity initiatives, such as the Belt and Road Initiative, will further drive growth in the locomotive industry. With the adoption of hybrid and hydrogen-powered locomotives, the market is set for substantial transformation.

Market Opportunities

- Introduction of Hybrid and Electric Locomotives: With the growing focus on sustainable transportation, Asia Pacific countries are accelerating the adoption of hybrid and electric locomotives. India, having electrified 95% of its rail network by 2023, has set ambitious targets for 100% electrification. China leads the way globally with over 95,000 km of electrified tracks. These advancements present significant opportunities for locomotive manufacturers and related industries.

- Modernization of Existing Rail Networks: Asia Pacific governments are prioritizing modernization projects for aging rail networks. Indias $30 billion investment plan focuses on upgrading signaling systems, tracks, and introducing high-speed trains. In 2023, Japan allocated $1.2 billion for digital signaling upgrades and station overhauls. These modernization efforts will enhance network efficiency, reduce operational costs, and increase passenger capacity, presenting opportunities for technology providers and contractors.

Scope of the Report

|

Segment |

Sub-Segment |

|

Type of Locomotive |

Diesel Locomotives |

|

Electric Locomotives |

|

|

Hybrid Locomotives |

|

|

Hydrogen-powered Locomotives |

|

|

Component |

Engine Systems |

|

Traction Motors |

|

|

Control Systems |

|

|

Braking Systems |

|

|

Technology |

Conventional Locomotive Technology |

|

Autonomous Locomotive Technology |

|

|

Digital Rail Solutions |

|

|

Application |

Freight Transport |

|

Passenger Transport |

|

|

Industrial Applications |

|

|

Country |

China |

|

India |

|

|

Japan |

|

|

Australia |

|

|

South Korea |

|

|

ASEAN Countries |

Products

Key Target Audience

Railway Equipment Manufacturers

Railway Operators and Service Providers

Technology Providers for Autonomous Locomotives

Freight and Logistics Companies

Urban Transport Planning Authorities

Energy and Utility Providers for Electrification Projects

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Railways, National Development and Reform Commission)

Companies

Major Players

CRRC Corporation

GE Transportation

Alstom

Siemens Mobility

Hitachi Rail

Bombardier Transportation

Kawasaki Heavy Industries

Hyundai Rotem

Bharat Heavy Electricals Limited (BHEL)

Toshiba Corporation

Stadler Rail

Mitsubishi Electric

Wabtec Corporation

Transmashholding

CAF

Table of Contents

1. Asia Pacific Locomotive Industry Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Locomotive Industry Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Locomotive Industry Analysis

3.1. Growth Drivers

3.1.1. Expansion of Freight Transportation (Ton-kilometers of freight)

3.1.2. Rapid Urbanization and Intercity Connectivity (Urbanization Rate)

3.1.3. Investment in Railway Infrastructure (Government Expenditure)

3.1.4. Adoption of Energy-efficient Locomotives (Energy Efficiency Parameters)

3.2. Market Challenges

3.2.1. High Initial Capital Investment (CAPEX Metrics)

3.2.2. Stringent Emission Regulations (Emission Standards)

3.2.3. Aging Rail Infrastructure (Infrastructure Longevity)

3.2.4. Lack of Skilled Technical Personnel (Workforce Availability)

3.3. Opportunities

3.3.1. Introduction of Hybrid and Electric Locomotives (Electrification Ratio)

3.3.2. Modernization of Existing Rail Networks (Network Modernization Projects)

3.3.3. International Collaborations for Technology Transfer (Technology Partnerships)

3.3.4. Growth in Rail Freight Transport (Freight Transport Volume)

3.4. Trends

3.4.1. Rising Adoption of Autonomous Locomotive Technology (Automation Penetration Rate)

3.4.2. Increased Demand for High-speed Rail (High-Speed Rail Projects)

3.4.3. Transition Towards Hydrogen-powered Locomotives (Hydrogen Fuel Adoption)

3.4.4. Shift to Digitalized Railway Operations (Digitalization Index in Railways)

3.5. Government Regulations

3.5.1. Regulatory Frameworks on Emission Controls (CO2 Emission Limits)

3.5.2. National Rail Development Plans (Rail Network Expansion Plans)

3.5.3. Incentives for Adoption of Cleaner Technology (Green Energy Initiatives)

3.5.4. Public-private Partnerships for Infrastructure Development (PPP Models in Railways)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia Pacific Locomotive Industry Segmentation

4.1. By Type of Locomotive (In Value %)

4.1.1. Diesel Locomotives

4.1.2. Electric Locomotives

4.1.3. Hybrid Locomotives

4.1.4. Hydrogen-powered Locomotives

4.2. By Component (In Value %)

4.2.1. Engine Systems

4.2.2. Traction Motors

4.2.3. Control Systems

4.2.4. Braking Systems

4.3. By Technology (In Value %)

4.3.1. Conventional Locomotive Technology

4.3.2. Autonomous Locomotive Technology

4.3.3. Digital Rail Solutions

4.4. By Application (In Value %)

4.4.1. Freight Transport

4.4.2. Passenger Transport

4.4.3. Industrial Applications

4.5. By Country (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. South Korea

4.5.6. ASEAN Countries

5. Asia Pacific Locomotive Industry Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. CRRC Corporation

5.1.2. GE Transportation

5.1.3. Alstom

5.1.4. Siemens Mobility

5.1.5. Hitachi Rail

5.1.6. Bombardier Transportation

5.1.7. Kawasaki Heavy Industries

5.1.8. Hyundai Rotem

5.1.9. Bharat Heavy Electricals Limited (BHEL)

5.1.10. Toshiba Corporation

5.1.11. Stadler Rail

5.1.12. Mitsubishi Electric

5.1.13. Wabtec Corporation

5.1.14. Transmashholding

5.1.15. CAF

5.2. Cross Comparison Parameters

5.2.1. No. of Employees

5.2.2. Headquarters Location

5.2.3. Annual Revenue

5.2.4. Market Share

5.2.5. Key Contracts and Projects

5.2.6. Investments in R&D

5.2.7. Green Technology Initiatives

5.2.8. Strategic Alliances

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Locomotive Industry Regulatory Framework

6.1. Emission Standards and Certifications

6.2. Operational Safety Regulations

6.3. Locomotive Certification Processes

6.4. Regional Environmental Compliance

7. Asia Pacific Locomotive Industry Future Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Locomotive Industry Future Segmentation

8.1. By Type of Locomotive (In Value %)

8.2. By Component (In Value %)

8.3. By Technology (In Value %)

8.4. By Application (In Value %)

8.5. By Country (In Value %)

9. Asia Pacific Locomotive Industry Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Asia Pacific locomotive market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the Asia Pacific locomotive market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple locomotive manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Asia Pacific locomotive market.

Frequently Asked Questions

1. How big is the Asia Pacific Locomotive Industry Market?

The Asia Pacific locomotive market is valued at USD 6 billion, driven by investments in rail infrastructure and the demand for energy-efficient transportation solutions.

2. What are the challenges in the Asia Pacific Locomotive Industry Market?

Challenges include high capital expenditure for rail infrastructure projects, stringent emission regulations, and the aging rail infrastructure across some countries in the region.

3. Who are the major players in the Asia Pacific Locomotive Industry Market?

Key players in the market include CRRC Corporation, GE Transportation, Alstom, Siemens Mobility, and Hitachi Rail. These companies lead due to their extensive technological capabilities and government contracts.

4. What are the growth drivers of the Asia Pacific Locomotive Industry Market?

The market is propelled by investments in rail infrastructure, government initiatives to reduce emissions, and the growing demand for freight and passenger transportation. Technological advancements such as hybrid and hydrogen-powered locomotives also contribute to the growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.