Asia Pacific Low Cost Carrier Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD6326

December 2024

99

About the Report

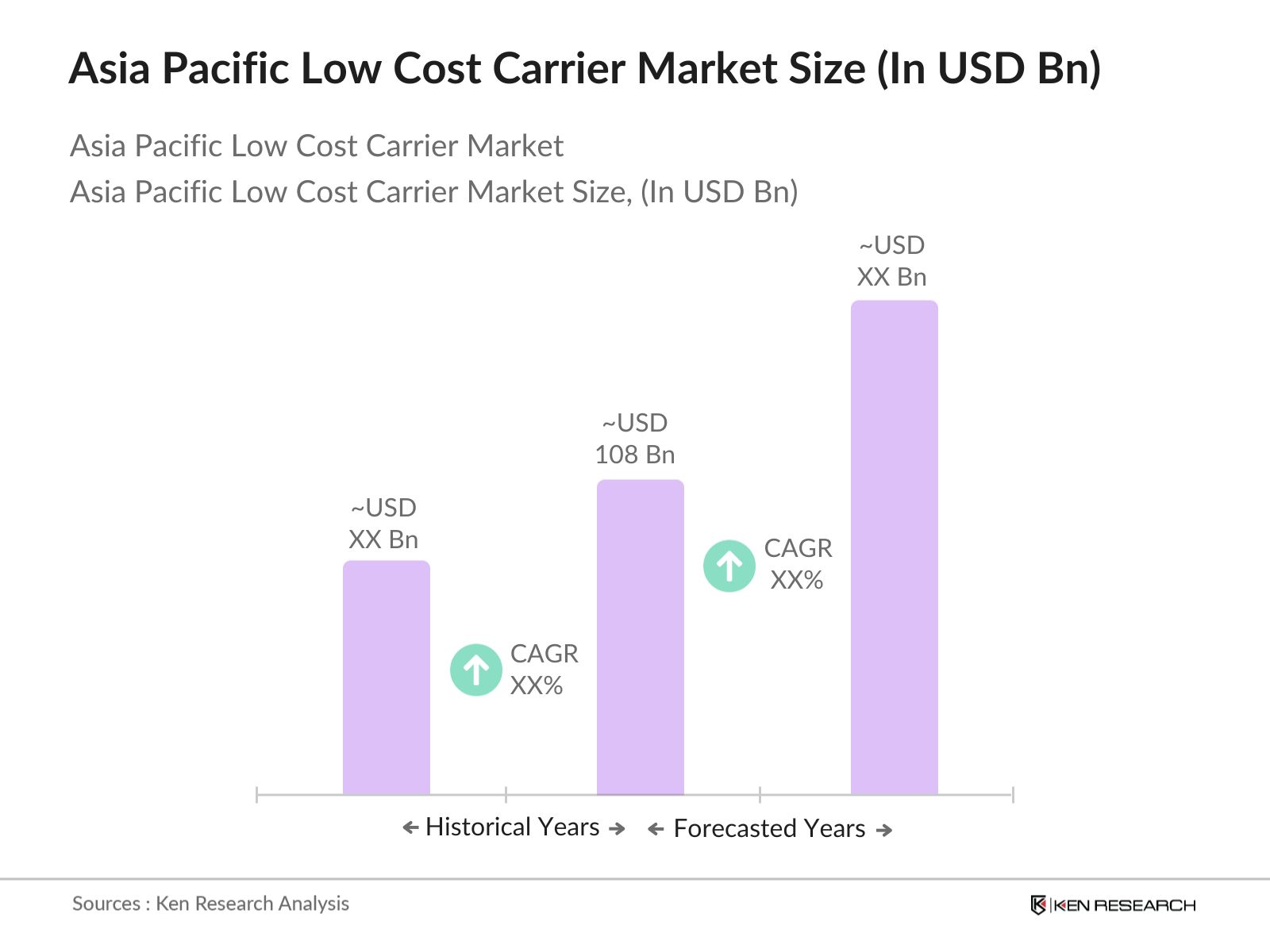

Asia Pacific Low Cost Carrier Market Overview

- The Asia Pacific Low Cost Carrier (LCC) Market is valued at USD 108 billion, based on a five-year historical analysis. The markets growth is largely driven by the increasing middle-class population, rising disposable incomes, and the growing preference for affordable travel across both domestic and international routes. Low-cost carriers provide budget-friendly services that attract price-conscious travellers, and they optimize operational efficiency through streamlined services, which contributes to the overall market expansion.

- China, India, and Indonesia dominate the Asia Pacific LCC market due to their large populations and expanding economies. In China, the dominance stems from the governments focus on infrastructure development and aviation liberalization. India benefits from its rapidly urbanizing population and the rise in domestic tourism, while Indonesias widespread archipelago necessitates air travel, boosting the demand for LCCs. Additionally, these countries have seen investments in airport development and route expansion by major LCCs.

- LCCs in Asia Pacific are increasingly relying on ancillary revenue models to boost profitability. Data from the International Air Transport Association (IATA) shows that by 2023, ancillary services accounted for 40% of total revenue for Asia Pacific LCCs. These include fees for checked baggage, priority boarding, in-flight meals, and seat selection. Ancillary revenues have become a crucial part of LCCs' strategy to maintain low base fares while enhancing profitability, allowing them to compete effectively against full-service airlines.

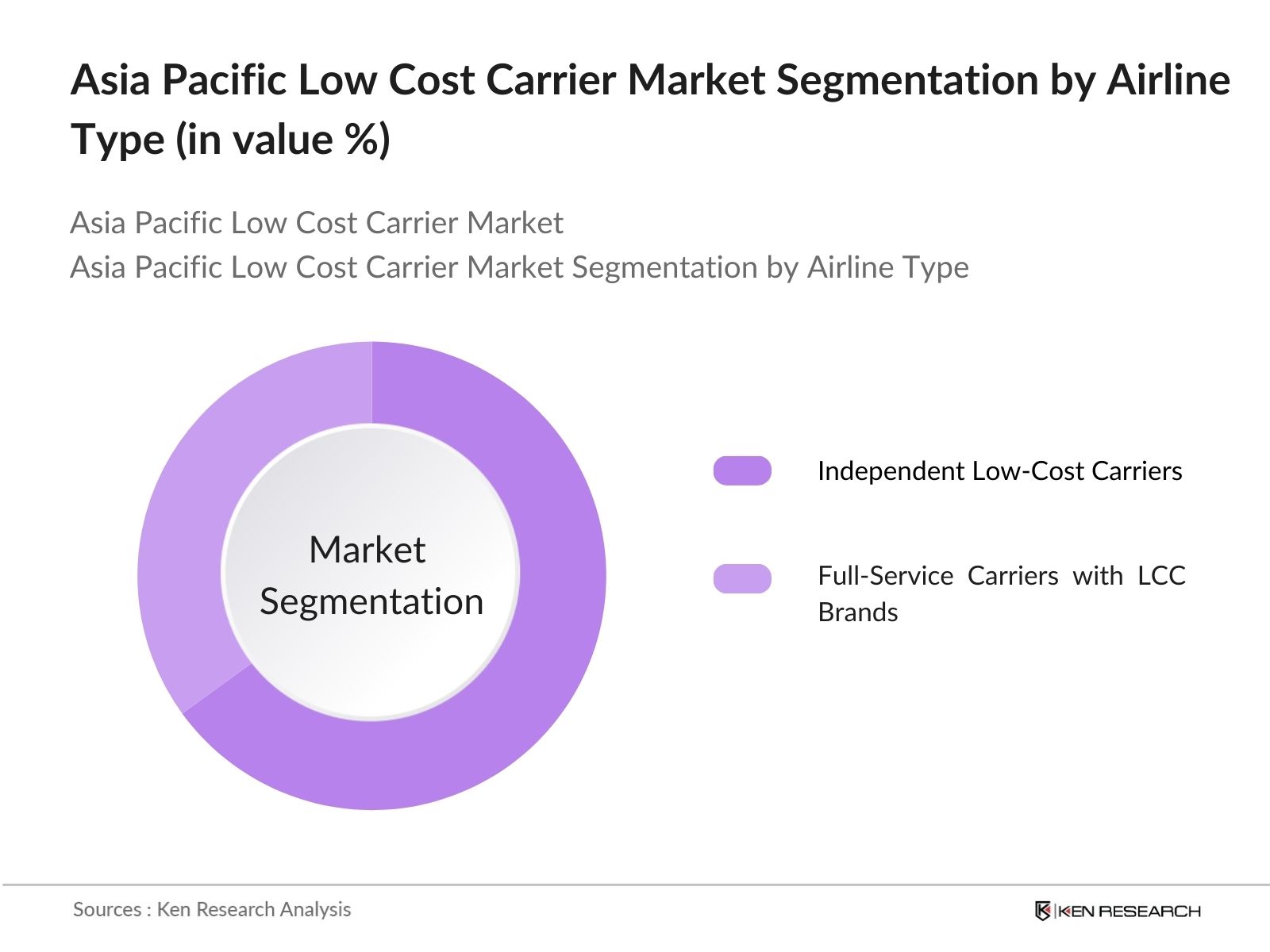

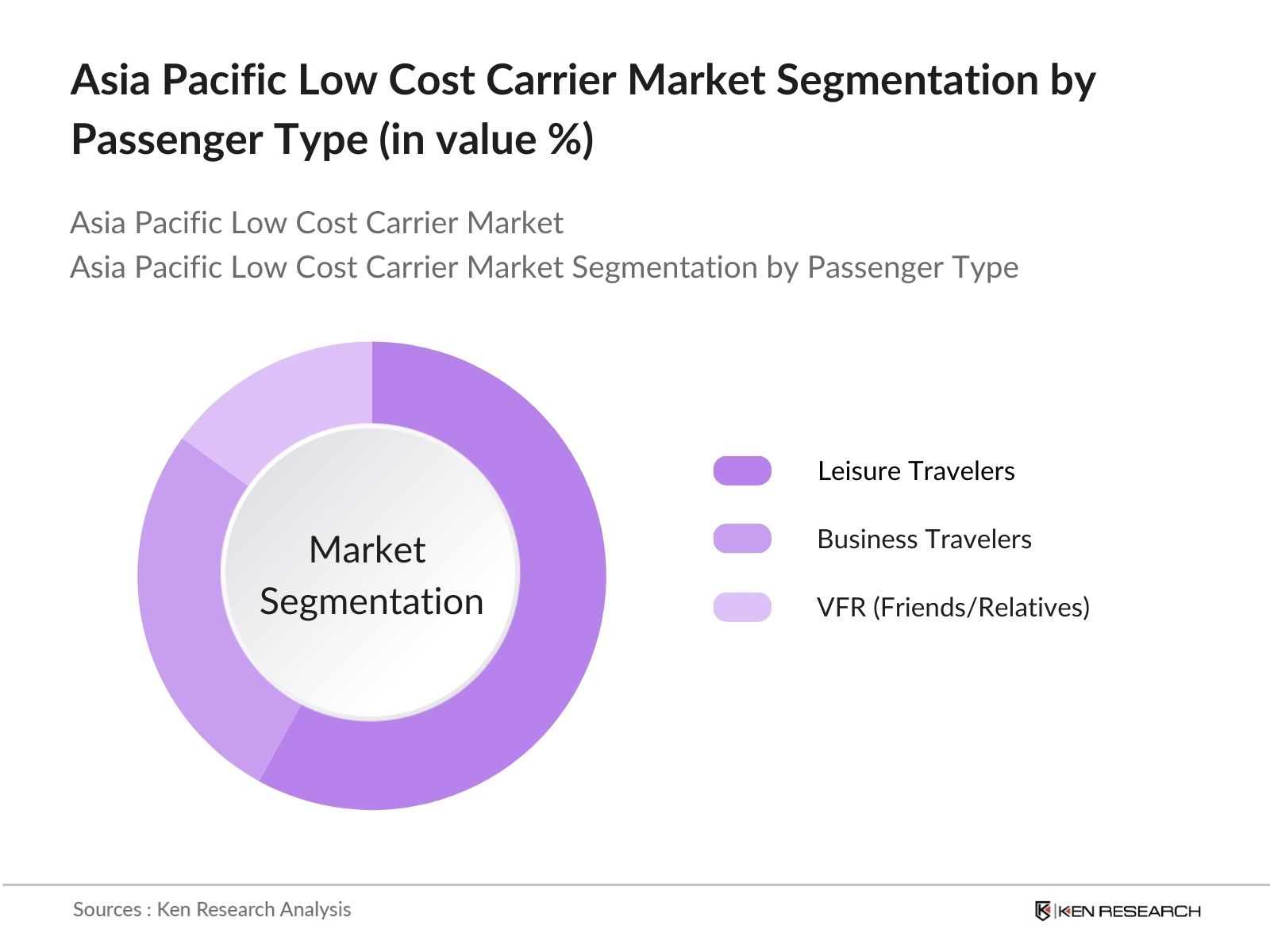

Asia Pacific Low Cost Carrier Market Segmentation

- By Airline Type: The market is segmented by airline type into independent low-cost carriers and full-service carriers with LCC subsidiaries. Independent low-cost carriers, such as AirAsia and Indigo, hold the dominant market share under this segmentation due to their established cost-effective operational models and extensive networks. These carriers emphasize no-frills services, allowing them to maintain low operational costs, which translates to competitive ticket prices and wider market reach.

- By Passenger Type: The market is also segmented by passenger type into leisure travellers, business travellers, and those visiting friends and relatives (VFR). Leisure travellers dominate the LCC passenger segment, driven by the increasing number of budget-conscious holidaymakers. LCCs offer affordable travel options that cater to the rising demand for short-haul vacations, especially within Southeast Asia. Moreover, the rapid growth of the tourism industry across key markets has further amplified the demand for affordable, accessible air travel services.

Asia Pacific Low Cost Carrier Market Competitive Landscape

The Asia Pacific Low Cost Carrier market is dominated by a few key players, both regional and global, who maintain a competitive advantage through strategic route expansions, competitive pricing, and efficient fleet utilization. These carriers rely heavily on ancillary revenue streams and cost-effective business models to remain competitive. The consolidation of the market around these major players demonstrates their strong influence, particularly in densely populated markets.

Company Name | Establishment Year | Headquarters | Fleet Size | Route Network | Revenue (USD Bn) | Ancillary Revenue | Customer Satisfaction Rating | Sustainability Initiatives |

AirAsia Group | 1993 | Kuala Lumpur | - | - | - | - | - | - |

Indigo | 2006 | Gurugram | - | - | - | - | - | - |

Scoot | 2011 | Singapore | - | - | - | - | - | - |

Jetstar Airways | 2003 | Melbourne | - | - | - | - | - | - |

VietJet Air | 2007 | Ho Chi Minh City | - | - | - | - | - | - |

Asia Pacific Low Cost Carrier Market Analysis

Asia Pacific Low Cost Carrier Market Growth Drivers

- Increasing Tourism in Emerging Markets: Tourism in Asia Pacific has seen a robust resurgence, driven by countries like Thailand, Vietnam, and Indonesia. The World Bank data indicates that international tourist arrivals in Asia Pacific crossed 450 million in 2023, spurred by relaxed travel restrictions and government support for tourism promotion. Low-cost carriers (LCCs) have capitalized on this surge, offering affordable air travel options to tourists. For example, Thailand recorded over 30 million tourist arrivals in 2023, a substantial boost for LCCs operating in the region. This rise in tourism is creating sustained demand for LCCs, with carriers expanding their fleet and destinations.

- Rise in Middle-Class Population and Disposable Income: The growing middle-class population across Asia Pacific, particularly in countries like India and China, has boosted air travel demand. According to the International Monetary Fund (IMF), over 1.3 billion people in Asia are now classified as middle-income as of 2023, with a notable increase in disposable income. For example, Indias per capita income reached USD 2,500 in 2023, contributing to increased travel expenditure. This demographic shift supports LCC growth, as cost-conscious consumers prefer budget airlines. LCCs have thus expanded rapidly, catering to the rising demand from these middle-income travellers.

- Low-Cost Business Model Adaptation: LCCs have increasingly optimized their low-cost business model by reducing overheads and maximizing operational efficiency. Airlines have adopted practices such as unbundled services, increasing revenue from ancillary services like baggage fees and seat selection. In 2023, Asia Pacific LCCs generated over USD 50 billion in ancillary revenue, reflecting a solid adaptation of the low-cost model. This strategy allows LCCs to keep ticket prices competitive, making air travel affordable for millions of passengers annually, especially in countries where full-service airlines dominate.

Asia Pacific Low Cost Carrier Market Challenges

- High Fuel Prices Impacting Operational Costs: Fuel costs remain a major challenge for LCCs, with jet fuel prices increasing by 12% in 2023, as reported by the International Energy Agency (IEA). With fuel accounting for nearly 30% of an airline's operating costs, Asia Pacific LCCs have faced rising expenses. For example, jet fuel prices averaged USD 120 per barrel in 2023, which directly impacted LCCs' ability to maintain ultra-low fares. Despite efforts to offset costs through ancillary revenues, high fuel prices continue to strain profitability and pressure airlines to reconsider their fare structures.

- Regulatory Restrictions in Certain Regions: Regulatory barriers remain an issue in several Asia Pacific countries, particularly regarding foreign ownership and bilateral air service agreements. Countries like China and Japan have stringent regulations limiting LCCs' operations, impeding their ability to freely expand. Data from the Asian Development Bank (ADB) in 2023 shows that such regulatory challenges have hindered the growth of foreign LCCs, as domestic markets remain protected. These restrictions stymie competition, limiting market entry and the expansion of affordable flight options for consumers.

Asia Pacific Low Cost Carrier Market Future Outlook

Over the next five years, the Asia Pacific Low Cost Carrier market is expected to experience robust growth driven by the increasing number of leisure travellers, expansion of tourism, and continued investments in aviation infrastructure across the region. The rise in the middle-class population and the rapid urbanization of smaller cities will further accelerate the demand for affordable air travel. In addition, technological advancements in aircraft fuel efficiency and environmental initiatives will play an important role in ensuring the markets long-term sustainability.

Asia Pacific Low Cost Carrier Market Opportunities

- Expansion of LCCs into Tier 2 and Tier 3 Cities: LCCs are increasingly expanding into Tier 2 and Tier 3 cities across Asia Pacific, unlocking new passenger markets. The World Bank reports that as of 2023, over 65% of Asia Pacifics population resides in non-metropolitan regions, which are underserved by traditional full-service airlines. For example, in India, airports in Tier 2 cities like Bhubaneswar and Coimbatore saw a 25% rise in passenger traffic in 2023, largely driven by LCCs. This expansion into previously untapped markets offers growth potential for LCCs looking to boost domestic travel demand.

- Growing Adoption of Digital Solutions for Efficiency: Digital transformation is a key growth opportunity for LCCs in Asia Pacific. According to the International Telecommunication Union (ITU), over 2.1 billion people in the region had internet access in 2023, facilitating the adoption of digital solutions like mobile check-in, dynamic pricing, and automated flight operations. LCCs, such as AirAsia, have embraced digital platforms to enhance customer experience, reduce costs, and improve operational efficiency. The use of AI-powered systems for route optimization and customer management also helps LCCs streamline operations, further driving market growth.

Scope of the Report

Airline Type | Full-Service Carriers with LCC Brands Independent Low-Cost Carriers |

Passenger Type | Leisure Travellers Business Travellers VFR (Visiting Friends & Relatives) |

Route Type | Domestic International |

Service Offering | Basic Economy Premium Economy Ancillary Services |

Region | Southeast Asia East Asia South Asia Oceania |

Products

Key Target Audience

Airline Operators

Airport Authorities

Aircraft Manufacturers

Banks and Financial Institutions

Government and Regulatory Bodies (Civil Aviation Authorities of respective countries)

Travel Agencies and Tourism Boards

Investors and Venture Capitalist Firms

Technology Solution Providers (In-flight entertainment, digital platforms)

Environmental and Sustainability Agencies

Companies

Players Mentioned in the Report

AirAsia Group

Indigo

Scoot

Jetstar Airways

VietJet Air

Lion Air

Cebu Pacific

Peach Aviation

Nok Air

SpiceJet

Table of Contents

1. Asia Pacific Low Cost Carrier Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Asia Pacific Low Cost Carrier Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Asia Pacific Low Cost Carrier Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Tourism in Emerging Markets

3.1.2 Rise in Middle-Class Population and Disposable Income

3.1.3 Low-Cost Business Model Adaptation

3.1.4 Expansion of International Routes by LCCs

3.2 Market Challenges

3.2.1 High Fuel Prices Impacting Operational Costs

3.2.2 Regulatory Restrictions in Certain Regions

3.2.3 Intense Competition from Full-Service Carriers

3.2.4 Limitations on Service Offerings and Customer Experience

3.3 Opportunities

3.3.1 Expansion of LCCs into Tier 2 and Tier 3 Cities

3.3.2 Growing Adoption of Digital Solutions for Efficiency

3.3.3 Partnerships with Tourism and Hospitality Industry

3.3.4 Introduction of New Aircraft with Improved Fuel Efficiency

3.4 Trends

3.4.1 Rise of Ancillary Revenue Models

3.4.2 Adoption of Self-Check-In and Automation Technologies

3.4.3 Increasing Focus on Sustainability and Carbon Offset Programs

3.4.4 Enhanced Customer Personalization through AI and Data Analytics

3.5 Government Regulation

3.5.1 Liberalization of Aviation Policies

3.5.2 Bilateral Air Service Agreements

3.5.3 Airport Infrastructure Development and Investment

3.5.4 Regulations on Passenger Rights and Compensation

3.6 SWOT Analysis

3.7 Stake Ecosystem (Airlines, Airports, MROs, Ancillary Service Providers)

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

4. Asia Pacific Low Cost Carrier Market Segmentation

4.1 By Airline Type (In Value %)

4.1.1 Full-Service Carriers Offering LCC Brands

4.1.2 Independent Low-Cost Carriers

4.2 By Passenger Type (In Value %)

4.2.1 Leisure Travellers

4.2.2 Business Travellers

4.2.3 VFR (Visiting Friends & Relatives)

4.3 By Route Type (In Value %)

4.3.1 Domestic

4.3.2 International

4.4 By Service Offering (In Value %)

4.4.1 Basic Economy

4.4.2 Premium Economy

4.4.3 Ancillary Services (Baggage, Seat Selection)

4.5 By Region (In Value %)

4.5.1 Southeast Asia

4.5.2 East Asia

4.5.3 South Asia

4.5.4 Oceania

5. Asia Pacific Low Cost Carrier Market Competitive Analysis

5.1 Detailed Profiles of Major Competitors

5.1.1 AirAsia Group

5.1.2 Scoot

5.1.3 Jetstar Airways

5.1.4 Lion Air

5.1.5 Cebu Pacific

5.1.6 Peach Aviation

5.1.7 VietJet Air

5.1.8 Indigo

5.1.9 Nok Air

5.1.10 SpiceJet

5.1.11 Spring Airlines

5.1.12 Jeju Air

5.1.13 Tigerair Taiwan

5.1.14 Air Seoul

5.1.15 Flynas

5.2 Cross Comparison Parameters (Fleet Size, Market Presence, Revenue, Profit Margin, Route Network, Ancillary Revenue, Customer Satisfaction Rating, Sustainability Initiatives)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Alliances, Code-sharing, New Route Launches)

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Aircraft Purchases, Digital Transformation)

5.7 Venture Capital and Private Equity Funding

5.8 Government Grants and Subsidies

6. Asia Pacific Low Cost Carrier Market Regulatory Framework

6.1 Aviation Safety Standards

6.2 Airline Certification Requirements

6.3 Environmental Compliance and Emission Standards

6.4 Consumer Protection Laws

6.5 Compliance with Bilateral and Multilateral Agreements

7. Asia Pacific Low Cost Carrier Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Asia Pacific Low Cost Carrier Future Market Segmentation

8.1 By Airline Type (In Value %)

8.2 By Passenger Type (In Value %)

8.3 By Route Type (In Value %)

8.4 By Service Offering (In Value %)

8.5 By Region (In Value %)

9. Asia Pacific Low Cost Carrier Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Consumer Cohort Analysis (Budget-conscious, Premium Economy Preferences)

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis (Untapped Routes, Emerging Markets)

DisclaimerContact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase involved constructing a detailed ecosystem map of stakeholders in the Asia Pacific Low Cost Carrier market. Secondary data sources, such as industry reports and proprietary databases, were utilized to gather comprehensive market information, including route networks, revenue models, and ancillary services.

Step 2: Market Analysis and Construction

During this phase, historical data regarding market size, fleet expansion, and consumer demand was collected and analyzed. This process included evaluating service quality statistics and compiling financial performance data to develop reliable forecasts and trend analysis.

Step 3: Hypothesis Validation and Expert Consultation

The hypothesis developed from secondary data was validated through direct consultations with industry experts. These interviews, conducted via computer-assisted telephone interviews (CATIs), provided practical insights from airline executives and aviation authorities, ensuring the accuracy of the research findings.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing the research findings into a comprehensive market report. Data verification and analysis were carried out in conjunction with airline operators to ensure the accuracy and reliability of the forecasts, segment performance, and competitive dynamics within the Asia Pacific Low Cost Carrier market.

Frequently Asked Questions

01. How big is the Asia Pacific Low Cost Carrier Market?

The Asia Pacific LCC market is valued at USD 108 billion, driven by the rising demand for affordable air travel among leisure and business travellers across the region.

02. What are the challenges in the Asia Pacific Low Cost Carrier Market?

Challenges in the Asia Pacific LCC market include rising fuel prices, stringent regulatory environments, and competition from full-service carriers offering budget alternatives. The fluctuating costs of aviation fuel also pose a major challenge to operational efficiency.

03. Who are the major players in the Asia Pacific Low Cost Carrier Market?

Key players in the Asia Pacific LCC market include AirAsia Group, Indigo, Scoot, Jetstar Airways, and VietJet Air. These companies dominate the market through strategic route expansion, competitive pricing, and high aircraft utilization.

04. What are the growth drivers of the Asia Pacific Low Cost Carrier Market?

Growth of the Asia Pacific LCC market is fueled by rising disposable incomes, increased demand for budget travel, and the expansion of tourism in emerging economies. Moreover, the liberalization of aviation policies in many countries further facilitates market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.