Asia Pacific Multiple Sclerosis Drugs Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD6360

November 2024

85

About the Report

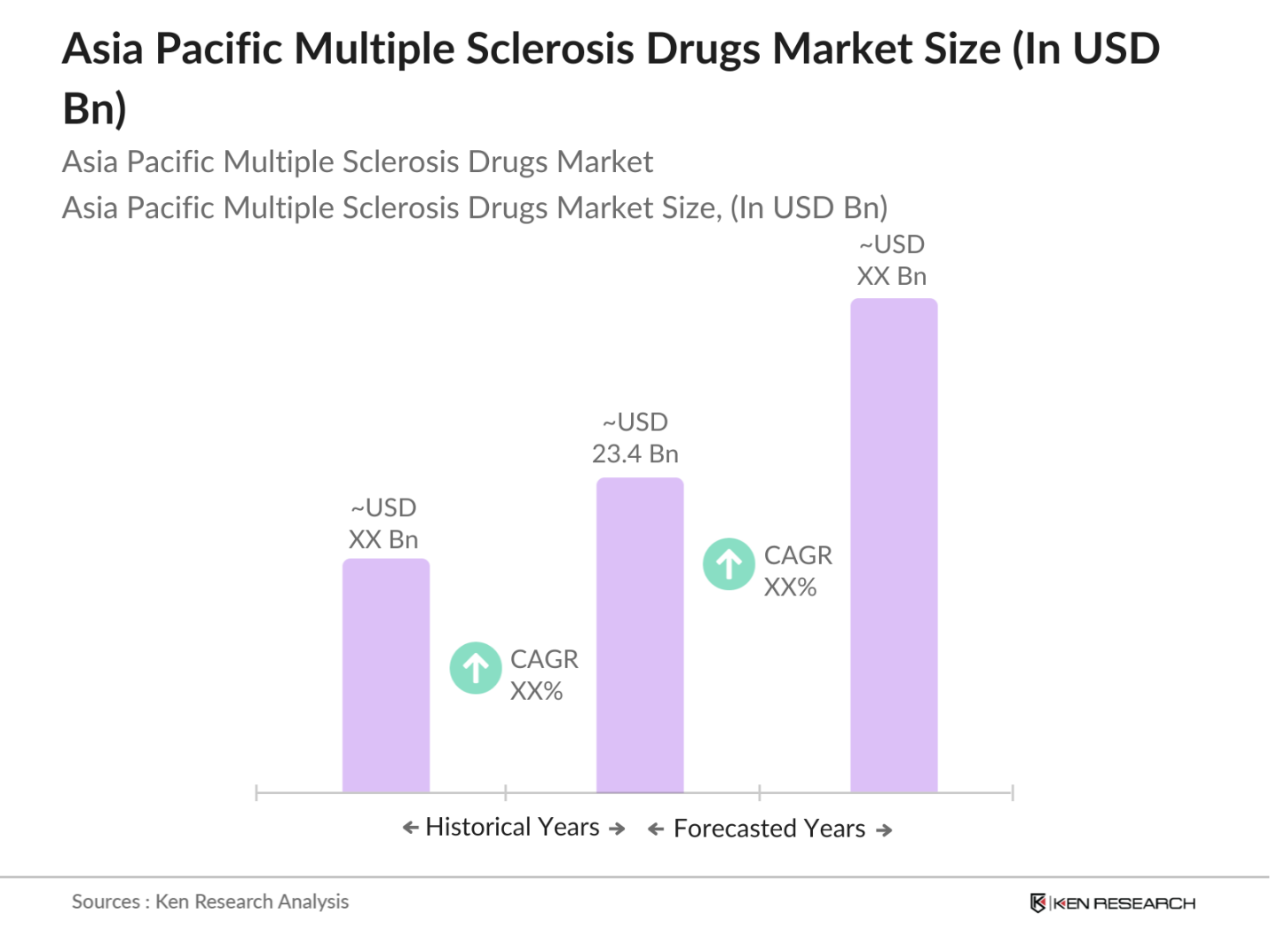

Asia Pacific Multiple Sclerosis Drugs Market Overview

- The Asia Pacific multiple sclerosis (MS) drugs market, valued at USD 23.4 billion, is driven by rising incidences of MS across the region and continuous advancements in drug formulations. The growing focus on biologics and biosimilars, coupled with an increase in early diagnosis initiatives and the availability of improved treatment options, has fueled market growth. Urbanization and improving healthcare access are contributing to a higher diagnosis rate, further expanding the market.

- Countries like China, Japan, and India dominate the Asia Pacific multiple sclerosis drugs market due to their large populations, higher healthcare spending, and rapid advancements in medical infrastructure. China, in particular, has seen significant investments in research and development for neurological diseases. Meanwhile, Japan's aging population and the country's focus on healthcare innovation have positioned it as a leader in the MS drugs market.

- Drug pricing in the Asia Pacific region is highly regulated, with governments like Japans setting strict price controls on biologic and biosimilar drugs. In 2023, Japans National Health Insurance system implemented a pricing policy that reduced the price of MS biologics by 15%, helping to make treatment more accessible. Similarly, Indias National Pharmaceutical Pricing Authority regulates MS drug prices, capping prices on several key treatments.

Asia Pacific Multiple Sclerosis Drugs Market Segmentation

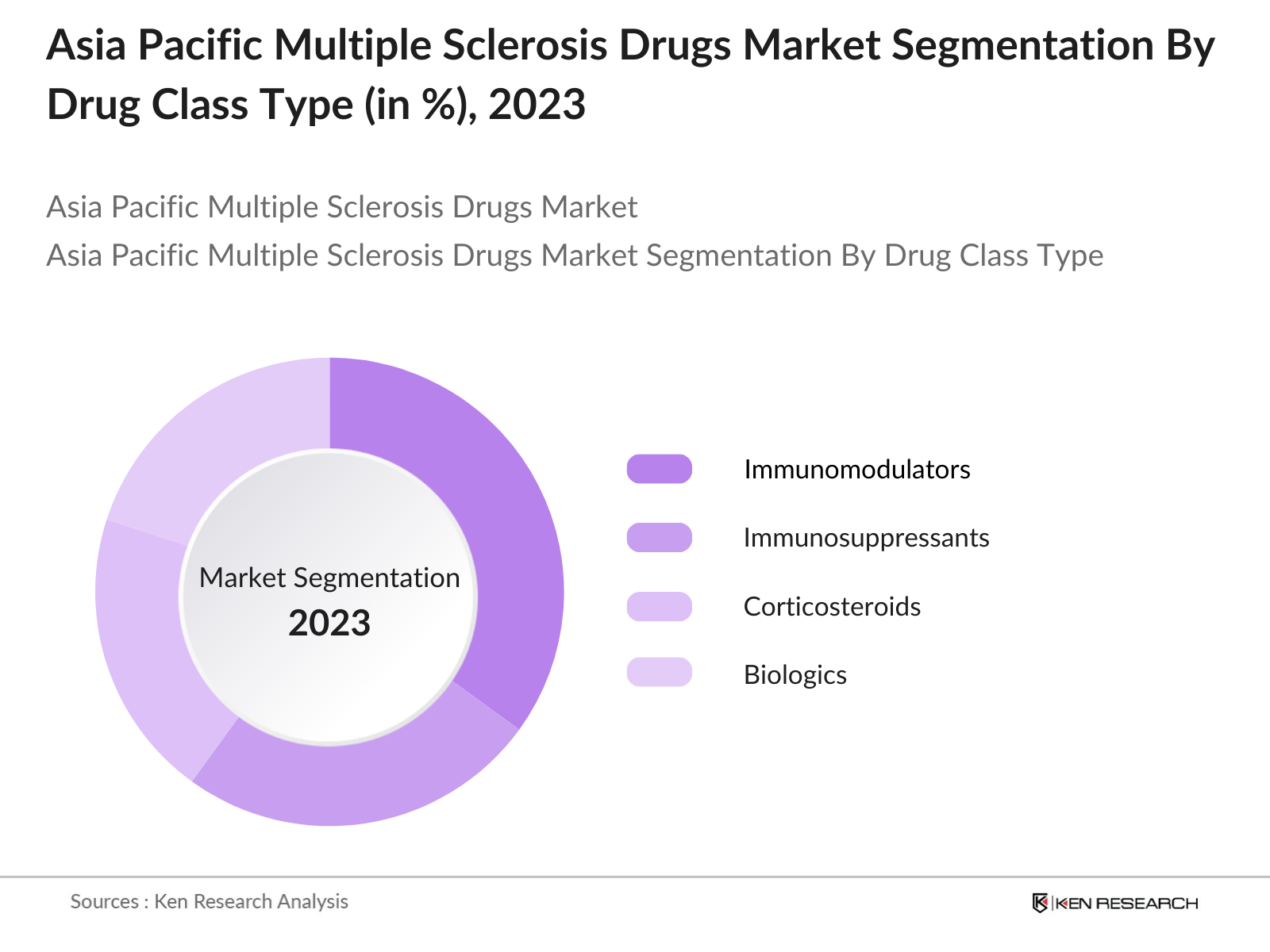

By Drug Class: The Asia Pacific multiple sclerosis drugs market is segmented by drug class into immunomodulators, immunosuppressants, corticosteroids, biologics, and others. Recently, immunomodulators have held a dominant market share under the drug class segmentation. This is due to their widespread use in managing relapsing forms of MS, which are more common. Their efficacy in reducing the frequency and severity of relapses, combined with fewer side effects compared to other drug classes, has made immunomodulators the preferred choice for treatment.

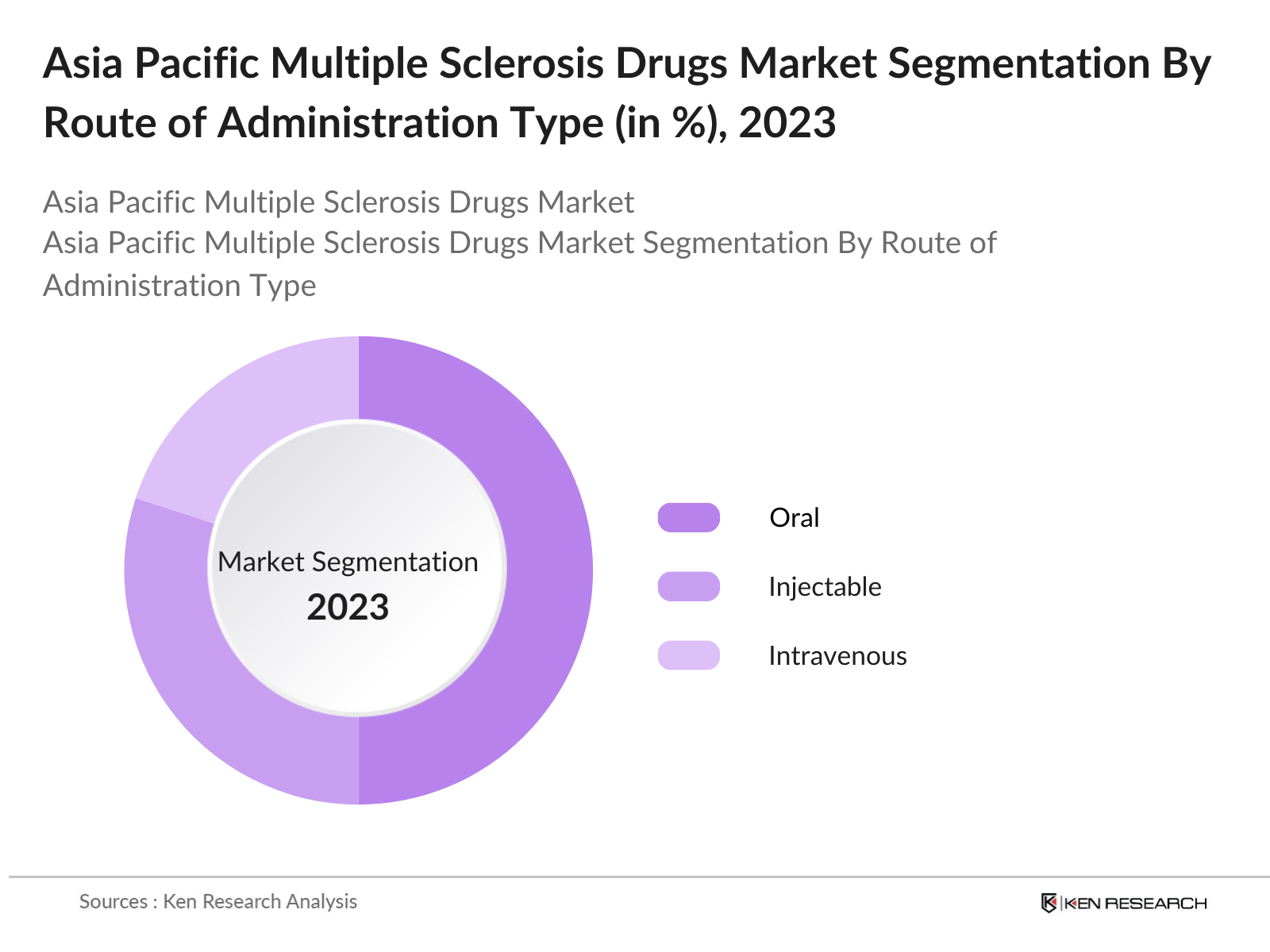

By Route of Administration: The market is also segmented by the route of administration into oral, injectable, and intravenous drugs. Oral drugs dominate the market in this segmentation, with a significant share due to the convenience and patient adherence they offer. Oral therapies, such as dimethyl fumarate, have become highly popular due to their ease of use compared to injectable options, improving patient compliance and overall treatment outcomes.

Asia Pacific Multiple Sclerosis Drugs Market Competitive Landscape

The Asia Pacific MS drugs market is dominated by several major players, including both local and global pharmaceutical companies. This consolidation is driven by their extensive product portfolios, significant R&D investments, and strong distribution networks across the region. The competitive landscape reflects the high entry barriers due to the complexity of drug development for neurological disorders, particularly in biologics and biosimilars.

Asia Pacific Multiple Sclerosis Drugs Industry Analysis

Growth Drivers

- Increasing prevalence of multiple sclerosis: The Asia Pacific region has seen an increase in the prevalence of multiple sclerosis (MS), with recent data showing that over 50,000 individuals in countries like Japan and South Korea are affected by the disease. In Australia, MS affects about 25,600 people, according to the Australian Institute of Health and Welfare. India and China, though historically low in reported cases, are witnessing an upward trend in diagnoses, likely due to improved diagnostics and better reporting mechanisms in urban areas. This growing prevalence is driving demand for MS drugs and treatment advancements in the region.

- Growing healthcare expenditure in the Asia Pacific: Government spending on healthcare has been on the rise in the Asia Pacific, with countries like Japan allocating over USD 450 billion to healthcare in 2023, up from USD 411 billion in 2022, as reported by Japans Ministry of Health, Labour and Welfare. Australias healthcare budget also surpassed USD 100 billion in 2023, emphasizing improved accessibility to treatment for chronic conditions like MS. This increased financial allocation has led to a stronger healthcare infrastructure, allowing for better access to MS treatments across the region.

- Advances in treatment modalities: The Asia Pacific region is at the forefront of advances in MS treatment, particularly with the introduction of biologics, biosimilars, and gene therapies. Japans healthcare market has seen biologic drug approval in 2023, such as Ocrelizumab, a widely adopted drug for treating primary progressive MS. In South Korea, investments in biosimilars development have surged, with the country producing biosimilars for global markets worth over USD 2 billion. This has fueled competitive pricing and expanded patient access to innovative therapies.

Market Challenges

- High cost of biologic treatments: The high cost of biologic treatments remains a significant barrier in the Asia Pacific, with prices ranging from USD 30,000 to USD 70,000 per year for drugs like Ocrelizumab and Alemtuzumab. These prices are significantly higher in countries like Japan and Australia compared to generic drug costs in countries like India, where biosimilars are more affordable due to government price regulations. Such disparities in drug costs create challenges for equal access across the region.

- Regulatory hurdles in drug approval: Drug approval processes in Asia Pacific vary significantly across countries, with countries like Japan and South Korea having stringent approval pathways that delay the introduction of new MS therapies. For instance, Japan's Pharmaceuticals and Medical Devices Agency (PMDA) requires an average of two years for new biologic drugs to be approved, compared to a much faster approval rate in Australia. These regulatory challenges can delay access to newer, potentially more effective MS treatments. PMDA Annual Report

Asia Pacific Multiple Sclerosis Drugs Market Future Outlook

Over the next five years, the Asia Pacific multiple sclerosis drugs market is expected to exhibit robust growth, driven by rising healthcare expenditure, ongoing R&D investments, and advancements in drug discovery technologies. The increasing availability of novel treatments, particularly biologics and biosimilars, will further bolster market growth. Government initiatives to improve healthcare infrastructure and access to treatments in countries like China, India, and Japan will play a significant role in shaping the future of the MS drugs market. Additionally, increasing awareness about MS among healthcare professionals and patients, alongside the focus on early diagnosis, is expected to create new opportunities for pharmaceutical companies.

Opportunities

- Expansion of generics and biosimilars market: The biosimilars market is expanding rapidly in Asia Pacific, particularly in countries like India and South Korea. South Korea, a global leader in biosimilar production, exported biosimilars worth USD 2.7 billion in 2023. India, meanwhile, is seeing the increased domestic production of MS-related biosimilars, offering a significant reduction in treatment costs. This expansion is expected to improve access to affordable MS treatments, particularly in lower-income regions of the Asia Pacific.

- Collaborations between pharma companies and research institutes: Collaborations between pharmaceutical companies and research institutions in the Asia Pacific are fueling innovation in MS treatment. For example, Japans National Institute of Neuroscience has partnered with several pharmaceutical firms to research novel MS therapies, with government support totaling USD 50 million in 2023. Such collaborations are expected to accelerate the development of innovative drugs, biosimilars, and treatment protocols, further boosting the market.

Scope of the Report

|

By Drug Class |

Immunomodulators Immunosuppressants Corticosteroids Biologics Others (including pipeline drugs) |

|

By Route of Administration |

Oral Injectable Intravenous |

|

By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

|

By Type of MS |

Relapsing-Remitting MS (RRMS) Secondary Progressive MS (SPMS) Primary Progressive MS (PPMS) Progressive-Relapsing MS (PRMS) |

|

By Region |

China Japan India Australia Southeast Asia |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Pharmaceutical Companies

Biologic Drug Manufacturing Companies

MS Research Companies

Neurology Clinics and Hospitals

Healthcare Service Provider Companies

Government and Regulatory Bodies (Ministry of Health, Drug Control Authority)

Investors and Venture Capitalist Firms

Biotech Companies

Companies

Players Mentioned in the Report

Biogen

Novartis AG

Roche Holding AG

Sanofi

Teva Pharmaceutical Industries Ltd.

Merck KGaA

Bristol Myers Squibb

Mylan N.V.

Bayer AG

Johnson & Johnson

Table of Contents

1. Asia Pacific Multiple Sclerosis Drugs Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (In relation to rising incidence of multiple sclerosis and advancements in drug formulations)

1.4. Market Segmentation Overview

2. Asia Pacific Multiple Sclerosis Drugs Market Size (In USD Mn)

2.1. Historical Market Size (In USD Mn, Drug Class, Key Regional Insights)

2.2. Year-On-Year Growth Analysis (In USD Mn, Growth Rate)

2.3. Key Market Developments and Milestones

3. Asia Pacific Multiple Sclerosis Drugs Market Analysis

3.1. Growth Drivers

3.1.1. Increasing prevalence of multiple sclerosis

3.1.2. Growing healthcare expenditure in the Asia Pacific

3.1.3. Advances in treatment modalities

3.1.4. Increasing awareness and early diagnosis initiatives

3.2. Market Challenges

3.2.1. High cost of biologic treatments

3.2.2. Regulatory hurdles in drug approval

3.2.3. Limited patient accessibility in rural areas

3.3. Opportunities

3.3.1. Expansion of generics and biosimilars market

3.3.2. Collaborations between pharma companies and research institutes

3.3.3. Digital therapeutics integration

3.4. Trends

3.4.1. Increasing adoption of oral drugs for MS treatment

3.4.2. Shift towards personalized medicine

3.4.3. Growth in research for remyelination therapies

3.5. Government Regulations

3.5.1. Drug pricing policies in Asia Pacific

3.5.2. Accelerated drug approval pathways

3.5.3. Clinical trial standards and requirements

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia Pacific Multiple Sclerosis Drugs Market Segmentation

4.1. By Drug Class (In Value %)

4.1.1. Immunomodulators

4.1.2. Immunosuppressants

4.1.3. Corticosteroids

4.1.4. Biologics

4.1.5. Others (including pipeline drugs)

4.2. By Route of Administration (In Value %) 4.2.1. Oral

4.2.2. Injectable

4.2.3. Intravenous

4.3. By Distribution Channel (In Value %) 4.3.1. Hospital Pharmacies

4.3.2. Retail Pharmacies

4.3.3. Online Pharmacies

4.4. By Type of MS (In Value %) 4.4.1. Relapsing-Remitting MS (RRMS)

4.4.2. Secondary Progressive MS (SPMS)

4.4.3. Primary Progressive MS (PPMS)

4.4.4. Progressive-Relapsing MS (PRMS)

4.5. By Region (In Value %) 4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. Australia

4.5.5. Southeast Asia

5. Asia Pacific Multiple Sclerosis Drugs Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Biogen

5.1.2. Novartis AG

5.1.3. Roche Holding AG

5.1.4. Sanofi

5.1.5. Teva Pharmaceutical Industries Ltd.

5.1.6. Merck KGaA

5.1.7. Bristol Myers Squibb

5.1.8. Mylan N.V.

5.1.9. Bayer AG

5.1.10. Johnson & Johnson

5.1.11. AstraZeneca

5.1.12. Pfizer Inc.

5.1.13. AbbVie Inc.

5.1.14. Eli Lilly and Company

5.1.15. GlaxoSmithKline

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters

5.2.3. R&D Expenditure

5.2.4. Inception Year

5.2.5. Revenue (In USD Mn)

5.2.6. Key Pipeline Drugs

5.2.7. MS Drug Sales

5.2.8. Global Market Share %

5.3. Market Share Analysis (In drug class, key players)

5.4. Strategic Initiatives (Collaborations, partnerships, R&D investments)

5.5. Mergers And Acquisitions (Recent and planned)

5.6. Investment Analysis

5.7. Venture Capital Funding (Specific investments in MS drug R&D)

5.8. Government Grants and Support Programs (Key initiatives supporting MS drug development)

5.9. Private Equity Investments (Focused on MS drug innovations)

6. Asia Pacific Multiple Sclerosis Drugs Market Regulatory Framework

6.1. Drug Approval Processes (Country-specific regulations for MS drugs)

6.2. Compliance and Certification (Pharmaceutical compliance standards)

6.3. Reimbursement Policies (Regional differences in MS drug reimbursement)

7. Asia Pacific Multiple Sclerosis Drugs Market Future Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Multiple Sclerosis Drugs Market Future Segmentation

8.1. By Drug Class (In Value %)

8.2. By Route of Administration (In Value %)

8.3. By Type of MS (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Multiple Sclerosis Drugs Market Analyst Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation and Cohort Analysis

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This step involves creating a comprehensive ecosystem map that covers all significant stakeholders in the Asia Pacific multiple sclerosis drugs market. Detailed desk research is conducted using proprietary and secondary databases to collect market information and identify key variables influencing the market.

Step 2: Market Analysis and Construction

Historical data on the Asia Pacific multiple sclerosis drugs market is compiled and analyzed, including sales figures, treatment uptake rates, and key market developments. This data is used to assess market growth and forecast future trends.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through consultations with industry experts. These insights provide valuable operational and financial data to refine the market models and forecasts.

Step 4: Research Synthesis and Final Output

Direct engagements with pharmaceutical companies are conducted to gather product-level data, consumer preferences, and market insights. These are combined with bottom-up approaches to create a final, validated market analysis for the Asia Pacific MS drugs market.

Frequently Asked Questions

01. How big is the Asia Pacific Multiple Sclerosis Drugs Market?

The Asia Pacific multiple sclerosis drugs market is valued at USD 23.4 billion, driven by rising incidences of MS and advancements in biologic and biosimilar drugs.

02. What are the challenges in the Asia Pacific Multiple Sclerosis Drugs Market?

Key challenges include the high cost of biologic treatments, regulatory barriers across different countries, and limited patient access to specialized care in rural regions.

03. Who are the major players in the Asia Pacific Multiple Sclerosis Drugs Market?

Major players include Biogen, Novartis AG, Roche Holding AG, Sanofi, and Teva Pharmaceutical Industries Ltd., who dominate due to their extensive R&D investments and established product portfolios.

04. What are the growth drivers of the Asia Pacific Multiple Sclerosis Drugs Market?

The market is driven by increasing healthcare expenditure, rising prevalence of MS, and growing demand for biologics and biosimilars. Early diagnosis initiatives also contribute to market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.