Asia Pacific Organic Wine Market Outlook to 2030

Region:Asia

Author(s):Meenakshi

Product Code:KROD4541

November 2024

84

About the Report

Asia Pacific Organic Wine Market Overview

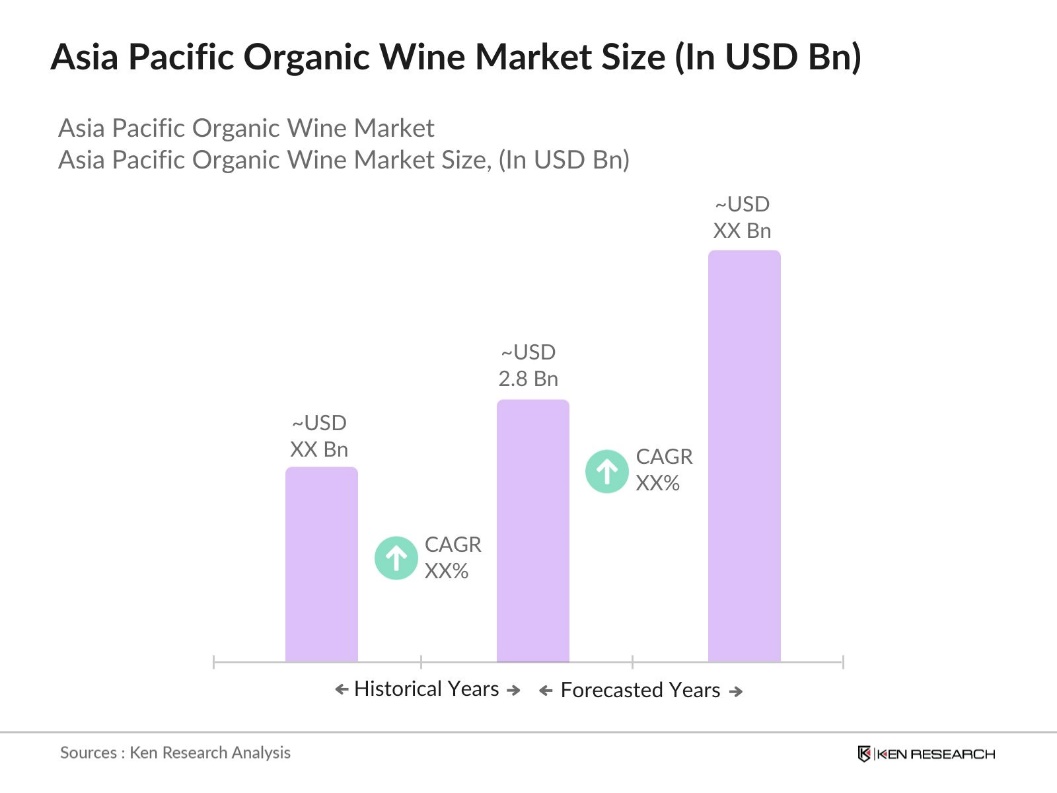

- The Asia Pacific Organic Wine Market is valued at USD 2.8 billion, with strong growth driven by increasing consumer demand for sustainable and organic products. The shift toward health-conscious lifestyles and the preference for natural ingredients have amplified the demand for organic wines. This growth is further propelled by increasing awareness regarding the environmental impact of conventional wine production, with organic wine positioning itself as a more eco-friendly alternative. Additionally, growing disposable income in the region has enabled consumers to spend more on premium organic products.

- Key countries dominating the Asia Pacific organic wine market include Australia, New Zealand, and Japan. Australia and New Zealand have a well-established tradition of organic viticulture, supported by government policies promoting sustainable farming. These nations benefit from ideal climatic conditions that foster organic grape cultivation. Japan, on the other hand, has shown increasing demand for organic wines due to the rising health-consciousness of consumers, who are becoming more inclined towards organic and natural products in the food and beverage sector.

- The new rules for wine labeling in the European Union, effective from December 2023, require all wines from the 2024 harvest to display a list of ingredients and nutritional values. Producers can include this information either on the label or via a QR code. Allergen content must remain on the physical label, and wines must also specify the product category, geographic indication (PDO or PGI), and other key details like alcoholic strength and provenance. These measures aim to enhance transparency and help consumers make informed choices.

Asia Pacific Organic Wine Market Segmentation

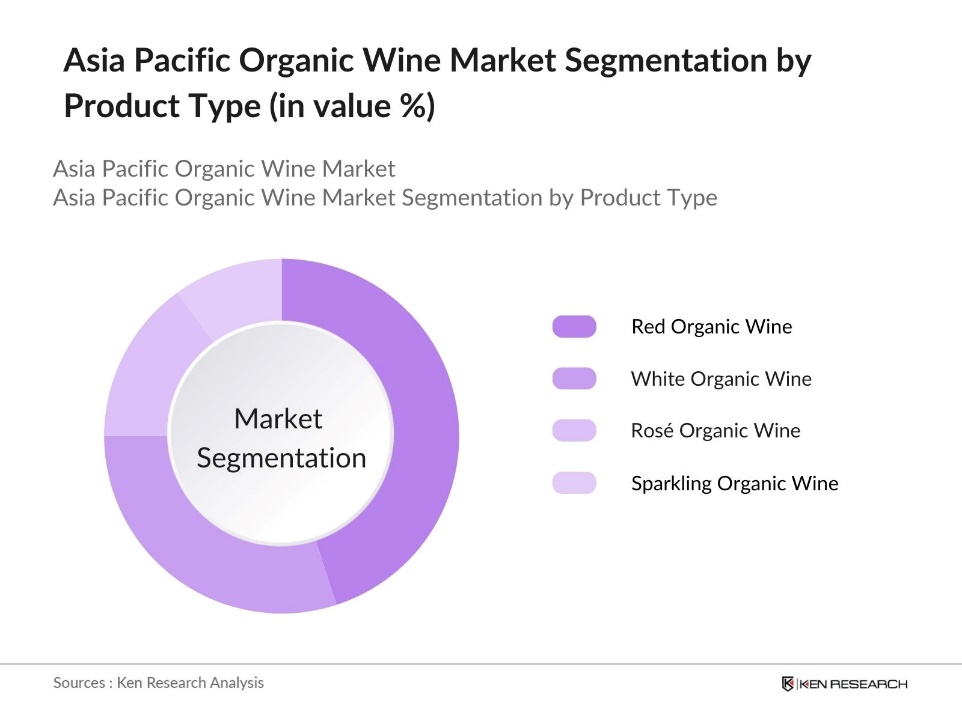

By Product Type: The Asia Pacific organic wine market is segmented by product type into red organic wine, white organic wine, ros organic wine, and sparkling organic wine. Recently, red organic wine has dominated the market due to its rich flavor profile and widespread appeal among both casual and connoisseur wine consumers. Additionally, the health benefits associated with red wine, such as its antioxidant properties, make it an attractive choice for health-conscious individuals, further boosting its demand. Australia and New Zealand are leading producers of red organic wine, ensuring a steady supply to meet this increasing demand.

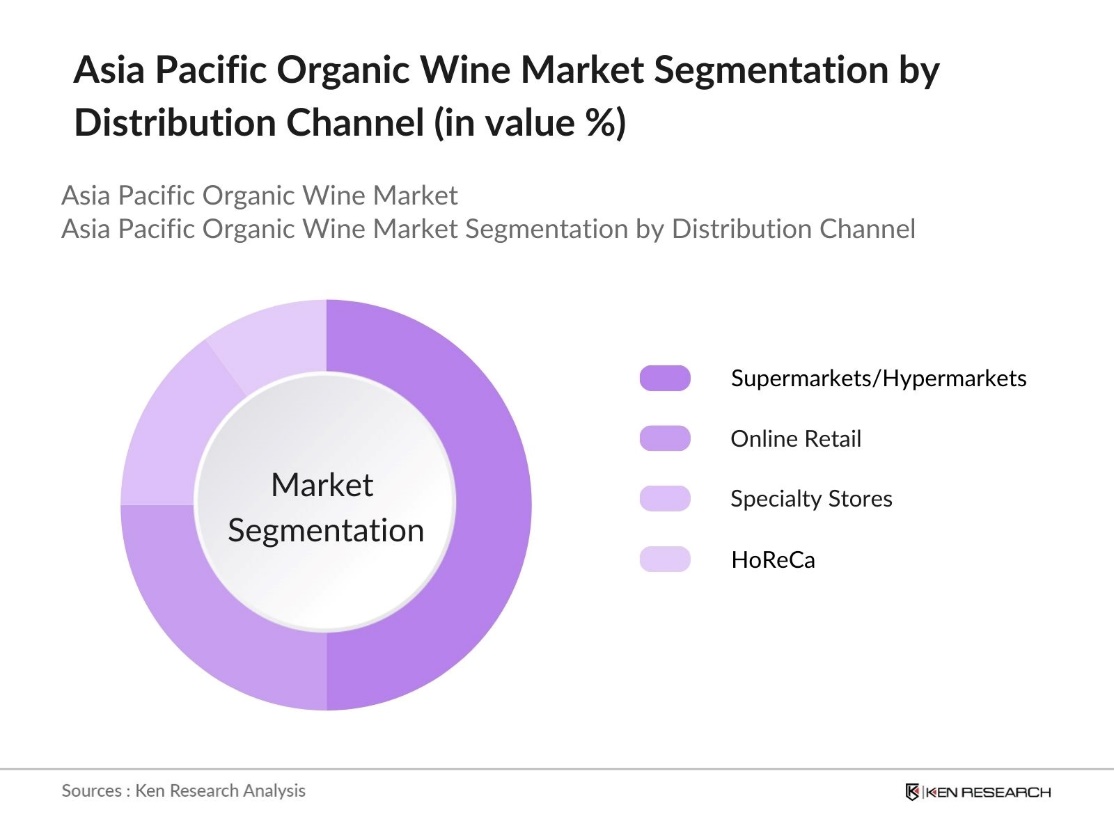

By Distribution Channel: The Asia Pacific organic wine market is segmented by distribution channels into online retail, supermarkets/hypermarkets, specialty stores, and HoReCa (Hotels, Restaurants, Cafes). Supermarkets/hypermarkets hold a dominant market share due to their wide reach and ability to cater to a broad consumer base. The convenience and trust associated with purchasing wine from these established retail chains, as well as promotional offers and wine-tasting events, drive the sales of organic wines through this channel. Additionally, supermarkets offer a range of organic wines at different price points, catering to both budget and premium segments.

Asia Pacific Organic Wine Market Competitive Landscape

The competitive landscape in this market is characterized by a mix of established global players and region-specific companies. Key players include organic wine specialists and traditional winemakers who have diversified their offerings to include organic varieties. The region benefits from Australia and New Zealand's strong production base, while Japan's growing demand for organic products creates opportunities for new entrants and international collaborations.

|

Company |

Establishment Year |

Headquarters |

Certification Type |

No. of Vineyards |

Annual Production Volume |

Main Export Markets |

Revenue (USD Mn) |

Key Organic Varietals |

|

Torres (Spain) |

1870 |

Spain |

||||||

|

Bonterra Organic Vineyards |

1987 |

USA |

||||||

|

Chteau Maris (France) |

1997 |

France |

||||||

|

Yalumba Organic Wines (Australia) |

1849 |

Australia |

||||||

|

Greenstone Vineyards (Australia) |

2003 |

Australia |

Asia Pacific Organic Wine Industry Analysis

Growth Drivers

- Rising Disposable Income (Per Capita Income Growth): The Asia Pacific region has experienced an upsurge in disposable income levels, driving the demand for premium organic wines. According to the IMF's reports indicate that while economic growth in the region was robust, reaching around 5.0% for the year. This income boost, coupled with urbanization trends, is contributing to a higher consumer spend on luxury goods, including organic wines. Countries such as China, India, and Australia have witnessed a surge in the consumption of premium products, making organic wines a growing sector in the alcoholic beverages market.

- Expansion of Organic Vineyards (Land Allocation for Organic Farming) As of 2024, the Asia Pacific region is witnessing a substantial increase in land allocated to organic vineyards. For the fiscal year 202223, Australian organic wine exports totaled 180,000 cases, valued at approximately $10 million FOB, which is around 0.3% of total wine export volume. This expansion is being facilitated by increasing demand for organic products, as consumers become more aware of the environmental benefits of organic agriculture.

- Increasing Consumer Awareness (Health & Sustainability): As of 2024, the Asia Pacific region has experienced a notable rise in consumer awareness regarding health and sustainability. Organic products, including wines, have become increasingly popular as consumers look for healthier, environmentally friendly alternatives that avoid harmful chemicals. This shift in behavior reflects a broader trend toward healthier lifestyles and organic consumption.

Market Challenges

- High Production Costs: Organic wine production tends to be more expensive due to the costs involved in obtaining organic certification and the higher prices of organic inputs like fertilizers and pest control. The process of certification requires significant financial investment, making it challenging for small to medium-sized organic wine producers. Additionally, organic farming often requires more labor-intensive methods and specialized inputs, further driving up production costs.

- Limited Shelf Life: A key challenge for organic wine producers in the Asia Pacific region is the limited shelf life of organic wines. Without synthetic preservatives, organic wines typically have a shorter shelf life compared to conventional wines, which can last longer. This shorter shelf life necessitates more efficient logistics and distribution to prevent spoilage before the wines reach consumers. Organic wines, being more sensitive to storage conditions, require careful handling, which adds another layer of complexity to the supply chain, particularly for smaller producers trying to compete in the broader market.

Asia Pacific Organic Wine Market Future Outlook

The Asia Pacific organic wine market is poised for robust growth over the next five years, driven by a combination of factors such as increased consumer demand for sustainable and organic products, advancements in organic viticulture practices, and expanding distribution networks, especially online. As more consumers prioritize health and environmental sustainability, the organic wine sector will likely see greater adoption, particularly in urban areas across Australia, New Zealand, and Japan.

Market Opportunities

- Growing Demand for Sustainable Products: The demand for sustainably produced goods, particularly those labeled organic and natural, is steadily increasing across the Asia Pacific region. Consumers are becoming more conscious of the environmental and health impacts of their purchasing decisions, leading to a greater preference for organic products, including wines. This shift is being driven by a desire for products that are perceived as healthier and less harmful to the environment.

- Expansion into Emerging Markets: Emerging markets in the Asia Pacific, such as Vietnam, Thailand, and the Philippines, offer significant growth potential for the organic wine industry. As these economies develop, urbanization and rising disposable incomes are contributing to increased consumer demand for premium products like organic wines. The middle class, particularly in younger populations, is showing a growing interest in health-conscious and sustainably sourced products, creating new opportunities for organic wine producers to expand into these developing markets.

Scope of the Report

|

By Product Type |

Red Organic Wine White Organic Wine Ros Organic Wine Sparkling Organic Wine |

|

By Distribution Channel |

Online Retail Supermarkets/Hypermarkets Specialty Stores Horeca |

|

By Certification Type |

USDA Organic EU Organic Australian Certified Organic JAS Organic (Japan) |

|

By End User |

Retail Consumers Horeca |

|

By Region |

Australia New Zealand Japan China India |

Products

Key Target Audience

Organic Wine Producers

Importers and Exporters of Organic Beverages

HoReCa (Hotels, Restaurants, Cafes)

E-commerce Platforms

Government and Regulatory Bodies (Australian Certified Organic, Japan Organic Agriculture Association)

Investment and Venture Capitalist Firms

Banks and Financial Institutions

Companies

Major Players

Torres

Bonterra Organic Vineyards

Chteau Maris

Yalumba Organic Wines

Greenstone Vineyards

Concha y Toro

The Organic Wine Company

Frey Vineyards

Avondale

Kendall-Jackson

Battle of Bosworth Wines

Kalleske Wines

Emiliana Organic Vineyards

La Crema

Bodega Argento

Table of Contents

1. Asia Pacific Organic Wine Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Organic Wine Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Organic Wine Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Consumer Awareness (Health & Sustainability)

3.1.2. Rising Disposable Income (Per Capita Income Growth)

3.1.3. Favorable Government Policies (Subsidies and Certification Incentives)

3.1.4. Expansion of Organic Vineyards (Land Allocation for Organic Farming)

3.2. Market Challenges

3.2.1. High Production Costs (Cost of Organic Certification and Inputs)

3.2.2. Limited Shelf Life (Preservation Techniques in Organic Wines)

3.2.3. Supply Chain Disruptions (Global Trade Barriers and Climate Impacts)

3.3. Opportunities

3.3.1. Growing Demand for Sustainable Products (Organic and Natural Labeling)

3.3.2. Expansion into Emerging Markets (Developing Economies in Asia Pacific)

3.3.3. Development of New Organic Varietals (Grapes Resistant to Pests)

3.4. Trends

3.4.1. Premiumization of Organic Wines (Consumer Shift to High-Quality Organic Wines)

3.4.2. E-commerce Growth (Online Organic Wine Sales and Platforms)

3.4.3. Collaborations with Fine Dining (Partnerships with High-End Restaurants)

3.5. Government Regulations

3.5.1. Certification Standards (Organic Certification Bodies)

3.5.2. Import and Export Regulations (Wine Trade Policies)

3.5.3. Labelling Requirements (Organic Claims and Transparency)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Winemakers, Retailers, Distributors, Consumers)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Asia Pacific Organic Wine Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Red Organic Wine

4.1.2. White Organic Wine

4.1.3. Ros Organic Wine

4.1.4. Sparkling Organic Wine

4.2. By Distribution Channel (In Value %)

4.2.1. Online Retail

4.2.2. Supermarkets/Hypermarkets

4.2.3. Specialty Stores

4.2.4. Horeca (Hotels, Restaurants, Cafes)

4.3. By Certification Type (In Value %)

4.3.1. USDA Organic

4.3.2. EU Organic

4.3.3. Australian Certified Organic

4.3.4. JAS Organic (Japan)

4.4. By End User (In Value %)

4.4.1. Retail Consumers

4.4.2. Horeca

4.5. By Region (In Value %)

4.5.1. Australia

4.5.2. New Zealand

4.5.3. Japan

4.5.4. China

4.5.5. India

5. Asia Pacific Organic Wine Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Torres (Spain)

5.1.2. Bonterra Organic Vineyards (USA)

5.1.3. Chteau Maris (France)

5.1.4. Concha y Toro (Chile)

5.1.5. Emiliana Organic Vineyards (Chile)

5.1.6. The Organic Wine Company (USA)

5.1.7. La Crema (USA)

5.1.8. Bodega Argento (Argentina)

5.1.9. Kendall-Jackson (USA)

5.1.10. Frey Vineyards (USA)

5.1.11. Avondale (South Africa)

5.1.12. Yalumba Organic Wines (Australia)

5.1.13. Battle of Bosworth Wines (Australia)

5.1.14. Kalleske Wines (Australia)

5.1.15. Greenstone Vineyards (Australia)

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Annual Revenue, Certification Type, Production Volume, Vineyard Size, Export Markets)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Organic Wine Market Regulatory Framework

6.1. Organic Farming Laws

6.2. Certification Processes

6.3. Import/Export Regulations

7. Asia Pacific Organic Wine Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Organic Wine Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By Certification Type (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Organic Wine Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis

9.3. White Space Opportunity Analysis

9.4. Marketing Initiatives

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first phase involves mapping out the ecosystem of the Asia Pacific organic wine market. Extensive desk research, utilizing secondary sources like industry reports, government databases, and proprietary research tools, is used to identify critical factors influencing the market, such as consumer preferences, environmental regulations, and production constraints.

Step 2: Market Analysis and Construction

In this stage, historical data related to the organic wine market is collected, including market penetration rates and revenue figures. The analysis also assesses trends in consumer behavior, production practices, and distribution channels to ensure accurate revenue projections and market segmentation.

Step 3: Hypothesis Validation and Expert Consultation

To validate the market assumptions, interviews with industry experts, including winemakers, distributors, and regulatory bodies, are conducted. These consultations provide practical insights into market dynamics, product performance, and future trends.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing all collected data, including inputs from market participants, to provide a detailed, reliable analysis of the Asia Pacific organic wine market. This output ensures that the final report is comprehensive and accurate.

Frequently Asked Questions

01. How big is the Asia Pacific Organic Wine Market?

The Asia Pacific Organic Wine Market is valued at USD 2.8 billion, driven by the rising demand for sustainable products and the region's expanding organic wine production.

02. What are the challenges in the Asia Pacific Organic Wine Market?

The key challenges in Asia Pacific Organic Wine Market include high production costs associated with organic certification, limited shelf life of organic wines, and supply chain disruptions due to global trade issues and climate change impacts.

03. Who are the major players in the Asia Pacific Organic Wine Market?

Key players in Asia Pacific Organic Wine Market include Torres, Bonterra Organic Vineyards, Château Maris, Yalumba Organic Wines, and Greenstone Vineyards. These companies are leaders due to their well-established vineyards, strong market presence, and commitment to organic viticulture.

04. What are the growth drivers of the Asia Pacific Organic Wine Market?

The Asia Pacific Organic Wine Market is driven by increasing consumer awareness of health and environmental sustainability, government policies promoting organic farming, and advancements in organic wine production techniques.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.