Asia Pacific Packaged Tuna Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD4778

December 2024

97

About the Report

Asia Pacific Packaged Tuna Market Overview

- The Asia Pacific packaged tuna market is valued at USD 4.4 billion, driven by a combination of factors including rising health awareness, the demand for convenient ready-to-eat foods, and the expansion of the retail sector across the region. Tuna is seen as a healthy protein source, rich in omega-3 fatty acids, and its increasing presence in supermarkets and e-commerce platforms has fueled market growth. The market's robust performance is supported by the growth of sustainable fishing practices and the introduction of premium and organic tuna products.

- Several countries dominate the Asia Pacific packaged tuna market, including Thailand, Japan, and the Philippines. Thailand, being one of the worlds largest exporters of canned tuna, benefits from its strong fishing industry and advanced processing capabilities. Japans high demand for premium seafood and sushi-grade tuna contributes to its dominance, while the Philippines holds a competitive edge due to its abundant marine resources and cost-effective labor in the fishing and canning industries.

- Government regulations related to fishing quotas and environmental standards are increasingly impacting the packaged tuna market. Many countries in the Asia Pacific are implementing stricter fishing quotas to preserve tuna populations, with the Western Central Pacific Fisheries Commission establishing quotas that could decrease total catch volumes by 15% by 2024. These regulations aim to promote sustainable fishing practices and protect marine biodiversity, but they may also lead to supply constraints for tuna processors. Compliance with these standards is crucial for companies to ensure long-term viability and market competitiveness in an environment that prioritizes sustainability.

Asia Pacific Packaged Tuna Market Segmentation

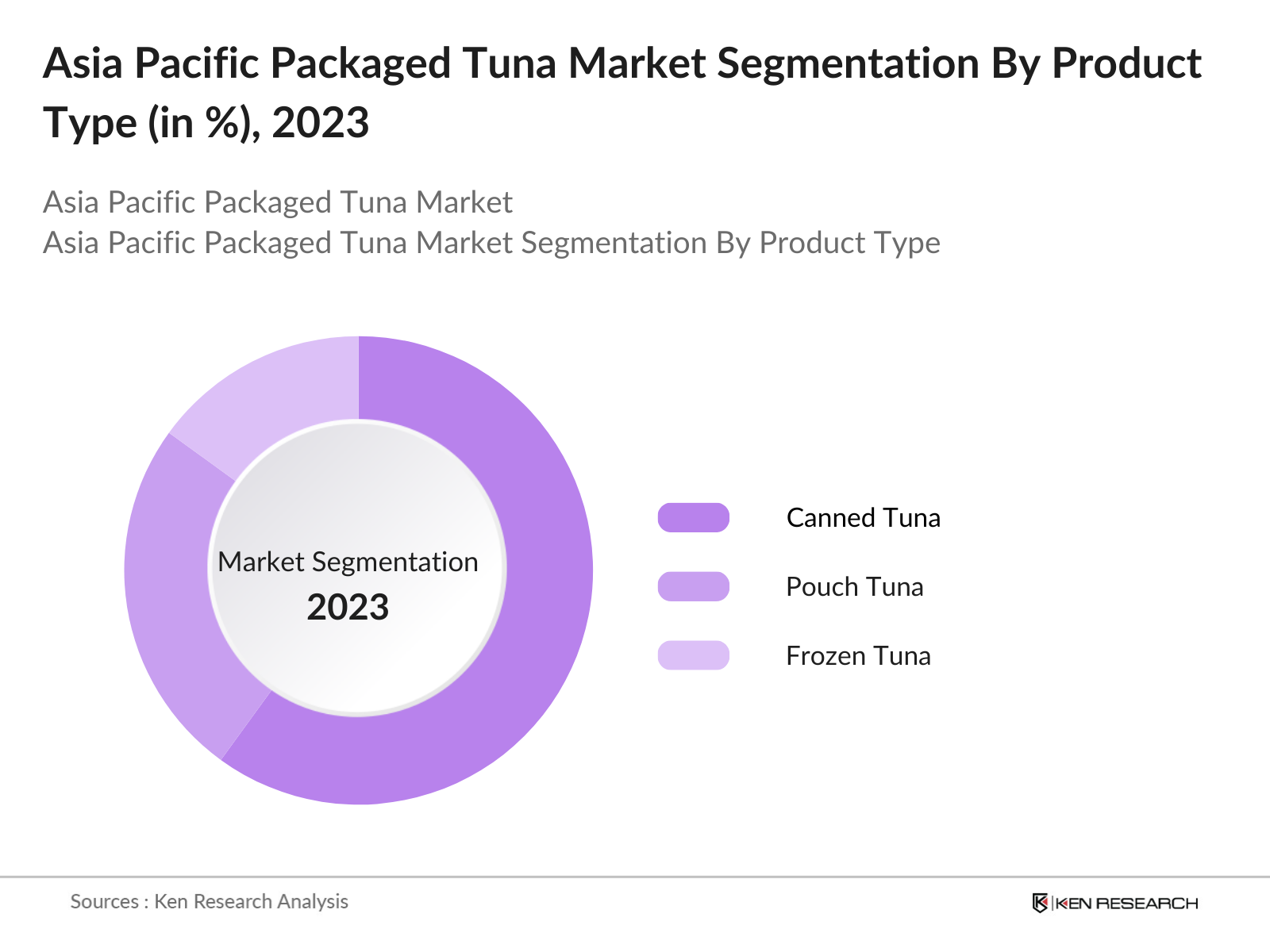

By Product Type: The Asia Pacific packaged tuna market is segmented by product type into canned tuna, pouch tuna, and frozen tuna. Canned tuna holds a dominant market share in this segmentation due to its longer shelf life, affordability, and widespread availability across supermarkets and retail stores. Major global brands have a strong presence in this segment, and it remains a consumer favorite for its versatility and convenience.

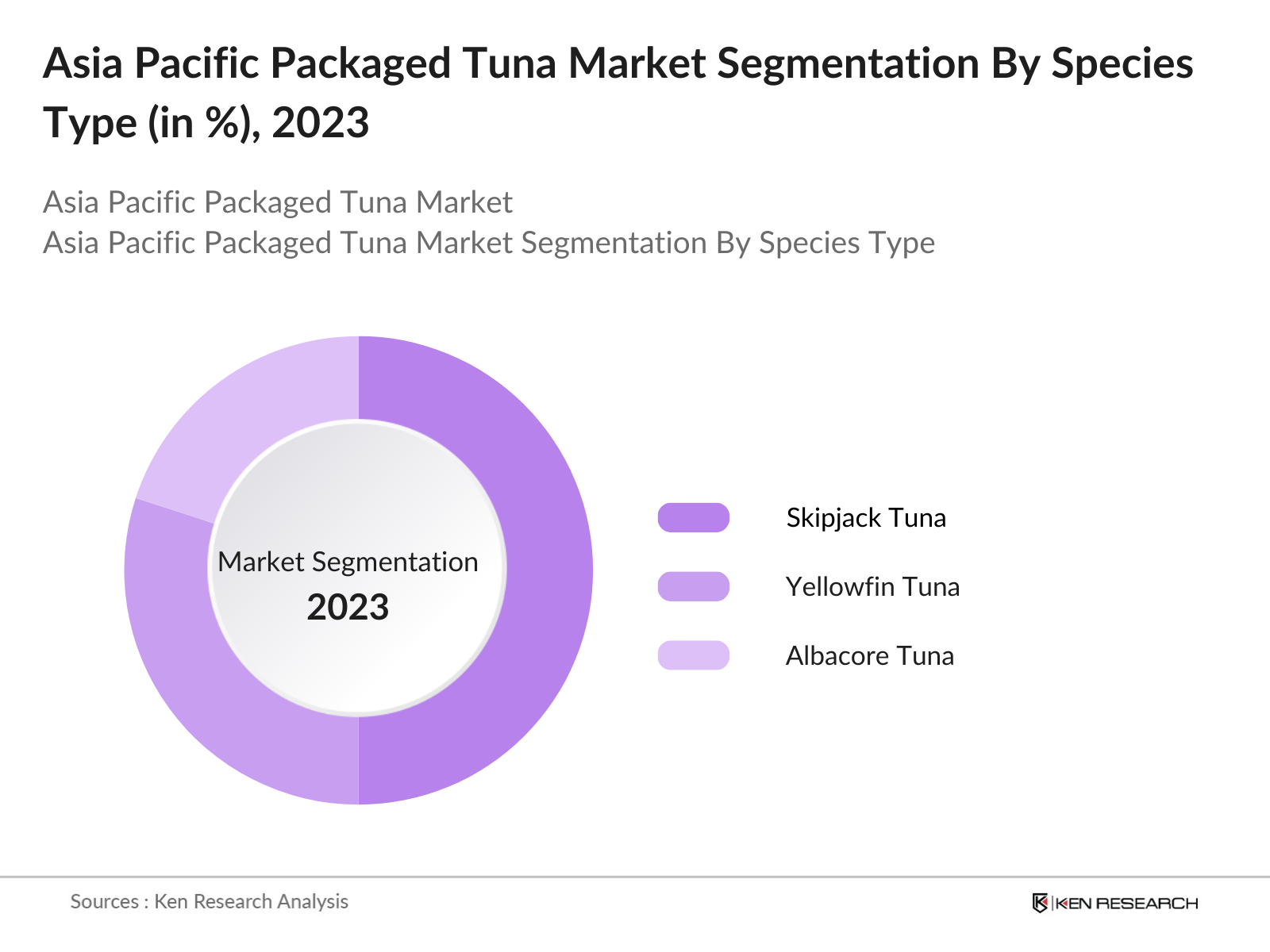

By Species Type: The market is also segmented by species type, including skipjack tuna, yellowfin tuna, and albacore tuna. Skipjack tuna holds the largest market share, accounting for the majority of canned tuna products due to its availability and lower cost compared to other species. Its wide use in canned products makes it a staple in both domestic consumption and exports, particularly in Thailand and the Philippines. The Asia Pacific packaged tuna market is highly consolidated, with large players like Thai Union Group and Dongwon Industries leading the industry. The focus on sustainability and eco-friendly packaging solutions, such as BPA-free cans and innovative pouch technology, has further strengthened these companies' positions in the market. Regional players, such as Century Pacific Food Inc., also compete strongly by leveraging cost-effective production methods and focusing on product diversification.

Asia Pacific Packaged Tuna Market Competitive Landscape

The Asia Pacific packaged tuna market is dominated by several key players, both regional and international, who control the majority of market share. These players have established strong supply chains, invested in sustainability initiatives, and focused on packaging innovations to maintain market competitiveness.

|

Company Name |

Establishment Year |

Headquarters |

Revenue |

Sustainability Initiatives |

No. of Employees |

Packaging Innovations |

Product Range |

Market Presence |

Distribution Channels |

|

Thai Union Group |

1977 |

Bangkok, Thailand |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Bumble Bee Foods |

1899 |

San Diego, USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Dongwon Industries |

1969 |

Seoul, South Korea |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Century Pacific Food Inc. |

1978 |

Manila, Philippines |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

FCF Fishery Co. Ltd. |

1972 |

Kaohsiung, Taiwan |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

Asia Pacific Packaged Tuna Industry Analysis

Growth Drivers

- Rising Health Consciousness: The demand for packaged tuna in the Asia Pacific is significantly influenced by rising health consciousness among consumers. With an increasing emphasis on health and nutrition, many individuals are opting for protein-rich diets, and tuna offers a low-calorie source of high-quality protein. As per the World Health Organization, a healthy diet should include a minimum of 30% protein. Moreover, reports indicate that 65% of consumers in Asia Pacific are actively seeking healthier food options, contributing to a growth trajectory for packaged tuna products. This growing awareness aligns with the forecasted rise in health food sales in the region, which is expected to reach USD 36 billion by 2025.

- Expansion of Distribution Channels: The expansion of distribution channels, particularly through supermarkets and e-commerce platforms, has facilitated the increased availability of packaged tuna in the Asia Pacific region. In 2023, e-commerce sales in the food and beverage sector reached USD 125 billion, reflecting a significant 30% increase from the previous year, primarily driven by changing consumer behaviors during the pandemic. Furthermore, major supermarket chains have started to incorporate dedicated seafood sections, enhancing the visibility and accessibility of tuna products. This shift in shopping habits is expected to further boost sales, with projections indicating that online grocery shopping will encompass 20% of total grocery sales in the region by 2025.

- Government Support for Sustainable Fishing Practices: Governments in the Asia Pacific are increasingly advocating for sustainable fishing practices to ensure the longevity of fish stocks and promote environmental health. Initiatives like the Australian Governments Fisheries Research and Development Corporation (FRDC) fund programs aimed at sustainable fisheries management. The UN Food and Agriculture Organization reports that sustainable fishing can increase fish stocks by up to 50%, promoting both ecological balance and economic growth. Additionally, governments are implementing regulations that incentivize sustainable practices, with funding reaching approximately USD 20 million in support of sustainable seafood initiatives in 2023. This government backing is crucial for enhancing the packaged tuna markets growth prospects in the region.

Market Challenges

- Rising Raw Material Costs: The packaged tuna market faces significant challenges due to rising raw material costs, affecting both fishing operations and packaging materials. The global price of tuna fish has seen a surge, with a reported increase of 15% in 2023 due to overfishing and stricter regulations on fishing quotas. Concurrently, packaging materials such as plastics have experienced price hikes, influenced by global supply chain disruptions, which have risen by 20% since 2022. This escalation in costs can squeeze profit margins for manufacturers and lead to higher retail prices for consumers, potentially hampering market growth. Manufacturers must adapt by optimizing their operations and exploring cost-effective sourcing options.

- Stringent Environmental Regulations: The implementation of stringent environmental regulations presents a notable challenge for the packaged tuna market in the Asia Pacific. Governments are instituting fishing quotas and sustainability measures to protect dwindling fish populations, which have led to reduced catch limits. For instance, the Western and Central Pacific Fisheries Commission has set catch limits that are projected to decrease overall tuna harvest by approximately 10% in 2024. These regulations aim to ensure long-term sustainability but may limit the supply of tuna available for processing and packaging, leading to increased competition and potential price volatility in the market.

Asia Pacific Packaged Tuna Market Future Outlook

Over the next five years, the Asia Pacific packaged tuna market is expected to witness steady growth, driven by rising consumer demand for healthy, protein-rich foods and ongoing advancements in sustainable fishing and packaging technologies. The increasing popularity of convenience foods, coupled with the expansion of online retail channels, will further enhance market accessibility and fuel demand. Government regulations promoting sustainable fishing and trade liberalization will also play a key role in shaping the market's trajectory. As consumers continue to shift toward premium and organic seafood options, companies that invest in eco-friendly practices and product innovation are expected to gain a competitive edge. The growing focus on reducing overfishing and ensuring traceability in the supply chain will be critical for long-term market success.

Opportunities

- Technological Innovations in Packaging: Technological advancements in packaging are creating opportunities for the packaged tuna market by extending shelf life and enhancing product quality. Innovations such as vacuum packaging and modified atmosphere packaging (MAP) can significantly reduce spoilage rates, currently estimated at 10-20% for fresh seafood. In 2023, the global market for smart packaging technologies reached USD 30 billion, with applications in food preservation seeing substantial growth. Companies implementing these technologies can improve consumer confidence, reduce waste, and increase market share by offering longer-lasting products. This trend reflects a growing consumer preference for quality and convenience, driving future growth.

- Growing Demand for Premium and Organic Tuna Products: The demand for premium and organic tuna products is on the rise in the Asia Pacific region, driven by increasing consumer awareness of health and sustainability. In 2023, organic food sales reached USD 28 billion in Asia, with seafood being one of the fastest-growing segments. This demand aligns with global trends, where consumers are willing to pay a premium for sustainably sourced and certified organic products. The introduction of certified organic tuna products can help brands capture market share among health-conscious consumers, with estimates indicating that organic seafood sales could increase by 15% annually, creating significant growth opportunities for producers.

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Tuna Processing Companies

Packaged Food Industries

Supermarkets and Hypermarkets Companies

E-Commerce Companies

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (Marine Stewardship Council, ASEAN Fishing Regulation Board)

Seafood Exporter Industries

Packaging Innovation Companies

Companies

Players Mentioned in the Report

Thai Union Group

Bumble Bee Foods

Dongwon Industries

FCF Fishery Co. Ltd.

Century Pacific Food Inc.

Bolton Group

Jealsa Rianxeira S.A.

Wild Planet Foods Inc.

Pataya Food Industries

Ocean Brands

Table of Contents

1. Asia Pacific Packaged Tuna Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Packaged Tuna Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Packaged Tuna Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Health Awareness

3.1.2. Growing Demand for Convenient Food Products

3.1.3. Expansion of Retail Distribution Channels

3.1.4. Rising Popularity of Seafood among Consumers

3.2. Market Challenges

3.2.1. Supply Chain Disruptions

3.2.2. Sustainability and Overfishing Concerns

3.2.3. High Competition in Packaged Food Market

3.3. Opportunities

3.3.1. Demand for Sustainable and Eco-Friendly Packaging

3.3.2. Product Innovation (Flavored Tuna, Low-Sodium Options)

3.3.3. Expansion into Emerging Economies

3.4. Trends

3.4.1. Increasing Preference for Ready-to-Eat Tuna Products

3.4.2. Growth in E-commerce Sales of Packaged Tuna

3.4.3. Surge in Tuna-based Meal Kits and Prepared Meals

3.5. SWOT Analysis

3.6. Stakeholder Ecosystem

3.7. Porter’s Five Forces

3.8. Competition Ecosystem

4. Asia Pacific Packaged Tuna Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Canned Tuna

4.1.2. Pouched Tuna

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Convenience Stores

4.2.3. Online Retail

4.3. By End-User (In Value %)

4.3.1. Retail Consumers

4.3.2. Foodservice Operators (Restaurants, Hotels)

4.4. By Packaging Type (In Value %)

4.4.1. Metal Cans

4.4.2. Flexible Pouches

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. South Korea

4.5.5. Southeast Asia

5. Asia Pacific Packaged Tuna Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Thai Union Group

5.1.2. Dongwon Industries

5.1.3. StarKist Co.

5.1.4. Bumble Bee Foods LLC

5.1.5. Tri Marine International

5.1.6. Ocean Harvest

5.1.7. Mitsui & Co. Ltd.

5.1.8. Maruha Nichiro Corporation

5.1.9. Sea Value Co. Ltd.

5.1.10. Tongwei Co., Ltd.

5.1.11. Wild Planet Foods

5.1.12. Royal Greenland A/S

5.1.13. H.J. Heinz Company

5.1.14. Chicken of the Sea International

5.1.15. ICMS Group

5.2. Cross Comparison Parameters (Revenue, Production Capacity, Geographic Reach, Brand Strength, Sustainability Practices, Market Share, Pricing Strategy, R&D Investment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Packaged Tuna Market Regulatory Framework

6.1. Food Safety Standards

6.2. Certification and Labeling Requirements

6.3. Environmental Sustainability Guidelines

6.4. Trade Regulations and Export-Import Policies

7. Asia Pacific Packaged Tuna Market Future Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Packaged Tuna Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By End-User (In Value %)

8.4. By Packaging Type (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Packaged Tuna Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research began by identifying major stakeholders and key variables within the Asia Pacific packaged tuna market. Through a combination of secondary research and proprietary databases, critical factors such as product type, species type, and market drivers were established.

Step 2: Market Analysis and Construction

The analysis involved gathering historical data on market penetration, product preferences, and revenue generation. The analysis also considered the expansion of distribution channels, particularly in emerging economies, and the impact of sustainability on market performance.

Step 3: Hypothesis Validation and Expert Consultation

Key industry experts were consulted through interviews and surveys to validate hypotheses related to market growth, sustainability practices, and consumer preferences. This feedback was instrumental in refining data accuracy and ensuring a comprehensive analysis.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing data from tuna manufacturers and processing companies. The aim was to verify product segmentation, sales trends, and consumer preferences, resulting in an accurate market forecast for the Asia Pacific packaged tuna market.

Frequently Asked Questions

01. How big is the Asia Pacific Packaged Tuna Market?

The Asia Pacific packaged tuna market is valued at USD 4.4 billion, driven by growing health consciousness, demand for ready-to-eat foods, and the expansion of retail and online channels.

02. What are the challenges in the Asia Pacific Packaged Tuna Market?

The major challenges include rising raw material costs, supply chain disruptions, and stringent environmental regulations regarding fishing quotas and sustainability practices.

03. Who are the major players in the Asia Pacific Packaged Tuna Market?

Key players include Thai Union Group, Bumble Bee Foods, Dongwon Industries, FCF Fishery Co. Ltd., and Century Pacific Food Inc., dominating through strong supply chains and sustainability initiatives.

04. What are the growth drivers of the Asia Pacific Packaged Tuna Market?

Growth is driven by increasing health awareness, demand for convenient seafood options, expansion of retail channels, and government support for sustainable fishing practices across the region.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.