Asia Pacific Point Of Care Diagnostics Market Outlook to 2030

Region:Afganistan

Author(s):Naman Rohilla

Product Code:KROD7459

Region:Afganistan

Author(s):Naman Rohilla

Product Code:KROD7459

December 2024

85

Listen to the audio summary

Asia Pacific Point of Care Diagnostics Market Segmentation

The Asia Pacific Point of Care Diagnostics market is dominated by several key players that have established a strong foothold due to their product innovations, extensive distribution networks, and strategic partnerships. Companies like Roche Diagnostics, Abbott Laboratories, and Siemens Healthineers lead the market with a robust portfolio of diagnostic products and services.

|

Company |

Year Established |

Headquarters |

Product Portfolio |

Regional Presence |

R&D Spending |

Technology Integration |

Strategic Partnerships |

Revenue |

|

Roche Diagnostics |

1896 |

Basel, Switzerland |

- |

- |

- |

- |

- |

- |

|

Abbott Laboratories |

1888 |

Illinois, USA |

- |

- |

- |

- |

- |

- |

|

Siemens Healthineers |

1847 |

Erlangen, Germany |

- |

- |

- |

- |

- |

- |

|

Danaher Corporation |

1984 |

Washington, USA |

- |

- |

- |

- |

- |

- |

|

Becton, Dickinson and Company |

1897 |

New Jersey, USA |

- |

- |

- |

- |

- |

- |

Over the next five years, the Asia Pacific Point of Care Diagnostics market is expected to witness growth, driven by increasing investments in healthcare infrastructure, the growing adoption of advanced diagnostic technologies, and rising demand for decentralized healthcare services. The rising burden of chronic diseases such as diabetes and cardiovascular conditions will further fuel demand for point-of-care testing solutions, especially in rural and underdeveloped areas where access to centralized laboratories is limited.

|

By Product Type |

Glucose Monitoring Kits Infectious Disease Testing Kits Cardiac Markers Pregnancy and Fertility Testing Kits Blood Gas/Electrolytes Analysis Devices |

|

By Application |

Hospitals Clinics Homecare Settings Diagnostic Centres Research Laboratories |

|

By Technology |

Lateral Flow Assays Polymerase Chain Reaction (PCR) Microfluidics Immunoassays Biosensors |

|

By End-User |

Public Healthcare Facilities Private Healthcare Providers Academic & Research Institutes Corporate Health Programs NGOs and Government Initiatives |

|

By Region |

China Japan India Australia Southeast Asia |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Growing Prevalence of Chronic Diseases

3.1.2. Increasing Demand for Rapid Diagnostics

3.1.3. Technological Advancements in Diagnostics

3.1.4. Rising Healthcare Expenditure

3.2. Market Challenges

3.2.1. Regulatory Compliance

3.2.2. Cost Constraints in Emerging Markets

3.2.3. Low Awareness in Remote Areas

3.3. Opportunities

3.3.1. Expansion in Rural Healthcare Infrastructure

3.3.2. Growing Focus on Preventive Healthcare

3.3.3. Adoption of AI and Machine Learning in Diagnostics

3.4. Trends

3.4.1. Integration with Telemedicine

3.4.2. Adoption of Wearable Diagnostic Devices

3.4.3. Increased Use of Multiplex Testing Platforms

3.5. Regulatory Landscape

3.5.1. Asia Pacific Medical Device Regulatory Framework

3.5.2. Point of Care Diagnostics Certification Programs

3.5.3. Compliance with ISO Standards

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Glucose Monitoring Kits

4.1.2. Infectious Disease Testing Kits

4.1.3. Cardiac Markers

4.1.4. Pregnancy and Fertility Testing Kits

4.1.5. Blood Gas/Electrolytes Analysis Devices

4.2. By Application (In Value %)

4.2.1. Hospitals

4.2.2. Clinics

4.2.3. Homecare Settings

4.2.4. Diagnostic Centers

4.2.5. Research Laboratories

4.3. By Technology (In Value %)

4.3.1. Lateral Flow Assays

4.3.2. Polymerase Chain Reaction (PCR)

4.3.3. Microfluidics

4.3.4. Immunoassays

4.3.5. Biosensors

4.4. By End-User (In Value %)

4.4.1. Public Healthcare Facilities

4.4.2. Private Healthcare Providers

4.4.3. Academic & Research Institutes

4.4.4. Corporate Health Programs

4.4.5. NGOs and Government Initiatives

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. Australia

4.5.5. Southeast Asia

5.1. Detailed Profiles of Major Companies

5.1.1. Abbott Laboratories

5.1.2. Roche Diagnostics

5.1.3. Siemens Healthineers

5.1.4. Danaher Corporation

5.1.5. Becton, Dickinson and Company

5.1.6. Thermo Fisher Scientific

5.1.7. Johnson & Johnson

5.1.8. PerkinElmer Inc.

5.1.9. QuidelOrtho Corporation

5.1.10. bioMrieux

5.1.11. Hologic Inc.

5.1.12. Sysmex Corporation

5.1.13. Cepheid

5.1.14. Nova Biomedical

5.1.15. EKF Diagnostics

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Regional Presence, R&D Spending, Technology Integration, Growth Strategy, Customer Base, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Medical Device Regulations

6.2. Import/Export Requirements

6.3. Certification Processes

6.4. Quality and Safety Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves identifying key market variables, including diagnostic technologies, product segments, and major stakeholders across the Asia Pacific Point of Care Diagnostics market. This process uses extensive secondary research and proprietary databases to capture relevant industry data and market dynamics.

In this phase, historical market data is analyzed, focusing on product penetration, the ratio of diagnostic tests performed at point-of-care versus centralized laboratories, and revenue generation across major markets. This includes evaluating both public and private sector participation.

Market hypotheses are validated through consultations with industry experts, including senior executives from diagnostic companies, healthcare providers, and regulatory agencies. These insights are obtained through CATI interviews to ensure the robustness of the market estimates and trends.

The final stage involves synthesizing research data from multiple sources, including interviews with point-of-care diagnostic manufacturers, to verify findings and produce a comprehensive report. This process ensures that the analysis is complete and market predictions are accurate.

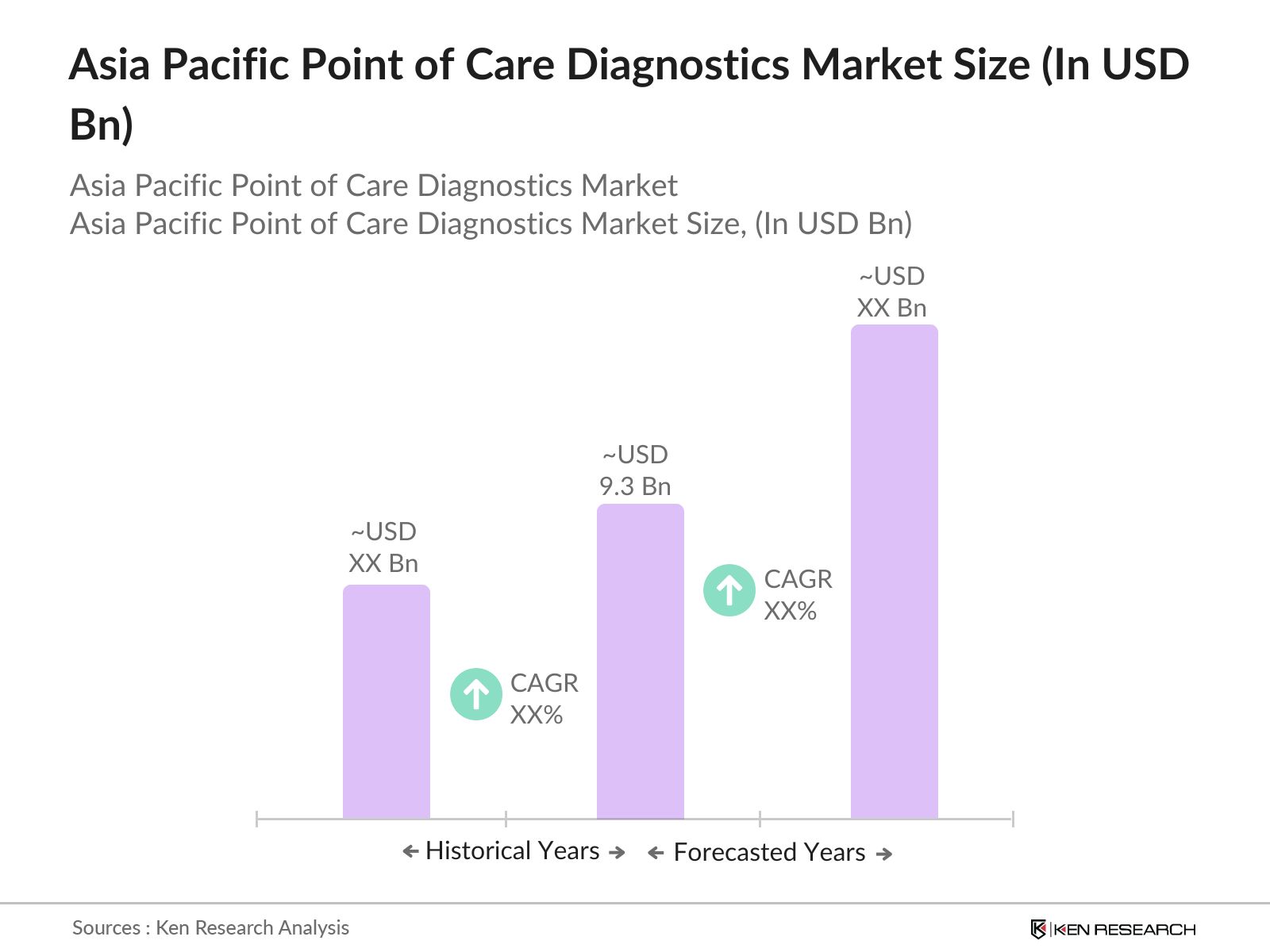

The Asia Pacific Point of Care Diagnostics market is valued at USD 9.3 billion, driven by increasing demand for rapid diagnostic testing, particularly for chronic diseases such as diabetes and cardiovascular conditions.

Challenges in the Asia Pacific Point of Care Diagnostics market include stringent regulatory compliance, the high cost of advanced diagnostic devices, and limited access to healthcare infrastructure in rural and remote areas across the region.

Key players in the Asia Pacific Point of Care Diagnostics market include Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, Danaher Corporation, and Becton, Dickinson and Company. These companies dominate the market through their extensive product portfolios and strong distribution networks.

Growth drivers of the Asia Pacific Point of Care Diagnostics market include the rising prevalence of chronic diseases, the adoption of telemedicine, and increased government investment in healthcare infrastructure across Asia Pacific, particularly in developing countries like India and China.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.