Asia Pacific Polyisobutylene Market Outlook to 2030

Region:Asia

Author(s):Shubham

Product Code:KROD2386

October 2024

123

About the Report

Asia Pacific Polyisobutylene Market Overview

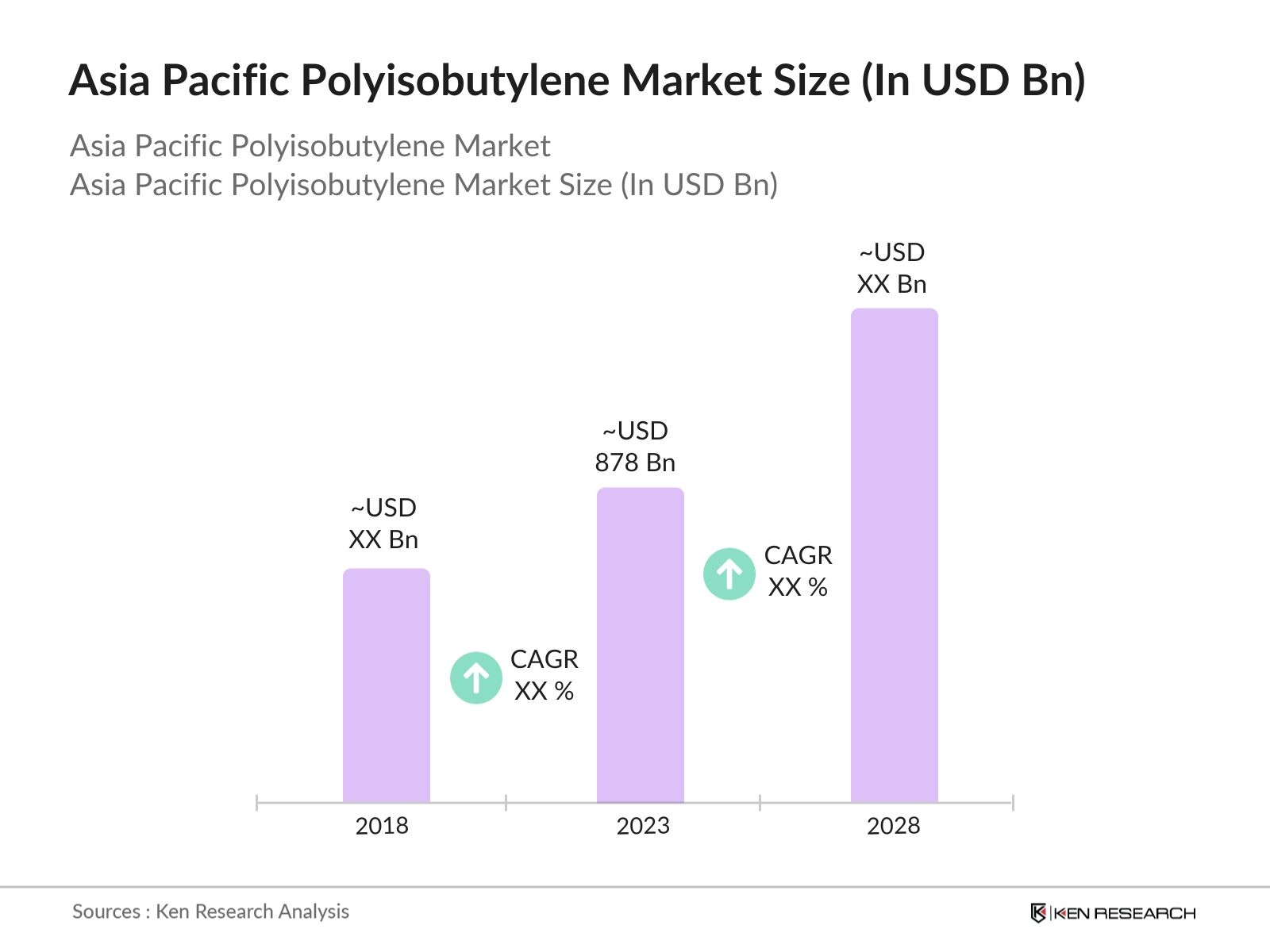

- The Asia-Pacific (APAC) Polyisobutylene Market was valued at USD 878 billion, driven by the rising demand in sectors such as automotive, construction, and packaging. The growing usage of polyisobutylene in adhesives, sealants, and lubricants further supports the market growth. Additionally, increased investment in infrastructure development and the rising automotive production in countries like China and India are boosting the demand for polyisobutylene.

- Leading companies in the Asia-Pacific polyisobutylene market include BASF SE, ExxonMobil, Lubrizol Corporation, and TPC Group. These firms are focusing on expanding their production capacities and innovating new grades of polyisobutylene to cater to various industrial applications.

- Major urban centers driving the APAC polyisobutylene market include Shanghai, Mumbai, and Tokyo. Shanghai benefits from China's robust construction activities, while Mumbai's market is driven by the automotive sector's growth in India. Tokyo plays a key role due to Japan's focus on high-quality industrial lubricants and sealants.

- In 2023, ExxonMobil announced plans to expand its polyisobutylene production facility in Singapore to meet the growing demand in the Asia-Pacific region. This expansion is expected to enhance the supply of high-performance polyisobutylene products used in various applications, particularly in adhesives and lubricants.

Asia Pacific Polyisobutylene Market Segmentation

The Asia Pacific Polyisobutylene Market can be segmented based on grade, application, end-use industry, and region:

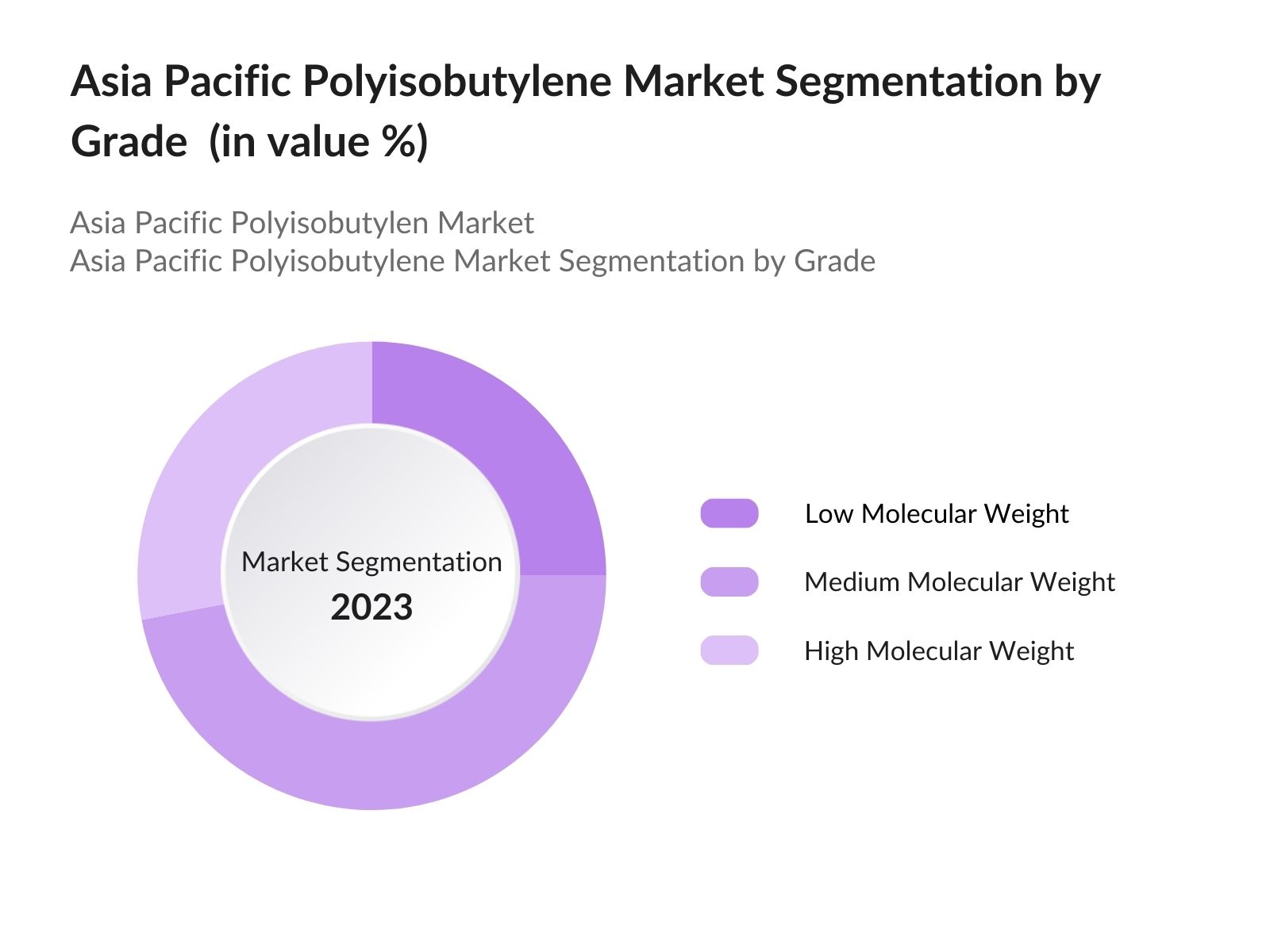

- By Grade: The market is segmented into low molecular weight polyisobutylene, medium molecular weight polyisobutylene, and high molecular weight polyisobutylene. In 2023, medium molecular weight polyisobutylene held the dominant market share due to its extensive use in adhesives, sealants, and automotive components.

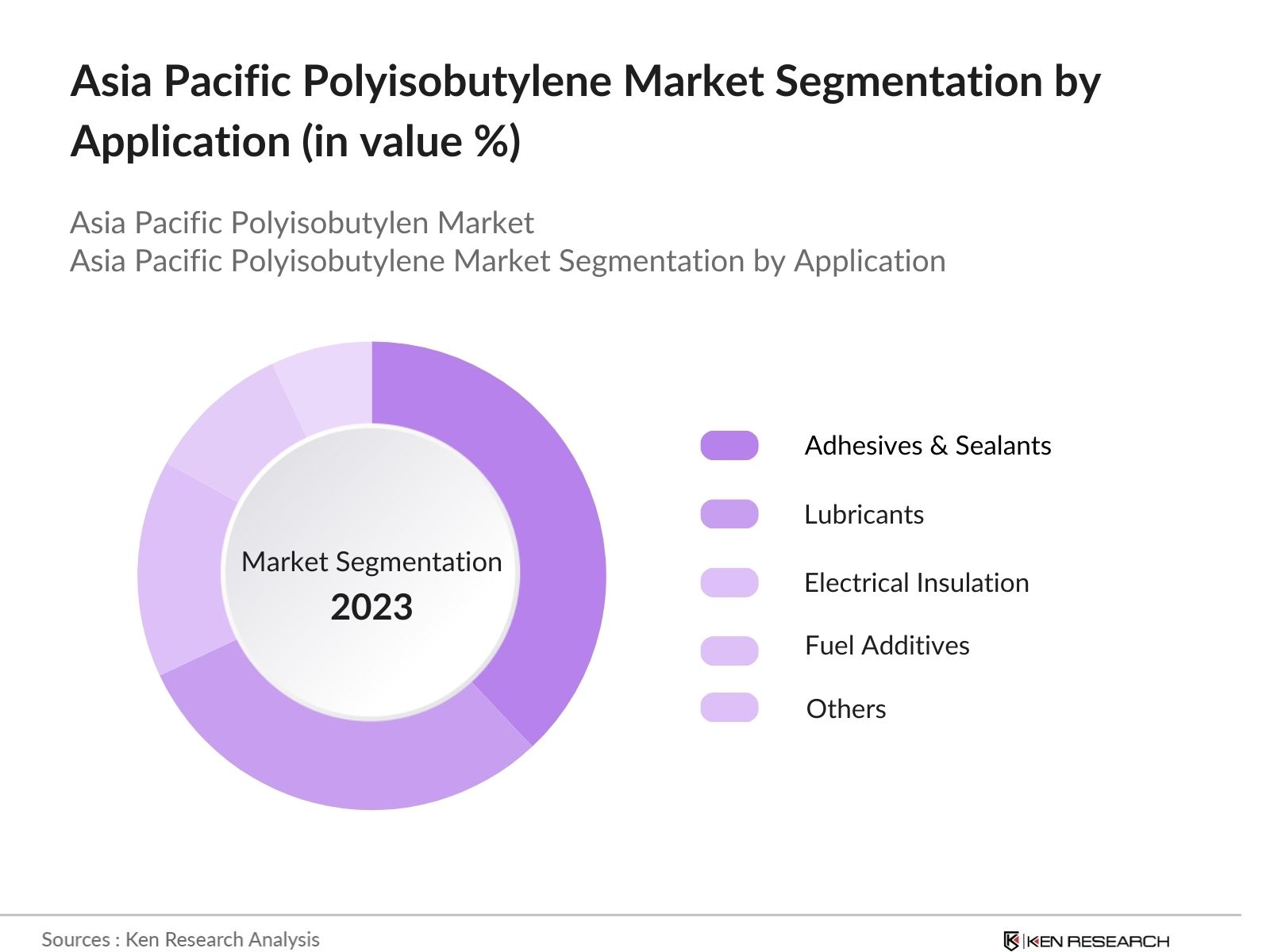

- By Application: The market is segmented into adhesives & sealants, lubricants, electrical insulation, fuel additives, and others. Adhesives & sealants represented the largest share in 2023, driven by increasing demand in the automotive and construction sectors. Lubricants are expected to witness significant growth due to the rising demand in industrial and automotive applications.

- By Region: The APAC market is segmented by country into China, India, Japan, Australia, and South Korea. In 2023, China held the largest market share, driven by the growth in automotive production and infrastructure projects. Indias market is expected to witness rapid growth due to increasing construction activities and demand for fuel-efficient vehicles.

Asia Pacific Polyisobutylene Market Competitive Landscape

|

Company Name |

Establishment Year |

Headquarters |

|

BASF SE |

1865 |

Ludwigshafen, Germany |

|

ExxonMobil Corporation |

1999 |

Irving, USA |

|

TPC Group |

1943 |

Houston, USA |

|

Lubrizol Corporation |

1928 |

Wickliffe, USA |

|

INEOS Group |

1998 |

London, UK |

- BASF SE: In 2023, BASF SE, in partnership with Sinopec, expanded its production capacity at the Nanjing Verbund site in China. This expansion is designed to meet the increasing demand for high-quality chemical intermediates, which includes products used in the adhesives and sealants market. The new facilities are expected to utilize renewable energy, aligning with BASF's focus on sustainability and energy efficiency in the region.

- TPC Group: In September 2023, TPC Group successfully concluded the first phase of its di-isobutylene capacity upgrade at its Houston, Texas plant. This positions the company to meet the surging global demand for di-isobutylene, which is fueled by the widespread adoption of low global warming potential refrigerants.

Asia Pacific Polyisobutylene Market Analysis

Growth Drivers:

- Rising Demand in the Automotive Industry: The Asia Pacific region, led by China and India, has seen a sharp rise in automotive production in recent years. In 2023, China manufactured over 27 million vehicles, according to the Chinese Ministry of Industry and Information Technology (MIIT). The automotive industry is a key consumer of polyisobutylene, especially in manufacturing lubricants, fuel additives, and sealants. As the automotive sector continues to grow, polyisobutylene demand is projected to increase further, particularly with the growth in electric vehicle (EV) production, where polyisobutylene is used in battery cooling systems.

- Rise in Infrastructure Development Projects: Several governments in the Asia Pacific region have allocated significant budgets for infrastructure development. The Government of India allocated approximately USD 134 billion for infrastructure projects in its 2024 budget. Polyisobutylene is widely used in construction sealants and adhesives due to its water-resistant and long-lasting properties. As these construction activities escalate, the demand for polyisobutylene-based materials will see substantial growth, particularly in urbanizing cities like Mumbai, Shanghai, and Seoul.

- Increasing Demand for Sustainable Packaging: The rise in consumer awareness about environmental sustainability is driving the demand for eco-friendly materials in packaging. Japan, one of the largest economies in the region, announced a 2024 ban on single-use plastics as part of its sustainable development goals. Polyisobutylene is increasingly being used in biodegradable packaging materials, which align with these sustainability mandates.

Challenges:

- Volatility in Raw Material Prices: The Asia Pacific polyisobutylene market faces logistical bottlenecks, exacerbated by ongoing geopolitical tensions and the lingering effects of the COVID-19 pandemic. According to the World Banks 2024 Logistics Performance Index, countries like Indonesia and the Philippines experienced notable disruptions in their supply chains due to poor infrastructure and frequent natural disasters.

- Stringent Environmental Regulations: Countries in the Asia Pacific region are increasingly tightening environmental regulations. For instance, Chinas National Development and Reform Commission (NDRC) introduced new mandates in 2024 to reduce carbon emissions in the chemical sector, which directly impacts the production of polyisobutylene.

Government Initiatives:

- Chinas Circular Economy Action Plan: China's Circular Economy Action Plan, part of the 14th Five-Year Plan (2021-2025), aims to enhance resource efficiency and sustainability. The plan includes a budget of approximately USD 773 billion to improve recycling systems, promote green design, and reduce waste. By 2025, it targets a 20% increase in resource productivity and significant reductions in energy and water consumption per GDP unit.

- Japans 2024 Plastic Reduction Mandate: In line with its sustainability goals, Japan enforced a 2024 mandate aimed at reducing plastic waste by replacing conventional plastics with biodegradable alternatives. This initiative supports the increased usage of polyisobutylene in biodegradable packaging materials. The mandate is part of Japans broader effort to curb pollution and promote sustainable packaging.

Asia Pacific Polyisobutylene Market Future Outlook

The Asia-Pacific Polyisobutylene Market is projected to experience growth during the forecast period, driven by increasing demand in the automotive and construction sectors. Technological advancements in production and the rising focus on sustainability will further fuel market growth.

Future Market Trends:

- Rising Demand for High-Performance Lubricants: Over the next five years, the Asia Pacific polyisobutylene market will be driven by the increasing demand for high-performance lubricants, particularly in the automotive and industrial sectors. As India and China ramp up production of electric and hybrid vehicles, polyisobutylene will play a crucial role in manufacturing high-performance lubricants with improved viscosity and thermal stability.

- Expansion of Eco-Friendly Packaging Solutions: As countries like Japan and Australia strengthen their regulations around single-use plastics and non-biodegradable materials, polyisobutylene will find growing application in sustainable packaging solutions. By 2028, biodegradable and recyclable packaging materials will account for a large portion of the market share in the APAC region.

Scope of the Report

|

By Grade |

Low Molecular Weight Medium Molecular Weight High Molecular Weight |

|

By Application |

Adhesives & Sealants Lubricants Electrical Insulation Fuel Additives Others |

|

By Packaging Type |

Flexible Packaging Rigid Packaging Glass Packaging Biodegradable Packaging |

|

By End-User |

Automotive Construction Packaging Others |

|

By Region |

China India Japan South Korea Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Automotive Manufacturers

Construction Companies

Packaging Manufacturers

Lubricant Producers

Adhesive and Sealant Manufacturers

Electrical Insulation Providers

Fuel Additive Manufacturers

Government and Regulatory Bodies (MIIT and NDRC)

Investments and Venture Capitalist Firms

Banks and Financial Institute

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

BASF SE

ExxonMobil Corporation

TPC Group

Lubrizol Corporation

INEOS Group

Kothari Petrochemicals

Chevron Phillips Chemical Company

LANXESS AG

Daelim Industrial

Shandong Hongrui New Material Technology Co., Ltd.

Zhejiang Shunda New Material Co., Ltd.

Reliance Industries Limited

SIBUR Holding

Braskem S.A.

TotalEnergies SE

Table of Contents

1. Asia Pacific Polyisobutylene Market Overview

1.1. Definition and Scope

1.2. Market Structure and Taxonomy

1.3. Market Growth Rate Analysis (Financial and Operational Metrics)

1.4. Key Market Developments and Milestones

2. Asia Pacific Polyisobutylene Market Size (USD Million)

2.1. Historical Market Size (Value and Volume)

2.2. Year-on-Year Growth Analysis (Operational Parameters)

2.3. Contribution of Key Regions (North APAC, South APAC, East APAC, West APAC)

2.4. Industry Revenue Analysis (Top-to-Bottom Approach)

2.5. Breakdown of Market Value by Polyisobutylene Type (Low, Medium, High Molecular Weight)

3. Asia Pacific Polyisobutylene Market Dynamics

3.1. Growth Drivers

3.1.1. Rising Demand for Automotive Lubricants

3.1.2. Expanding Infrastructure and Construction Activities

3.1.3. Government Policies Promoting Industrial Production

3.2. Market Challenges

3.2.1. Fluctuations in Raw Material Prices

3.2.2. Strict Environmental Regulations in Major Countries

3.2.3. Supply Chain Constraints in Remote Markets

3.3. Market Opportunities

3.3.1. Adoption of Bio-Based Polyisobutylene

3.3.2. Increasing Usage in Electric Vehicles (EVs)

3.3.3. Growth of Cold Chain Logistics in Food and Pharma

4. Asia Pacific Polyisobutylene Market Segmentation

(In Value %)

5. Asia Pacific Polyisobutylene Market Competitive Landscape

5.1. Competitive Market Share Analysis (Market Share %, Financial and Operational Metrics)

5.2. Strategic Initiatives and Partnerships (Investments, JVs, and Alliances)

5.3. Key Market Players Analysis

5.3.1. BASF SE

5.3.2. ExxonMobil

5.3.3. TPC Group

5.3.4. Lubrizol Corporation

5.3.5. INEOS Group

5.4. Cross-Comparison (Company Profiles Establishment Year, Headquarters, Revenue, No. of Employees)

5.4.1. Daelim Industrial

5.4.2. Kothari Petrochemicals

5.4.3. Reliance Industries Limited

5.4.4. Chevron Phillips Chemical Company

5.4.5. LANXESS AG

6. Asia Pacific Polyisobutylene Market Financial Analysis

6.1. Financial Performance of Key Players

6.1.1. Revenue Analysis by Key Companies

6.1.2. Operational Efficiency Metrics (Cost Efficiency, Production Output)

6.2. Investment and Venture Capital Analysis

6.2.1. Recent Investments and Fundings (Venture Capital, Government Grants)

6.2.2. Mergers and Acquisitions

6.3. Profitability and Revenue Forecasts

7. Asia Pacific Polyisobutylene Market Regulatory Framework

7.1. Government Policies Supporting Industrial Growth

7.2. Compliance and Certification Requirements for Polyisobutylene Production

7.3. Environmental Regulations and Sustainability Standards

7.4. Safety and Labor Regulations in Chemical Industries

8. Future Outlook for Asia Pacific Polyisobutylene Market

8.1. Market Growth Projections

8.2. Key Trends Shaping Future Demand (Sustainable Materials, Advanced Technologies)

8.3. Expansion of Applications in Automotive and Packaging

8.4. Adoption of AI and Automation in Polyisobutylene Manufacturing

9. Asia Pacific Polyisobutylene Market Future Segmentation, 2028

9.1. By Molecular Weight (In Value %)

9.2. By Application (In Value %)

9.3. By End-User Industry (In Value %)

9.4. By Packaging Type (In Value %)

9.5. By Region (In Value %)

10. Analyst Recommendations

10.1. TAM/SAM/SOM Analysis for Asia Pacific Polyisobutylene Market

10.2. Key Strategic Recommendations for Polyisobutylene Manufacturers

10.3. Emerging Markets and White-Space Opportunities (Bio-Based Polyisobutylene, EVs)

10.4. Environmental and Sustainable Manufacturing Strategies

11. Disclaimer

12. Contact Us

Research Methodology

Step 1 Identifying Key Variables

: Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry-level information.

Step 2 Market Building

: Collating statistics on the Asia Pacific polyisobutylene market over the years, penetration of marketplaces, and service providers ratio to compute revenue generated for the Asia Pacific polyisobutylene market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step 3 Validating and Finalizing

: Building market hypotheses and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step 4 Research Output

: Our team will approach multiple essential polyisobutylene companies and understand the nature of product segments and sales, consumer preference, and other parameters, which will support us to validate statistics derived through a bottom-to-top approach from polyisobutylene companies.

Frequently Asked Questions

How big is the Asia Pacific polyisobutylene market?

The Asia Pacific polyisobutylene market was valued at USD 878 billion in 2023, driven by the rising demand in the automotive, construction, and packaging sectors. Increasing applications in lubricants and sealants further contribute to its growth.

What are the challenges in the Asia Pacific polyisobutylene market?

Challenges include raw material price volatility due to fluctuating crude oil prices, strict environmental regulations across key markets like China and India, and supply chain disruptions, which impact the timely delivery of raw materials and finished products.

Who are the major players in the Asia Pacific polyisobutylene market?

Key players in the Asia Pacific polyisobutylene market include BASF SE, ExxonMobil, TPC Group, Lubrizol Corporation, and INEOS Group. These companies dominate the market through their strong production capacities, innovation in product applications, and extensive distribution networks.

What are the growth drivers of the Asia Pacific polyisobutylene market?

Growth drivers include the increasing automotive production in China and India, rising infrastructure development projects across the region, and the growing demand for sustainable packaging solutions, which are aligned with government initiatives promoting eco-friendly practices.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.