Asia Pacific Polyurea Coating Market Outlook to 2030

Region:Asia

Author(s):Shreya Garg

Product Code:KROD6415

December 2024

81

About the Report

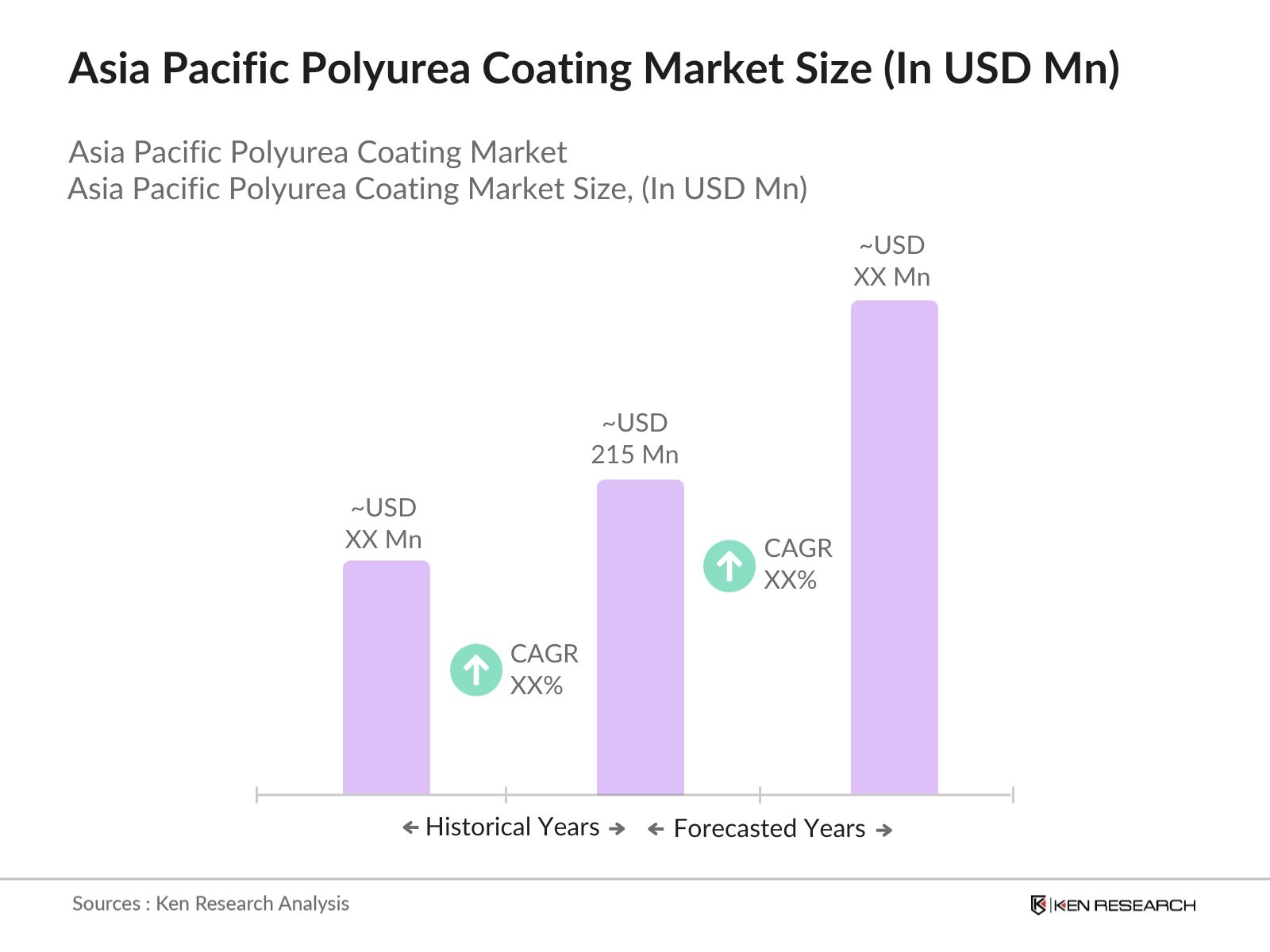

Asia Pacific Polyurea Coating Market Overview

- The Asia Pacific polyurea coating market, valued at USD 215 million, is driven by rapid industrialization and urbanization across the region. The construction sector's expansion, particularly in countries like China and India, has significantly increased the demand for durable and efficient coating solutions. Polyurea coatings are favored for their exceptional properties, including fast curing times and superior resistance to chemicals and abrasion, making them ideal for various applications in construction and industrial settings.

- China stands as the dominant player in the Asia Pacific polyurea coating market, primarily due to its massive infrastructure projects and robust industrial activities. The country's commitment to urban development and modernization has led to a substantial increase in the use of polyurea coatings for waterproofing, corrosion protection, and structural enhancement. Additionally, China's focus on environmental sustainability has prompted the adoption of eco-friendly coating solutions, further boosting the market.

- Public-Private Partnerships (PPPs) have become a cornerstone of India's infrastructure development strategy. The government has initiated numerous PPP projects to enhance infrastructure, including roads, bridges, and urban development. These collaborations often stipulate the use of high-quality, durable materials, such as advanced coatings, to ensure the longevity and sustainability of infrastructure projects. The emphasis on quality standards in PPP agreements creates a significant market opportunity for manufacturers of advanced coating solutions.

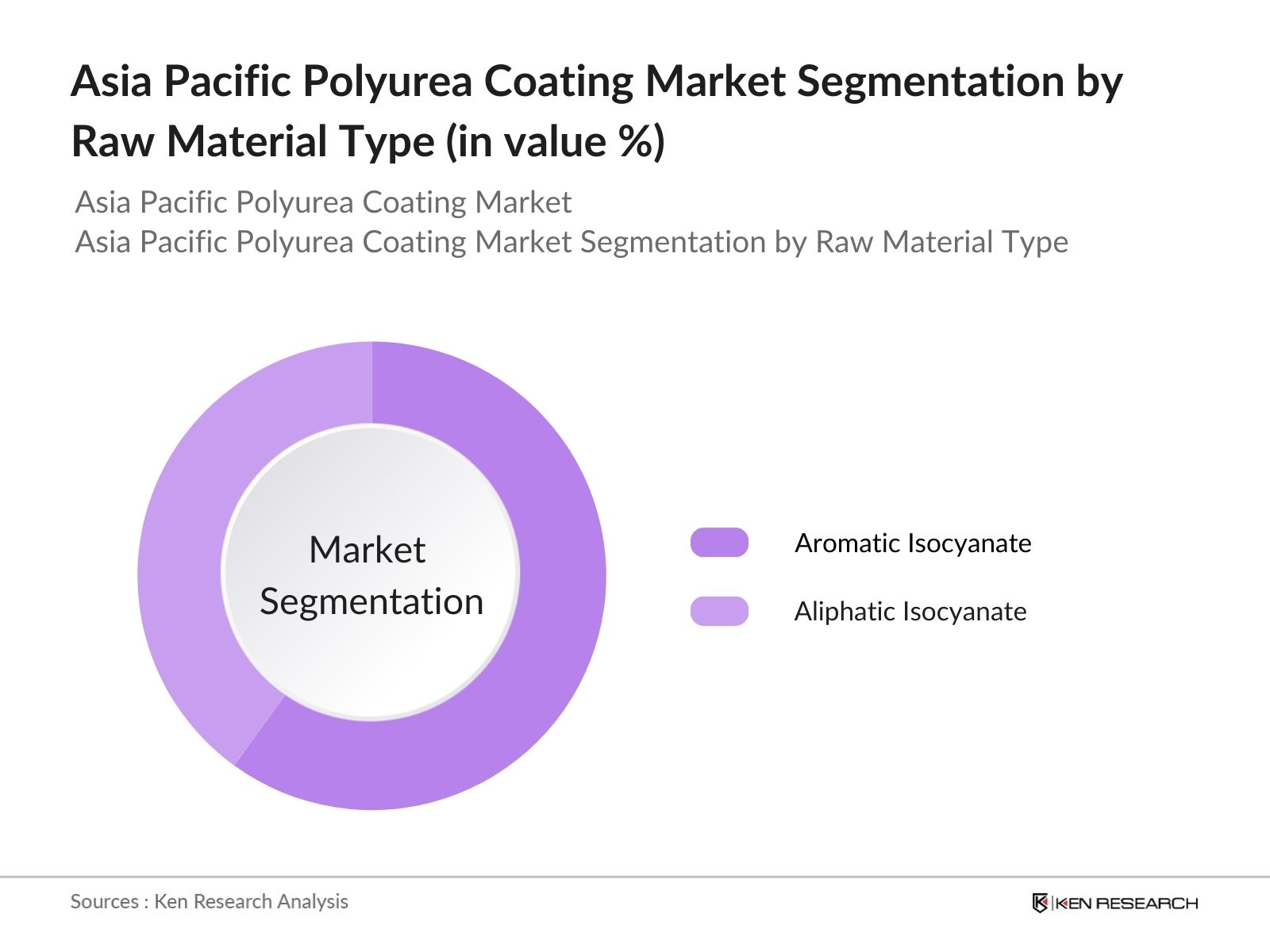

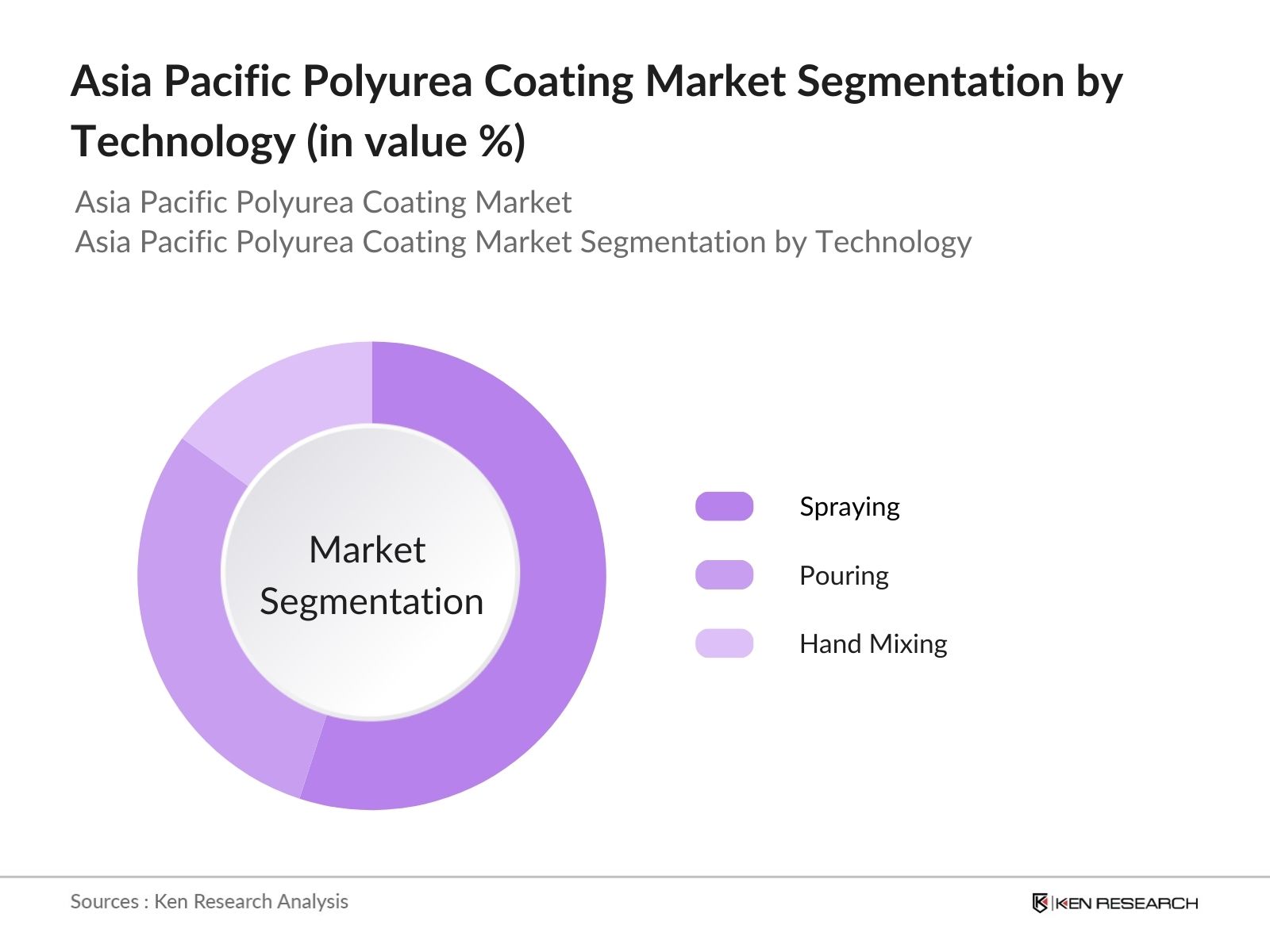

Asia Pacific Polyurea Coating Market Segmentation

By Raw Material Type: The market is segmented by raw material type into aromatic isocyanate and aliphatic isocyanate. Aromatic isocyanate-based polyurea coatings hold a dominant market share due to their cost-effectiveness and suitability for applications where UV stability is not a critical requirement. These coatings are extensively used in industrial flooring, secondary containment systems, and tank linings, where their excellent mechanical properties and chemical resistance are highly valued.

By Technology: The market is also segmented by technology into spraying, pouring, and hand mixing. The spraying technology segment dominates the market, attributed to its efficiency and ability to provide uniform and seamless coatings over large surfaces. This method is particularly advantageous in applications requiring quick turnaround times and minimal downtime, such as in construction and industrial maintenance projects.

Asia Pacific Polyurea Coating Market Competitive Landscape

The Asia Pacific polyurea coating market is characterized by the presence of several key players who contribute to its growth and development.

Asia Pacific Polyurea Coating Industry Analysis

Growth Drivers

- Rapid Urbanization and Infrastructure Development: India's urban population is projected to reach 600 million by 2031, necessitating substantial infrastructure development to accommodate this growth. The government has allocated 10 lakh crore for infrastructure projects in the 2024-25 budget, focusing on transportation, housing, and urban amenities. This surge in urbanization and infrastructure spending is expected to drive demand for advanced coating solutions, including polyurea coatings, to protect and enhance the durability of new structures.

- Advancements in Coating Technologies: The coatings industry is witnessing significant technological advancements, such as the development of smart coatings that respond to environmental stimuli and bio-based coatings derived from renewable resources. These innovations are enhancing the performance, sustainability, and application efficiency of coatings, making them more attractive for various industries, including construction and automotive sectors.

- Increasing Demand in Automotive and Transportation Sectors: India's automotive industry is experiencing robust growth, with over 326 million registered vehicles as of 2020. The sector contributes significantly to the nation's GDP and is a major consumer of coatings for vehicle protection and aesthetics. The expansion of transportation infrastructure, including roads and railways, further amplifies the demand for durable and high-performance coatings.

Market Challenges

- High Application Costs: The application of advanced coatings like polyurea requires specialized equipment and skilled labor, leading to higher costs compared to traditional coatings. This cost factor can be a barrier for small and medium-sized enterprises, limiting the widespread adoption of such technologies.

- Technical Application Challenges: Applying polyurea coatings requires precise environmental conditions and skilled applicators to ensure optimal performance. Factors such as humidity, temperature, and substrate preparation play crucial roles in the application process. These technical challenges can lead to application errors, affecting the coating's effectiveness and longevity.

Asia Pacific Polyurea Coating Market Future Outlook

Over the next five years, the Asia Pacific polyurea coating market is expected to experience significant growth, driven by continuous infrastructure development, advancements in coating technologies, and increasing demand for eco-friendly and durable coating solutions. The region's focus on sustainable development and stringent environmental regulations will further propel the adoption of polyurea coatings in various applications, including construction, transportation, and industrial sectors.

Future Market Opportunities

- Emerging Applications in Marine and Defense Sectors: India is enhancing its naval capabilities, with plans to build two nuclear-powered attack submarines at an estimated cost of $5.4 billion. The marine and defense sectors require coatings that offer superior corrosion resistance and durability. Polyurea coatings, known for their robustness, present significant opportunities in these sectors to protect assets from harsh marine environments and extend their service life.

- Growth in Emerging Economies: Emerging economies are investing heavily in infrastructure development to support urbanization and economic growth. For instance, India's infrastructure spending has increased twelvefold over the past decade, with significant investments in roads, railways, and urban development. This trend creates a substantial market for advanced coatings to protect and enhance the lifespan of new infrastructure projects.

Scope of the Report

|

Raw Material Type |

Aromatic Isocyanate |

|

Polyurea Type |

Pure Polyurea |

|

Technology |

Spraying |

|

End-Use Industry |

Building & Construction |

|

Country |

China |

Products

Key Target Audience

Polyurea Coating Manufacturers

Raw Material Suppliers

Construction Companies

Automotive Manufacturers

Industrial Equipment Manufacturers

Government and Regulatory Bodies (e.g., Ministry of Industry and Information Technology)

Investors and Venture Capitalist Firms

Research and Development Institutes

Companies

Major Players

BASF SE

Huntsman Corporation

PPG Industries, Inc.

The Sherwin-Williams Company

Sika AG

Covestro AG

Rhino Linings Corporation

Nukote Coating Systems International LLC

Teknos Group Oy

VIP Coatings International GmbH & Co. KG

Fosroc Inc.

Isomat S.A.

Krypton Chemical

Armorthane Inc.

Chemline Inc.

Table of Contents

Asia Pacific Polyurea Coating Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

Asia Pacific Polyurea Coating Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

Asia Pacific Polyurea Coating Market Analysis

3.1. Growth Drivers

3.1.1. Rapid Urbanization and Infrastructure Development

3.1.2. Advancements in Coating Technologies

3.1.3. Increasing Demand in Automotive and Transportation Sectors

3.1.4. Stringent Environmental Regulations Promoting Eco-friendly Coatings

3.2. Market Challenges

3.2.1. High Application Costs

3.2.2. Availability of Substitutes

3.2.3. Technical Application Challenges

3.3. Opportunities

3.3.1. Emerging Applications in Marine and Defense Sectors

3.3.2. Growth in Emerging Economies

3.3.3. Development of Bio-based Polyurea Coatings

3.4. Trends

3.4.1. Adoption of Spray Polyurea Coating Technology

3.4.2. Integration with Smart Coating Systems

3.4.3. Increased Use in Waterproofing Applications

3.5. Government Regulations

3.5.1. National Standards for Coating Applications

3.5.2. Environmental Compliance Requirements

3.5.3. Incentives for Sustainable Coating Solutions

3.5.4. Public-Private Partnerships in Infrastructure Projects

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

Asia Pacific Polyurea Coating Market Segmentation

4.1. By Raw Material Type (In Value %)

4.1.1. Aromatic Isocyanate

4.1.2. Aliphatic Isocyanate

4.2. By Polyurea Type (In Value %)

4.2.1. Pure Polyurea

4.2.2. Hybrid Polyurea

4.3. By Technology (In Value %)

4.3.1. Spraying

4.3.2. Pouring

4.3.3. Hand Mixing

4.4. By End-Use Industry (In Value %)

4.4.1. Building & Construction

4.4.2. Transportation

4.4.3. Industrial

4.4.4. Landscape

4.4.5. Others

4.5. By Country (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. South Korea

4.5.5. Australia

4.5.6. Rest of Asia Pacific

Asia Pacific Polyurea Coating Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. BASF SE

5.1.2. Huntsman Corporation

5.1.3. PPG Industries, Inc.

5.1.4. The Sherwin-Williams Company

5.1.5. Sika AG

5.1.6. Covestro AG

5.1.7. Rhino Linings Corporation

5.1.8. Nukote Coating Systems International LLC

5.1.9. Teknos Group Oy

5.1.10. VIP Coatings International GmbH & Co. KG

5.1.11. Fosroc Inc.

5.1.12. Isomat S.A.

5.1.13. Krypton Chemical

5.1.14. Armorthane Inc.

5.1.15. Chemline Inc.

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Presence, R&D Investment, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

Asia Pacific Polyurea Coating Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

Asia Pacific Polyurea Coating Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

Asia Pacific Polyurea Coating Future Market Segmentation

8.1. By Raw Material Type (In Value %)

8.2. By Polyurea Type (In Value %)

8.3. By Technology (In Value %)

8.4. By End-Use Industry (In Value %)

8.5. By Country (In Value %)

Asia Pacific Polyurea Coating Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Asia Pacific polyurea coating market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the Asia Pacific polyurea coating market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple polyurea coating manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Asia Pacific polyurea coating market.

Frequently Asked Questions

How big is the Asia Pacific polyurea coating market?

The Asia Pacific polyurea coating market is valued at USD 215 million, driven by rapid industrialization and urbanization across the region.

What are the challenges in the Asia Pacific polyurea coating market?

The Asia Pacific polyurea coating market faces challenges such as high application costs, which can limit adoption among smaller companies, and technical difficulties in application processes that require skilled labor. Additionally, the availability of alternative coating materials also poses competitive challenges.

Who are the major players in the Asia Pacific polyurea coating market?

Major players in the Asia Pacific polyurea coating market include BASF SE, Huntsman Corporation, PPG Industries, Inc., The Sherwin-Williams Company, and Sika AG. These companies dominate due to their extensive portfolios, strong R&D investments, and strategic presence across multiple industries.

What are the growth drivers of the Asia Pacific polyurea coating market?

Growth drivers in the Asia Pacific polyurea coating market include the expanding construction and infrastructure sector, demand for durable coating solutions in industrial applications, and the push for sustainable, eco-friendly products due to environmental regulations.

Which country dominates the Asia Pacific polyurea coating market, and why?

China dominates the Asia Pacific polyurea coating market because of its large-scale infrastructure projects, rapid urbanization, and substantial investment in sustainable development initiatives, which drive demand for advanced coating solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.