Asia Pacific Power Electronics Market Outlook to 2030

Region:Asia

Author(s):Meenakshi

Product Code:KROD6420

November 2024

85

About the Report

Asia Pacific Power Electronics Market Overview

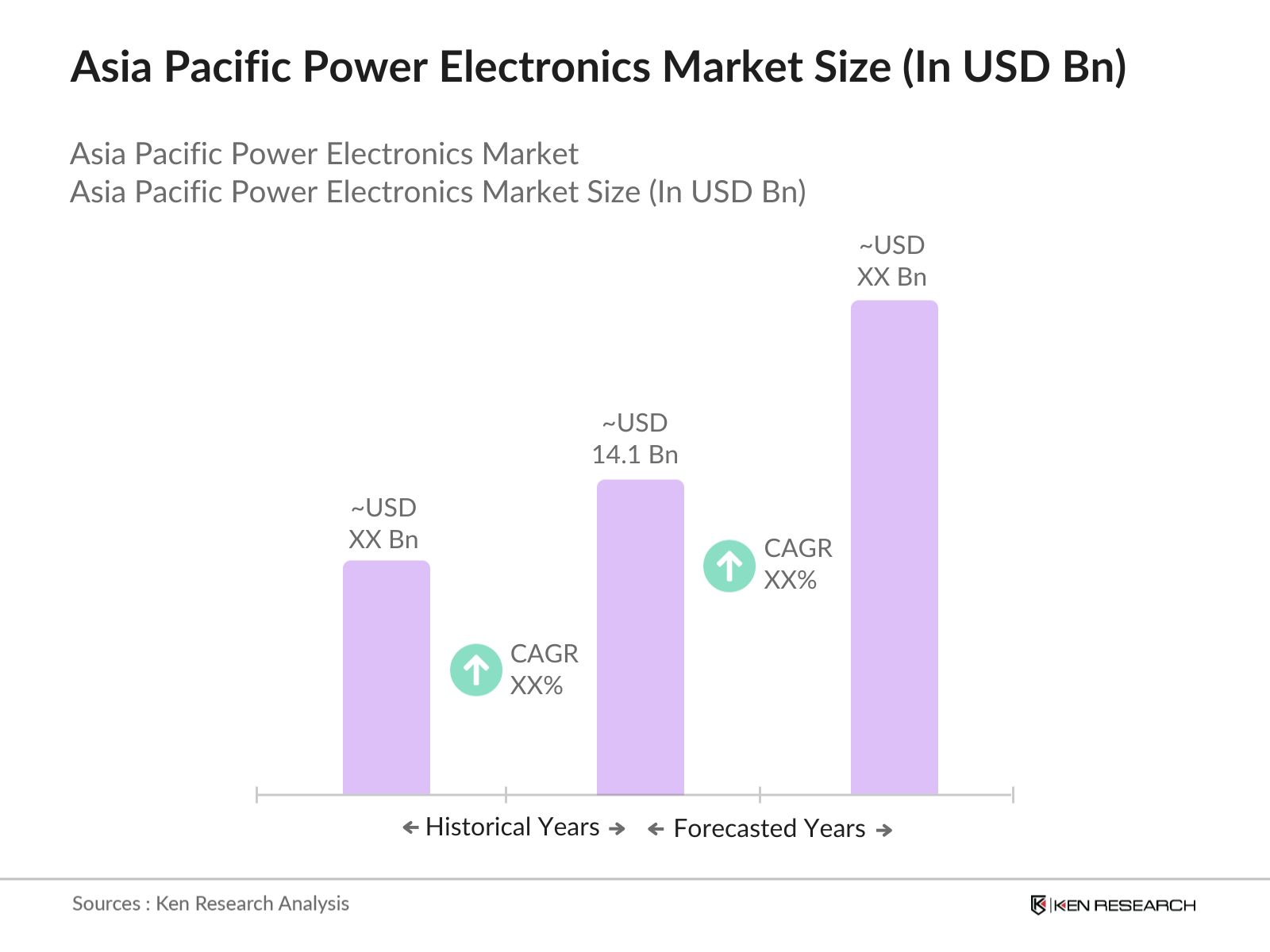

- The Asia Pacific power electronics market is valued at USD 14.1 billion, driven by the increasing demand for energy-efficient solutions across various industries. The rapid adoption of renewable energy, electric vehicles (EVs), and industrial automation in the region is a major contributor to market expansion. Key applications, such as solar inverters, EV powertrains, and industrial motor drives, are pushing this demand, making power electronics a critical component of modern energy solutions.

- China and Japan are the dominant players in the Asia Pacific power electronics market due to their advanced manufacturing capabilities and leadership in semiconductor technologies. Chinas large-scale investments in renewable energy projects and electric vehicle infrastructure, along with its strong supply chain, make it a leader in the region. Japan, known for its technological innovation, maintains a competitive edge through its expertise in high-efficiency power modules and wide-bandgap semiconductors.

- Governments in Asia Pacific are setting ambitious renewable energy targets, pushing the adoption of power electronics to support renewable energy generation and distribution. In 2023, China's renewable energy installed capacity surpassed 1.45 billion kilowatts, making up over 50% of the country's total power generation capacity, according to the National Energy Administration. These standards mandate a certain percentage of electricity to come from renewable sources, thus driving the demand for power electronics to manage renewable energy systems.

Asia Pacific Power Electronics Market Segmentation

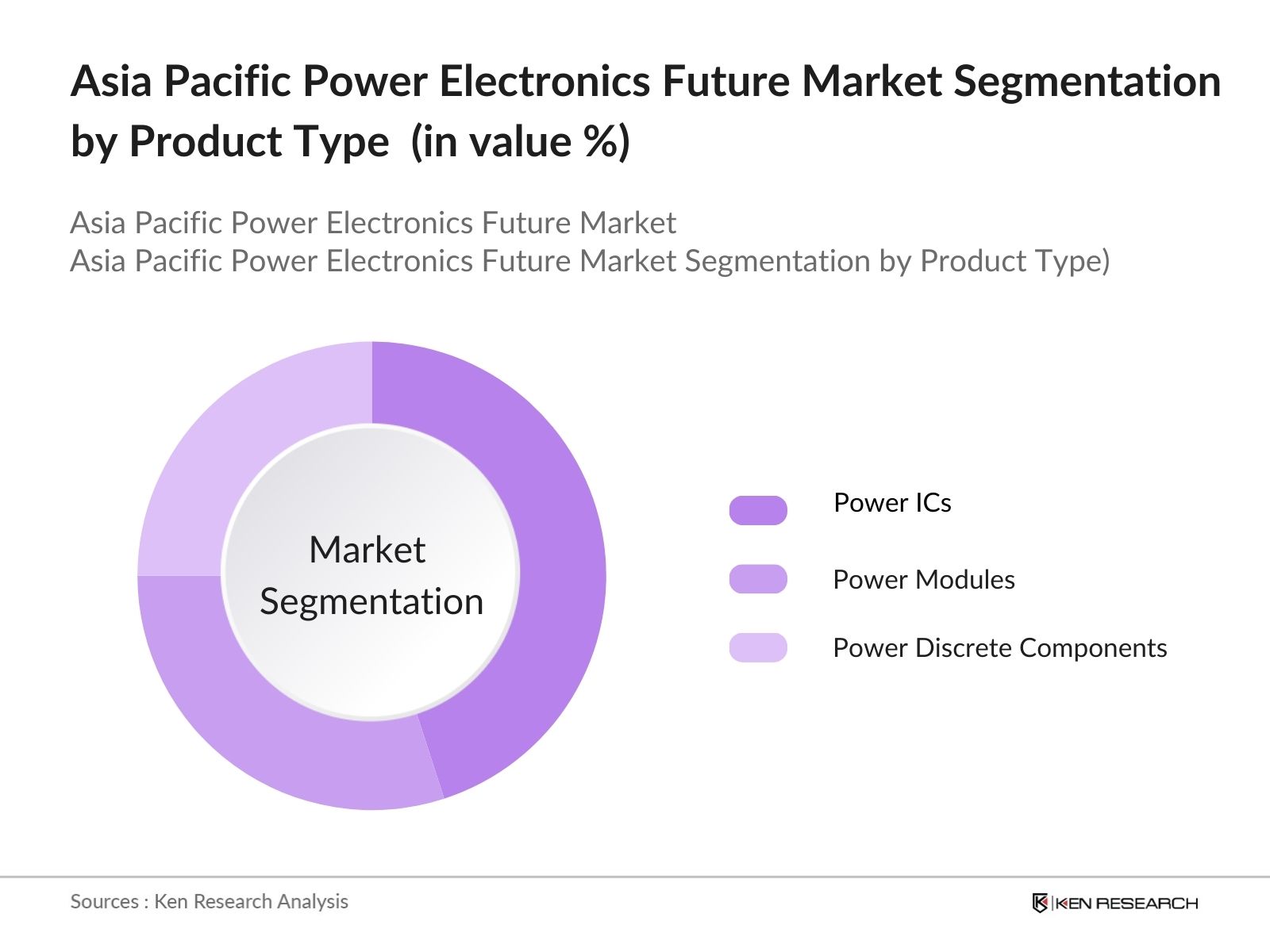

By Product Type: The market is segmented by product type into power integrated circuits (ICs), power modules, and power discrete components. Power ICs have a dominant market share due to their versatility in various applications, particularly in consumer electronics and automotive sectors. With growing demands for miniaturization and energy efficiency, power ICs are increasingly being integrated into devices, reducing component size and power consumption, which is critical for portable electronics and electric vehicles.

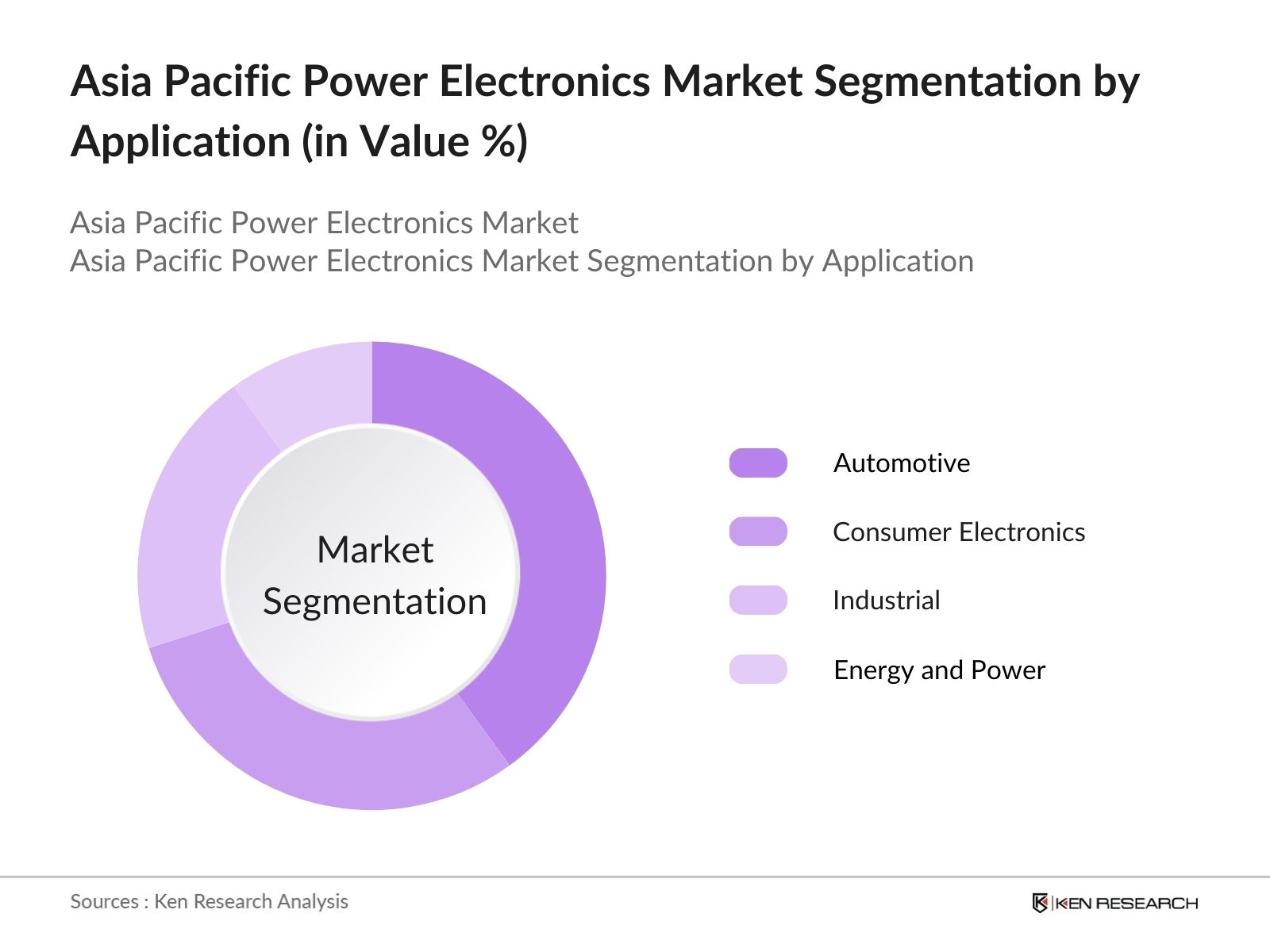

By Application: The market is segmented by application into consumer electronics, automotive, industrial, and energy and power sectors. The automotive segment holds a significant share, driven by the rapid adoption of electric vehicles (EVs) across the region. As governments push for cleaner transportation, the demand for advanced power electronics in EV powertrains, charging infrastructure, and battery management systems is accelerating. The rise of hybrid and fully electric vehicles requires efficient energy conversion and management, where power electronics plays a crucial role.

Asia Pacific Power Electronics Market Competitive Landscape

The Asia Pacific power electronics market is dominated by major players that leverage technological advancements and extensive production capabilities to maintain their positions. These companies excel in semiconductor innovation, energy-efficient solutions, and applications in automotive and renewable energy industries. These firms dominate in sectors such as automotive and renewable energy, leveraging innovation in SiC and GaN semiconductors for enhanced energy efficiency.

Asia Pacific Power Electronics Industry Analysis

Growth Drivers

- Rising Demand for Energy Efficiency Solutions (Energy Efficiency): The demand for energy-efficient solutions across the Asia Pacific region is increasing due to rising energy consumption and regulatory pressure. For example, the regions electricity consumption hit 13,694 TWh in 2023, with governments enforcing energy efficiency regulations to curb this growth. Japan and South Korea have rolled out stringent energy efficiency standards, leading to increased adoption of power electronics in sectors like industrial manufacturing. Power electronics, especially inverters and rectifiers, play a crucial role in reducing energy wastage by optimizing power conversion.

- Increasing Electrification in the Transportation Sector (EV Adoption Rate): Electrification in transportation is driving demand for power electronics in the Asia Pacific, particularly with the rapid growth in electric vehicle (EV) adoption. China alone sold over 6 million EVs in 2023, a number supported by government subsidies and the increasing availability of charging infrastructure. Power electronics components such as converters and inverters are essential for EVs, contributing to higher energy efficiency and performance. Japan and South Korea are also following this trend, with South Korea aiming for 2.8 million EVs on the road by 2025. This surge in EV numbers is significantly influencing the power electronics market.

- Advancements in Power Semiconductor Technologies (Technological Advancements): New semiconductor technologies like SiC (Silicon Carbide) and GaN (Gallium Nitride) are driving significant advancements in power electronics across the Asia Pacific. These materials enable greater efficiency, faster switching, and lower energy losses, especially in renewable energy and electric vehicles. Supported by government investments, these innovations are accelerating the adoption of advanced power electronics, enhancing energy efficiency across various applications

Market Challenges

- High Cost of Initial Investment (Capital Expenditure): While energy-efficient power electronics offer significant long-term benefits, the high initial investment required for their deployment is a considerable barrier for many sectors in Asia Pacific. Advanced technologies, such as those used in renewable energy projects, often come with higher upfront costs compared to traditional systems. This poses a challenge, particularly for smaller businesses and developing countries, where limited financial resources make it difficult to invest in cutting-edge power electronics solutions.

- Power Management Issues in Renewable Integration (Grid Stability): Integrating renewable energy sources into existing power grids creates significant management challenges in the Asia Pacific region. Renewable energy generation, especially from solar and wind, can fluctuate unpredictably, causing grid instability. Power electronics play a crucial role in managing these variations, ensuring stable and efficient energy distribution. However, substantial investment in both grid infrastructure and advanced power management systems is required to achieve seamless integration, posing a challenge for many countries in the region.

Asia Pacific Power Electronics Market Future Outlook

The Asia Pacific power electronics market is expected to experience substantial growth in the coming years, driven by advancements in semiconductor technology and the rapid shift toward renewable energy and electric mobility. Governments in the region are enforcing stricter energy efficiency regulations and investing in modernizing infrastructure, further propelling demand for power electronics solutions.

Market Opportunities

- Expanding Electric Vehicle Infrastructure (EV Charging Networks): The expansion of electric vehicle (EV) infrastructure in the Asia Pacific region presents a substantial opportunity for power electronics manufacturers. As countries continue to develop extensive charging networks, power electronics play a vital role in ensuring efficient voltage regulation and power transfer at these charging stations. This growing infrastructure supports increased demand for key power electronics components, including inverters, converters, and battery management systems, fostering further market growth.

- Smart Grid and Microgrid Deployments (Grid Modernization): The deployment of smart grids and microgrids is gaining traction across Asia Pacific, as countries focus on modernizing their energy systems for improved efficiency and reliability. Power electronics are integral to these systems, facilitating the integration of renewable energy and distributed resources. Microgrid technologies, particularly in remote areas, are also seeing significant investment, boosting demand for advanced power electronics solutions to enhance energy management and distribution.

Scope of the Report

|

By Product Type |

Power ICs Power Modules Power Discrete Components |

|

By Application |

Consumer Electronics Automotive Industrial Energy and Power |

|

By Material Type |

Silicon (Si) Silicon Carbide (SiC) Gallium Nitride (GaN) |

|

By End-User |

Renewable Energy Data Centers Telecom Aerospace and Defense |

|

By Region |

China India Japan South Korea Australia |

Products

Key Target Audience

Automotive Manufacturers

Renewable Energy Companies

Industrial Automation

Telecom Equipment Manufacturers

Government and Regulatory Bodies (Ministries of Energy, National Energy Agencies)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Infineon Technologies AG

Mitsubishi Electric Corporation

ON Semiconductor Corporation

Toshiba Corporation

Texas Instruments Inc.

STMicroelectronics

Renesas Electronics Corporation

Fuji Electric Co., Ltd.

Rohm Co., Ltd.

NXP Semiconductors

Table of Contents

1. Asia Pacific Power Electronics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Power Electronics Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Power Electronics Market Analysis

3.1. Growth Drivers

3.1.1. Rising Demand for Energy Efficiency Solutions (Energy Efficiency)

3.1.2. Increasing Electrification in the Transportation Sector (EV Adoption Rate)

3.1.3. Government Incentives for Renewable Energy Projects (Government Initiatives)

3.1.4. Advancements in Power Semiconductor Technologies (Technological Advancements)

3.2. Market Challenges

3.2.1. High Cost of Initial Investment (Capital Expenditure)

3.2.2. Power Management Issues in Renewable Integration (Grid Stability)

3.2.3. Dependence on Global Semiconductor Supply Chains (Supply Chain Challenges)

3.3. Opportunities

3.3.1. Expanding Electric Vehicle Infrastructure (EV Charging Networks)

3.3.2. Smart Grid and Microgrid Deployments (Grid Modernization)

3.3.3. Increased Adoption in Industrial Automation (Industry 4.0 Integration)

3.4. Trends

3.4.1. Integration of Wide Bandgap Semiconductors (SiC, GaN Technologies)

3.4.2. Use of AI in Power System Management (AI and Machine Learning)

3.4.3. Growth of Distributed Energy Resources (DER Integration)

3.4.4. Shifts towards Solid-State Transformers (Solid-State Technologies)

3.5. Government Regulation

3.5.1. Renewable Energy Targets and Incentives (Renewable Portfolio Standards)

3.5.2. Energy Efficiency Standards (Efficiency Regulations)

3.5.3. Power Electronics Standards and Certifications (Standards Compliance)

3.5.4. Import Tariffs on Semiconductor Components (Trade Policies)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Stakeholder Analysis, OEMs, End-Users, Investors)

3.8. Porters Five Forces (Threat of New Entrants, Supplier Power, Buyer Power, etc.)

3.9. Competition Ecosystem

4. Asia Pacific Power Electronics Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Power ICs (Integrated Circuits)

4.1.2. Power Modules

4.1.3. Power Discrete Components

4.2. By Application (In Value %)

4.2.1. Consumer Electronics

4.2.2. Automotive

4.2.3. Industrial

4.2.4. Energy and Power

4.3. By Material Type (In Value %)

4.3.1. Silicon (Si)

4.3.2. Silicon Carbide (SiC)

4.3.3. Gallium Nitride (GaN)

4.4. By End-User (In Value %)

4.4.1. Renewable Energy

4.4.2. Data Centers

4.4.3. Telecom

4.4.4. Aerospace and Defense

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. South Korea

4.5.5. Australia

5. Asia Pacific Power Electronics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Infineon Technologies AG

5.1.2. Mitsubishi Electric Corporation

5.1.3. ON Semiconductor Corporation

5.1.4. Toshiba Corporation

5.1.5. Texas Instruments Inc.

5.1.6. Renesas Electronics Corporation

5.1.7. STMicroelectronics

5.1.8. Fuji Electric Co., Ltd.

5.1.9. Rohm Co., Ltd.

5.1.10. NXP Semiconductors

5.1.11. Vishay Intertechnology

5.1.12. ABB Ltd.

5.1.13. Eaton Corporation

5.1.14. Schneider Electric SE

5.1.15. Siemens AG

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Product Portfolio, Revenue, Market Share, Strategic Initiatives, Technological Focus, Manufacturing Capabilities)

5.3. Market Share Analysis (Top Players by Market Share)

5.4. Strategic Initiatives (Partnerships, Product Launches, Mergers)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Power Electronics Market Regulatory Framework

6.1. Energy Efficiency Directives

6.2. Environmental Compliance

6.3. Certification and Testing Processes

7. Asia Pacific Power Electronics Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Power Electronics Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Material Type (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Power Electronics Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the initial phase, the power electronics ecosystem in the Asia Pacific market is mapped, identifying key players, including manufacturers, suppliers, and end-users. Extensive desk research is conducted, drawing from secondary data sources such as industry reports and government databases.

Step 2: Market Analysis and Construction

Historical data is analyzed to evaluate the penetration of power electronics across industries, focusing on revenue generation from applications like automotive and renewable energy. This step also involves assessing technological trends and product innovation.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from power electronics manufacturers and research institutes are consulted via CATIs. These consultations help validate market hypotheses, particularly in growth sectors like electric vehicles and energy storage systems.

Step 4: Research Synthesis and Final Output

Final data synthesis includes insights from manufacturers on product performance and future demand trends. The analysis is cross-verified through a bottom-up approach to ensure data accuracy and reliability for stakeholders.

Frequently Asked Questions

01. How big is the Asia Pacific Power Electronics Market?

The Asia Pacific power electronics market is valued at USD 14.1 billion, with significant demand coming from renewable energy, electric vehicles, and industrial automation.

02. What are the challenges in the Asia Pacific Power Electronics Market?

Challenges in Asia Pacific power electronics market include high capital expenditure requirements for initial setup, dependency on global semiconductor supply chains, and technical complexities in integrating power electronics with renewable energy systems.

03. Who are the major players in the Asia Pacific Power Electronics Market?

Key players in Asia Pacific power electronics market include Infineon Technologies, Mitsubishi Electric, ON Semiconductor, Toshiba Corporation, and Texas Instruments, which dominate due to their technological innovation and extensive product portfolios.

04. What are the growth drivers of the Asia Pacific Power Electronics Market?

The Asia Pacific power electronics market growth is driven by increasing demand for energy-efficient solutions in automotive and industrial sectors, government incentives for renewable energy, and advancements in semiconductor technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.