Asia Pacific Precision Diagnostics Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD6424

December 2024

100

About the Report

Asia Pacific Precision Diagnostics Market Overview

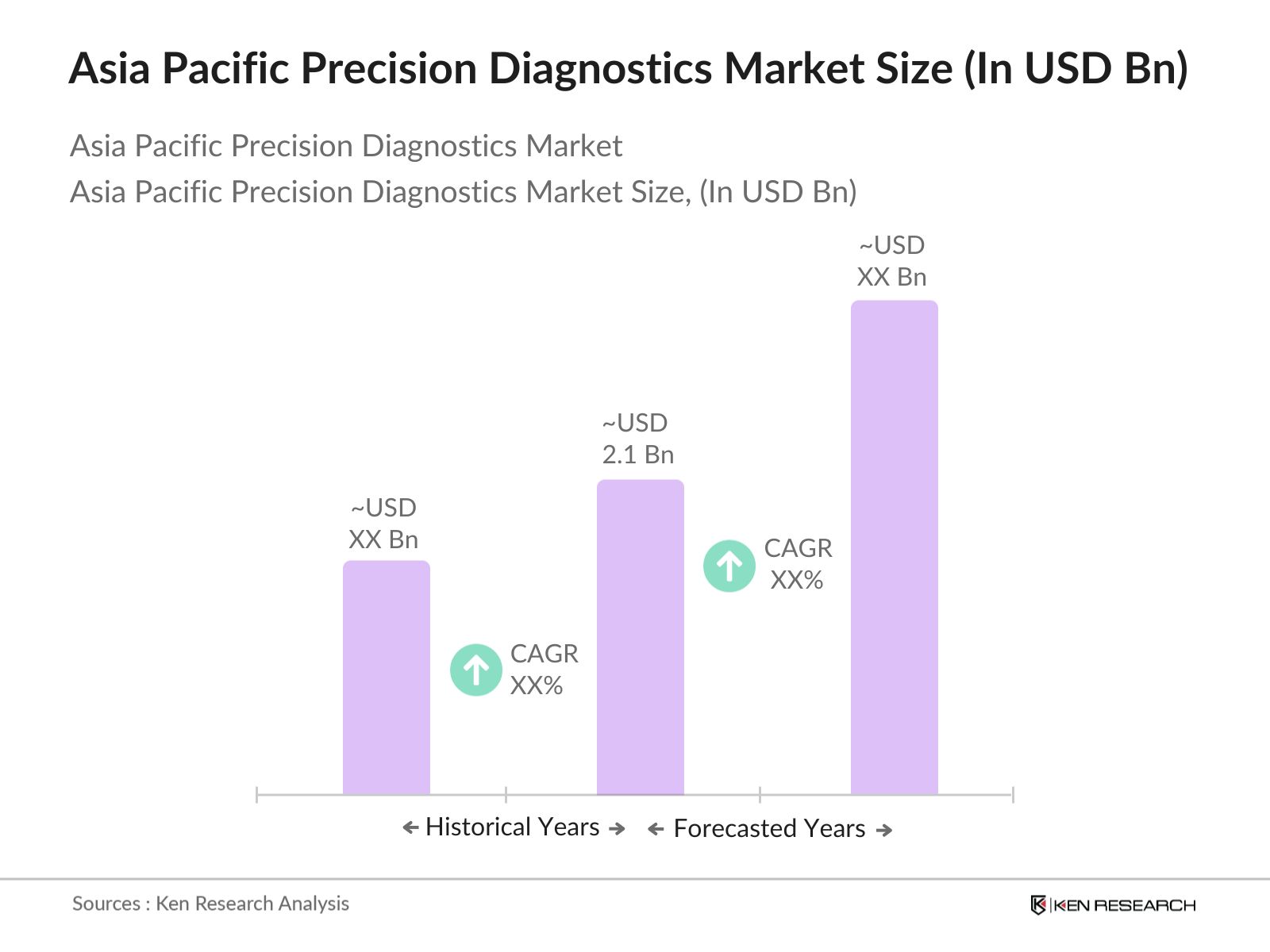

- The Asia Pacific Precision Diagnostics Market is valued at USD 2.1 billion, based on a five-year historical analysis. The rapid growth of this market is primarily driven by the rising adoption of precision medicine, growing awareness about early disease detection, and advancements in genomic and diagnostic technologies such as Next-Generation Sequencing (NGS). These innovations have led to more personalized treatment approaches, particularly for complex diseases like cancer and cardiovascular disorders. The increasing investment in healthcare infrastructure across the region has also contributed to the growth of the precision diagnostics market.

- Countries like China, Japan, and India dominate the Asia Pacific Precision Diagnostics Market due to their robust healthcare systems, strong governmental support for healthcare research, and rising healthcare expenditure. Chinas dominance is attributed to its large-scale biomedical research initiatives and investments in genomics, while Japans leadership stems from its early adoption of advanced diagnostic technologies like AI-driven diagnostics and its focus on personalized medicine. India benefits from a growing population and government initiatives aimed at improving healthcare access, thereby increasing the demand for precision diagnostics solutions.

- Precision diagnostics in the Asia Pacific region are governed by several international and regional regulatory frameworks. In 2024, over 80% of precision diagnostic products in the region were compliant with ISO standards, ensuring quality and consistency in diagnostic procedures (ISO, 2024). Additionally, the U.S. FDA has collaborated with several Asia Pacific countries to align precision diagnostic guidelines with global standards. These guidelines are crucial for ensuring the safety and efficacy of diagnostic products, particularly as the market continues to expand and new technologies emerge.

Asia Pacific Precision Diagnostics Market Segmentation

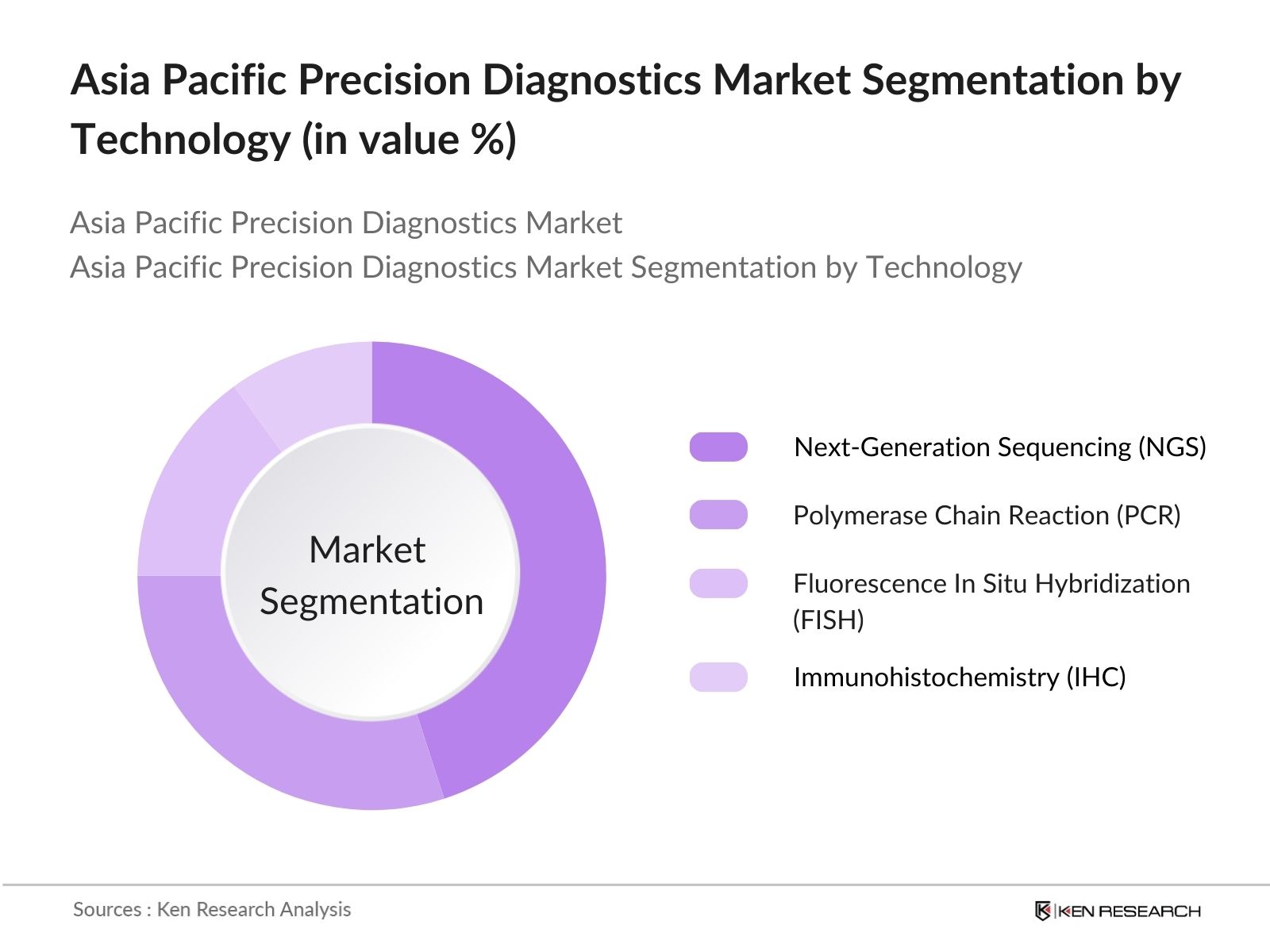

- By Technology: The Asia Pacific Precision Diagnostics Market is segmented by technology into Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), Fluorescence In Situ Hybridization (FISH), and Immunohistochemistry (IHC). Among these, NGS holds the dominant market share due to its ability to provide comprehensive genetic insights at a lower cost compared to traditional methods. NGS is widely used in oncology diagnostics, allowing for the identification of mutations and genomic variants that guide personalized treatment approaches. The growing number of NGS-based clinical trials and its application in liquid biopsy further strengthen its market position.

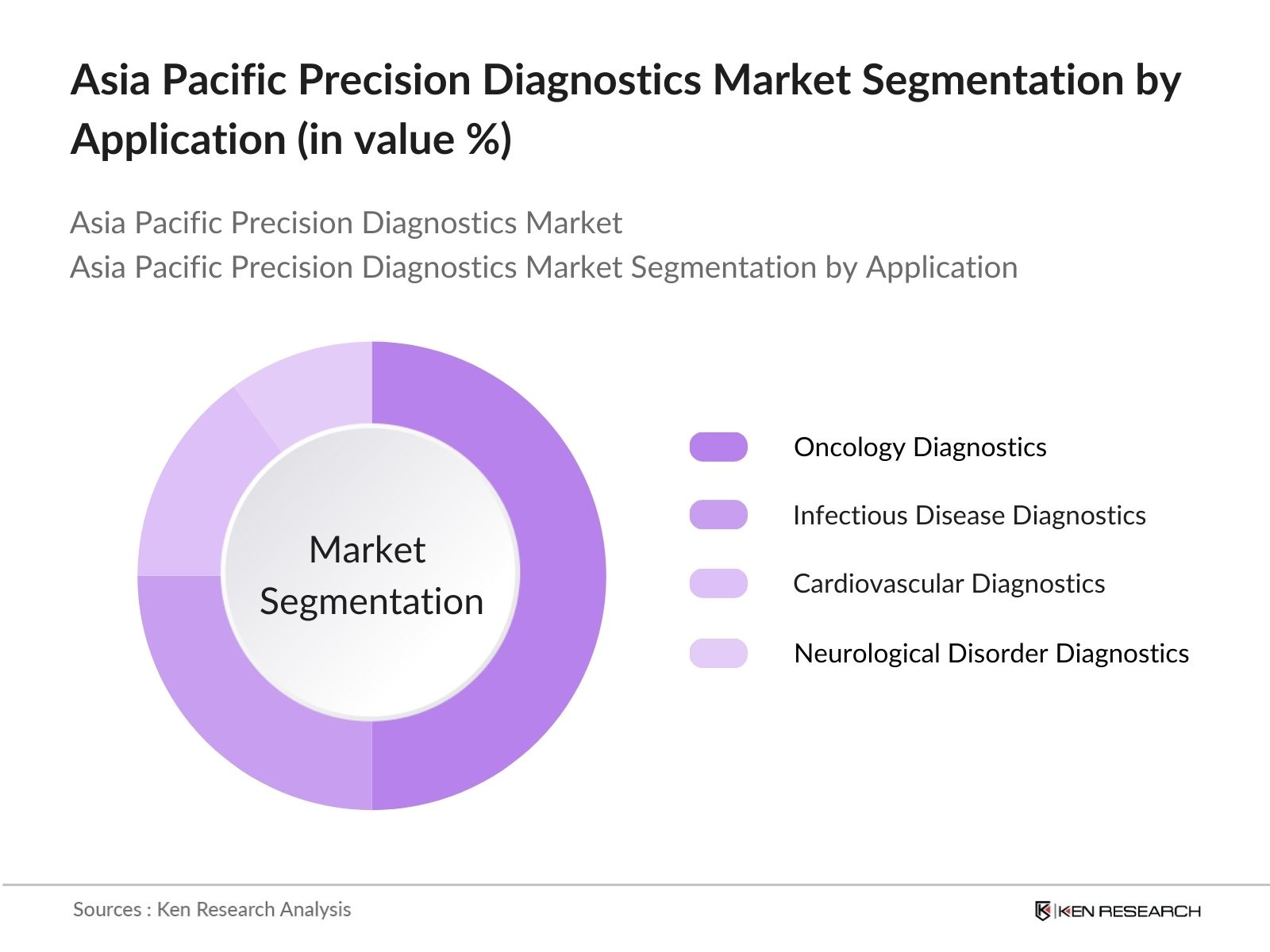

- By Application: The market is also segmented by application into Oncology Diagnostics, Infectious Disease Diagnostics, Cardiovascular Diagnostics, and Neurological Disorder Diagnostics. Oncology Diagnostics is the leading sub-segment, accounting for the largest market share, driven by the rising prevalence of cancer across the Asia Pacific region. The increasing need for personalized treatment approaches in oncology, combined with the use of advanced diagnostics such as NGS and liquid biopsy, has led to the dominance of this sub-segment. The growing awareness about early detection and precision treatment of cancer is further driving demand for oncology diagnostics.

Asia Pacific Precision Diagnostics Market Competitive Landscape

The Asia Pacific Precision Diagnostics Market is dominated by a few key global and regional players, leveraging their strong research and development capabilities and extensive distribution networks. Companies like Roche Diagnostics, Illumina, and Thermo Fisher Scientific have been at the forefront of innovation in genomics and personalized medicine, establishing themselves as leaders in the market. These companies have also engaged in strategic collaborations and partnerships to enhance their market reach and product portfolios.

Company | Year of Establishment | Headquarters | R&D Expenditure | Technology Portfolio | Regional Presence | Market Share (%) | Strategic Initiatives | Mergers & Acquisitions |

Roche Diagnostics | 1896 | Basel, Switzerland | - | - | - | - | - | - |

Illumina Inc. | 1998 | California, USA | - | - | - | - | - | - |

Thermo Fisher Scientific | 1956 | Massachusetts, USA | - | - | - | - | - | - |

Agilent Technologies | 1999 | California, USA | - | - | - | - | - | - |

Qiagen N.V. | 1984 | Hilden, Germany | - | - | - | - | - | - |

Asia Pacific Precision Diagnostics Market Analysis

Asia Pacific Precision Diagnostics Market Growth Drivers

- Increase in Genomic Testing: The increase in genomic testing is a major growth driver in the Asia Pacific precision diagnostics market, with substantial focus on precision medicine and genetic screening. In 2024, over 50 million genetic tests are projected to be conducted globally, and Asia Pacific is emerging as a critical region for this market, driven by countries like China and Japan, which have invested heavily in precision medicine initiatives. For example, Chinas National Genomics Project alone aims to sequence one million genomes by 2025. As the healthcare expenditure per capita in the region grows, currently at $1,317 in Japan (World Bank), genomic testing is becoming more accessible, contributing to market expansion.

- Rise in Chronic Diseases: The rise in chronic diseases like cancer and cardiovascular diseases is propelling demand for precision diagnostics. In 2023, the World Health Organization (WHO) reported that over 8 million people in the Asia Pacific region were diagnosed with cancer, accounting for 44% of global cases. Cardiovascular diseases, responsible for 10 million deaths annually in the region (WHO, 2024), further underscore the need for precision diagnostics. These conditions necessitate advanced diagnostic tools for early detection, fostering growth in the market. Governments are responding by increasing healthcare budgetsIndia, for example, raised healthcare spending to $30 billion in 2023 (IMF).

- Technological Advancements: Technological advancements, particularly in Next-Generation Sequencing (NGS) and digital pathology, are key drivers of the Asia Pacific precision diagnostics market. NGS technologies are being widely adopted across the region, with over 1,000 sequencing facilities operational in China and Japan in 2023. These technologies have drastically reduced the time required for genetic sequencing, now possible in less than 24 hours (NIH, 2024). The push for automation in diagnostics, with digital pathology systems now installed in over 300 hospitals across South Korea, is enabling faster, more accurate disease detection and is transforming the diagnostic landscape.

Asia Pacific Precision Diagnostics Market Challenges

- High Costs of Precision Diagnostic Tests: One of the primary challenges in the Asia Pacific precision diagnostics market is the high cost of precision diagnostic tests. A single genome sequencing test can cost between $800 to $1,500, making it unaffordable for a large portion of the population, particularly in developing countries like India and Indonesia. While healthcare spending is rising across the region, with countries like Indonesia increasing their health budget by 7% in 2024 (World Bank), these costs remain prohibitive for widespread adoption, limiting access to advanced diagnostic tools in lower-income populations.

- Regulatory and Compliance Barriers: Regulatory and compliance barriers pose major challenges for the precision diagnostics market in Asia Pacific. The region lacks uniform regulatory frameworks, with different countries adhering to diverse regulations. In 2024, China imposed stringent clinical trial requirements for diagnostic products, causing delays in product approvals by up to 12 months (IMF). Additionally, compliance costs in countries like South Korea have increased by 18%, as reported by the government in 2023. These barriers create complexities for companies looking to expand their precision diagnostics offerings across multiple countries in the region.

Asia Pacific Precision Diagnostics Market Future Outlook

Over the next five years, the Asia Pacific Precision Diagnostics Market is expected to experience robust growth, driven by increasing demand for personalized medicine, advancements in diagnostic technologies, and government initiatives to improve healthcare outcomes. The growing focus on early disease detection, particularly in oncology, will continue to fuel market growth. Key players in the market are expected to invest heavily in research and development to introduce innovative diagnostic solutions that cater to the evolving needs of healthcare providers and patients.

Asia Pacific Precision Diagnostics Market Opportunities

- Increasing Adoption of Companion Diagnostics: The adoption of companion diagnostics, which are used to select appropriate treatments for patients, is increasing in the Asia Pacific region. In 2023, over 500 companion diagnostic tests were approved in Japan and South Korea, making it one of the fastest-growing segments in the precision diagnostics market. This adoption is driven by advancements in personalized medicine, which is gaining momentum in treating diseases like cancer. The growing healthcare infrastructure and investment in research and development, with South Korea allocating $500 million to biopharma research in 2024, are driving this trend (IMF).

- Growth of AI and Data Analytics: The integration of AI and data analytics into precision diagnostics is an emerging opportunity. In 2024, AI-driven diagnostics have become critical in analyzing vast amounts of genomic data. In China, more than 150 hospitals have implemented AI-based diagnostic tools that enhance the accuracy of predictive modeling for diseases like cancer and Alzheimers (IMF). These technologies are reducing the time to diagnosis, with AI-powered systems processing data 10 times faster than traditional methods. The development of AI in diagnostics is poised to revolutionize the market, improving patient outcomes across the region.

Scope of the Report

Technology | PCR NGS FISH Digital Pathology IHC |

Application | Oncology Diagnostics Infectious Diseases Genetic Testing Cardiovascular Neurological |

End-User | Hospitals Diagnostic Labs Research Institutes Clinics Pharma & Biotech Companies |

Sample Type | Blood Tissue Biopsy Liquid Biopsy Saliva Urine |

Country | China Japan India Australia South Korea |

Products

Key Target Audience

Government and Regulatory Bodies (National Medical Products Administration, Pharmaceuticals and Medical Devices Agency)

Hospitals and Diagnostic Laboratories

Biotechnology and Pharmaceutical Companies

Medical Device Manufacturers

Banks and Financial Institutions

Research Institutes and Academia

Healthcare IT Companies

Investors and Venture Capitalist Firms

Healthcare Service Providers

Companies

Players Mentioned in the Report

Roche Diagnostics

Illumina Inc.

Thermo Fisher Scientific

Agilent Technologies

Qiagen N.V.

Bio-Rad Laboratories

Danaher Corporation

PerkinElmer Inc.

Siemens Healthineers

Myriad Genetics

Table of Contents

1. Asia Pacific Precision Diagnostics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Precision Diagnostics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Precision Diagnostics Market Analysis

3.1. Growth Drivers

3.1.1. Increase in Genomic Testing (Precision Medicine, Genetic Screening)

3.1.2. Rise in Chronic Diseases (Cancer, Cardiovascular Diseases)

3.1.3. Technological Advancements (Next-Generation Sequencing, Digital Pathology)

3.1.4. Government and Private Investments (Health Initiatives, Funding)

3.2. Market Challenges

3.2.1. High Costs of Precision Diagnostic Tests

3.2.2. Regulatory and Compliance Barriers (Asia Pacific Region)

3.2.3. Lack of Standardization (Cross-Country Standardization)

3.3. Opportunities

3.3.1. Increasing Adoption of Companion Diagnostics

3.3.2. Growth of AI and Data Analytics (AI in Diagnostics, Predictive Modeling)

3.3.3. Expansion of Telehealth and Remote Diagnostics (Telemedicine, Mobile Diagnostics)

3.4. Trends

3.4.1. Integration of AI for Predictive Diagnostics

3.4.2. Personalized Medicine (Targeted Therapies)

3.4.3. Cross-Border Healthcare Collaborations (Partnerships for Clinical Trials)

3.5. Regulatory Framework

3.5.1. Precision Diagnostics Guidelines (ISO, FDA)

3.5.2. Regional Regulations (Country-Specific Regulatory Bodies)

3.5.3. Patents and Intellectual Property Protection

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Analysis

4. Asia Pacific Precision Diagnostics Market Segmentation

4.1. By Technology (In Value %)

4.1.1. Polymerase Chain Reaction (PCR)

4.1.2. Next-Generation Sequencing (NGS)

4.1.3. Fluorescence In Situ Hybridization (FISH)

4.1.4. Digital Pathology

4.1.5. Immunohistochemistry (IHC)

4.2. By Application (In Value %)

4.2.1. Oncology Diagnostics

4.2.2. Infectious Disease Diagnostics

4.2.3. Genetic and Genomic Testing

4.2.4. Cardiovascular Diagnostics

4.2.5. Neurological Disorder Diagnostics

4.3. By End-User (In Value %)

4.3.1. Hospitals

4.3.2. Diagnostic Laboratories

4.3.3. Research Institutes

4.3.4. Specialty Clinics

4.3.5. Pharmaceutical and Biotech Companies

4.4. By Sample Type (In Value %)

4.4.1. Blood

4.4.2. Tissue Biopsy

4.4.3. Liquid Biopsy

4.4.4. Saliva

4.4.5. Urine

4.5. By Country (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. Australia

4.5.5. South Korea

5. Asia Pacific Precision Diagnostics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Roche Diagnostics

5.1.2. Illumina Inc.

5.1.3. Thermo Fisher Scientific

5.1.4. Agilent Technologies

5.1.5. Bio-Rad Laboratories

5.1.6. Qiagen N.V.

5.1.7. Danaher Corporation

5.1.8. PerkinElmer Inc.

5.1.9. Siemens Healthineers

5.1.10. Myriad Genetics

5.1.11. Abbott Laboratories

5.1.12. GE Healthcare

5.1.13. Pacific Biosciences

5.1.14. Genomic Health

5.1.15. Luminex Corporation

5.2. Cross Comparison Parameters (Technology Portfolio, R&D Expenditure, Regional Presence, Market Share, Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Funding Programs

6. Asia Pacific Precision Diagnostics Market Regulatory Framework

6.1. Compliance Standards (ISO, FDA, CE Marking)

6.2. Quality Control Requirements

6.3. Certification Processes

6.4. Licensing and Patent Regulations

7. Asia Pacific Precision Diagnostics Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Precision Diagnostics Future Market Segmentation

8.1. By Technology (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Sample Type (In Value %)

8.5. By Country (In Value %)

9. Asia Pacific Precision Diagnostics Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Product Development Strategies

9.3. White Space Opportunity Analysis

9.4. Customer Segment Prioritization

DisclaimerContact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Asia Pacific Precision Diagnostics Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the Asia Pacific Precision Diagnostics Market. This includes assessing market penetration, the ratio of technology adoption to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through interviews with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights, refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with diagnostic equipment manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the Asia Pacific Precision Diagnostics Market.

Frequently Asked Questions

01. How big is the Asia Pacific Precision Diagnostics Market?

The Asia Pacific Precision Diagnostics Market is valued at USD 2.1 billion, driven by advancements in genomics and demand for personalized medicine.

02. What are the major challenges in the Asia Pacific Precision Diagnostics Market?

The major challenges in the Asia Pacific Precision Diagnostics Market include the high cost of precision diagnostic tools, regulatory hurdles, and a lack of standardization across countries in the Asia Pacific region.

03. Who are the key players in the Asia Pacific Precision Diagnostics Market?

Key players in the Asia Pacific Precision Diagnostics Market include Roche Diagnostics, Illumina Inc., Thermo Fisher Scientific, Agilent Technologies, and Qiagen N.V., among others.

04. What drives growth in the Asia Pacific Precision Diagnostics Market?

The Asia Pacific Precision Diagnostics Market is driven by the rising demand for early disease diagnosis, especially for chronic conditions like cancer and cardiovascular diseases, along with technological advancements in genomics and data analytics.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.