Asia Pacific Premium Bottled Water Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD5611

November 2024

80

About the Report

Asia Pacific Premium Bottled Water Market Overview

- The Asia Pacific premium bottled water market is valued at USD 3.5 billion, driven by rising health consciousness among consumers and increasing disposable incomes across the region. Premium bottled water is viewed as a healthier and more purified alternative to tap water, and its demand is being further fueled by the growing number of fitness-conscious individuals who prefer natural mineral or spring water.

- Countries such as China, Japan, and Australia dominate the market due to their advanced distribution networks and higher consumer awareness regarding health and wellness. In China, the sheer size of the population, combined with increasing urbanization and concerns over tap water safety, propels the demand for premium bottled water. Japan's dominance is attributed to its strong culture of healthy living, while Australia's market is driven by its preference for high-quality and environmentally sustainable water brands.

- Governments in Southeast Asia, led by countries like Malaysia and Thailand, are advancing their Circular Economy Action Plan, aimed at promoting sustainability across industries. In 2024, these governments earmarked $150 million in funding to support innovations in packaging, recycling, and waste management. Premium bottled water companies are encouraged to adopt circular economy principles, which will drive the development of reusable and biodegradable bottles in the coming years.

Asia Pacific Premium Water Bottled Market Segmentation

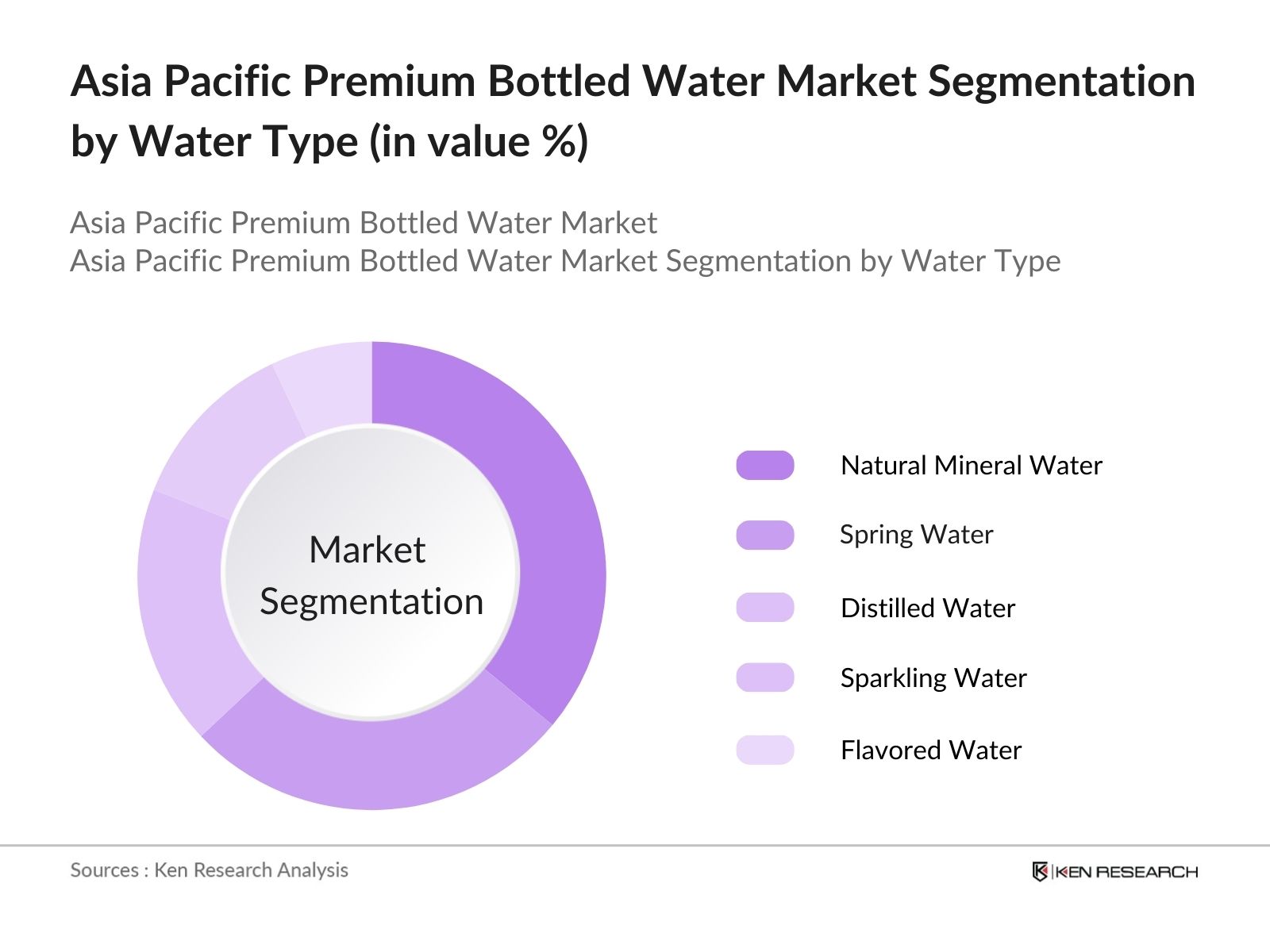

By Water Type: The market is segmented by water type into natural mineral water, spring water, distilled water, sparkling water, and flavored water. Natural mineral water currently dominates the market, largely due to its perceived health benefits. Consumers prefer mineral water for its natural source and essential minerals, which are believed to promote overall well-being. Additionally, brands such as VOSS and Fiji Water, which offer natural mineral water, have established strong brand loyalty among consumers due to their premium quality and marketing efforts.

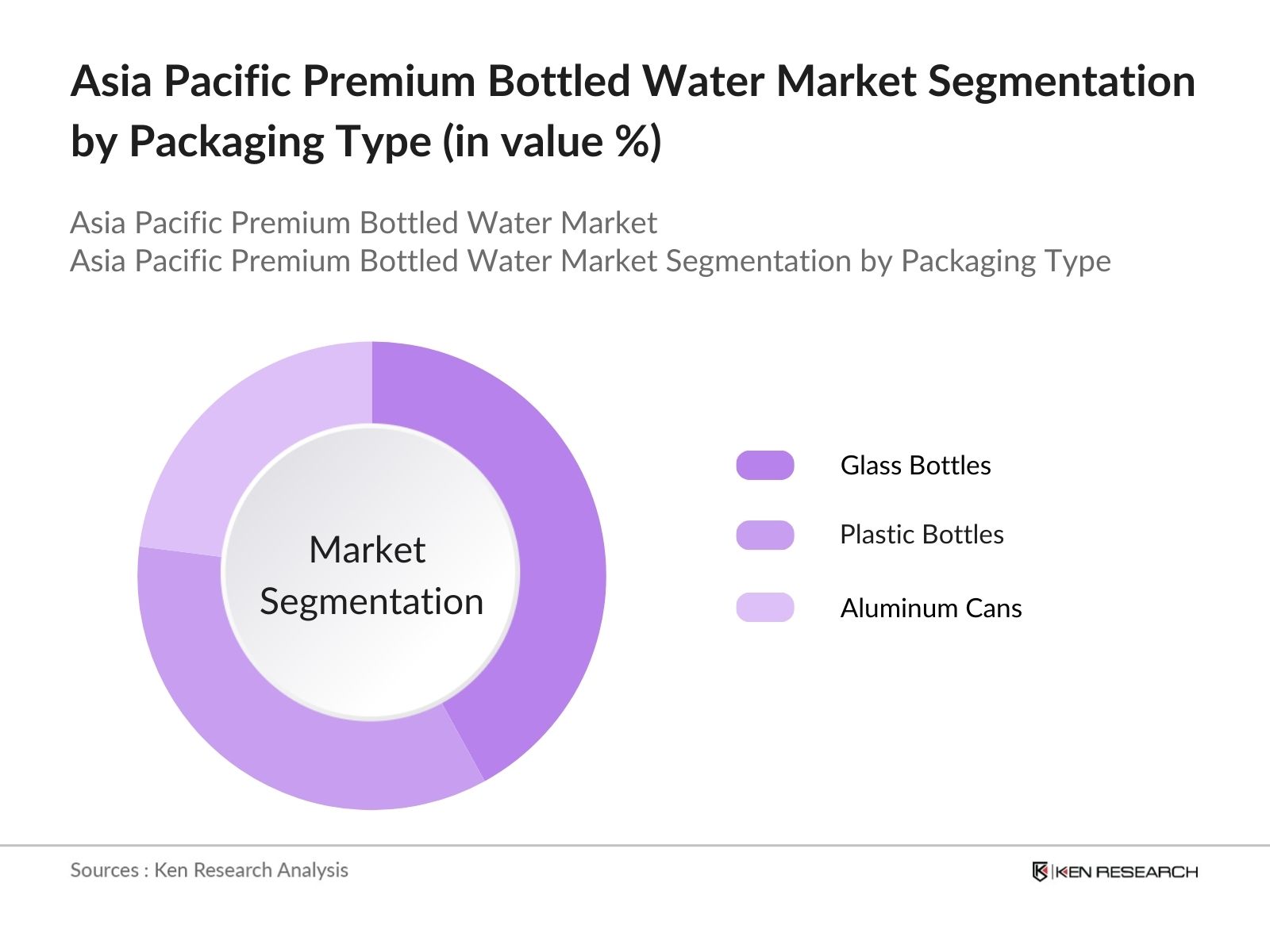

By Packaging Type: The market is also segmented by packaging type, including glass bottles, plastic bottles, and aluminum cans. Glass bottles dominate the market due to their premium positioning and environmental benefits. Glass packaging is preferred by environmentally conscious consumers and is often used by high-end brands to enhance their products luxury image. Many consumers associate glass bottles with purity and higher quality, which supports their dominance in the premium bottled water market.

Asia Pacific Premium Water Bottled Market Competitive Landscape

The market is dominated by several key players, including multinational companies and domestic brands. The market is highly competitive, with leading brands leveraging their strong distribution networks, high product quality, and strategic marketing campaigns to maintain their market position.

|

Company Name |

Establishment Year |

Headquarters |

Annual Revenue |

Number of Employees |

Global Reach |

Product Range |

Sustainability Initiatives |

Key Markets |

|

Nestl Waters |

1992 |

Switzerland |

||||||

|

Danone Waters |

1973 |

France |

||||||

|

Nongfu Spring Co., Ltd. |

1996 |

China |

||||||

|

VOSS Water |

2001 |

Norway |

||||||

|

Fiji Water |

1996 |

Fiji |

Asia Pacific Premium Bottled Water Market Analysis

Market Growth Drivers

- Rising Health Awareness Among Consumers: The Asia Pacific region has witnessed an increase in demand for premium bottled water due to growing consumer awareness regarding health and wellness. The shift towards healthy and functional beverages has driven demand, with consumers increasingly seeking high-quality, mineral-rich bottled water. In 2024, over 230 million people in China alone are actively choosing premium bottled water for its perceived health benefits, aligning with the growing wellness trend in the region.

- Expansion of the Hospitality and Tourism Industry: The market is being fueled by the expansion of luxury hotels, resorts, and fine dining establishments across the Asia Pacific region. The region welcomed more than 350 million international tourists in 2023, which includes high-net-worth individuals who prefer premium water options. Luxury hotels in countries like Japan and Thailand report serving 50 million bottles of premium water annually, with demand rising in tandem with high-end tourism growth.

- Environmental and Sustainability Concerns Leading to Eco-friendly Packaging: Governments in the Asia Pacific region have tightened regulations around plastic waste management, prompting premium bottled water companies to adopt sustainable packaging solutions. In 2024, regulatory changes in Japan and South Korea have resulted in the use of eco-friendly materials in over 80 million premium bottled water packages. This shift has been driven by stringent government mandates, including China's nationwide plan to cut single-use plastic production by 25 billion units in the next five years.

Market Challenges

- Competition from Local Water Sources and Brands: Many countries in the Asia Pacific region have a long history of local mineral and spring water brands, which are often preferred by consumers over imported premium brands. In South Korea, local brands such as Samdasoo dominate 65 million liters of premium bottled water sold annually. The strength of these local brands, coupled with their historical significance and consumer loyalty, poses a challenge for international premium brands attempting to capture market share.

- Regulatory Hurdles and Compliance Costs: The bottled water industry faces increasing scrutiny from governments across Asia Pacific due to environmental concerns, labeling standards, and health safety regulations. In 2024, new regulations in Australia and New Zealand impose stricter quality and transparency standards, impacting nearly 40% of premium bottled water imports. The costs associated with meeting these stringent standards, including testing and certification processes, have caused delays in product launches and increased operational costs for premium bottled water companies.

Asia Pacific Premium Bottled Water Market Future Outlook

Over the next five years, the Asia Pacific premium bottled water industry is expected to show growth, driven by increasing consumer demand for high-quality, healthy beverages and a greater focus on environmental sustainability. Key factors that will contribute to this growth include the expansion of distribution networks, especially in rural areas, and the development of innovative and eco-friendly packaging solutions.

Future Market Opportunities

- Increased Adoption of Sustainable Packaging Solutions: Over the next five years, premium bottled water companies will increasingly adopt sustainable packaging solutions. By 2029, it is estimated that 100 million units of premium bottled water sold in the Asia Pacific region will be packaged using biodegradable or plant-based materials. This trend will be driven by growing consumer demand for environmentally friendly products and increasing government regulations on plastic usage.

- Technological Integration in Bottled Water Tracking: In the future, premium bottled water brands will leverage blockchain and smart technology to ensure product transparency and traceability. By 2029, over 70 million bottles of premium water are expected to include QR codes or other traceability features, allowing consumers to track the water source and processing stages, aligning with the rising demand for transparency in product origin.

Scope of the Report

|

Water Type |

Natural Mineral Water Spring Water Distilled Water Sparkling Water Flavored Water |

|

Packaging Type |

Glass Bottles Plastic Bottles Aluminum Cans |

|

Distribution Channel |

Supermarkets/Hypermarkets Specialty Stores Online Retail HoReCa |

|

End-User |

Residential Commercial Institutional |

|

Region |

China India Japan Australia Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Premium bottled water manufacturers

Banks and Financial Institution

Private Equity Firms

Government and regulatory bodies (Food Safety and Standards Authority of India, China Food and Drug Administration)

Investments and venture capital firms

Packaging and bottling solution providers

Companies

Players Mentioned in the Report:

Nestl Waters

Danone Waters

The Coca-Cola Company

PepsiCo Inc.

Nongfu Spring Co., Ltd.

VOSS Water

Tata Global Beverages

Fiji Water Company LLC

Asahi Group Holdings, Ltd.

Perrier-Jout

Ferrarelle

Suntory Beverage & Food

Evian

Highland Spring Group

Waiakea Hawaiian Volcanic Water

Table of Contents

1. Asia Pacific Premium Bottled Water Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (in terms of CAGR)

1.4. Market Segmentation Overview

2. Asia Pacific Premium Bottled Water Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Premium Bottled Water Market Analysis

3.1. Growth Drivers

3.1.1. Health-conscious consumer trends

3.1.2. Urbanization and lifestyle shifts

3.1.3. Premiumization in beverage choices

3.1.4. Increase in tourism and hospitality sectors

3.2. Market Challenges

3.2.1. High costs associated with packaging and distribution

3.2.2. Environmental concerns and regulatory constraints

3.2.3. Intense competition and counterfeit products

3.3. Opportunities

3.3.1. Rising demand for sustainable packaging solutions

3.3.2. Technological advancements in water filtration and bottling

3.3.3. Expansion into rural and semi-urban markets

3.4. Trends

3.4.1. Shift towards glass and aluminum packaging

3.4.2. Growing preference for functional and flavored bottled water

3.4.3. Strategic collaborations and brand endorsements

3.5. Government Regulation

3.5.1. Bottled water safety standards and quality control

3.5.2. Sustainability and environmental packaging mandates

3.5.3. Import-export regulations and tariffs on premium water brands

3.6. SWOT Analysis

3.6.1. Strengths

3.6.2. Weaknesses

3.6.3. Opportunities

3.6.4. Threats

3.7. Stake Ecosystem (Manufacturers, Distributors, Retailers)

3.8. Porters Five Forces (Bargaining Power of Suppliers, Buyers, New Entrants, Substitutes, Competitive Rivalry)

3.9. Competition Ecosystem

4. Asia Pacific Premium Bottled Water Market Segmentation

4.1. By Water Type (In Value %)

4.1.1. Natural Mineral Water

4.1.2. Spring Water

4.1.3. Distilled Water

4.1.4. Sparkling Water

4.1.5. Flavored Water

4.2. By Packaging Type (In Value %)

4.2.1. Glass Bottles

4.2.2. Plastic Bottles

4.2.3. Aluminum Cans

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets/Hypermarkets

4.3.2. Specialty Stores

4.3.3. Online Retail

4.3.4. HoReCa (Hotels, Restaurants, and Cafes)

4.4. By End-User (In Value %)

4.4.1. Residential

4.4.2. Commercial (Hotels, Offices, Gyms, etc.)

4.4.3. Institutional

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. Rest of APAC

5. Asia Pacific Premium Bottled Water Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Nestl Waters

5.1.2. Danone Waters

5.1.3. The Coca-Cola Company

5.1.4. PepsiCo Inc.

5.1.5. Fiji Water Company LLC

5.1.6. VOSS Water

5.1.7. Tata Global Beverages

5.1.8. Nongfu Spring Co., Ltd.

5.1.9. Asahi Group Holdings, Ltd.

5.1.10. Perrier-Jout

5.1.11. Ferrarelle

5.1.12. Suntory Beverage & Food

5.1.13. Evian

5.1.14. Highland Spring Group

5.1.15. Waiakea Hawaiian Volcanic Water

5.2. Cross Comparison Parameters (Annual Revenue, Headquarters, Product Range, Sustainability Initiatives, Market Penetration, Packaging Innovations, Key Geographic Markets, Pricing Strategies)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. Asia Pacific Premium Bottled Water Market Regulatory Framework

6.1. Environmental Standards

6.2. Packaging and Labeling Requirements

6.3. Water Resource Management Regulations

7. Asia Pacific Premium Bottled Water Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Premium Bottled Water Future Market Segmentation

8.1. By Water Type (In Value %)

8.2. By Packaging Type (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Premium Bottled Water Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase of this research involved identifying the key variables influencing the Asia Pacific premium bottled water market. Extensive desk research was conducted using secondary sources such as industry reports, proprietary databases, and company filings to map out the stakeholder ecosystem and to understand the various factors affecting market growth.

Step 2: Market Analysis and Construction

The second step focused on analyzing historical data and constructing a detailed market model for the Asia Pacific region. This involved assessing the penetration of premium bottled water products, evaluating distribution channels, and determining the revenue generated by different segments. Additionally, key performance indicators (KPIs) such as product quality, packaging innovation, and distribution efficiency were measured.

Step 3: Hypothesis Validation and Expert Consultation

To validate our market findings, we engaged in structured interviews with industry experts, including executives from leading bottled water brands, distributors, and suppliers. These interviews provided crucial insights into the operational challenges and emerging opportunities within the market, thereby helping refine our market estimates and growth projections.

Step 4: Research Synthesis and Final Output

The final phase entailed the synthesis of all gathered data, including insights from both desk research and expert interviews, to produce an accurate and comprehensive report. The final output was verified through interactions with manufacturers and distributors to ensure that the findings aligned with industry trends and market dynamics.

Frequently Asked Questions

How big is the Asia Pacific Premium Bottled Water Market?

The Asia Pacific premium bottled water market is valued at USD 3.5 billion, driven by increasing consumer health awareness and rising disposable incomes.

What are the challenges in the Asia Pacific Premium Bottled Water Market?

Challenges in the Asia Pacific premium bottled water market includes high production and packaging costs, environmental concerns over plastic usage, and regulatory hurdles in key markets such as China and Japan.

Who are the major players in the Asia Pacific Premium Bottled Water Market?

Key players in the Asia Pacific premium bottled water market include Nestl Waters, Danone Waters, Nongfu Spring Co., Ltd., VOSS Water, and Tata Global Beverages, all of whom dominate through extensive distribution networks and strong brand recognition.

What are the growth drivers of the Asia Pacific Premium Bottled Water Market?

Growth drivers in the Asia Pacific premium bottled water market include rising health consciousness, increasing urbanization, and consumer preference for high-quality and eco-friendly beverage options.

What trends are shaping the future of the Asia Pacific Premium Bottled Water Market?

Emerging trends in the Asia Pacific premium bottled water market include the shift towards sustainable packaging solutions, the rising popularity of flavored and functional water, and increased collaborations with hospitality chains for premium water offerings.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.