Asia Pacific Refrigerator Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD3628

December 2024

83

About the Report

Asia Pacific Refrigerator Market Overview

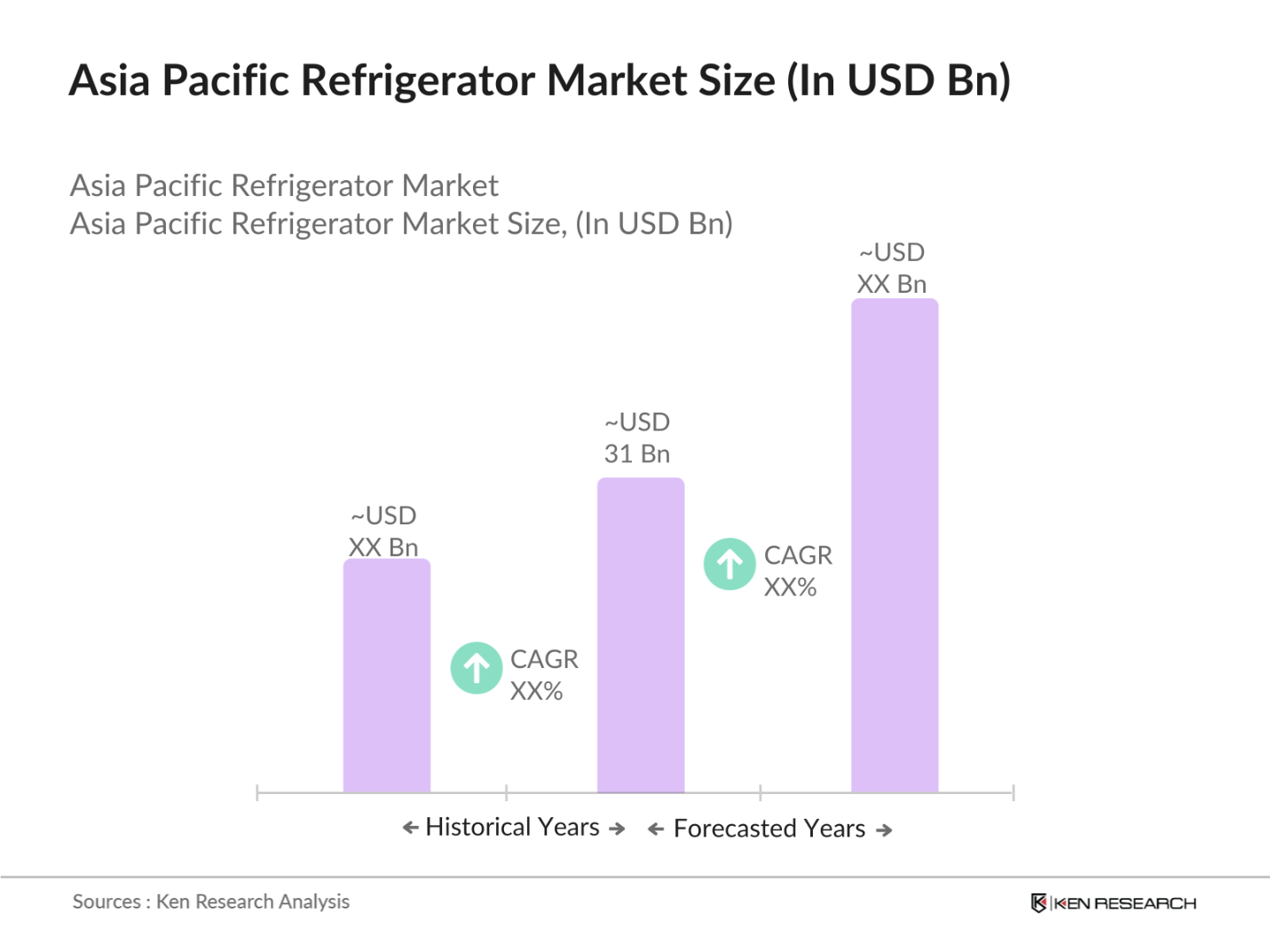

- The Asia Pacific refrigerator market is valued at USD 31 billion, driven by rapid urbanization and the growing adoption of smart home appliances. The market's expansion is fueled by increasing consumer demand for energy-efficient refrigerators, supported by governmental regulations promoting energy conservation. The growing middle class, especially in emerging economies like China and India, has contributed significantly to rising demand, as disposable incomes enable more households to upgrade to modern, technology-integrated appliances.

- China and India are the leading countries in the Asia Pacific refrigerator market, due to their large population bases and increasing urbanization. China's dominance is attributed to the strong presence of local manufacturers like Haier and Midea, who offer affordable yet advanced refrigerator models. India, on the other hand, has seen robust demand for refrigerators due to rising electrification in rural areas and government initiatives like "Make in India," encouraging local manufacturing. Additionally, both nations benefit from evolving consumer preferences for smart.

- Government regulations on energy efficiency are becoming increasingly stringent in the Asia Pacific region. In 2022, new Minimum Energy Performance Standards (MEPS) were implemented, mandating that all new refrigerators meet specific energy consumption benchmarks. Compliance rates among major manufacturers reached 90%, reflecting the industry's commitment to sustainability. As energy efficiency regulations continue to evolve, they will significantly influence product development and innovation in the refrigerator market, encouraging manufacturers to focus on energy-efficient technologies.

Asia Pacific Refrigerator Market Segmentation

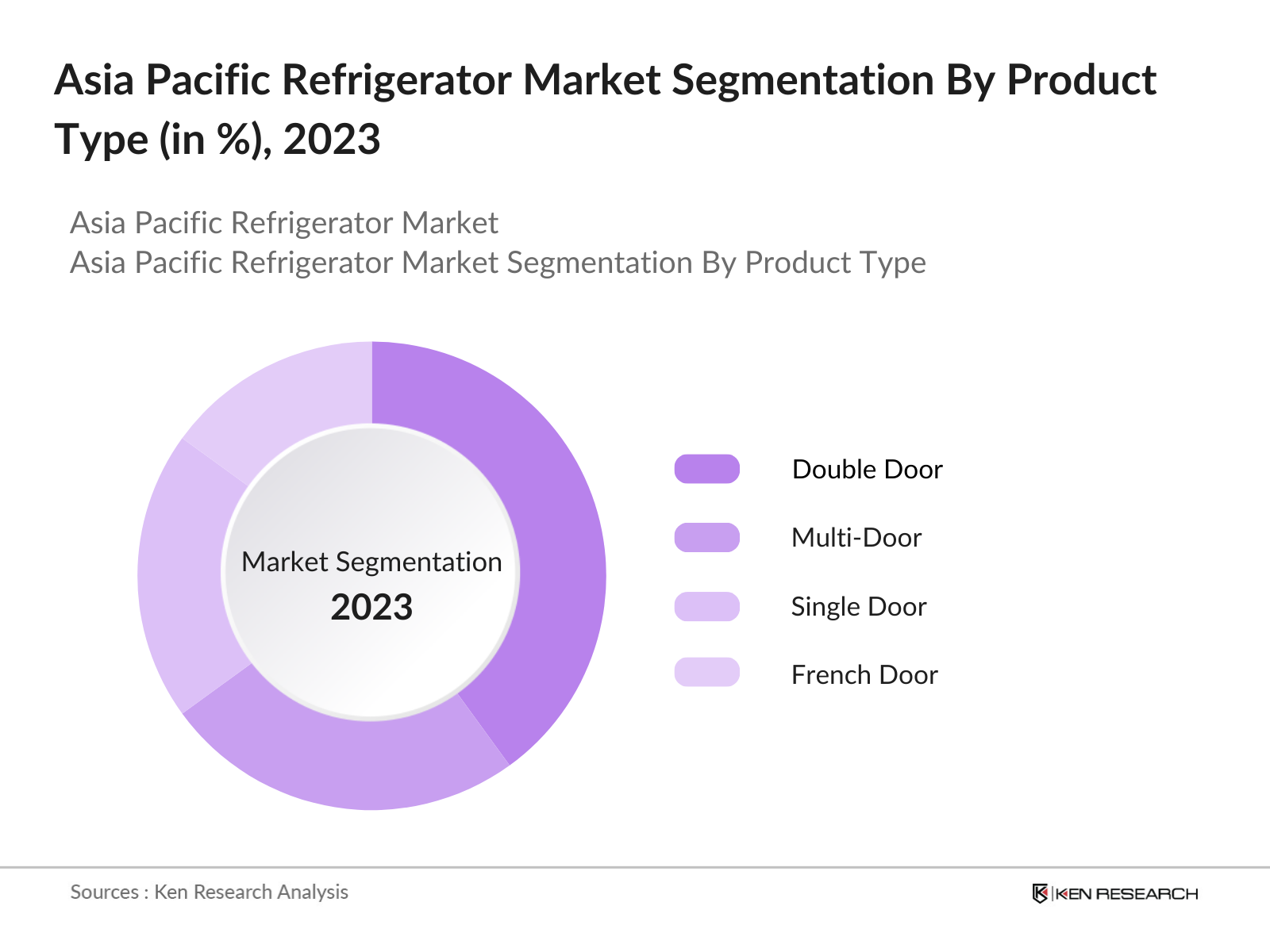

By Product Type: The Asia Pacific refrigerator market is segmented by product type into single door, double door, multi-door, and French door refrigerators. Among these, double door refrigerators hold a dominant market share due to their large capacity, affordable price range, and suitability for middle-income households. Brands such as LG and Samsung have introduced models with frost-free technology, further boosting the popularity of double door refrigerators. These products cater well to the needs of families, providing better energy efficiency and more storage space.

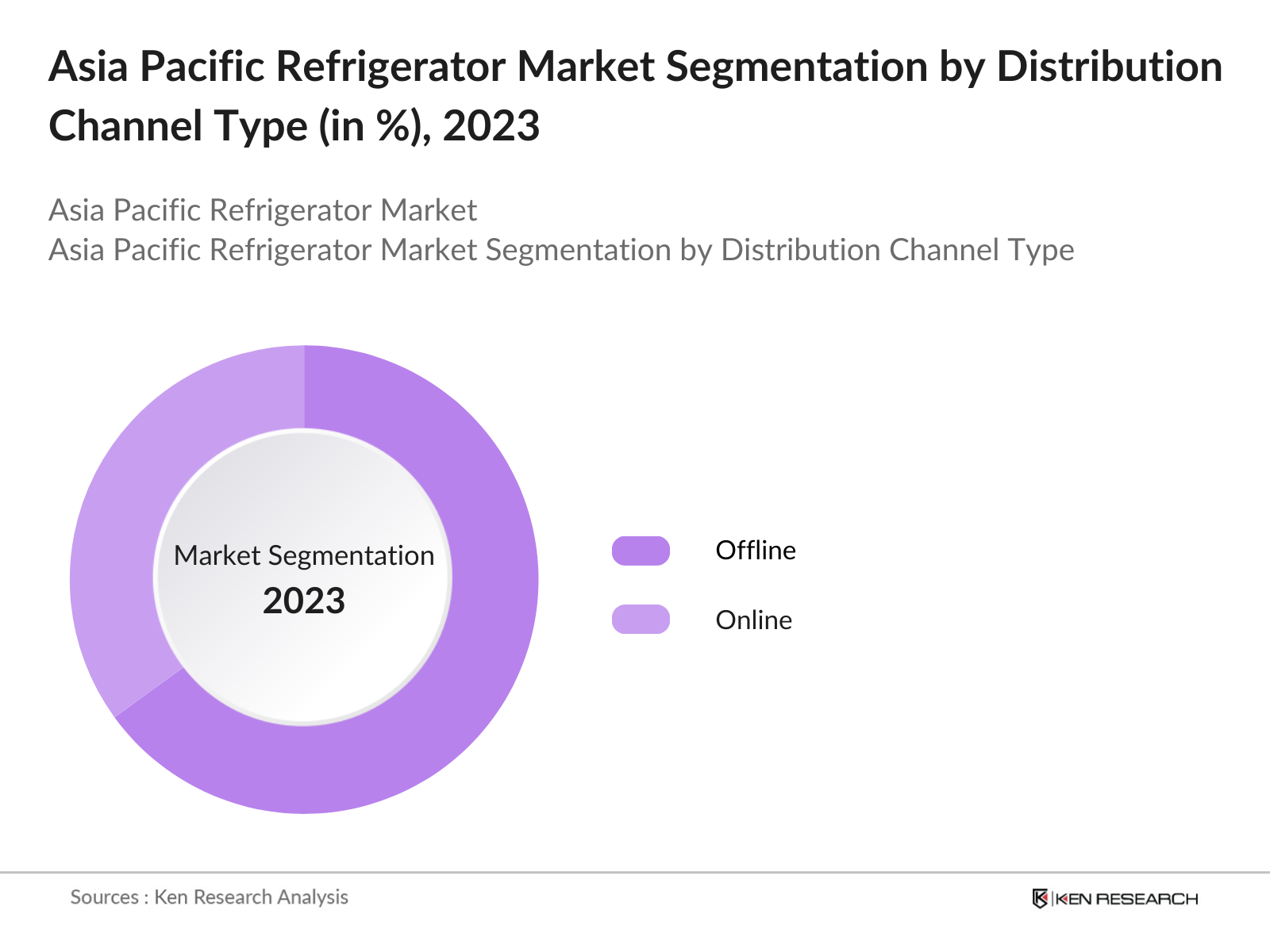

By Distribution Channel: The distribution channels in the Asia Pacific refrigerator market are divided into offline and online. Offline channels, particularly supermarkets and specialty stores, dominate the market, accounting for a significant share. This is largely because consumers in this region prefer to physically inspect products before purchasing. However, the online channel is gaining traction, especially in urban areas, thanks to the convenience of home delivery, competitive pricing, and easy access to reviews.

Asia Pacific Refrigerator Market Competitive Landscape

The Asia Pacific refrigerator market is dominated by several key players, with a mix of both local and international brands. Leading manufacturers are focusing on innovation, energy efficiency, and smart technology integration to maintain a competitive edge. The market is highly competitive, with companies investing heavily in research and development to meet the evolving consumer demand for sustainable and intelligent refrigeration solutions.

|

Company Name |

Established |

Headquarters |

Revenue (2023) |

No. of Employees |

Product Portfolio |

Innovation Index |

Energy Efficiency Standards |

Smart Technology Integration |

Sustainability Initiatives |

|

LG Electronics |

1958 |

South Korea |

|||||||

|

Samsung Electronics |

1938 |

South Korea |

|||||||

|

Haier Group Corporation |

1984 |

China |

|||||||

|

Whirlpool Corporation |

1911 |

USA |

|||||||

|

Panasonic Corporation |

1918 |

Japan |

Asia Pacific Refrigerator Industry Analysis

Growth Drivers

- Rising Disposable Income: The Asia Pacific region has seen significant increases in disposable income, with GDP per capita reaching approximately $4,500 in 2022 and projected to rise to around $5,200 by 2025. This growth is largely attributed to rapid urbanization, with urban populations expected to increase from 2.5 billion in 2022 to over 3 billion by 2025. Higher disposable incomes enable consumers to invest in modern appliances like refrigerators, reflecting a shift toward premium products. Urban centers are experiencing a growing middle class that prioritizes quality and technological advancement in home appliances.

- Expansion of Smart Homes: The proliferation of smart home technology is driving demand for refrigerators integrated with Internet of Things (IoT) capabilities. In 2022, the number of smart homes in the Asia Pacific was estimated at 185 million, projected to grow to 225 million by 2025. This trend is fueled by increasing consumer interest in convenience and energy efficiency. The integration of smart technology in refrigerators not only enhances user experience but also aligns with the regional push towards smarter living environments, creating a significant market opportunity.

- Increasing Consumer Preferences for Energy Efficiency: Consumer demand for energy-efficient appliances is on the rise, with energy-efficient refrigerator sales increasing significantly. In 2022, approximately 55% of refrigerators sold in the region were rated with Energy Star certifications, reflecting a growing awareness of energy consumption and environmental impact. This trend is supported by government initiatives aimed at reducing energy usage, with targets set to decrease energy consumption in residential sectors by 15% by 2025. As energy prices continue to rise, consumers are more inclined to invest in energy-efficient products, boosting market growth.

Market Challenges

- High Production Costs: The production costs of refrigerators in the Asia Pacific region are experiencing volatility due to fluctuations in raw material prices. For instance, the cost of steel, a key component in refrigerator manufacturing, surged by 30% in 2022 compared to 2021, driven by global supply chain issues. This rise in material costs poses challenges for manufacturers, leading to increased retail prices and potential impacts on consumer purchasing behavior. As production costs remain high, manufacturers must find ways to optimize operations to maintain competitiveness.

- Supply Chain Disruptions: Supply chain disruptions have significantly impacted the refrigerator market in the Asia Pacific, particularly post-pandemic. In 2022, shipping delays increased by 40%, causing delays in the availability of critical components for refrigerator manufacturing. These disruptions have resulted in a backlog of orders and heightened pressure on manufacturers to manage inventory effectively. Consequently, this challenge affects delivery timelines, increases costs, and hampers the ability to meet growing consumer demand for new and innovative products.

Asia Pacific Refrigerator Market Future Outlook

Over the next five years, the Asia Pacific refrigerator market is expected to experience significant growth, driven by the increasing demand for smart home appliances and energy-efficient solutions. The proliferation of internet penetration, especially in developing economies, will accelerate the adoption of smart refrigerators. Furthermore, advancements in inverter technology and government-backed energy efficiency programs are expected to support this markets expansion. The shift toward sustainable and eco-friendly refrigeration solutions will also play a crucial role in shaping the market's future trajectory.

Market Opportunities

- Rising Demand in Developing Markets: Developing markets within the Asia Pacific are experiencing a surge in demand for refrigerators, driven by urbanization and increasing household incomes. In 2022, the refrigerator penetration rate in emerging economies like India and Vietnam was approximately 35%, compared to 85% in developed countries. As these markets expand and more households transition to modern living standards, the demand for refrigeration solutions is projected to increase substantially. This trend presents significant growth opportunities for manufacturers looking to penetrate these emerging markets.

- Technological Advancements: Technological advancements in artificial intelligence and smart control systems are creating new opportunities in the refrigerator market. In 2022, around 40 million smart refrigerators with AI capabilities were sold in the Asia Pacific, up from 25 million in 2021. These innovations not only enhance energy efficiency but also improve user convenience through features such as inventory management and predictive maintenance. As consumers increasingly seek high-tech appliances, the market for smart refrigerators is expected to grow, providing manufacturers with a chance to diversify their offerings.

Scope of the Report

|

Product Type |

Single Door Double Door Multi-Door French Door |

|

Distribution Channel |

Offline Retail Online Channels |

|

End User |

Residential, Commercial |

|

Technology |

Smart Refrigerators Frost-Free Technology Inverter-Based Refrigerators |

|

Region |

China India Japan Australia South Korea |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Refrigerator Manufacturing Companies

Component Companies

Distribution and Retail Channels

Government and Regulatory Bodies (e.g., Bureau of Energy Efficiency, Department of Energy)

Investment and Venture Capitalist Firms

Smart Home Technology Companies

Renewable Energy Supplier Companies

Consumer Electronics Companies

Companies

Players Mentioned in the Report:

LG Electronics

Samsung Electronics

Haier Group Corporation

Whirlpool Corporation

Panasonic Corporation

Hitachi Appliances Inc.

Midea Group

Godrej Appliances

Bosch Siemens Hausgerte (BSH)

Electrolux

Toshiba Corporation

Hisense

Arelik A..

Sharp Corporation

Liebherr Appliances

Table of Contents

1. Asia Pacific Refrigerator Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Refrigerator Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Refrigerator Market Analysis

3.1. Growth Drivers

3.1.1. Rising Disposable Income (Urbanization, GDP per Capita Growth)

3.1.2. Expansion of Smart Homes (IoT Integration)

3.1.3. Increasing Consumer Preferences for Energy Efficiency (Energy Star Ratings)

3.1.4. Favorable Government Initiatives (Subsidies and Energy Policies)

3.2. Market Challenges

3.2.1. High Production Costs (Raw Material Price Volatility)

3.2.2. Supply Chain Disruptions (Shipping Delays, Component Shortages)

3.2.3. Strict Regulatory Compliance (Environmental Regulations, Energy Consumption Standards)

3.3. Opportunities

3.3.1. Rising Demand in Developing Markets (Penetration in Emerging Economies)

3.3.2. Technological Advancements (AI and Smart Control Systems)

3.3.3. Expansion of E-commerce Channels (Direct-to-Consumer Sales)

3.4. Trends

3.4.1. Growth in Multi-Door and French Door Refrigerators

3.4.2. Increasing Adoption of Smart Refrigerators (Voice Control, Remote Monitoring)

3.4.3. Customization in Design (Modular, Built-in Refrigerators)

3.5. Government Regulation

3.5.1. Appliance Energy Efficiency Regulations (Minimum Energy Performance Standards)

3.5.2. Import Tariffs and Trade Policies (Impact on Cost and Availability)

3.5.3. Environmental Protection Policies (Refrigerant Regulations, Carbon Footprint Reduction)

3.6. SWOT Analysis

3.7. Porters Five Forces Analysis

3.8. Competition Ecosystem

4. Asia Pacific Refrigerator Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Single Door

4.1.2. Double Door

4.1.3. Multi-Door

4.1.4. French Door

4.2. By Distribution Channel (In Value %)

4.2.1. Offline Retail (Supermarkets, Specialty Stores)

4.2.2. Online Channels

4.3. By End User (In Value %)

4.3.1. Residential

4.3.2. Commercial (Hotels, Restaurants, Retail Outlets)

4.4. By Technology (In Value %)

4.4.1. Smart Refrigerators

4.4.2. Frost-Free Technology

4.4.3. Inverter-Based Refrigerators

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. South Korea

5. Asia Pacific Refrigerator Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. LG Electronics

5.1.2. Samsung Electronics

5.1.3. Haier Group Corporation

5.1.4. Whirlpool Corporation

5.1.5. Panasonic Corporation

5.1.6. Hitachi Appliances Inc.

5.1.7. Midea Group

5.1.8. Godrej Appliances

5.1.9. Bosch Siemens Hausgerte (BSH)

5.1.10. Electrolux

5.1.11. Toshiba Corporation

5.1.12. Hisense

5.1.13. Arelik A..

5.1.14. Sharp Corporation

5.1.15. Liebherr Appliances

5.2. Cross Comparison Parameters (Revenue, Market Share, Number of Employees, Market Penetration, Product Portfolio, Innovation Index, Technology Integration, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (New Product Launches, Market Expansion, Mergers & Acquisitions, Joint Ventures)

5.5. Investment Analysis (CapEx Investments, R&D Spending)

5.6. Venture Capital Funding

5.7. Private Equity Investments

6. Asia Pacific Refrigerator Market Regulatory Framework

6.1. Energy Consumption Regulations

6.2. Certification Processes (ISO Standards, Energy Star Compliance)

6.3. Import and Export Regulations

7. Asia Pacific Refrigerator Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Refrigerator Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By End User (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Refrigerator Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Entry Strategies

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves the identification of key variables affecting the Asia Pacific refrigerator market. This includes the analysis of factors such as technological advancements, energy efficiency standards, and consumer preferences. Extensive secondary research was conducted using a combination of proprietary databases and government sources.

Step 2: Market Analysis and Construction

The next phase entails a detailed analysis of the market, including the collection of historical data, examining the market penetration of major brands, and evaluating revenue generation from different segments. This stage ensures a comprehensive understanding of market dynamics and growth potential.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed and validated through expert consultations, primarily via interviews with key stakeholders such as manufacturers, distributors, and industry experts. These consultations provided valuable insights, helping refine the market projections.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing the data gathered to produce a detailed report that presents a complete picture of the market. This includes the validation of market size, competitive landscape, and future outlook, ensuring accurate and actionable insights for stakeholders.

Frequently Asked Questions

1. How big is the Asia Pacific Refrigerator Market?

The Asia Pacific refrigerator market is valued at USD 31 billion, driven by rising demand for energy-efficient and smart refrigerators across both developed and developing nations.

2. What are the major challenges in the Asia Pacific Refrigerator Market?

Key challenges include high manufacturing costs due to the volatility in raw material prices and compliance with stringent energy efficiency regulations. Supply chain disruptions also pose a challenge, affecting the availability of components.

3. Who are the major players in the Asia Pacific Refrigerator Market?

The major players in the market include LG Electronics, Samsung Electronics, Haier Group Corporation, Whirlpool Corporation, and Panasonic Corporation. These companies lead the market due to their strong innovation capabilities and extensive distribution networks.

4. What are the growth drivers of the Asia Pacific Refrigerator Market?

The market is driven by factors such as increasing disposable incomes, the proliferation of smart home devices, and rising awareness about energy efficiency. Government initiatives promoting energy conservation also contribute to market growth.

5. What are the key trends in the Asia Pacific Refrigerator Market?

Key trends include the growing adoption of smart refrigerators, the integration of AI and IoT technologies, and the demand for environmentally sustainable refrigeration solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.