Asia-Pacific Solar PV Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD3241

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD3241

November 2024

90

The Asia-Pacific Solar PV Market is segmented by technology, application type, end-user industry, product type, and geographical region.

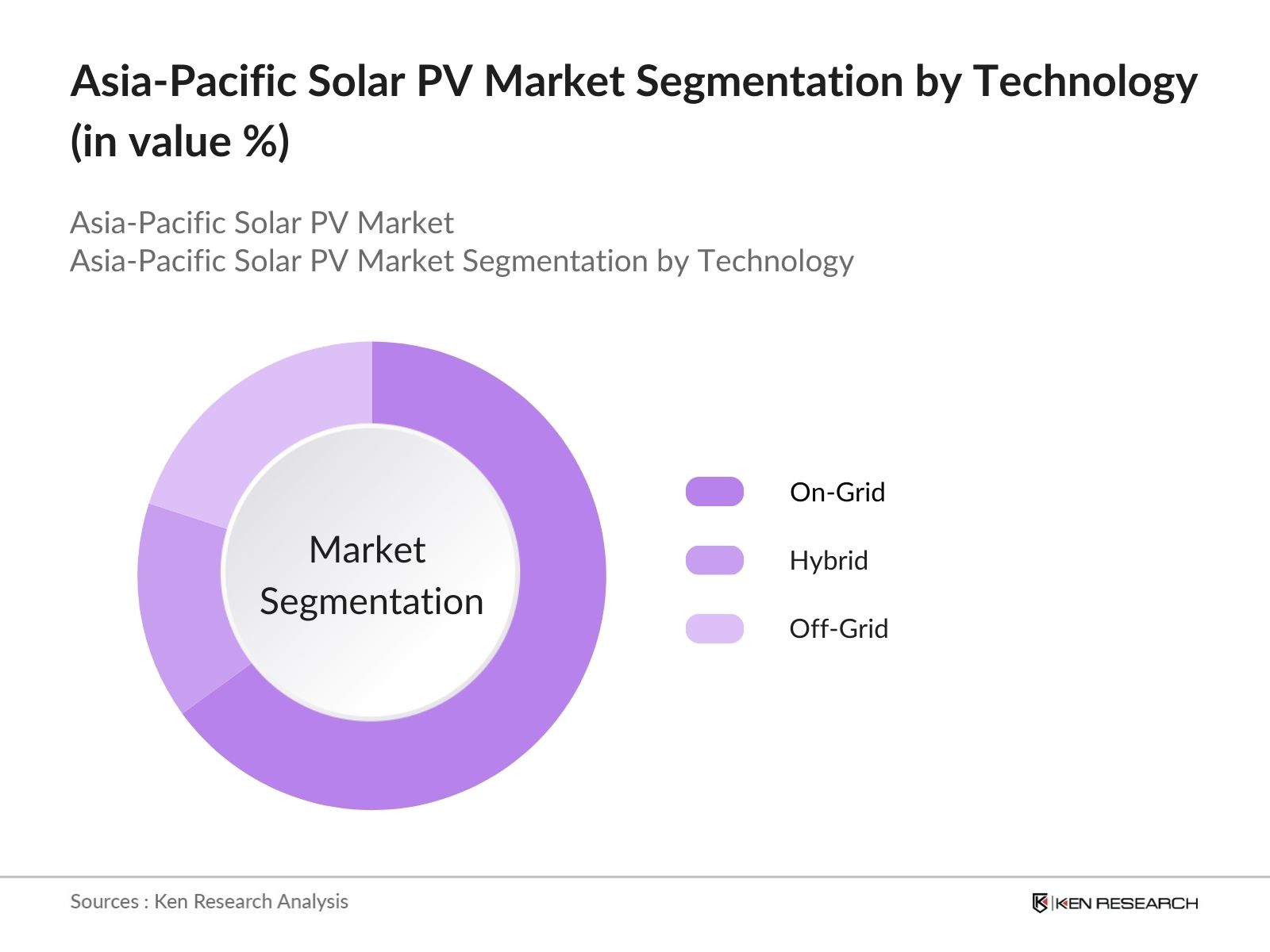

By Technology: The Asia-Pacific Solar PV market is segmented by technology into On-Grid, Off-Grid, and Hybrid systems. On-grid solar PV systems dominate the market due to their compatibility with the region's energy grids, reduced installation costs, and favorable government policies encouraging grid-connected solar energy. The strong demand from utility-scale projects further cements this segments dominance, particularly in countries like China and India where large solar farms are being integrated with national grids.

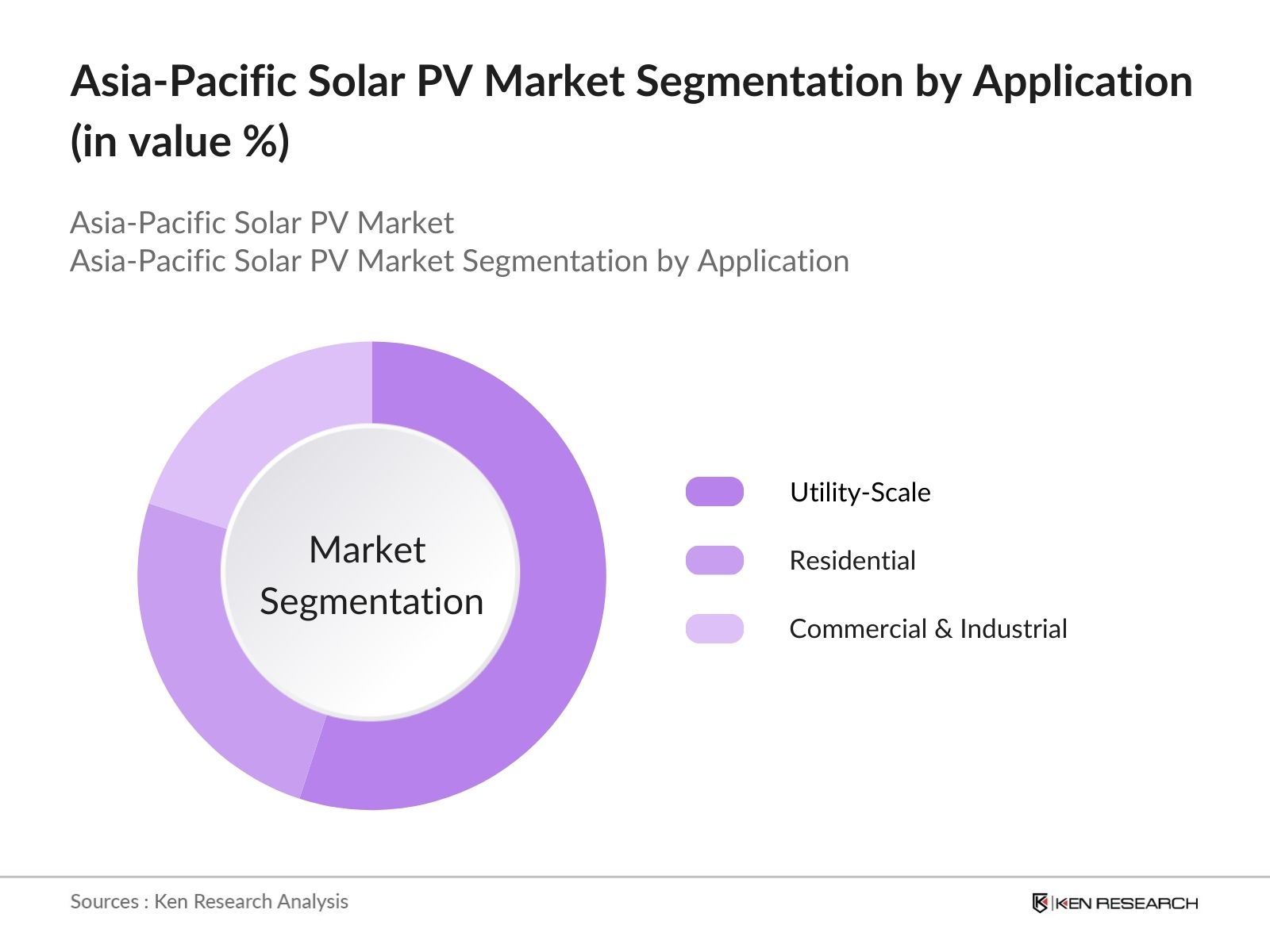

By Application: The market is also segmented by application into Utility-Scale, Residential, and Commercial & Industrial (C&I) sectors. Utility-scale solar PV systems hold a dominant share due to their large-scale installations across various countries, driven by government mandates and favorable tariffs. The C&I sector is also gaining momentum as more corporations aim to meet sustainability goals through renewable energy adoption. Countries such as Australia and Japan see C&I adoption due to increasing energy costs and policies promoting self-sufficiency.

The Asia-Pacific Solar PV market is dominated by several key players, including both global and local manufacturers. Companies such as JinkoSolar and LONGi have established a strong presence in the region through strong distribution networks, technological innovation, and competitive pricing. Additionally, local players like Adani Solar and Tata Power Solar Systems benefit from strong government support and localized market expertise, making the market highly competitive. International players like First Solar continue to maintain a foothold through technological innovations, particularly in module efficiency.

|

Company |

Established |

Headquarters |

Capacity Installed (MW) |

Revenue (USD Bn) |

Module Efficiency (%) |

Production Capacity |

Global Installations |

R&D Spending (USD Mn) |

|

JinkoSolar |

2006 |

China |

- |

- |

- |

- |

- |

- |

|

Trina Solar |

1997 |

China |

- |

- |

- |

- |

- |

- |

|

First Solar |

1999 |

USA |

- |

- |

- |

- |

- |

- |

|

LONGi |

2000 |

China |

- |

- |

- |

- |

- |

- |

|

Adani Solar |

2015 |

India |

- |

- |

- |

- |

- |

- |

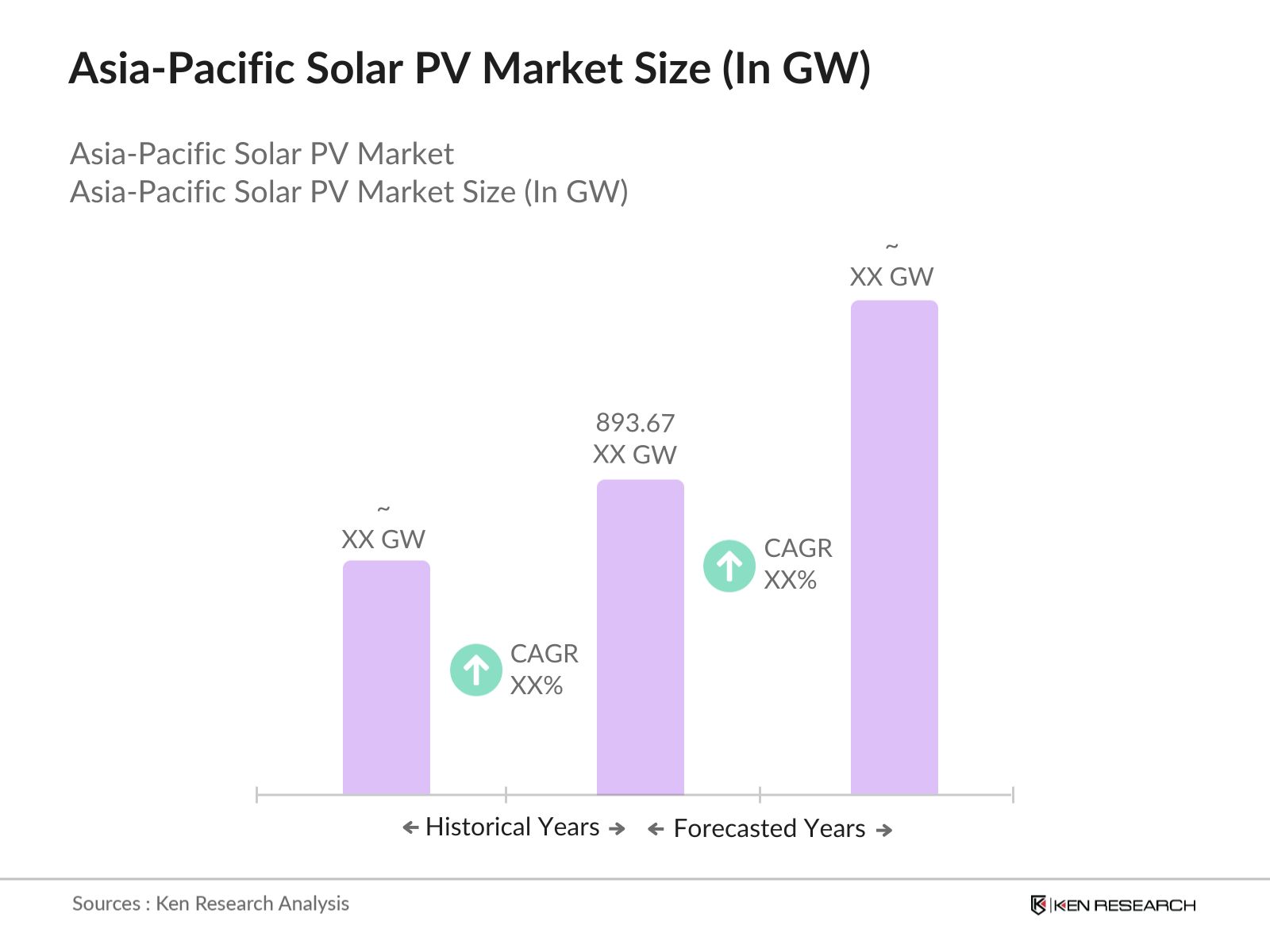

Over the next five years, the Asia-Pacific Solar PV market is expected to experience robust growth, driven by increasing investments in renewable energy, technological advancements in solar PV modules, and supportive government policies aimed at reducing carbon emissions. Countries like China and India are expected to continue leading the market in terms of installed capacity, while emerging markets in Southeast Asia and the Pacific Islands are likely to see substantial growth as they ramp up renewable energy efforts.

|

By Type |

Crystalline Silicon (Monocrystalline, Polycrystalline) Thin Film (Cadmium Telluride, Amorphous Silicon, Copper Indium Gallium Selenide) |

|

By Application |

Utility Scale (Solar Farms, Floating Solar) Residential (Rooftop Installations, Microgrids) Commercial & Industrial (Industrial Rooftop, Corporate PPAs) |

|

By Technology |

On-Grid Off-Grid Hybrid |

|

By End-User |

Industrial Users (Manufacturing, Large Enterprises) Residential Users (Households, Housing Societies) Commercial Users (Office Complexes, Malls) |

|

By Region |

China South Korea Japan India Australia Rest of APAC |

1.1. Definition and Scope

1.2. Market Taxonomy (Solar PV Systems, Photovoltaic Modules, Inverters, Balance of Systems)

1.3. Market Growth Rate (CAGR, Capacity Addition, Revenue Growth)

1.4. Market Segmentation Overview (By Type, Application, Technology, End-User, and Region)

2.1. Historical Market Size (Capacity Installed, Revenue, Number of Projects)

2.2. Year-On-Year Growth Analysis (Capacity and Revenue)

2.3. Key Market Developments and Milestones (Policy Milestones, Installed Base, Largest Projects)

3.1. Growth Drivers

3.1.1. Government Incentives (FIT, PPA Tariffs, Green Energy Certificates)

3.1.2. Declining Solar PV Costs (Silicon Wafer Pricing, Module Efficiency Gains)

3.1.3. Energy Transition Policies (Decarbonization Targets, Renewable Energy Mix Goals)

3.1.4. International Investment and Funding (FDI, Private Sector Funding, Green Bonds)

3.2. Market Challenges

3.2.1. Grid Infrastructure Issues (Grid Integration, Energy Storage Requirements)

3.2.2. Regulatory Hurdles (Permitting, Land Acquisition Challenges)

3.2.3. Supply Chain Disruptions (Polysilicon Shortages, Shipping Delays)

3.3. Opportunities

3.3.1. Emerging Markets (Southeast Asia, Pacific Islands)

3.3.2. Floating Solar Farms (Reservoirs, Off-Shore Potential)

3.3.3. Smart Grid Integration (Energy Storage, IoT)

3.4. Trends

3.4.1. Adoption of Bifacial PV Modules

3.4.2. Integration with Energy Storage Systems (ESS)

3.4.3. Corporate Renewable Power Purchase Agreements (PPAs)

3.5. Government Regulation

3.5.1. National Renewable Energy Targets

3.5.2. Solar Parks and SEZ (Special Economic Zones for Solar Manufacturing)

3.5.3. Tariff and Duty Policies (Import Duties, Subsidies)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Developers, Installers, Equipment Manufacturers)

3.8. Porters Five Forces (Competition, Bargaining Power, Threat of Substitutes)

3.9. Competitive Ecosystem (IPPs, EPC Contractors, Manufacturers)

4.1. By Type (In Value % & Capacity Installed)

4.1.1. Crystalline Silicon (Monocrystalline, Polycrystalline)

4.1.2. Thin Film (Cadmium Telluride, Amorphous Silicon, Copper Indium Gallium Selenide)

4.2. By Application (In Value % & Capacity Installed)

4.2.1. Utility Scale (Solar Farms, Floating Solar)

4.2.2. Residential (Rooftop Installations, Microgrids)

4.2.3. Commercial & Industrial (Industrial Rooftop, Corporate PPAs)

4.3. By Technology (In Value % & Capacity Installed)

4.3.1. On-Grid

4.3.2. Off-Grid

4.3.3. Hybrid

4.4. By End-User (In Value % & Capacity Installed)

4.4.1. Industrial Users (Manufacturing, Large Enterprises)

4.4.2. Residential Users (Households, Housing Societies)

4.4.3. Commercial Users (Office Complexes, Malls)

4.5. By Region (In Value % & Capacity Installed)

4.5.1. China

4.5.2. South Korea

4.5.3. Japan

4.5.4. India

4.5.5. Australia

4.5.6. Rest of APAC

5.1 Detailed Profiles of Major Companies

5.1.1. JinkoSolar Holding Co., Ltd.

5.1.2. Trina Solar Limited

5.1.3. LONGi Green Energy Technology Co., Ltd.

5.1.4. First Solar, Inc.

5.1.5. Canadian Solar Inc.

5.1.6. JA Solar Technology Co., Ltd.

5.1.7. SunPower Corporation

5.1.8. Hanwha Q Cells Co., Ltd.

5.1.9. Risen Energy Co., Ltd.

5.1.10. Tata Power Solar Systems Ltd.

5.1.11. Adani Solar

5.1.12. GCL-Poly Energy Holdings Limited

5.1.13. Waaree Energies Ltd.

5.1.14. REC Solar Holdings AS

5.1.15. Shunfeng International Clean Energy Ltd.

5.2 Cross Comparison Parameters (Capacity Installed, Revenue, Market Presence, Market Share, R&D Spending, Module Efficiency, Production Capacity, Global Installations)

5.3. Market Share Analysis (Key Players Share in the Total Installed Capacity)

5.4. Strategic Initiatives (Partnerships, Alliances, R&D Investments)

5.5. Mergers and Acquisitions (Recent Deals, Valuation)

5.6. Investment Analysis (Private Equity, Green Bonds, Project Financing)

5.7. Venture Capital Funding (Startups, Innovation)

5.8. Government Grants (Subsidies, Support Programs)

5.9. Private Equity Investments (Key Players and Funded Projects)

6.1. Environmental Standards (Emissions Regulations, Certifications)

6.2. Compliance Requirements (Permitting, Zoning Regulations)

6.3. Certification Processes (Module Standards, Inverter Certifications)

7.1. Future Market Size Projections (Capacity and Revenue)

7.2. Key Factors Driving Future Market Growth (Policies, Technological Innovations)

8.1. By Type (In Value % & Capacity Installed)

8.2. By Application (In Value % & Capacity Installed)

8.3. By Technology (In Value % & Capacity Installed)

8.4. By End-User (In Value % & Capacity Installed)

8.5. By Region (In Value % & Capacity Installed)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Residential, Commercial, Industrial)

9.3. Marketing Initiatives (Policy Advocacy, Brand Positioning)

9.4. White Space Opportunity Analysis (Geographical Expansion, Untapped Markets)

Disclaimer Contact UsWe begin by constructing an in-depth ecosystem map, including major stakeholders in the Asia-Pacific Solar PV market. This step involves extensive desk research, utilizing proprietary databases and secondary sources to gather detailed industry information. The goal is to pinpoint the key variables affecting market trends and developments.

In this phase, we compile and assess historical data on market penetration, revenue generation, and technology adoption rates in the Solar PV sector. Additionally, we evaluate the market's competitive structure and service provider landscape to generate reliable and precise revenue estimates.

Market hypotheses are developed and validated through expert consultations via computer-assisted telephone interviews (CATIs) with industry specialists. These interactions provide insights into market dynamics, trends, and operational challenges, enriching the quantitative data with qualitative input.

The final stage involves synthesizing all data and insights into a comprehensive market report. This step includes direct engagements with manufacturers and key industry players to verify and corroborate data, ensuring the report is both accurate and reflective of the markets current and future state.

The Asia-Pacific Solar PV market boasts a cumulative installed capacity of 893.67GW, driven by rapid adoption of renewable energy and government incentives for solar power infrastructure.

The Asia-Pacific Solar PV market's key drivers include increasing demand for clean energy, government subsidies, declining costs of solar PV modules, and strong investments in renewable energy infrastructure.

China, India, and Japan are the leading countries in this Asia-Pacific Solar PV market due to their extensive solar installations, government support, and investments in renewable energy projects.

The Asia-Pacific Solar PV market challenges include grid integration issues, regulatory hurdles, supply chain disruptions, and the high initial cost of solar energy infrastructure in some developing countries.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.