Asia Pacific Space Technology Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD11253

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD11253

December 2024

82

By Component Type: The market is segmented by component type into launch vehicles, satellites, spacecraft, ground equipment, and space robotics. Recently, satellites hold a dominant market share within this segmentation due to their multipurpose application in communications, weather forecasting, and environmental monitoring. Countries like China and India have established strong satellite manufacturing bases, facilitating cost-efficient production. Additionally, advancements in miniaturized satellite technology further fuel the growth of this segment, as smaller and more affordable satellites attract both government and commercial customers.

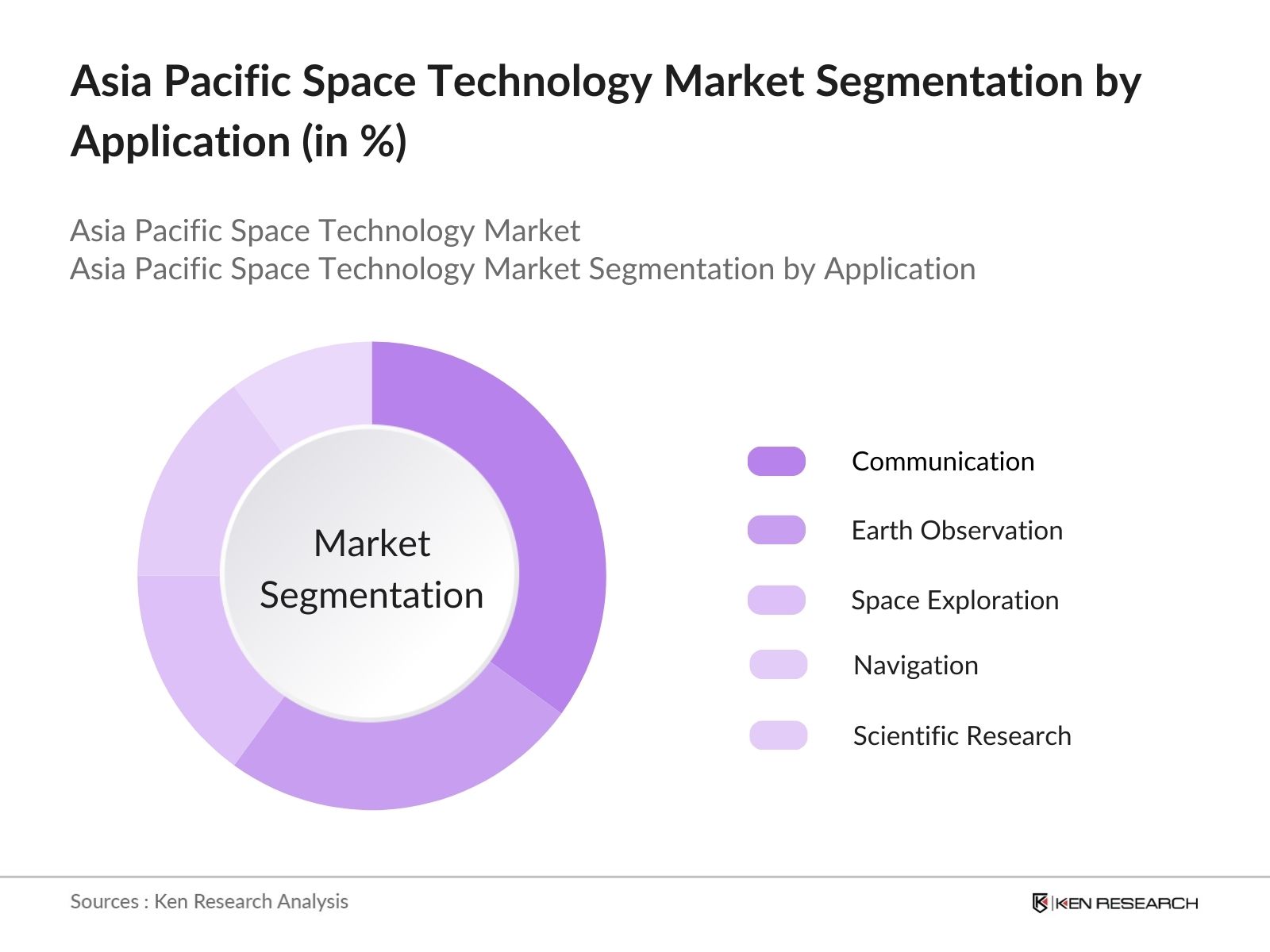

By Application: The market is also segmented by application, covering communication, Earth observation, space exploration, navigation and positioning, and scientific research. Within this category, communication applications lead the market, driven by the rising need for reliable and high-speed connectivity across the region. The demand for internet services, particularly in rural areas, drives the growth of communication satellites, which play a crucial role in bridging the connectivity gap. Consequently, major space programs in the region focus on increasing their satellite launches dedicated to communication purposes.

The market is primarily controlled by a select group of prominent players, with government-backed agencies and private companies leading development in space exploration, satellite deployment, and space services.

Over the next five years, the Asia Pacific Space Technology industy is expected to see considerable growth, spurred by a mix of government support, technological advancements, and rising commercial interest.

|

Component Type |

Launch Vehicles |

|

Application |

Communication |

|

End-User |

Government and Defense |

|

Technology |

Satellite-Based AI |

|

Region |

China |

1.1 Definition and Scope

1.2 Market Taxonomy (Satellite Types, Launch Systems, Applications)

1.3 Market Growth Rate Analysis (CAGR and Volume Metrics)

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Developments and Innovations

3.1 Growth Drivers

3.1.1 Increasing Government Investments in Space Programs

3.1.2 Expanding Commercial Satellite Applications

3.1.3 Growing Demand for Space-Based Data Services

3.2 Market Challenges

3.2.1 High Capital Investment Requirements

3.2.2 Regulatory and Policy Barriers

3.2.3 Technological Constraints in Emerging Markets

3.3 Opportunities

3.3.1 Advancements in Miniaturized Satellite Technologies

3.3.2 Expansion of Space Tourism Ventures

3.3.3 Collaborations Between Private Players and Governments

3.4 Trends

3.4.1 Growth in Reusable Rocket Technologies

3.4.2 Adoption of AI and Big Data in Space Missions

3.4.3 Focus on Sustainable Space Exploration

3.5 Regulatory Landscape

3.5.1 Space Debris Mitigation Policies

3.5.2 Regional Compliance for Space Exploration Activities

3.5.3 Export and Import Policies for Space Technologies

3.6 SWOT Analysis

3.7 Value Chain Analysis (Raw Materials, Manufacturing, Launch Services, Data Distribution)

3.8 Porters Five Forces Model

3.9 Competitive Ecosystem

4.1 By Application (In Volume %)

4.1.1 Communication

4.1.2 Earth Observation

4.1.3 Navigation

4.1.4 Space Exploration

4.1.5 Space Tourism

4.2 By Technology Type (In Volume %)

4.2.1 Satellite Technologies

4.2.2 Rocket and Launch Technologies

4.2.3 Ground Infrastructure

4.2.4 Space Robotics

4.3 By End-User (In Volume %)

4.3.1 Government and Defense

4.3.2 Commercial Enterprises

4.3.3 Research Institutions

4.4 By Component Type (In Volume%)

4.4.1 Launch Vehicles

4.4.2 Satellites

4.4.3 Spacecraft

4.4.4 Ground Equipment

4.4.5 Space Robotics

4.5 By Region (In Volume %)

4.5.1 East Asia

4.5.2 Southeast Asia

4.5.3 South Asia

4.5.4 Oceania

4.5.5 Central Asia

5.1 Profiles of Major Companies

5.1.1 SpaceX

5.1.2 Blue Origin

5.1.3 Indian Space Research Organisation (ISRO)

5.1.4 Mitsubishi Electric Corporation

5.1.5 Japan Aerospace Exploration Agency (JAXA)

5.1.6 Lockheed Martin Corporation

5.1.7 Airbus SE

5.1.8 China National Space Administration (CNSA)

5.1.9 Thales Alenia Space

5.1.10 Northrop Grumman Corporation

5.2 Cross Comparison Parameters (R&D Investments, Mission Success Rate, Partnerships, Sustainability Initiatives, Geographic Presence)

5.3 Market Share Analysis

5.4 Key Strategic Initiatives

5.5 Mergers, Acquisitions, and Joint Ventures

5.6 Investment Analysis

5.7 Private Equity and Venture Capital Funding

6.1 Regional Space Policy Frameworks

6.2 Compliance Standards for Space Missions

6.3 Certification Processes for Space Technology Development

7.1 Market Size Forecasts

7.2 Key Growth Catalysts and Projections

8.1 By Application

8.2 By Technology Type

8.3 By End-User

8.4 By Component Type

8.5 By Region

9.1 Total Addressable Market (TAM)/Serviceable Available Market (SAM)/Serviceable Obtainable Market (SOM) Analysis

9.2 Consumer Behavior Analysis

9.3 Marketing Strategies and Recommendations

9.4 Emerging White Space Opportunities

The initial phase involved identifying core stakeholders and their roles in the Asia Pacific Space Technology Market. Secondary data sources such as industry reports and government publications were analyzed to outline the primary factors impacting the market.

Historical market data was compiled to assess current market conditions and trends, focusing on satellite deployment, component manufacturing, and revenue generation. This analysis provided insight into the demand and supply dynamics within the market.

Key industry hypotheses were formulated and validated through expert consultations. Insights from senior industry professionals across government agencies and private space firms were gathered to refine market projections.

The final report was synthesized by corroborating quantitative and qualitative data, ensuring an accurate and comprehensive overview. The resulting analysis was verified through engagements with satellite manufacturers and space technology providers.

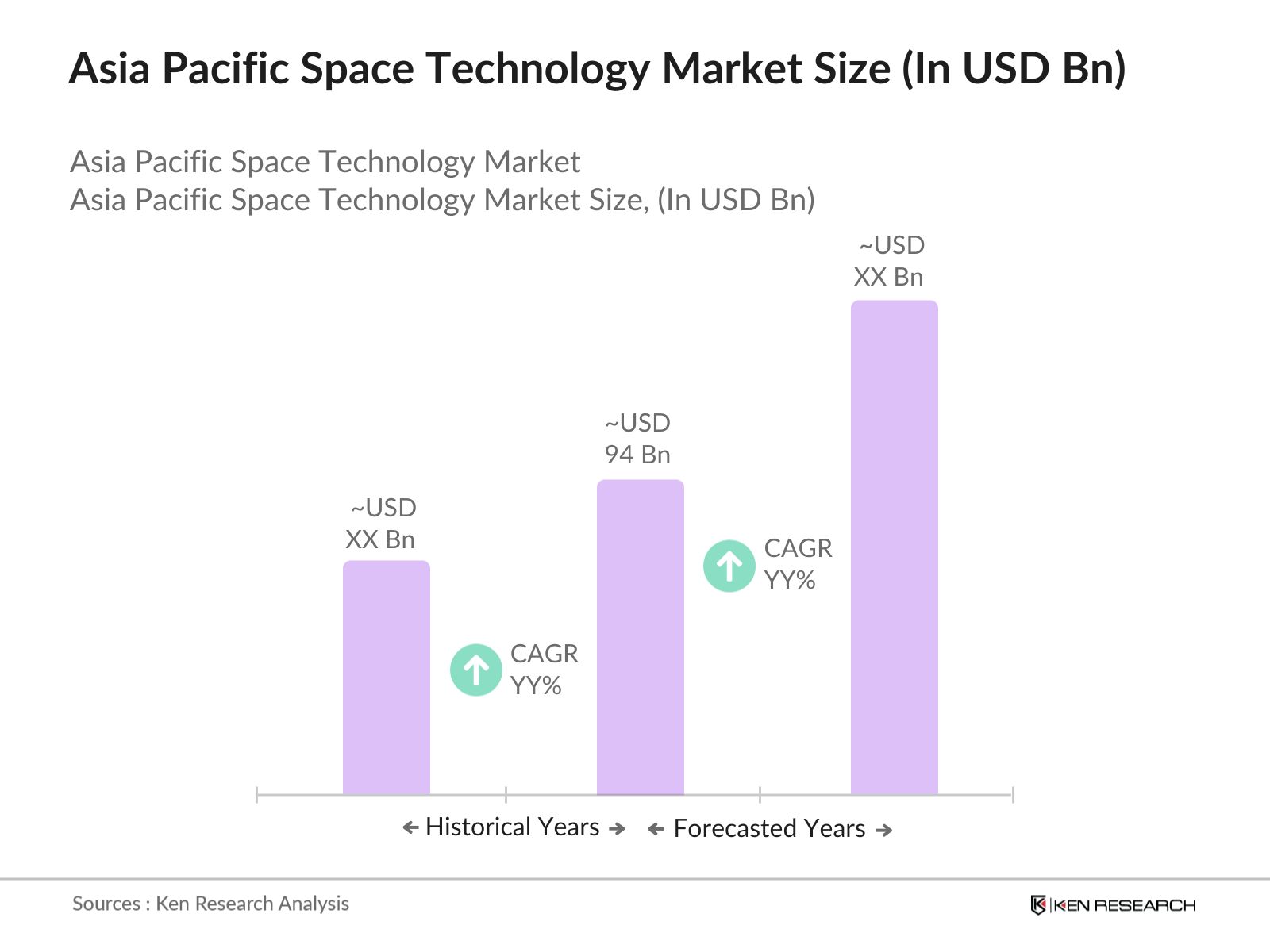

The Asia Pacific Space Technology Market, valued at USD 94 billion, is growing due to increased investments in satellite technology and demand for space exploration.

Challenges in the Asia Pacific Space Technology Market include high capital requirements, regulatory complexities, and the limited availability of a skilled workforce in specialized space technology fields.

Key players in the Asia Pacific Space Technology Market include CNSA, ISRO, Mitsubishi Heavy Industries, Rocket Lab, and Astroscale, which dominate due to their robust infrastructure, technological capabilities, and government support.

Growth drivers in the Asia Pacific Space Technology Market encompass increasing government investments, technological advancements, and rising demand for satellite-based applications across telecommunications and navigation sectors.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.