Asia Pacific SSD Caching Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD8993

November 2024

100

About the Report

Asia Pacific SSD Caching Market Overview

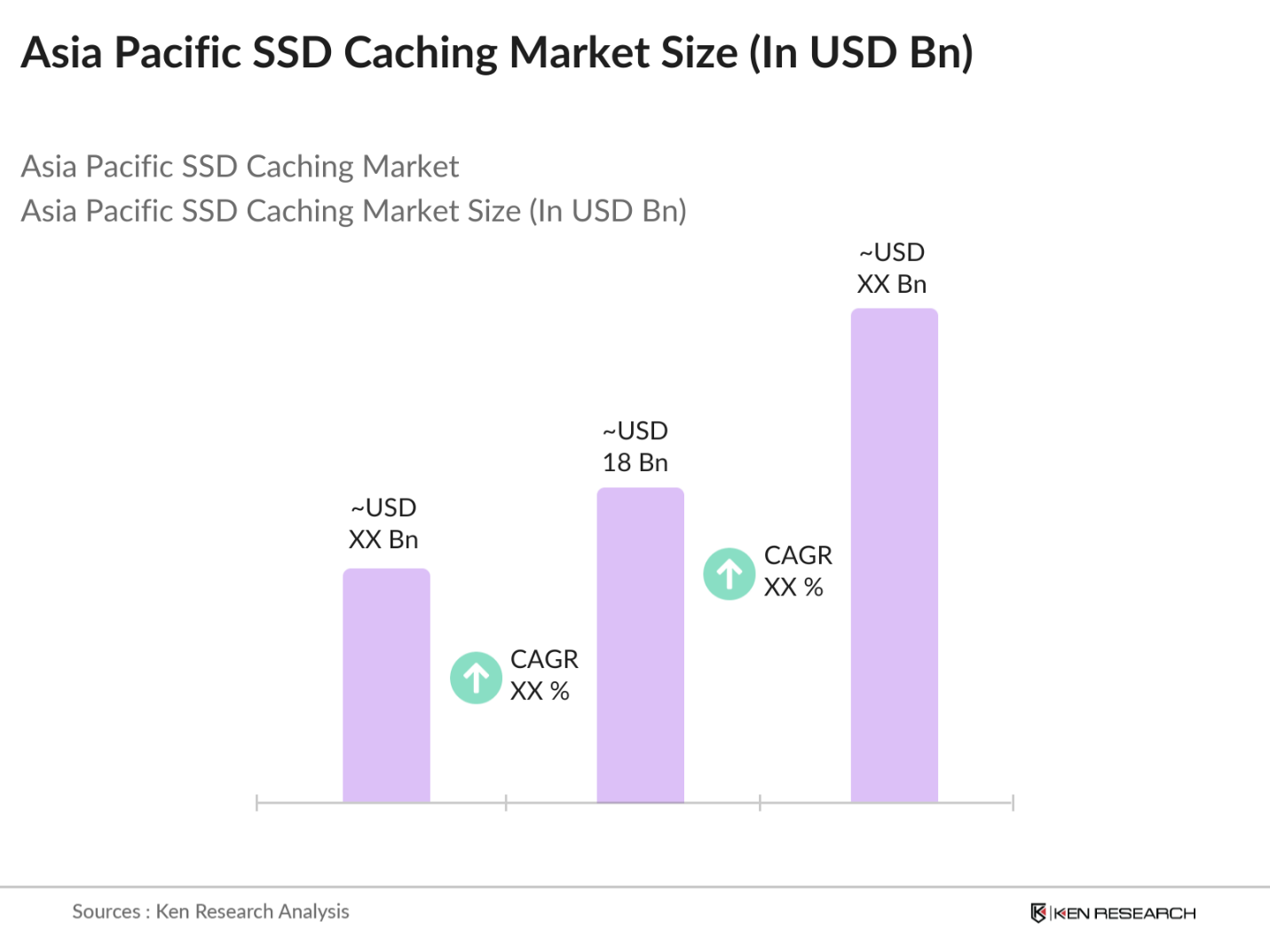

- The Asia Pacific SSD Caching Market is valued at USD 18 billion, based on a five-year historical analysis. This market is primarily driven by the increasing demand for high-speed data processing in sectors like IT, telecommunications, and finance, where the need for low-latency and efficient data access has become critical. The expanding adoption of cloud computing, edge computing, and IoT solutions further strengthens this demand, making SSD caching a preferred choice for high-performance data storage and accelerated application processing across the region.

- The market is primarily led by countries such as China, Japan, and South Korea, thanks to their advanced technological infrastructure, high data center density, and established IT sectors. China dominates due to its robust manufacturing capabilities and extensive digital transformation initiatives, while Japan and South Korea leverage their technological advancements and substantial investments in high-performance data storage solutions.

- Countries like Australia and India have instituted compliance regulations for data storage, mandating strict protocols for data handling and storage. These regulations influence SSD caching deployment, as companies must ensure their storage solutions meet legal requirements for data safety and accessibility.

Asia Pacific SSD Caching Market Segmentation

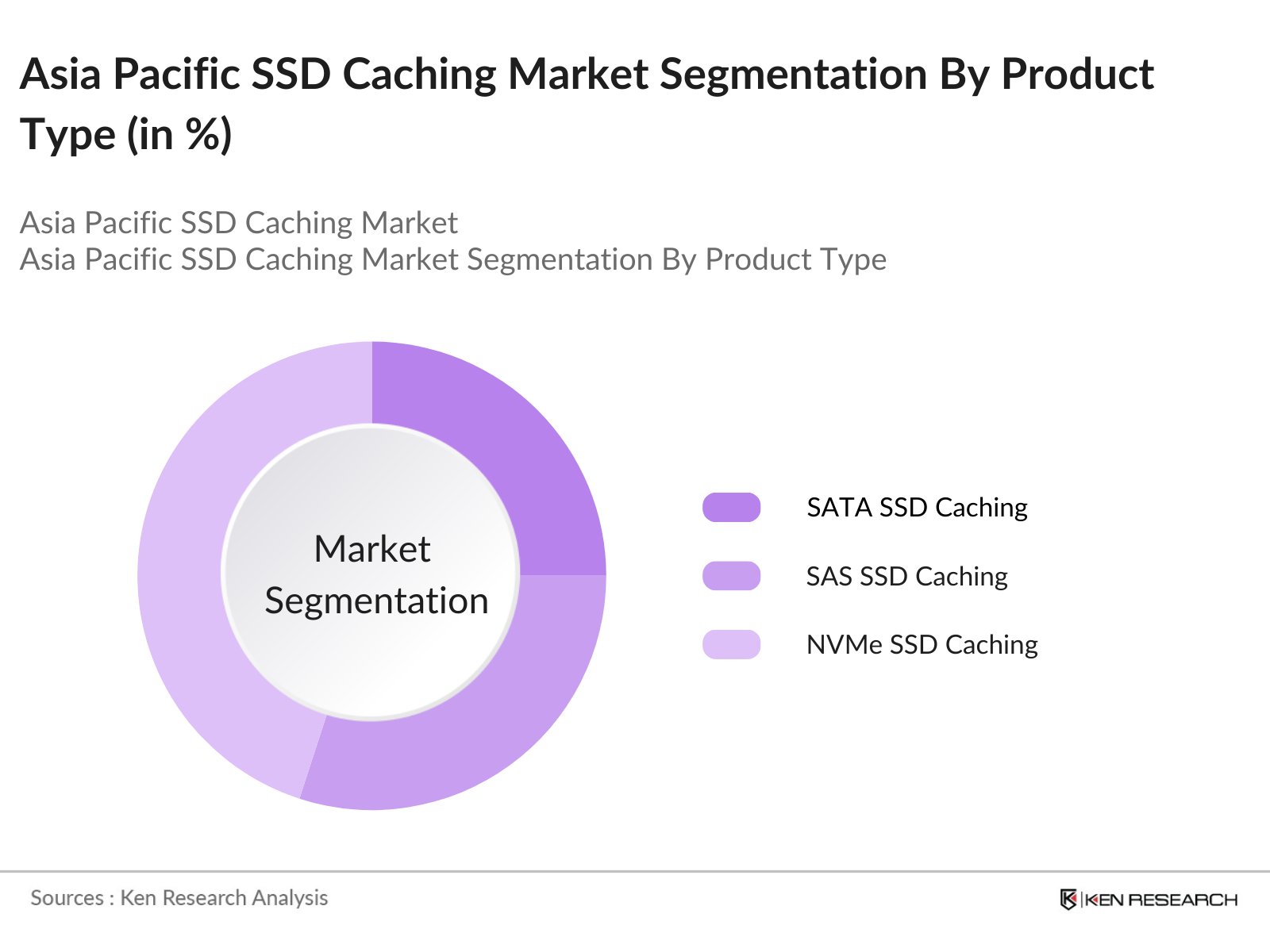

By Product Type: The market is segmented by product type into SATA SSD Caching, SAS SSD Caching, and NVMe SSD Caching. Recently, NVMe SSD Caching has secured a dominant market share within this segment due to its enhanced data transfer speeds and low latency, which cater to demanding applications in data centers and enterprise computing.

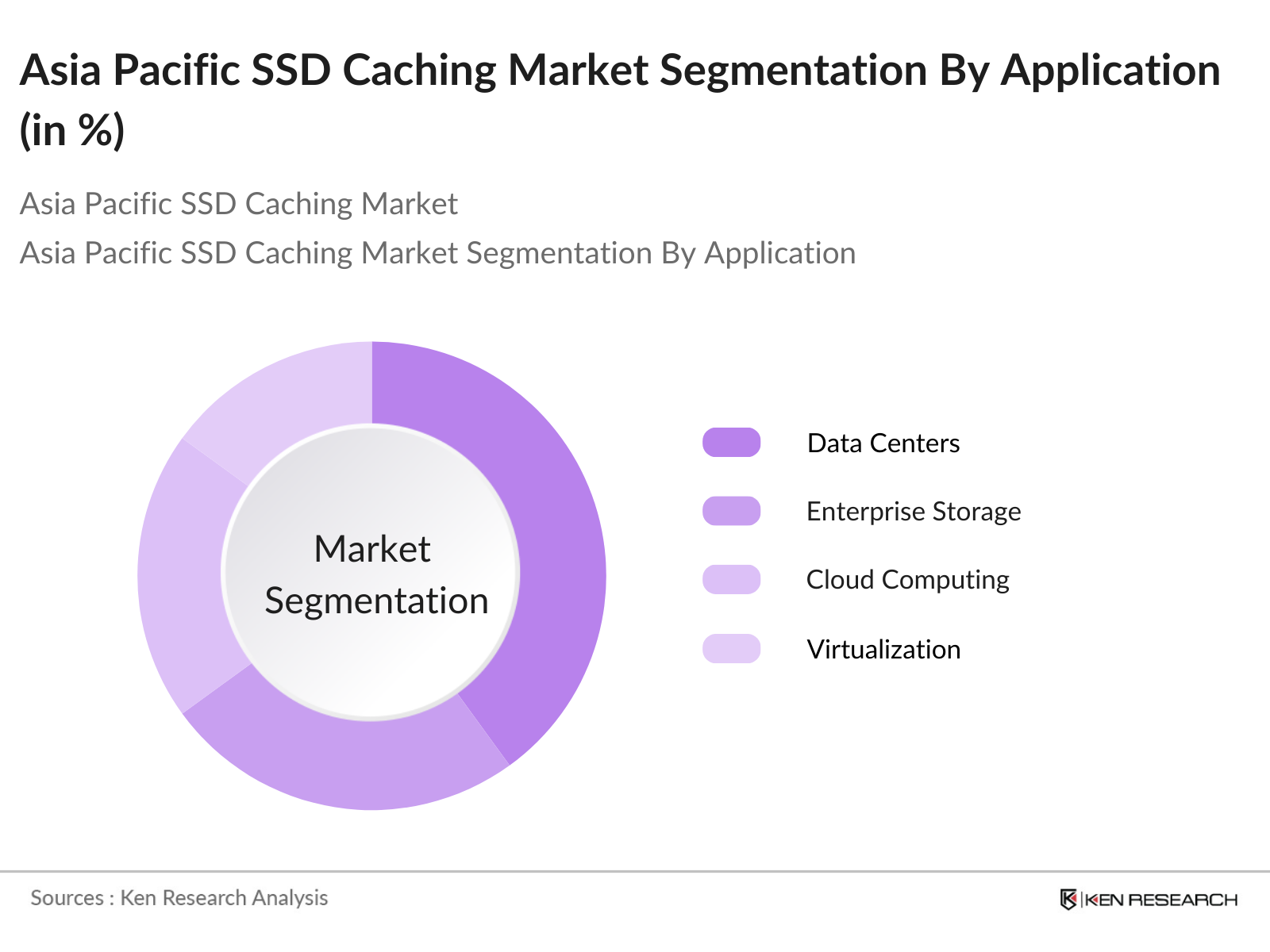

By Application: The Asia Pacific SSD Caching Market is also segmented by application into Data Centers, Enterprise Storage, Cloud Computing, and Virtualization. Data Centers represent the largest share within this category, as the region experiences rapid data center expansion to accommodate rising data volumes and demand for high-speed, reliable data access.

Asia Pacific SSD Caching Market Competitive Landscape

The Asia Pacific SSD Caching Market is characterized by a competitive landscape dominated by established players, including global giants and regional manufacturers. This consolidation allows the market to benefit from extensive R&D efforts, ensuring the rapid deployment of high-speed storage solutions across sectors.

Asia Pacific SSD Caching Industry Analysis

Growth Drivers

- Increasing Demand for Data Storage Solutions: The Asia Pacific regions rapid data consumption surge, reaching over 20 billion gigabytes in total data generated annually, has driven the demand for enhanced storage solutions. Enterprises across sectors, including finance, retail, and telecommunications, require advanced storage due to exponential data growth from digital transactions, user data, and system logs. Countries like India and China are seeing significant increases in data traffic, with data consumption projected to continue to rise sharply in 2024, supported by government digitalization initiatives.

- Rising Adoption of Cloud-Based Solutions: Cloud migration in the Asia Pacific region has accelerated, with government and private sector data centers expanding in countries like Singapore and Japan. As of 2024, the region hosts over 50,000 data centers. The adoption of SSD caching aids in managing the heavy data requirements posed by cloud storage. Enterprises adopting SSD caching can achieve up to 3x faster data retrieval speeds, essential for real-time processing needs.

- Enhanced Computing Needs: With Asia Pacifics edge computing market reaching a deployment of 5 million edge servers, theres an increasing integration of AI and IoT. The regions industries, from manufacturing to healthcare, rely on SSD caching for real-time processing and fast data access. This trend is supported by national AI strategies in countries like South Korea and Singapore, which require high-performance storage solutions.

Market Challenges

- Technical Integration Issues: Integrating SSD caching with legacy systems poses a challenge, with 60% of existing infrastructures in Asia Pacific reported to be incompatible with advanced SSD systems. Upgrading systems requires considerable resources and expertise, delaying SSD adoption in traditional sectors like manufacturing. This challenge impacts both cost and operational efficiency, as companies must overhaul existing systems.

- Data Privacy and Security Concerns: Data privacy is increasingly critical, with new regulations in Asia Pacific enforcing stringent compliance. For example, Chinas Personal Information Protection Law (PIPL) mandates high standards for data processing, adding layers of compliance that enterprises must navigate. Security breaches are costly, with the average data breach costing approximately $2 million for affected companies in the region.

Asia Pacific SSD Caching Market Future Outlook

Over the next five years, the Asia Pacific SSD Caching Market is projected to experience robust growth, driven by continuous advancements in SSD technologies, increased adoption of high-speed storage in AI and big data analytics, and growing investments in data center infrastructure. This growth is expected to be further bolstered by government initiatives supporting digitalization, alongside an expanding base of tech-savvy consumers and enterprises prioritizing high-efficiency data processing.

Market Opportunities

- Technological Innovation in Caching Algorithms: Innovations in caching algorithms are reshaping the SSD caching landscape, enhancing efficiency by over 20% in data retrieval processes. Advanced algorithms reduce latency, optimize cache memory, and are increasingly being adopted by enterprises for superior data handling. For instance, Japans technology sector is seeing substantial R&D investments aimed at developing next-gen caching technologies.

- Partnerships with Cloud Service Providers: Collaborations with cloud service providers present lucrative opportunities for SSD caching technology providers. In 2024, the Asia Pacific region reported 200+ partnerships between tech firms and cloud giants, aimed at leveraging storage optimization. Such alliances enable localized data processing and storage solutions that meet the unique needs of regional enterprises.

Scope of the Report

|

Product Type |

SATA SSD Caching SAS SSD Caching NVMe SSD Caching |

|

Application |

Data Centers Enterprise Storage Cloud Computing Virtualization |

|

End-User Industry |

IT & Telecom BFSI Government Healthcare Retail |

|

Deployment Mode |

On-Premises Cloud-Based |

|

Region |

China Japan South Korea Southeast Asia Australia and New Zealand |

Products

Key Target Audience

Data Center Infrastructure Providers

Cloud Service Providers

Government and Regulatory Bodies (e.g., Ministry of Industry and Information Technology - China, Telecommunications Regulatory Authority - Japan)

Storage Hardware Manufacturers

Enterprise IT Solutions Providers

Investments and Venture Capital Firms

Tech-Enabled Healthcare Organizations

High-Tech Manufacturing Companies

Companies

Players Mentioned in the Report

Samsung Electronics Co., Ltd.

Western Digital Corporation

Intel Corporation

Micron Technology, Inc.

Toshiba Memory Corporation

ADATA Technology Co., Ltd.

Seagate Technology Holdings PLC

Kioxia Holdings Corporation

Kingston Technology Corporation

Huawei Technologies Co., Ltd.

Table of Contents

1. Asia Pacific SSD Caching Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Segmentation Overview

2. Asia Pacific SSD Caching Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Technological Advancements

3. Asia Pacific SSD Caching Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for Data Storage Solutions (Data Consumption, Enterprise Demand)

3.1.2. Rising Adoption of Cloud-Based Solutions (Cloud Migration, Data Center Needs)

3.1.3. Enhanced Computing Needs (Edge Computing, AI, IoT Integrations)

3.1.4. Cost Reduction in Flash Storage Technology

3.2. Market Challenges

3.2.1. High Initial Capital Investment

3.2.2. Technical Integration Issues

3.2.3. Data Privacy and Security Concerns

3.3. Opportunities

3.3.1. Technological Innovation in Caching Algorithms

3.3.2. Partnerships with Cloud Service Providers

3.3.3. Expansion of Enterprise Storage Solutions

3.4. Trends

3.4.1. Growth of Hybrid Storage Solutions

3.4.2. Adoption of NVMe and PCIe SSDs

3.4.3. Increased Demand for High-Performance Storage

3.5. Regulatory Landscape

3.5.1. Data Storage Compliance Regulations

3.5.2. Environmental and Disposal Standards

3.5.3. Standards for Energy-Efficient Storage Solutions

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. Asia Pacific SSD Caching Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. SATA SSD Caching

4.1.2. SAS SSD Caching

4.1.3. NVMe SSD Caching

4.2. By Application (In Value %)

4.2.1. Data Centers

4.2.2. Enterprise Storage

4.2.3. Cloud Computing

4.2.4. Virtualization

4.3. By End-User Industry (In Value %)

4.3.1. IT & Telecom

4.3.2. BFSI

4.3.3. Government

4.3.4. Healthcare

4.3.5. Retail

4.4. By Deployment Mode (In Value %)

4.4.1. On-Premises

4.4.2. Cloud-Based

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Southeast Asia

4.5.5. Australia and New Zealand

5. Asia Pacific SSD Caching Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Samsung Electronics Co., Ltd.

5.1.2. Western Digital Corporation

5.1.3. Intel Corporation

5.1.4. Micron Technology, Inc.

5.1.5. Kingston Technology Corporation

5.1.6. Seagate Technology Holdings PLC

5.1.7. Toshiba Memory Corporation

5.1.8. ADATA Technology Co., Ltd.

5.1.9. SK Hynix Inc.

5.1.10. Kioxia Holdings Corporation

5.1.11. Huawei Technologies Co., Ltd.

5.1.12. Transcend Information Inc.

5.1.13. Marvell Technology Group Ltd.

5.1.14. IBM Corporation

5.1.15. NetApp, Inc.

5.2. Cross Comparison Parameters (Product Portfolio, Cloud Compatibility, Speed Metrics, Power Consumption, Pricing Strategy, Regional Presence, Customer Support Network, Data Security Capabilities)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

5.9. Government Grants and Incentives

6. Asia Pacific SSD Caching Market Regulatory Framework

6.1. Data Privacy Standards

6.2. Energy Efficiency and Environmental Standards

6.3. Compliance Requirements for Data Storage Solutions

6.4. Certification Processes for Enterprise-Grade Solutions

7. Asia Pacific SSD Caching Future Market Size (In USD Billion)

7.1. Projected Market Growth and Forecasts

7.2. Key Growth Drivers for Future Market Expansion

8. Asia Pacific SSD Caching Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User Industry (In Value %)

8.4. By Deployment Mode (In Value %)

8.5. By Region (In Value %)

8. Asia Pacific SSD Caching Market Analysts Recommendations

8.1. TAM/SAM/SOM Analysis

8.2. Target Customer Segmentation and Demand Analysis

8.3. Product Differentiation Strategies

8.4. Market Expansion Opportunities and Strategic Recommendations

8.5. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins with identifying key variables across the SSD Caching Market in Asia Pacific, considering significant industry stakeholders. This phase entails extensive desk research through reliable databases to define core market drivers and challenges.

Step 2: Market Analysis and Construction

Historical data regarding SSD caching solutions is compiled and analyzed to understand market penetration, user adoption rates, and evolving revenue channels. Insights are drawn from both primary and secondary sources to ensure comprehensive market coverage.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are refined and validated through interviews with industry experts. This approach ensures data accuracy and provides deeper insights into operational efficiencies, market trends, and future projections directly from market practitioners.

Step 4: Research Synthesis and Final Output

Direct collaboration with leading SSD caching companies and tech providers helps verify segment-specific data, ensuring the final report offers precise, validated information across the Asia Pacific SSD caching landscape.

Frequently Asked Questions

1. How big is the Asia Pacific SSD Caching Market?

The Asia Pacific SSD Caching Market is valued at USD 18 billion, based on a five-year historical analysis. This market is primarily driven by the increasing demand for high-speed data processing in sectors like IT, telecommunications, and finance, where the need for low-latency and efficient data access has become critical.

2. What are the key challenges in the Asia Pacific SSD Caching Market?

Major challenges include high initial investment costs, technical integration hurdles, and stringent data privacy regulations, which impact the deployment of SSD caching solutions in the region.

3. Who are the leading players in the Asia Pacific SSD Caching Market?

Leading players include Samsung Electronics, Western Digital, Intel, Micron Technology, and Toshiba Memory, each known for strong product portfolios and substantial R&D investments.

4. Which product type dominates the Asia Pacific SSD Caching Market?

NVMe SSD caching leads due to its high-speed performance, appealing to data-intensive applications in AI and big data analytics. It is highly favored by enterprises and data centers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.