Asia Pacific Surgical Robots Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD1854

October 2024

81

About the Report

Asia Pacific Surgical Robots Market Overview

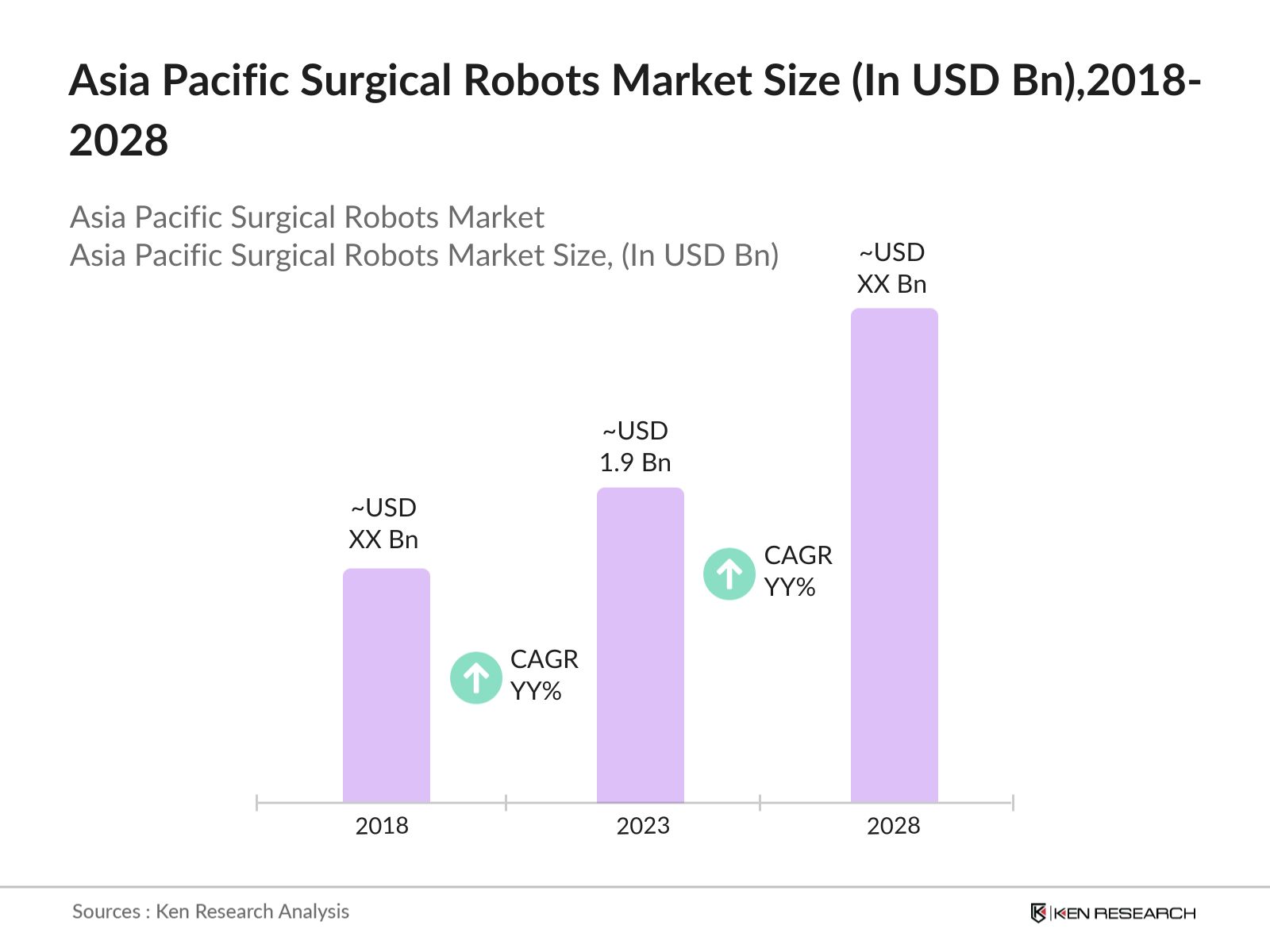

- The Asia Pacific Surgical Robots Market was valued at USD 1.98 Billion in 2023. This growth can be attributed to the increasing adoption of surgical robots in hospitals and healthcare facilities, driven by their ability to enhance precision, reduce recovery times, and improve patient outcomes.

- The market is dominated by several key players, including Intuitive Surgical, Medtronic, Stryker Corporation, Smith & Nephew, and Johnson & Johnson. These companies are leading the market with their innovative robotic surgery systems, extensive research and development activities, and strategic partnerships with healthcare institutions.

- Medtronic's Hugo robotic-assisted surgery system has gained regulatory approval in Japan, marking its entry into the world's third-largest robotics market. This expansion, along with approvals in the EU and Canada, aims to enhance access to minimally invasive surgeries, addressing over 80% of global RAS procedures in general surgery, urology, and gynecology.

- Japan is currently the leading market for surgical robots in the Asia Pacific region, due to Japans advanced healthcare infrastructure, high adoption rate of new technologies, and strong government support for medical innovation. The country's rapidly aging population has also driven the demand for minimally invasive surgeries, further boosting the market for surgical robots.

Asia Pacific Surgical Robots Market Segmentation

The market is segmented into various factors like product, application, and region.

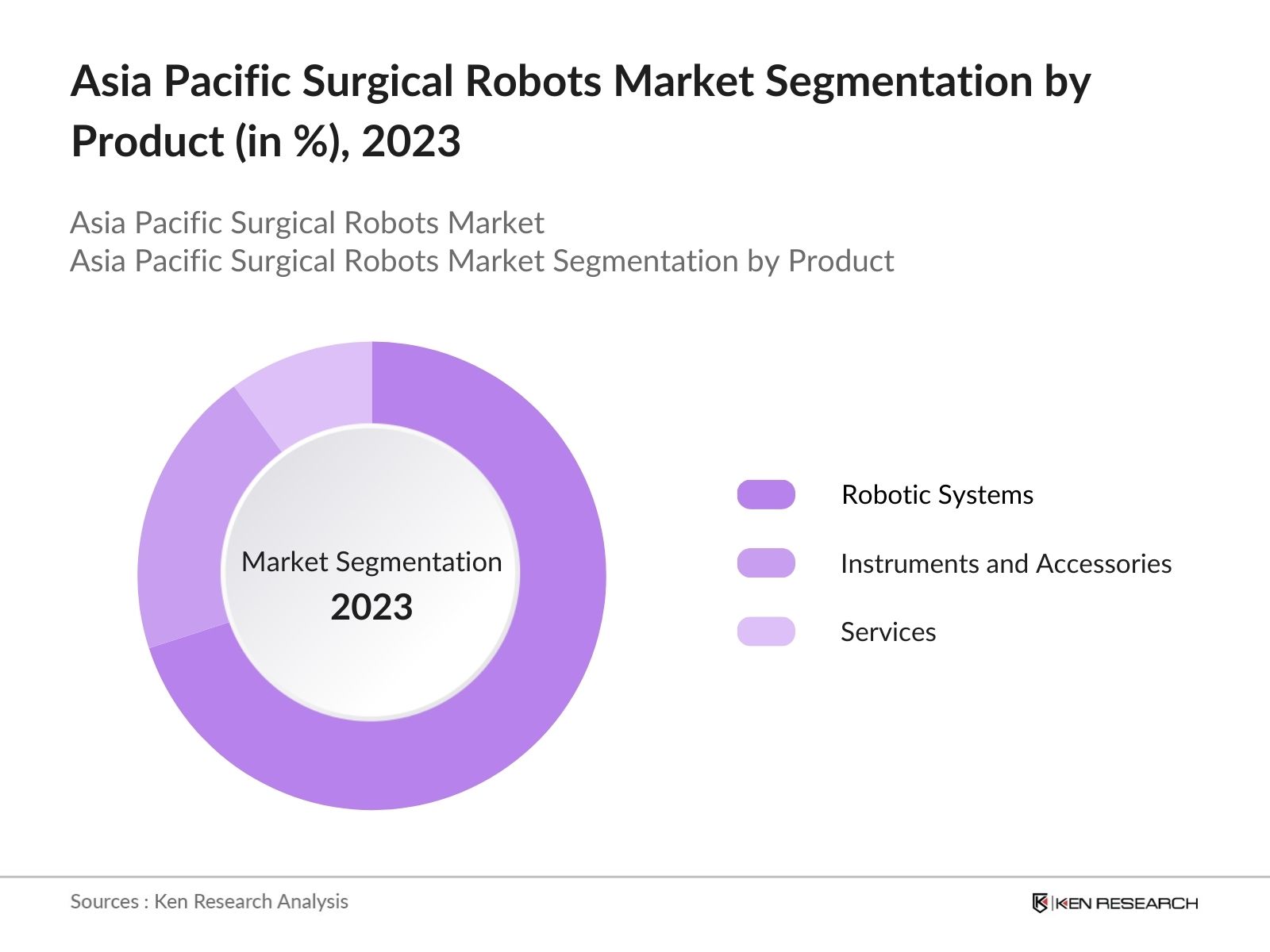

By Product: The market is segmented by product into robotic systems, instruments & accessories, and services. In 2023, robotic systems held a dominant market share, due to the high initial cost of these systems and their critical role in enabling robotic-assisted surgeries.

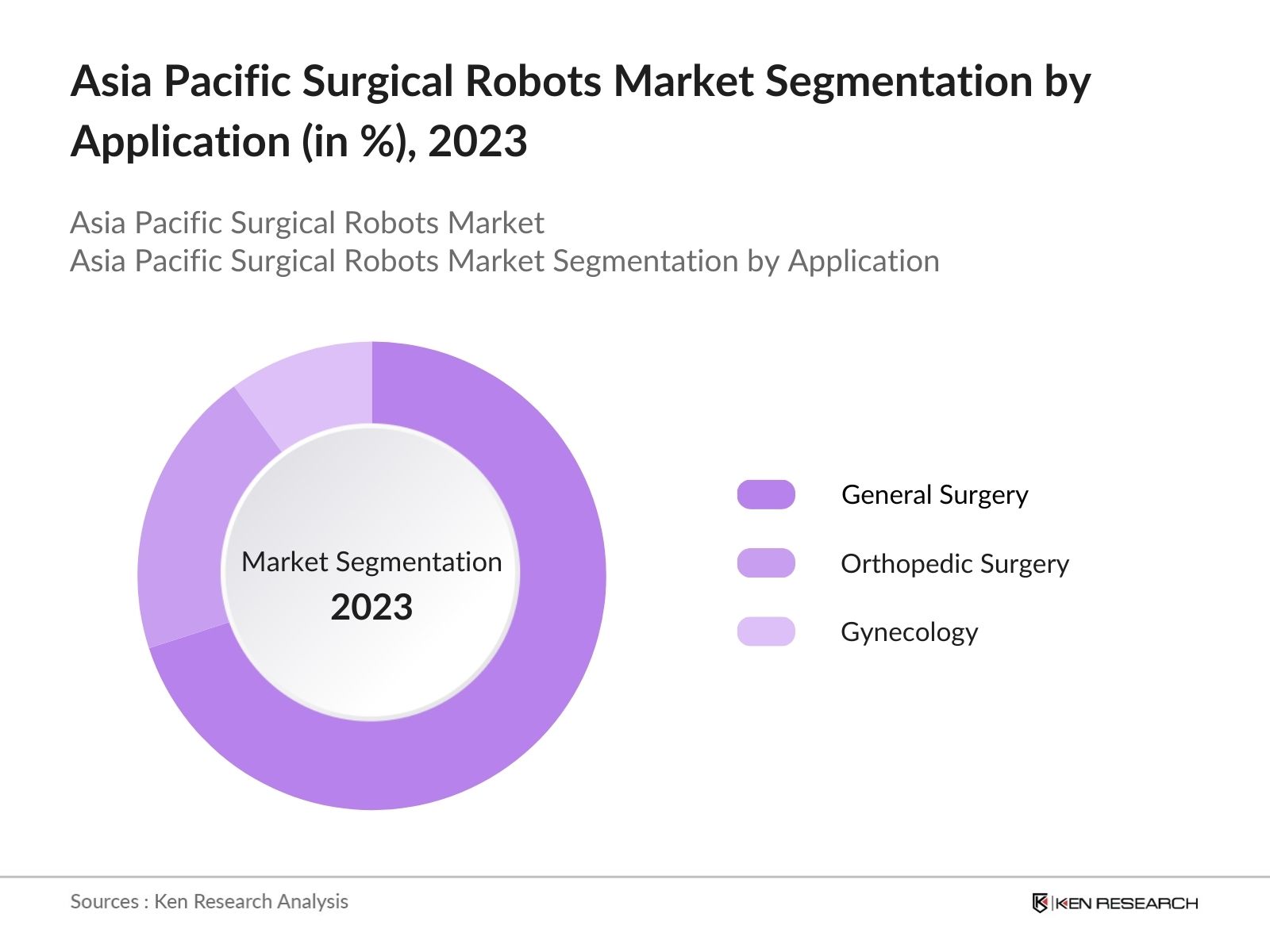

By Application: The market is segmented by application into general surgery, gynecological surgery, urological surgery, orthopedic surgery, and others. In 2023, general surgery emerged as the leading segment, due to the widespread use of robotic systems in complex procedures, such as colorectal and gastrointestinal surgeries, which has fueled the growth of this segment.

By Region: The market is segmented by region into China, South Korea, Japan, India, Australia, and the Rest of APAC. In 2023, Japan led the market with its advanced healthcare system, strong government support for innovation, and a large geriatric population in need of surgical care.

Asia Pacific Surgical Robots Market Competitive Landscape

|

Company Name |

Establishment Year |

Headquarters |

|

Intuitive Surgical |

1995 |

Sunnyvale, California, USA |

|

Medtronic |

1949 |

Dublin, Ireland |

|

Stryker Corporation |

1941 |

Kalamazoo, Michigan, USA |

|

Smith & Nephew |

1856 |

London, United Kingdom |

|

Johnson & Johnson |

1886 |

New Brunswick, New Jersey, USA |

- Johnson & Johnson: Johnson & Johnson (J&J) has acquired Auris Health for $3.4 billion, marking the largest robotics and medtech private M&A deal in history. The deal includes up to $2.35 billion in milestone payments, totaling approximately $5.75 billion. Auris's Monarch platform aims to improve early lung cancer diagnosis and treatment access.

- Intuitive Surgical: Intuitive Surgical's new da Vinci 5 robotic surgery system saw a faster-than-expected rollout in Q2 2024, with 70 units placed, making up 47% of U.S. placements. This contributed to a 14.5% increase in revenue to $2.01 billion and a 25.2% increase in net income to $526.9 million compared to the same period last year.

Asia Pacific Surgical Robots Market Analysis

Market Growth Drivers

- Increased Surgical Procedures in Aging Population: The Asia Pacific region, particularly Japan and South Korea, is experiencing a rapid increase in the aging population. By 2024, Japan alone will have over 36 million people aged 65 and older. This demographic shift is leading to a surge in the number of surgical procedures required for age-related conditions. As a result, the demand for surgical robots, which enhance precision and reduce recovery times, is expected to rise.

- Healthcare Infrastructure Development: The Indian government's commitment to healthcare infrastructure is evident in its allocation of over $200 billion for medical infrastructure by 2024. This investment is set to significantly boost the adoption of advanced medical technologies, including surgical robots, across India, enhancing healthcare accessibility and driving market growth in the surgical robots sector.

- Surge in Chronic Diseases: The rising prevalence of chronic diseases, such as cardiovascular diseases and cancer, is a significant growth driver for the surgical robots market in the Asia Pacific region. In 2024, it is estimated that over 8 million new cases of cancer will be diagnosed in the region, necessitating complex surgical interventions. Surgical robots, known for their precision, are increasingly being utilized in oncology surgeries.

Market Challenges

- High Cost of Surgical Robots: One of the primary challenges facing the surgical robots market in the Asia Pacific region is the high cost associated with the purchase, installation, and maintenance of these systems. The average cost of a surgical robot in 2024 is high, which is prohibitively expensive for many smaller hospitals, particularly in developing countries like India and Vietnam.

- Shortage of Skilled Surgeons: The effective use of surgical robots requires highly trained surgeons, and there is a significant shortage of such professionals in the Asia Pacific region. In 2024, it was reported that less than 20% of surgeons in India and Southeast Asia had received formal training in robotic-assisted surgery.

Government Initiatives

- Chinas Healthcare Modernization Plan: In 2024, China aims to enhance public healthcare access and reduce financial burdens through comprehensive reforms. Key initiatives include improving primary healthcare services, reforming public hospital payment systems, and expanding drug procurement programs to cover 500 medications, ensuring better healthcare for all citizens.

- Indias Subsidy Scheme for Robotic Surgeries: The Indian government introduced a subsidy scheme in 2024 to promote the use of surgical robots in public hospitals. The scheme provides financial assistance of up to 20% of the cost of robotic surgery systems, making it easier for hospitals, particularly in rural areas, to adopt this technology.

Asia Pacific Surgical Robots Market Future Outlook

The Asia Pacific surgical robots industry is expected to grow significantly, with advancements in AI integration, expansion into emerging markets, development of cost-effective systems, and increased government support driving growth over the next five years.

Future Market trends

- Increased Adoption of AI in Surgical Robots: Over the next five years, the Asia Pacific surgical robots industry is expected to see a significant increase in the integration of artificial intelligence (AI) into robotic systems. AI will enhance the precision and efficiency of robotic-assisted surgeries, allowing for more complex procedures to be performed with greater accuracy.

- Development of Cost-Effective Robotic Systems: In response to the high costs associated with current surgical robots, the next five years will see the development and introduction of more cost-effective robotic systems in the Asia Pacific region. These new systems will be designed to be affordable for mid-sized hospitals and emerging markets, without compromising on quality or precision.

Scope of the Report

|

By Product |

Robotic Systems Instruments and Accessories Services |

|

By Application |

General Surgery Orthopedic Surgery Gynecology |

|

By Region |

China South Korea Japan India Australia Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Medical Device Manufacturers

Government Regulatory Bodies

Medical Technology Companies

Banking and Financial Institutions

Technology Investors

Healthcare Companies

Companies

Players Mentioned in the Report:

Intuitive Surgical

Stryker Corporation

Medtronic

Zimmer Biomet

Smith & Nephew

Asensus Surgical

Auris Health

CMR Surgical

Johnson & Johnson

Brainlab

Renishaw

Siemens Healthineers

Think Surgical

Titan Medical

Globus Medical

Table of Contents

1. Asia Pacific Surgical Robots Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Surgical Robots Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Surgical Robots Market Analysis

3.1. Growth Drivers

3.1.1. Aging Population

3.1.2. Healthcare Infrastructure Investments

3.1.3. Prevalence of Chronic Diseases

3.1.4. Government Support for Advanced Technologies

3.2. Restraints

3.2.1. High Costs of Robotic Systems

3.2.2. Shortage of Skilled Surgeons

3.2.3. Regulatory Hurdles

3.2.4. Limited Awareness in Emerging Markets

3.3. Opportunities

3.3.1. AI Integration in Surgical Robots

3.3.2. Expansion into Emerging Markets

3.3.3. Cost-Effective System Development

3.3.4. Increased Government Support for Research

3.4. Trends

3.4.1. AI and Machine Learning in Surgery

3.4.2. Rise of Teleoperated Surgery

3.4.3. Adoption in Emerging Markets

3.4.4. New Product Launches Focused on Cost Efficiency

3.5. Government Regulation

3.5.1. Healthcare Modernization Plans

3.5.2. Subsidy Schemes

3.5.3. Regulatory Approvals for New Systems

3.5.4. National Training Programs

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competitive Ecosystem

4. Asia Pacific Surgical Robots Market Segmentation, 2023

4.1. By Product Type (in Value %)

4.1.1. Robotic Systems

4.1.2. Instruments and Accessories

4.1.3. Services

4.2. By Application (in Value %)

4.2.1. General Surgery

4.2.2. Orthopedic Surgery

4.2.3. Gynecology

4.3. By Region (in Value %)

4.3.1. Japan

4.3.2. China

4.3.3. South Korea

4.3.4. India

4.3.5. Australia

4.3.6. Rest of APAC

5. Asia Pacific Surgical Robots Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. Intuitive Surgical

5.1.2. Medtronic

5.1.3. Stryker Corporation

5.1.4. Zimmer Biomet

5.1.5. Smith & Nephew

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. Asia Pacific Surgical Robots Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7. Asia Pacific Surgical Robots Market Regulatory Framework

7.1. Certification Processes

7.2. Compliance Requirements

7.3. Environmental Standards

8. Asia Pacific Surgical Robots Market Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. Asia Pacific Surgical Robots Market Future Market Segmentation, 2028

9.1. By Product Type (in Value %)

9.2. By Application (in Value %)

9.3. By Region (in Value %)

10. Asia Pacific Surgical Robots Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step:1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step:2 Market Building:

Collating statistics on Asia Pacific Surgical Robots industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Asia Pacific Surgical Robots Industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step:3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step:4 Research output:

Our team will approach multiple healthcare companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such healthcare companies.

Frequently Asked Questions

01 How big is the Asia Pacific Surgical Robots market?

The Asia Pacific Surgical Robots Market was valued at USD 1.98 Billion in 2023. This growth can be attributed to the increasing adoption of surgical robots in hospitals and healthcare facilities, driven by their ability to enhance precision, reduce recovery times, and improve patient outcomes.

02 What are the challenges in Asia Pacific Surgical Robots market?

The major challenges in the Asia Pacific Surgical Robots market include high cost of robotic systems, a shortage of trained surgeons, regulatory hurdles, and limited awareness in emerging markets within the region.

03 Who are the major players in the Asia Pacific Surgical Robots market?

Key players in the Asia Pacific Surgical Robots market include Intuitive Surgical, Medtronic, Stryker Corporation, Zimmer Biomet, and Smith & Nephew, known for their innovative surgical robot systems and extensive market presence.

04 What are the main growth drivers of the Asia Pacific Surgical Robots market?

The growth of the Asia Pacific Surgical Robots market driven by aging population, rising prevalence of chronic diseases, increased government investments in healthcare infrastructure, and the growing adoption of minimally invasive surgeries.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.