Asia Pacific Used Car Market Outlook to 2030

Region:Asia

Author(s):Sanjna

Product Code:KROD9796

Region:Asia

Author(s):Sanjna

Product Code:KROD9796

November 2024

88

By Vehicle Type: The Asia Pacific used car market is segmented by vehicle type into hatchbacks, sedans, SUVs, and pickup trucks. SUVs hold a dominant market share due to consumer preference for larger vehicles that offer more space and versatility. The increased affordability of pre-owned SUVs, coupled with their perceived higher safety and status, makes them a popular choice among buyers in both urban and rural areas. Brands like Toyota and Hyundai have a strong foothold in the SUV segment, further driving its dominance.

By Fuel Type: The market is also segmented by fuel type into petrol, diesel, and electric/hybrid vehicles. Petrol vehicles dominate the market share due to their widespread availability, lower upfront costs, and easier maintenance compared to diesel and electric counterparts. With consumers showing increasing interest in fuel-efficient and affordable options, petrol cars have maintained their strong presence in the market. However, the growing awareness of environmental concerns is gradually shifting attention toward electric and hybrid options.

Asia Pacific Used Car Market Competitive Landscape

Asia Pacific Used Car Market Competitive LandscapeThe Asia Pacific used car market is highly competitive, with a mix of established automakers, online platforms, and independent dealerships. Companies such as Maruti Suzuki, CARS24, and Alibaba-backed Tmall Cars dominate the market, leveraging their extensive networks, digital presence, and certified pre-owned programs to attract consumers. This competitive landscape is also witnessing new entrants focusing on AI-driven platforms that offer better vehicle valuation and customer experience.

|

Company Name |

Establishment Year |

Headquarters |

Market Reach |

Online Sales Platform |

Certified Pre-Owned Vehicles |

Warranty Programs |

Financing Options |

Number of Dealerships |

|

Maruti Suzuki True Value |

1983 |

New Delhi, India |

- |

- |

- |

- |

- |

- |

|

CARS24 |

2015 |

Gurugram, India |

- |

- |

- |

- |

- |

- |

|

Toyota U-Trust |

2007 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

|

Alibaba (Tmall Cars) |

1999 |

Hangzhou, China |

- |

- |

- |

- |

- |

- |

|

Honda Auto Terrace |

2001 |

Tokyo, Japan |

- |

- |

- |

- |

- |

- |

The Asia Pacific used car market is expected to witness significant growth in the coming years. Key drivers include the growing adoption of digital sales platforms, government incentives promoting electric and hybrid vehicle adoption, and the increasing availability of affordable financing options. The shift towards eco-friendly transportation solutions is expected to create a steady demand for electric and hybrid used cars, while traditional petrol and diesel models will continue to dominate in the short term.

|

Segment |

Sub-Segments |

|

By Vehicle Type |

Hatchbacks |

|

Sedans |

|

|

SUVs |

|

|

Pickup Trucks |

|

|

By Fuel Type |

Petrol |

|

Diesel |

|

|

Electric/Hybrid |

|

|

By Sales Channel |

Online Platforms |

|

Franchise Dealers |

|

|

Independent Dealers |

|

|

By End User |

Individual Buyers |

|

Commercial Fleet Buyers |

|

|

By Region |

China |

|

India |

|

|

Japan |

|

|

South Korea |

|

|

ASEAN |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics Overview

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (e.g., rise in disposable income, digital transformation in car sales, affordability trends)

3.1.1. Economic Recovery

3.1.2. Increasing Internet Penetration

3.1.3. Growing Consumer Shift from New to Used Cars

3.1.4. Increased Supply of Quality Used Cars (lease returns, rental fleet renewals)

3.2. Market Challenges (e.g., lack of transparency in car history, fragmented regulatory environment)

3.2.1. Vehicle Fraud

3.2.2. Absence of Uniform Pricing

3.2.3. Complex Regulatory and Tax Structures

3.3. Opportunities (e.g., technological advancements, digital platforms)

3.3.1. Adoption of AI-Based Valuation Tools

3.3.2. Growth in Online and Omnichannel Used Car Platforms

3.3.3. Financing and Warranty Options

3.4. Trends (e.g., growing demand for certified pre-owned vehicles, sustainability trends)

3.4.1. Increasing Preference for Electric and Hybrid Used Cars

3.4.2. Rising Demand for Crossovers and SUVs in Used Car Segment

3.4.3. Digital Platforms Offering Instant Financing and Online Purchases

3.5. Government Regulation (e.g., vehicle emissions standards, import/export regulations)

3.5.1. Vehicle Import Policies

3.5.2. Regulatory Standards for Emissions and Safety

3.5.3. Changes in GST/VAT on Used Cars

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (manufacturers, dealers, auction houses, leasing companies)

3.8. Porters Five Forces (supplier power, buyer power, competitive rivalry)

3.9. Competitive Ecosystem

4.1. By Vehicle Type (In Value %)

4.1.1. Hatchbacks

4.1.2. Sedans

4.1.3. SUVs

4.1.4. Pickup Trucks

4.2. By Fuel Type (In Value %)

4.2.1. Petrol

4.2.2. Diesel

4.2.3. Electric/Hybrid

4.3. By Sales Channel (In Value %)

4.3.1. Online Platforms

4.3.2. Franchise Dealers

4.3.3. Independent Dealers

4.4. By End User (In Value %)

4.4.1. Individual Buyers

4.4.2. Commercial Fleet Buyers

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. South Korea

4.5.5. ASEAN

5.1. Detailed Profiles of Major Companies

5.1.1. CarTrade Tech Ltd.

5.1.2. OLX Autos

5.1.3. Maruti Suzuki True Value

5.1.4. CARS24

5.1.5. Hyundai H Promise

5.1.6. Honda Auto Terrace

5.1.7. Toyota U-Trust

5.1.8. Alibaba Group (Tmall Cars)

5.1.9. Mahindra First Choice

5.1.10. Droom Technologies

5.2. Cross Comparison Parameters (Year of Establishment, Number of Dealerships, Market Penetration, Certified Pre-Owned Vehicles, Online Sales Platform, After-Sales Service, Warranty Policies, Financing Options)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Emission Norms

6.2. Ownership Transfer Regulations

6.3. Warranty and Inspection Requirements

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Vehicle Type (In Value %)

8.2. By Fuel Type (In Value %)

8.3. By Sales Channel (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Market Penetration Strategies

9.3. White Space Opportunity Analysis

The research process begins with identifying all critical variables influencing the Asia Pacific used car market, including economic recovery rates, consumer purchasing behavior, and regulatory frameworks. This step is supported by extensive desk research using a mix of proprietary and secondary databases to compile relevant market information.

In this phase, historical data on used car sales, vehicle depreciation rates, and consumer trends are compiled. Data on vehicle supply chains, including dealership networks and online platform penetration, is analyzed to provide accurate market insights.

Through telephone interviews with industry experts from major automotive companies and digital car trading platforms, key market hypotheses are validated. These consultations provide operational insights that ensure the accuracy of the collected data.

The final synthesis involves direct engagement with automotive manufacturers, dealers, and platforms to gather detailed insights into customer preferences, sales performance, and certification programs. This ensures a thorough analysis of the Asia Pacific used car market.

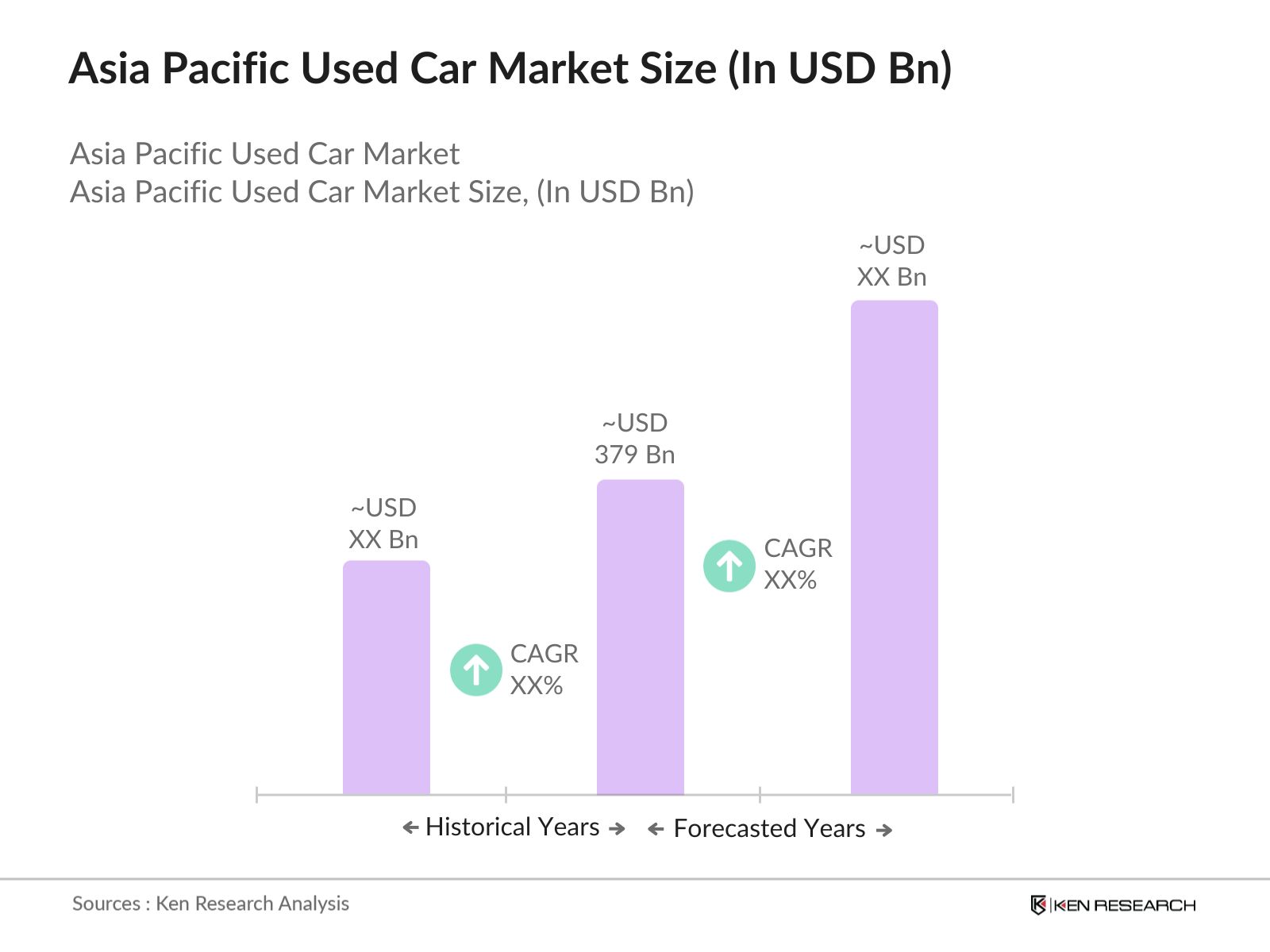

The Asia Pacific used car market is valued at USD 379 billion, driven by factors such as consumer demand for affordable cars, digital trading platforms, and a steady supply of quality pre-owned vehicles.

Key challenges in Asia Pacific used car market include a lack of transparency in car history, inconsistent pricing mechanisms across markets, and complex regulatory frameworks governing vehicle ownership transfers and emissions standards.

The major players in Asia Pacific used car market include Maruti Suzuki True Value, CARS24, Toyota U-Trust, Alibaba (Tmall Cars), and Honda Auto Terrace, each contributing significantly through their extensive networks and online platforms.

Growth in Asia Pacific used car market is driven by factors such as the increasing shift towards digital car trading, the rising affordability of pre-owned vehicles, and a steady increase in the supply of used cars from lease returns and fleet renewals.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.