Asia Pacific Vegetable Market Outlook to 2030

Region:Afganistan

Author(s):Shreya Garg

Product Code:KROD8710

Region:Afganistan

Author(s):Shreya Garg

Product Code:KROD8710

December 2024

97

Listen to the audio summary

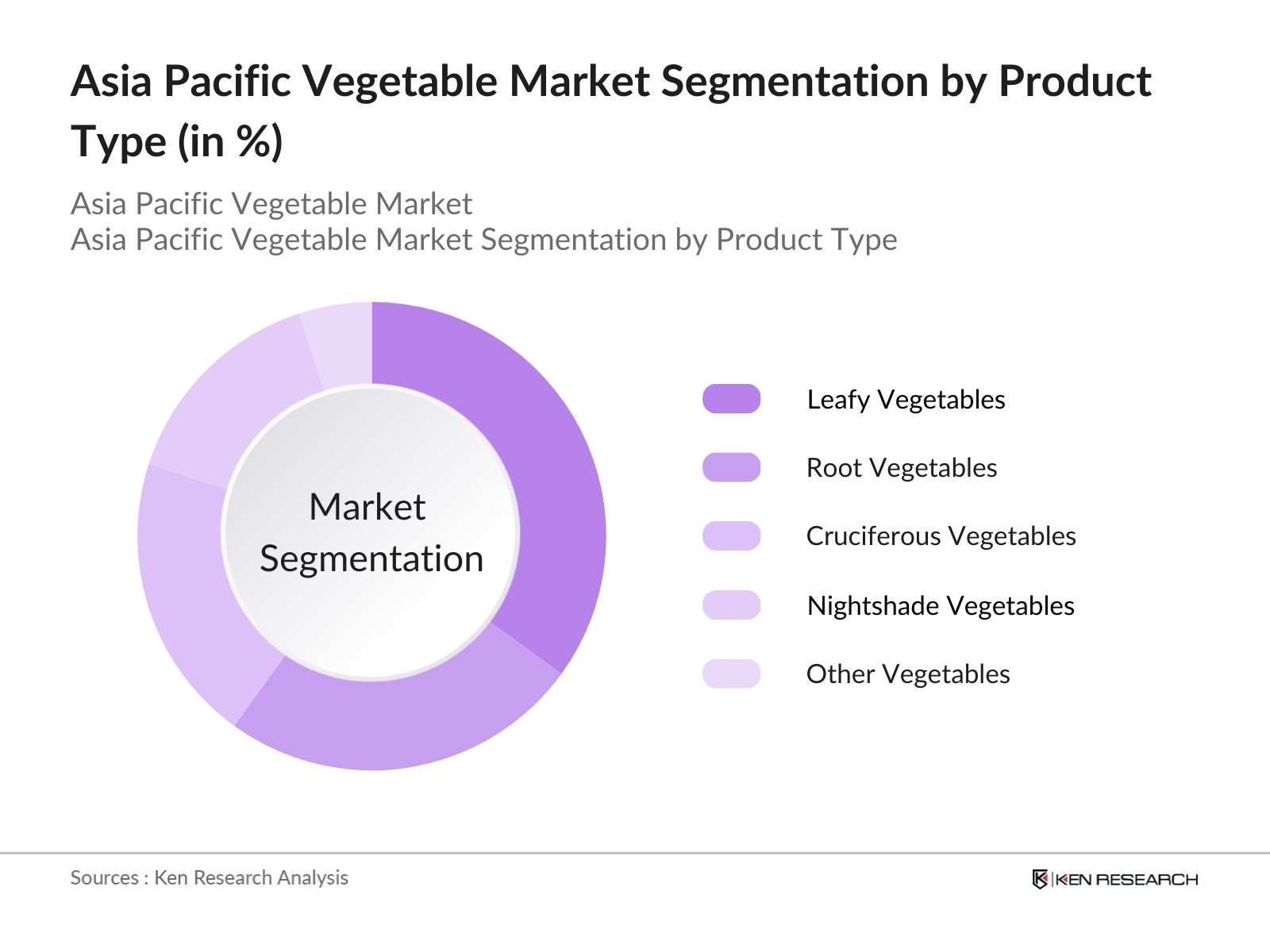

By Product Type: The market is segmented by product type into leafy vegetables, root vegetables, cruciferous vegetables, and nightshade vegetables. Leafy vegetables, including spinach and lettuce, dominate the product type segmentation due to increasing consumer demand for healthy and nutrient-dense foods. The high yield and relatively shorter growing period of leafy vegetables, combined with the rising popularity of organic produce, make them a top choice among consumers, particularly in urban areas where health-consciousness is growing rapidly.

By Distribution Channel: The market is also segmented by distribution channel into direct-to-consumer (farmers markets), retail distribution (supermarkets, convenience stores), food service (restaurants, catering), and online channels. Retail distribution holds a dominant market share as consumers increasingly prefer the convenience of purchasing fresh produce from supermarkets and convenience stores. Major retail chains in countries like China and India have extensive distribution networks that ensure the availability of fresh vegetables, contributing to the growth of this segment.

The Asia Pacific vegetable market is characterized by the presence of a few key players who dominate the market through extensive distribution networks, product innovation, and sustainability initiatives. Key companies are implementing advanced farming technologies such as IoT-based precision farming and organic production methods, which are critical differentiators in the competitive landscape. The competitive landscape highlights the consolidation of the market among these few large players, with a significant influence on price and supply dynamics.

|

Company Name |

Established |

Headquarters |

Production Volume |

Sustainability Initiatives |

Distribution Network |

R&D Investments |

Technological Integration |

Product Portfolio |

|

Olam International |

1989 |

Singapore |

||||||

|

Fresh Del Monte Produce |

1886 |

USA |

||||||

|

Dole Food Company |

1851 |

USA |

||||||

|

Nature's Pride |

2000 |

Netherlands |

||||||

|

Costa Group |

1888 |

Australia |

The Asia Pacific vegetable market is expected to witness substantial growth in the coming years, driven by technological advancements such as smart irrigation systems, precision agriculture, and growing demand for organic produce. Urbanization and rising health awareness will continue to fuel the market, while government initiatives supporting sustainable farming practices will further drive production efficiency. The shift toward eco-friendly and organic vegetables will remain a key trend, as consumers increasingly prefer pesticide-free produce, further expanding the market for organic vegetables.

|

Product Type |

Leafy Vegetables Root Vegetables Cruciferous Vegetables Nightshade Vegetables Other Vegetables |

|

Farming Method |

Traditional Farming Organic Farming Hydroponics Vertical Farming |

|

Distribution Channel |

Direct to Consumer Retail Distribution Food Service |

|

End Use |

Fresh Consumption Processed and Frozen Vegetables Packaged Meals and Ready-to-Eat |

|

Region |

China India Southeast Asia Australia and New Zealand Rest of Asia Pacific |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics Overview (Consumer Preferences, Organic Farming Practices, Irrigation Technology Advancements, Sustainable Farming Trends)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Trade Policies, Climate Adaptation Technologies, Regional Government Initiatives)

3.1. Growth Drivers

3.1.1. Shift Toward Organic and Non-GMO Produce

3.1.2. Increased Government Support for Agricultural Sustainability Programs

3.1.3. Expansion of the Export Market to Developed Nations

3.1.4. Increasing Health Awareness Among Consumers

3.2. Market Challenges

3.2.1. Weather Dependency and Climate Change

3.2.2. Limited Access to Advanced Farming Technologies in Rural Areas

3.2.3. High Production Costs and Labor Shortages

3.3. Opportunities

3.3.1. Integration of IoT and Precision Agriculture in Vegetable Farming

3.3.2. Growing Demand for Packaged and Ready-to-Eat Vegetable Products

3.3.3. Expansion into Urban Vertical Farming

3.4. Market Trends

3.4.1. Increased Focus on Sustainable Agricultural Practices

3.4.2. Emergence of Smart Irrigation Systems

3.4.3. Adoption of Blockchain for Food Traceability

3.5. Government Regulation

3.5.1. Asia-Pacific Agricultural Subsidy Programs

3.5.2. Organic Certification and Regulations

3.5.3. Environmental Standards for Water and Soil Usage

3.5.4. National Food Security Policies

3.6. SWOT Analysis (Specific to Vegetable Farming)

3.7. Stake Ecosystem (Farmers, Distributors, Retailers, Processors)

3.8. Porters Five Forces (Bargaining Power of Buyers, Threat of Substitutes, etc.)

3.9. Competitive Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Leafy Vegetables (Lettuce, Spinach)

4.1.2. Root Vegetables (Carrots, Potatoes)

4.1.3. Cruciferous Vegetables (Broccoli, Cauliflower)

4.1.4. Nightshade Vegetables (Tomatoes, Peppers)

4.1.5. Other Vegetables (Mushrooms, Asparagus)

4.2. By Farming Method (In Value %)

4.2.1. Traditional Farming

4.2.2. Organic Farming

4.2.3. Hydroponics

4.2.4. Vertical Farming

4.3. By Distribution Channel (In Value %)

4.3.1. Direct to Consumer (Farmers Markets)

4.3.2. Retail Distribution (Supermarkets, Convenience Stores)

4.3.3. Food Service (Restaurants, Catering)

4.4. By End Use (In Value %)

4.4.1. Fresh Consumption

4.4.2. Processed and Frozen Vegetables

4.4.3. Packaged Meals and Ready-to-Eat

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Southeast Asia

4.5.4. Australia and New Zealand

4.5.5. Rest of Asia Pacific

5.1. Detailed Profiles of Major Companies

5.1.1. Olam International

5.1.2. Fresh Del Monte Produce Inc.

5.1.3. Dole Food Company

5.1.4. Nature's Pride

5.1.5. Kagome Co., Ltd.

5.1.6. Greenyard NV

5.1.7. Griffith Foods

5.1.8. Costa Group

5.1.9. Total Produce

5.1.10. Sunfresh Farms Inc.

5.1.11. Sakata Seed Corporation

5.1.12. Vilmorin & Cie

5.1.13. Bonduelle Group

5.1.14. Hortifrut SA

5.1.15. Sumitomo Chemical Co., Ltd.

5.2. Cross Comparison Parameters (Production Volume, Regional Market Share, Sustainability Initiatives, Revenue, Distribution Reach, Technological Integration, Product Portfolio, R&D Investments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants for Agribusiness

5.8. Private Equity Investments

6.1. Import and Export Policies

6.2. Compliance Requirements for Organic Certification

6.3. Certification Processes for Non-GMO Products

6.4. Water Use and Environmental Compliance Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Health Trends, Technological Innovations in Farming)

8.1. By Product Type (In Value %)

8.2. By Farming Method (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End Use (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Cohort Analysis

9.3. Marketing Strategies

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial stage of this report involved identifying critical variables such as vegetable production volume, farming practices, and consumer preferences across the Asia Pacific region. Data from government sources, industry reports, and proprietary databases were used to define key factors influencing market dynamics.

This phase involved an in-depth analysis of historical data, focusing on agricultural production statistics, export trends, and consumption patterns in the Asia Pacific vegetable market. We analyzed these variables to construct a comprehensive view of market growth.

Key market hypotheses were validated through consultations with agricultural experts, farmers, and government officials. These insights provided real-world perspectives on production challenges, technological adoption, and distribution strategies.

The final stage included synthesizing the data collected and providing a validated analysis of the market. This was done through engagement with vegetable producers, ensuring the accuracy of the reports findings and providing a comprehensive outlook on future trends.

The Asia Pacific vegetable market is valued at USD 61.5 billion, driven by increased consumer demand for fresh and organic produce, along with government-backed initiatives aimed at improving agricultural productivity.

The Asia Pacific vegetable market faces challenges such as climate change, labor shortages, and rising production costs, which impact the efficiency and sustainability of farming practices across the region.

Major players in the Asia Pacific vegetable market include Olam International, Fresh Del Monte Produce Inc., Dole Food Company, Natures Pride, and Costa Group. These companies dominate due to their vast distribution networks and advanced farming techniques.

The Asia Pacific vegetable market is primarily driven by the rising health awareness among consumers, government support for sustainable farming practices, and advancements in farming technologies such as precision agriculture.

Future trends in the Asia Pacific vegetable market include the adoption of smart farming technologies, increased demand for organic produce, and a shift towards urban vertical farming to meet the rising demand for fresh vegetables in densely populated urban centers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.