Asia-Pacific Virtual Reality (VR) Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD7060

December 2024

92

About the Report

Asia-Pacific Virtual Reality (VR) Market Overview

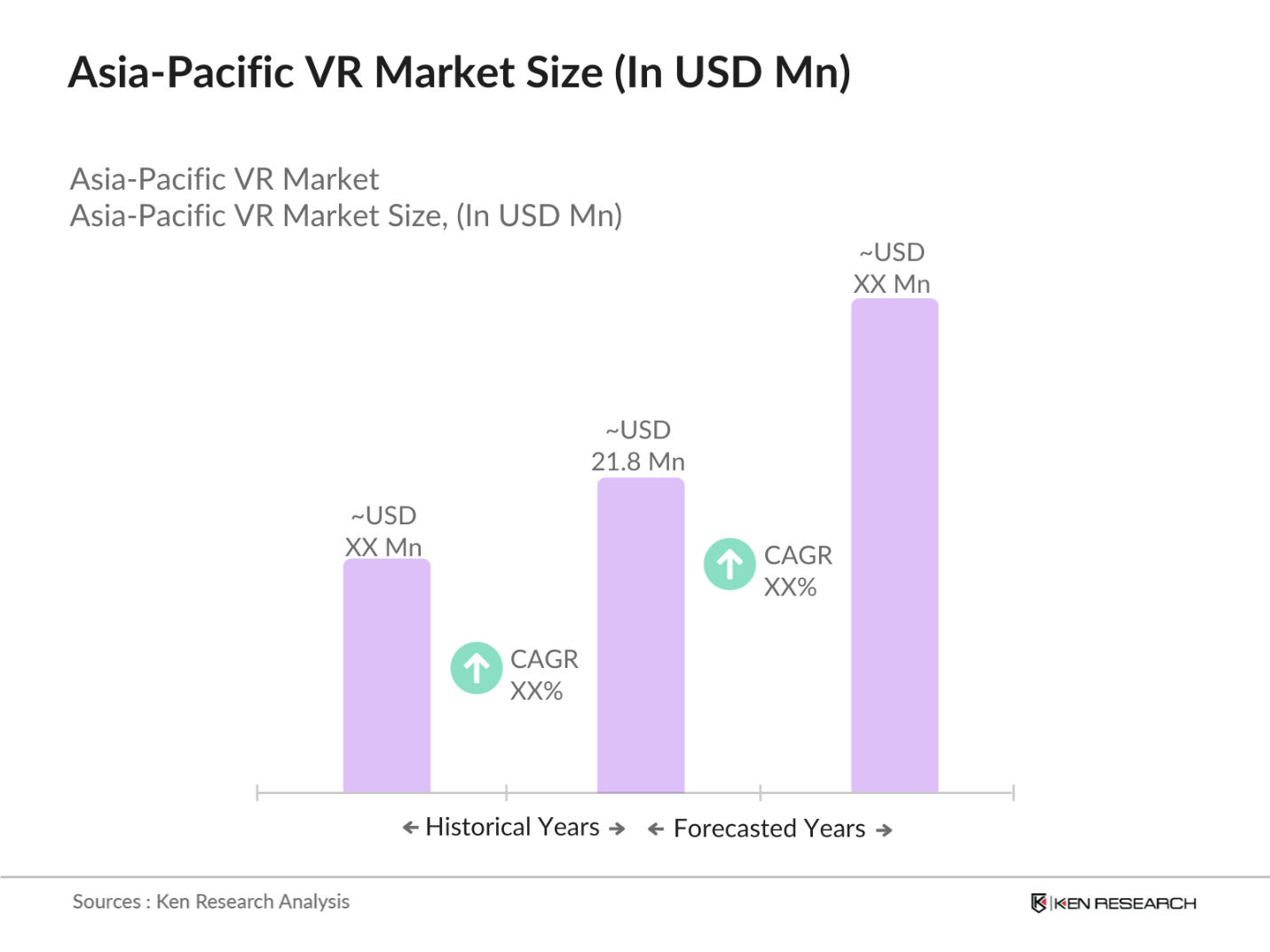

- The Asia-Pacific Virtual Reality (VR) market is valued at USD 21.8 billion, driven by rapid advancements in immersive technologies and the increasing adoption of VR across industries such as gaming, healthcare, education, and retail. The adoption is heavily supported by governments promoting digital transformation and increased investments in technology infrastructure. Rising consumer demand for innovative and interactive experiences is fueling the markets growth, with sectors like entertainment and education leading the way. Notably, the widespread use of VR headsets in gaming and professional training environments has contributed significantly to the market's value.

- Dominant countries such as China, Japan, and South Korea lead the market, driven by high levels of technological advancement, strong gaming industries, and proactive government support for the tech sector. China's dominance stems from its large-scale manufacturing capabilities and consumer base, while Japan and South Korea are front-runners due to their cutting-edge technology ecosystems and investment in AR/VR innovations. These regions also benefit from a robust gaming culture, which has significantly boosted the demand for VR hardware and content.

- Data privacy laws in the Asia-Pacific region are beginning to affect the VR market, particularly in countries like Japan and South Korea. In 2023, Japan implemented the Act on the Protection of Personal Information, mandating strict data privacy protocols for VR applications, especially in gaming and healthcare. South Korea's Personal Information Protection Commission introduced similar regulations, requiring companies to adopt higher standards of data security for VR applications that handle sensitive personal data.

Asia-Pacific Virtual Reality (VR ) Market Segmentation

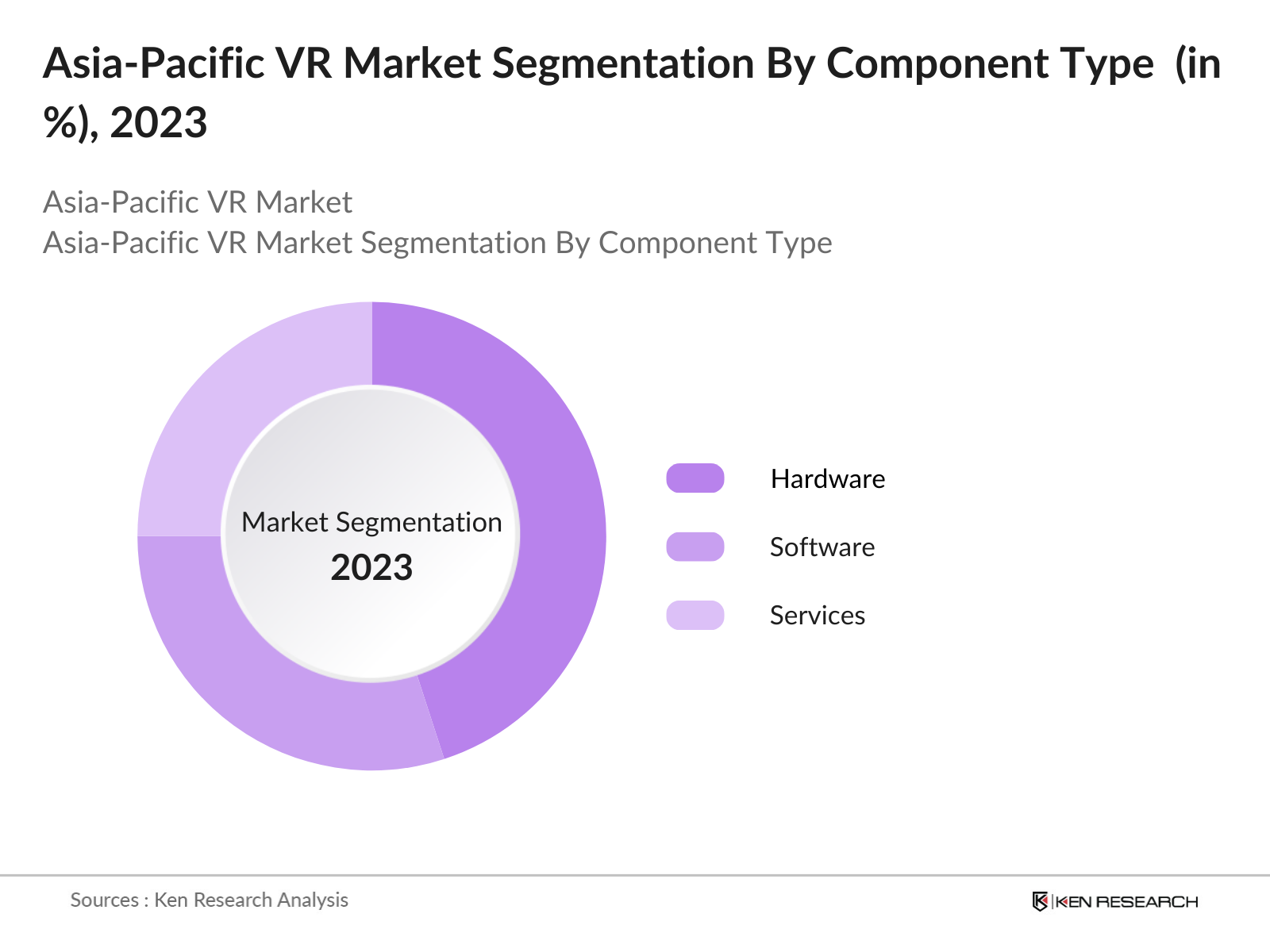

By Component: The Asia-Pacific VR market is segmented by components into hardware, software, and services. Hardware dominates the market due to the significant demand for VR headsets, sensors, and controllers. Within this segment, head-mounted displays (HMDs) have been leading, thanks to their growing applications in gaming, healthcare, and education. The surge in consumer interest in gaming and entertainment experiences, particularly after the introduction of affordable and user-friendly devices like the Oculus Rift and HTC Vive, has driven demand for HMDs.

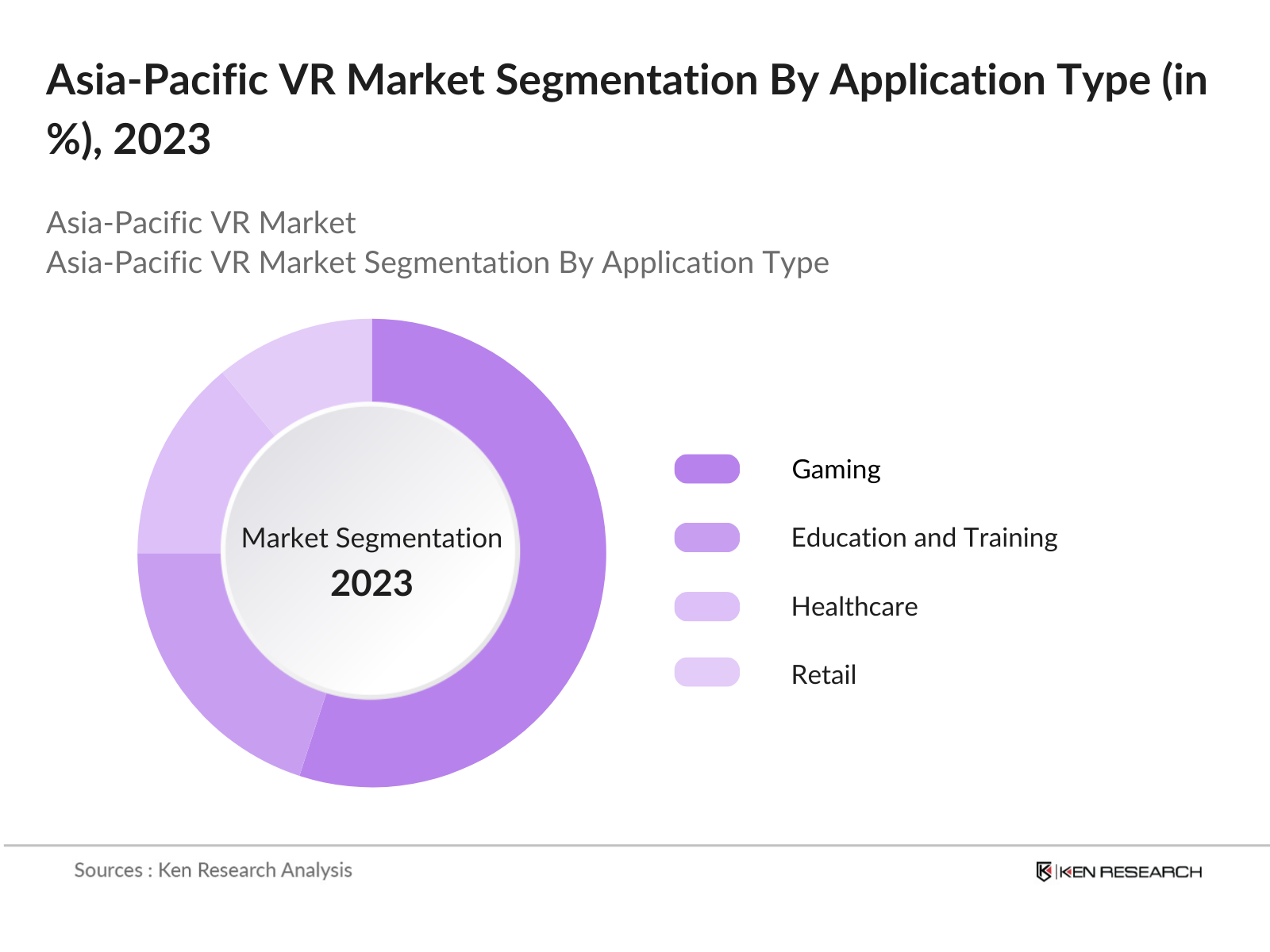

By Application: The VR market is segmented by applications into gaming, education and training, healthcare, retail, and real estate. Gaming remains the dominant sub-segment, driven by immersive gaming experiences and the increasing availability of VR-compatible games across platforms. The rise of eSports, coupled with major game development studios creating VR versions of popular titles, has ensured gaming's continued leadership in this category. Furthermore, advancements in 5G technology are enabling smoother and more interactive VR gaming experiences, attracting a broader audience.

Asia-Pacific Virtual Reality (VR ) Market Competitive Landscape

The Asia-Pacific VR market is dominated by several key players, both local and global. The market remains competitive, with major companies constantly innovating to stay ahead of trends. Companies such as Sony Corporation and HTC Corporation lead due to their strong foothold in both hardware production and VR content development. Meanwhile, Microsoft is gaining ground through its enterprise VR solutions, and Unity Technologies is a leader in providing VR development tools for creating immersive environments.

|

Company |

Established |

Headquarters |

Product Portfolio |

Global Presence |

R&D Investment |

Partnerships |

Market Share |

Recent Innovations |

Patents |

|

Sony Corporation |

1946 |

Tokyo, Japan |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

HTC Corporation |

1997 |

Taipei, Taiwan |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Oculus (Meta Platforms) |

2012 |

Menlo Park, USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Microsoft Corporation |

1975 |

Redmond, USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Unity Technologies |

2004 |

San Francisco, USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

Asia-Pacific Virtual Reality (VR ) Industry Analysis

Growth Drivers

- Technological Advancements in VR Hardware: The advancement in VR hardware such as headsets and sensors has been a significant driver in the Asia-Pacific region. In 2024, countries like Japan and South Korea reported a steady rise in demand for VR devices, driven by investments in technological R&D. For instance, South Korea invested over $3 billion in virtual and augmented reality technologies, supporting the hardware sector. Additionally, innovations in sensors have improved the accuracy and experience of VR, with Japan's Ministry of Economy highlighting investments of $1.5 billion toward VR hardware research.

- Increased Adoption in Gaming and Entertainment: The gaming industry in the Asia-Pacific region has seen increased integration of VR technologies, significantly driving demand. In 2023, China's VR gaming market was bolstered by a $1.2 billion investment in VR content creation. The entertainment sector in countries like South Korea and Japan has also embraced VR experiences, particularly in e-sports and cinema, further driving growth. Data from the Ministry of Science and ICT in South Korea shows a 15% increase in VR adoption in the entertainment industry compared to 2022.

- Government Support for Digital Transformation: Governments across the Asia-Pacific are investing in digital transformation, with a focus on integrating VR into various sectors. For instance, in 2024, the Chinese government allocated $600 million towards fostering digital technology, including VR, in public services such as education and healthcare. Similarly, India's Ministry of Electronics and Information Technology announced a $500 million initiative to integrate VR in the country's digital transformation efforts, especially for smart cities.

Market Challenges

- High Cost of Advanced VR Systems: The cost of advanced VR systems remains a barrier to mass adoption, particularly in developing economies. In 2023, reports from India's Ministry of Electronics and Information Technology showed that high-end VR systems can cost upwards of $1,500, a price point that remains prohibitive for many consumers. Additionally, affordability is a challenge across Southeast Asian countries, where median incomes are substantially lower, limiting widespread consumer adoption of premium VR equipment.

- Limited Content Availability for Non-Gaming Applications: A lack of sufficient VR content outside gaming continues to constrain the market in 2024. In China, despite significant growth in the gaming sector, VR content tailored to education, healthcare, and other industries remains limited. A government report from Japans Ministry of Economy, Trade, and Industry indicated that only 25% of VR content development is focused on non-gaming sectors. This gap in content diversity poses a challenge to market expansion beyond entertainment

Asia-Pacific Virtual Reality (VR ) Market Future Outlook

Over the next five years, the Asia-Pacific VR market is expected to experience significant growth driven by continuous technological advancements, government initiatives supporting digital innovation, and increased demand across various industries. The growth will be supported by the integration of VR with other emerging technologies such as AI and 5G, leading to more interactive and seamless VR experiences. Additionally, sectors like education, healthcare, and enterprise training will increasingly rely on VR for practical and immersive simulations, further boosting market expansion.

Opportunities

Expansion of VR into Education and Healthcare: The integration of VR in education and healthcare presents significant opportunities for growth. In 2024, Singapore allocated $50 million towards VR-based medical training programs, highlighting its application in medical education. Similarly, Chinas education ministry is piloting VR in schools, with over 200 institutions adopting VR for immersive learning experiences. These developments indicate the potential for VR to transform both education and healthcare systems across the Asia-Pacific region.

Adoption of 5G for Enhanced VR Experiences: With the rollout of 5G in countries like South Korea, Japan, and China, VR experiences have become more immersive due to faster data transfer speeds. In 2023, South Koreas Ministry of Science and ICT reported that over 60% of VR users experienced enhanced performance with 5G-enabled devices, driving further VR adoption. Japan's 5G expansion has also led to improved VR streaming quality, particularly in gaming and entertainment applications, which rely on low latency.

Scope of the Report

|

By Component |

Hardware Software Services |

|

By Application |

Gaming Education and Training Healthcare Retail Real Estate |

|

By Device Type |

Head-Mounted Displays (HMDs) Gesture-tracking Devices Data Gloves Stationary VR Systems |

|

By End-User Industry |

Consumer Enterprise Healthcare Military and Defense Automotive |

|

By Country/Region |

China Japan South Korea India Australia |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

VR Hardware Companies

Gaming Studios and Developers

Government and Regulatory Bodies (Ministry of Industry and Information Technology, Japans METI)

Healthcare Providers and Hospital Industry

Enterprise Training Companies

Venture Capital and Investment Firms

Telecommunication Companies (5G Providers)

Companies

Players Mentioned in the Report:

Sony Corporation

HTC Corporation

Oculus (Meta Platforms)

Microsoft Corporation

Unity Technologies

Samsung Electronics Co., Ltd.

Varjo Technologies

Xiaomi Corporation

Lenovo Group Ltd.

LG Electronics

Table of Contents

1. Asia-Pacific VR Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia-Pacific VR Market Size (in USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia-Pacific VR Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Adoption of Immersive Technologies in Gaming (Industry-specific)

3.1.2. Rising Demand for VR in Education and Training (Industry-specific)

3.1.3. Government Support for Digital Transformation (Industry-specific)

3.1.4. Surge in Remote Work Solutions (Industry-specific)

3.2. Market Challenges

3.2.1. High Development and Implementation Costs (Cost Barrier)

3.2.2. Limited Content Availability (Content Creation Bottleneck)

3.2.3. Lack of Standardization (Technology Standards)

3.2.4. Latency and Technical Limitations (Performance Barriers)

3.3. Opportunities

3.3.1. Expansion of 5G Networks (Technology Booster)

3.3.2. Integration of AI in VR (Emerging Technologies)

3.3.3. Collaborations with Educational Institutions (New Market Applications)

3.3.4. Growing Adoption in Healthcare (Emerging Sectors)

3.4. Trends

3.4.1. Advancements in Haptic Feedback (Technology Trends)

3.4.2. Use of VR for Employee Training (Corporate Adoption)

3.4.3. Rise of Location-based VR Entertainment (Consumer Trends)

3.4.4. Personalized VR Experiences (Customization Trends)

3.5. Government Regulations

3.5.1. Data Privacy Laws (APAC Regulatory Environment)

3.5.2. Funding Initiatives for Digital Innovation (Government Support Programs)

3.5.3. VR-Related Patent Regulations (Intellectual Property)

3.5.4. Cross-border Trade Policies for VR Products (International Trade)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape Overview

4. Asia-Pacific VR Market Segmentation

4.1. By Component (in Value %)

4.1.1. Hardware

4.1.2. Software

4.1.3. Services

4.2. By Application (in Value %)

4.2.1. Gaming

4.2.2. Education and Training

4.2.3. Healthcare

4.2.4. Retail

4.2.5. Real Estate

4.3. By Device Type (in Value %)

4.3.1. Head-Mounted Displays (HMDs)

4.3.2. Gesture-tracking Devices

4.3.3. Data Gloves

4.3.4. Stationary VR Systems

4.4. By End-User Industry (in Value %)

4.4.1. Consumer

4.4.2. Enterprise

4.4.3. Healthcare

4.4.4. Military and Defense

4.4.5. Automotive

4.5. By Country/Region (in Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Australia

5. Asia-Pacific VR Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Sony Corporation

5.1.2. HTC Corporation

5.1.3. Oculus (Meta Platforms)

5.1.4. Samsung Electronics Co., Ltd.

5.1.5. Microsoft Corporation

5.1.6. Unity Technologies

5.1.7. Varjo Technologies

5.1.8. Xiaomi Corporation

5.1.9. Lenovo Group Ltd.

5.1.10. LG Electronics

5.1.11. Pimax Technology

5.1.12. CyberGlove Systems

5.1.13. SenseGlove

5.1.14. Sixense Enterprises Inc.

5.1.15. Noitom Ltd.

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Global Presence, R&D Investment, Number of Patents, Market Share, Strategic Partnerships, Key Innovations)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia-Pacific VR Market Regulatory Framework

6.1. VR Product Safety Standards

6.2. Compliance with Data Protection Regulations

6.3. Certification and Licensing Requirements

6.4. Intellectual Property Rights

7. Asia-Pacific VR Future Market Size (in USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8. Asia-Pacific VR Future Market Segmentation

8.1. By Component (in Value %)

8.2. By Application (in Value %)

8.3. By Device Type (in Value %)

8.4. By End-User Industry (in Value %)

8.5. By Country/Region (in Value %)

9. Asia-Pacific VR Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation and Persona Analysis

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first phase involves identifying key stakeholders and drivers of the Asia-Pacific VR market. Through extensive desk research, we map the entire VR ecosystem, focusing on understanding market dynamics, including manufacturers, developers, and end-users. This phase sets the foundation by isolating the most critical factors influencing market demand and growth.

Step 2: Market Analysis and Construction

In this phase, historical data from VR sales, technology adoption, and content creation are gathered and analyzed. Market penetration rates and adoption levels within each segment are reviewed to assess the markets current state and future growth potential. Data is drawn from credible sources such as industry reports, government publications, and company filings.

Step 3: Hypothesis Validation and Expert Consultation

After gathering preliminary data, the hypotheses on growth drivers and challenges are validated through interviews with industry experts and VR professionals. These insights help refine the market models, providing accuracy in growth projections and identifying potential future trends.

Step 4: Research Synthesis and Final Output

The final phase synthesizes the research data into a comprehensive report. This includes quantitative analysis backed by qualitative insights gained from industry experts. The final report also includes future projections, competitive analysis, and key recommendations for stakeholders.

Frequently Asked Questions

01. How big is the Asia-Pacific VR market?

The Asia-Pacific VR market was valued at USD 21.8 billion, driven by technological innovations and increased adoption in gaming, healthcare, and education sectors. The demand for immersive experiences and VR content is projected to continue rising, further fueling market growth.

02. What are the challenges in the Asia-Pacific VR market?

Key challenges include the high costs associated with VR hardware and development, limited content availability, and technical issues such as latency. Additionally, the lack of standardization across devices and platforms poses barriers to widespread adoption.

03. Who are the major players in the Asia-Pacific VR market?

The major players include Sony Corporation, HTC Corporation, Oculus (Meta Platforms), Microsoft Corporation, and Unity Technologies. These companies dominate the market through a combination of hardware innovations, strong content portfolios, and strategic partnerships.

04. What are the growth drivers of the Asia-Pacific VR market?

Growth drivers include the integration of VR with emerging technologies such as AI and 5G, increased demand for VR applications in gaming and enterprise training, and strong government support for digital innovation.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.