Asia Pacific White Oil Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD5164

December 2024

90

About the Report

Asia Pacific White Oil Market Overview

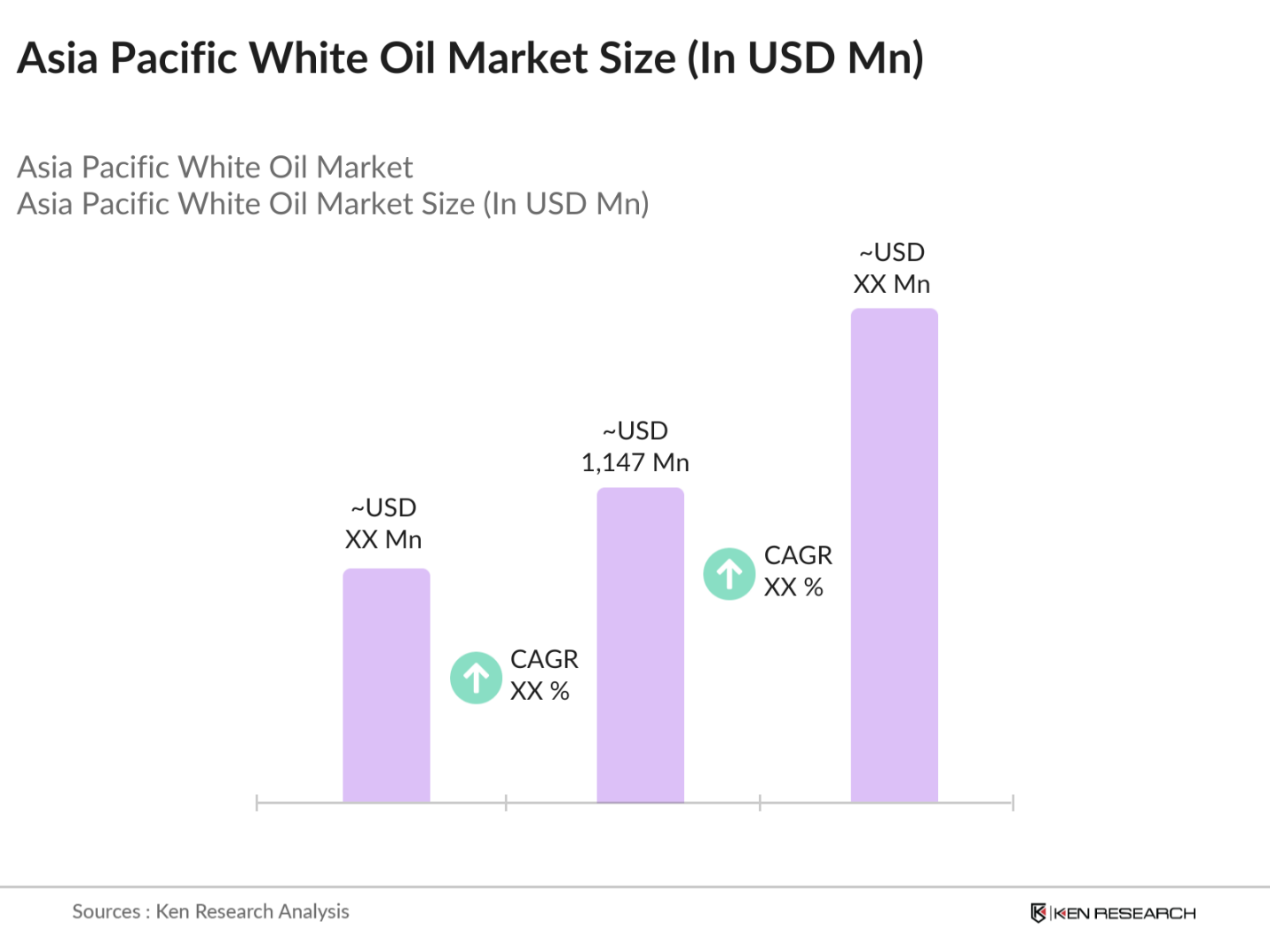

- The Asia Pacific White Oil market is valued at USD 1,147 million, based on a five-year historical analysis. This market is driven by increasing demand from the pharmaceutical, cosmetic, and food industries, where white oil is widely used as a base for products such as ointments, lotions, and food-grade lubricants. The rising focus on high-purity, safe ingredients, particularly in personal care and pharmaceutical applications, along with industrial growth in countries like China and India, further propels the market forward, enhancing the demand for high-quality white oil products.

- China and India dominate the Asia Pacific white oil market due to their large industrial base and robust demand from pharmaceutical, cosmetic, and personal care sectors. Chinas significant refining capacity and technological advancements in white oil production, coupled with Indias expanding pharmaceutical and food-grade white oil sectors, establish these nations as leaders in the market. The demand is concentrated in industrial hubs like Shanghai, Beijing, Mumbai, and Bangalore, where manufacturing and pharmaceutical industries are prevalent.

- Countries across Asia Pacific have specific import tariffs and export policies that impact the trade of white oil. In 2023, China imposed a 5% import tariff on petroleum-based products, including white oil, to protect its domestic oil industry. Similarly, India introduced export incentives to encourage the production and international trade of pharmaceutical-grade white oil.

Asia Pacific White Oil Market Segmentation

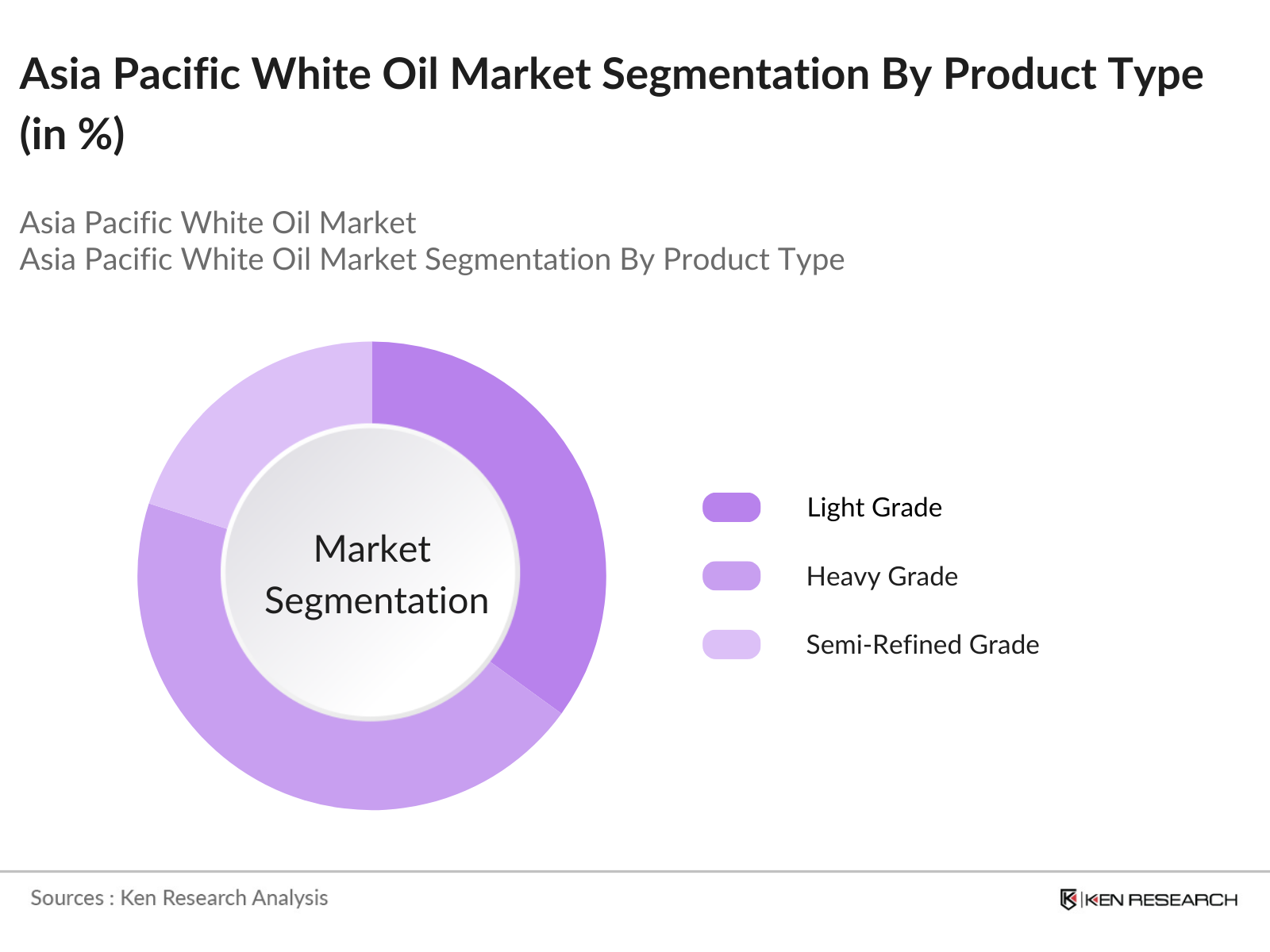

By Product Type: The market is segmented by product type into light-grade, heavy-grade, and semi-refined white oil. Heavy-grade white oil dominates the product type segmentation due to its widespread application in industries such as rubber and polymer manufacturing, where it is used as a lubricant and release agent. The consistency and stability of heavy-grade white oil make it ideal for these industries, particularly in China and India, where the production of rubber goods and plastics has been expanding rapidly in recent years.

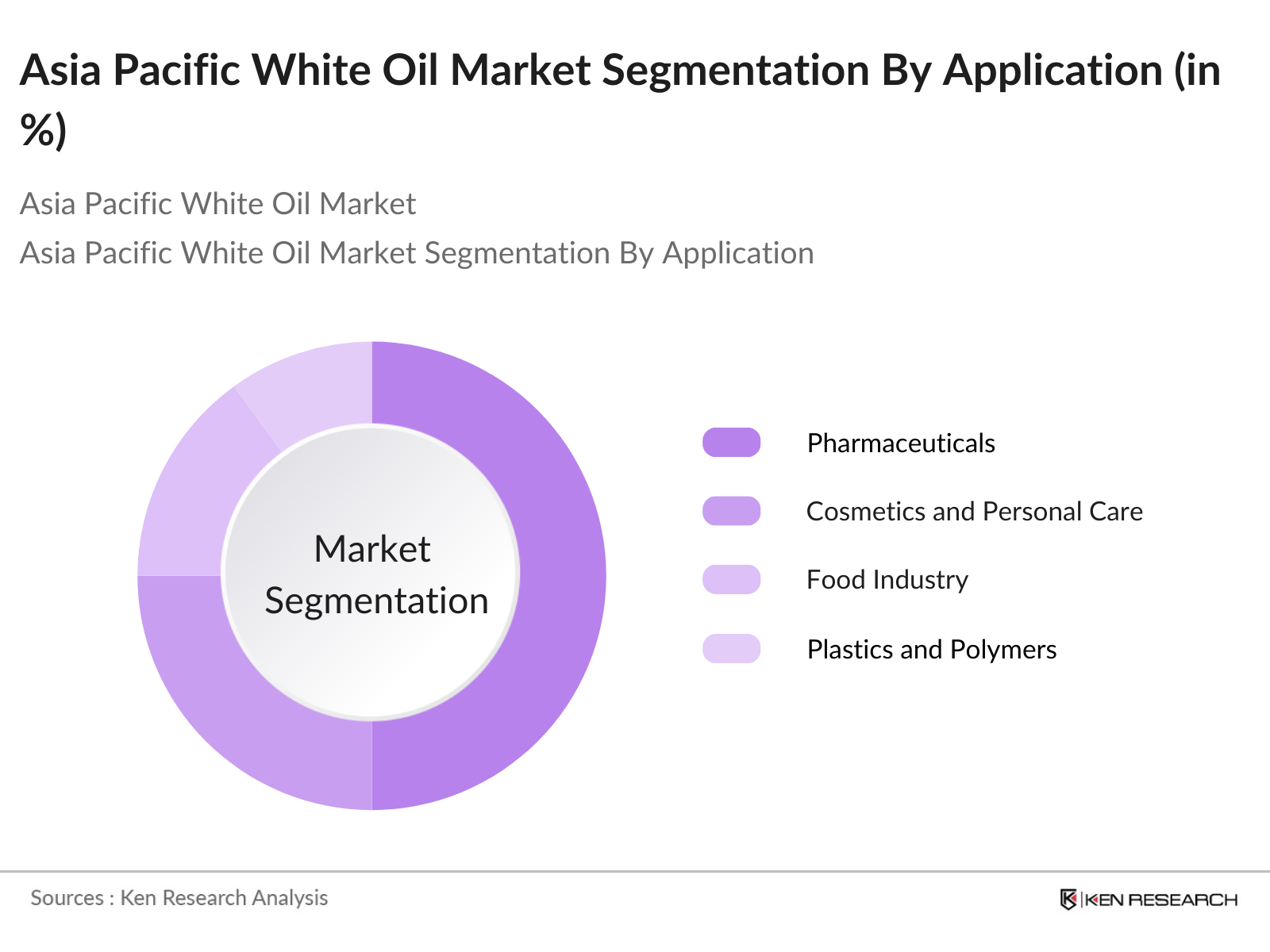

By Application: The market is also segmented by application into pharmaceuticals, cosmetics and personal care, food industry, plastics and polymers, and rubber processing. Pharmaceuticals lead this segment due to the high demand for white oil as a base for ointments, laxatives, and other medical products. The increasing population and growing healthcare sector in Asia Pacific countries, especially in India and China, drive the use of white oil in pharmaceutical formulations.

Asia Pacific White Oil Market Competitive Landscape

The Asia Pacific white oil market is dominated by both local and global players, with a few major companies leading the sector. These companies have established themselves through a combination of strong distribution networks, product quality, and technological advancements in oil refining processes. Multinational corporations like ExxonMobil and Royal Dutch Shell leverage their global presence and extensive research and development capabilities, while local players in Asia Pacific have strengthened their market positions through strategic partnerships and expanding production capacities.

Asia Pacific White Oil Industry Analysis

Growth Drivers

- Rising Demand from Personal Care Industry (Usage in skin care, hair care): The Asia Pacific personal care industry has seen a significant uptick in demand for white oil, driven by the increasing consumer focus on skincare and hair care products. In 2023, the region accounted for over 40% of global personal care product consumption, supported by countries like China, Japan, and India. White oil is widely used in moisturizing creams, lotions, and baby oils due to its non-comedogenic properties.

- Increasing Application in Pharmaceuticals (As a base for ointments, laxatives): The pharmaceutical industry in the Asia Pacific region heavily relies on white oil for its role as a base in ointments and laxatives. In 2023, pharmaceutical exports from India alone were valued at over USD 24 billion, demonstrating the growing need for pharmaceutical-grade white oils. Countries like China and South Korea also contribute to the pharmaceutical market's expansion, with the region's healthcare expenditure surpassing USD 1.3 trillion in 2024.

- Industrial Expansion in Emerging Markets (Use in rubber processing, polymer): Industrial growth across emerging economies like Indonesia, Vietnam, and Malaysia has resulted in a growing demand for white oil in rubber processing and polymer production. The manufacturing sector in Indonesia expanded by 5% in 2023, reaching a value of USD 270 billion. White oil is extensively used in these sectors as a release agent and lubricant.

Market Challenges

- Price Volatility in Feedstock (Crude oil dependency): White oil production is closely tied to the global crude oil market, making it susceptible to price volatility. Asia Pacific economies like Japan and South Korea, which heavily depend on crude oil imports, faced higher energy import costs, with crude oil prices averaging USD 80 per barrel in 2023. This dependency creates challenges for manufacturers as price fluctuations in crude oil directly impact the cost of white oil production, limiting profitability and increasing production costs for end-users.

- Stringent Regulatory Requirements (Purity standards, FDA regulations): Countries in Asia Pacific have implemented strict purity and safety standards for white oil, particularly in pharmaceuticals and food-grade products. For example, Japan and South Korea enforce stringent compliance with FDA standards, requiring white oils to meet high purity levels. The Japanese Ministry of Health, Labour and Welfare mandates white oil products to undergo rigorous testing to ensure they meet pharmaceutical-grade purity.

Asia Pacific White Oil Market Future Outlook

The Asia Pacific white oil market is expected to experience significant growth over the next five years. This expansion is driven by rising demand in the pharmaceutical, cosmetic, and food industries, particularly as consumer preferences shift toward high-quality, safe, and pure products. The growing trend toward clean-label cosmetics and personal care items, along with the stringent purity requirements in pharmaceutical applications, will continue to drive the adoption of white oil in the region.

Market Opportunities

- Rising Demand for Cosmetic and Personal Care Products (Clean label trend): Consumers across Asia Pacific are increasingly seeking personal care products with minimal chemical additives, driving the demand for highly purified white oil. In 2024, Japan's beauty industry was valued at USD 35 billion, with China and South Korea close behind. White oils role as a non-irritating, hypoallergenic base in clean label personal care products, such as lotions, creams, and baby oils, is expected to grow in line with consumer preferences for natural and safe ingredients.

- Adoption in Biodegradable and Renewable Products (Biodegradable oils): There is increasing adoption of biodegradable white oils in industrial applications across Asia Pacific. In 2023, Japan and South Korea introduced guidelines promoting the use of renewable and biodegradable products, aligning with their commitment to achieving net-zero emissions by 2050. This regulatory support has fueled research into sustainable alternatives, with companies exploring renewable feedstock for white oil production.

Scope of the Report

|

By Product Type |

Light Grade Heavy Grade Semi-Refined Grade |

|

By Application |

Pharmaceuticals Cosmetics and Personal Care Food Industry Plastics and Polymers Rubber Processing |

|

By End-Use Industry |

Medical, Automotive Industrial Food and Beverage Chemical Manufacturing |

|

By Grade |

Pharmaceutical Grade Industrial Grade Food-Grade |

|

By Region |

China India Japan South Korea Australia |

Products

Key Target Audience

Pharmaceutical Manufacturers

Cosmetic and Personal Care Product Manufacturers

Food-Grade Lubricant Manufacturers

Plastics and Polymer Manufacturers

Rubber Processing Industries

Automotive Component Manufacturers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Food and Drug Administration, Environmental Agencies)

Companies

Players Mentioned in the Report

ExxonMobil Corporation

Royal Dutch Shell

Sinopec Corporation

FUCHS Petrolub SE

Sasol Limited

TotalEnergies SE

Chevron Corporation

Sonneborn LLC

Nynas AB

Petro-Canada Lubricants

Table of Contents

1. Asia Pacific White Oil Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific White Oil Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific White Oil Market Analysis

3.1. Growth Drivers

3.1.1. Rising Demand from Personal Care Industry (Usage in skin care, hair care)

3.1.2. Increasing Application in Pharmaceuticals (As a base for ointments, laxatives)

3.1.3. Industrial Expansion in Emerging Markets (Use in rubber processing, polymer)

3.1.4. Expanding Food-Grade Oil Applications (Additive in packaging, food-grade lubricants)

3.2. Market Challenges

3.2.1. Price Volatility in Feedstock (Crude oil dependency)

3.2.2. Stringent Regulatory Requirements (Purity standards, FDA regulations)

3.2.3. Environmental Concerns (Sustainability of raw materials)

3.3. Opportunities

3.3.1. Rising Demand for Cosmetic and Personal Care Products (Clean label trend)

3.3.2. Adoption in Biodegradable and Renewable Products (Biodegradable oils)

3.3.3. Technological Advancements in Purification Processes (Hydrocracking, Catalytic Dewaxing)

3.4. Trends

3.4.1. Preference for Highly Refined White Oils (Pharmaceutical and cosmetic grades)

3.4.2. Shift Toward Natural and Organic Ingredients (Alternative sources of white oil)

3.4.3. Increasing Usage in Rubber and Plastics Manufacturing (Release agents, lubricants)

3.5. Government Regulations

3.5.1. Asia Pacific Standards for Food-Grade Oils (Food safety, chemical regulations)

3.5.2. Import Tariffs and Export Policies (Trade regulations)

3.5.3. Cosmetic Product Safety Guidelines (Country-specific compliance)

3.5.4. Regulatory Support for Pharmaceutical Applications (National health agencies approvals)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Asia Pacific White Oil Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Light Grade

4.1.2. Heavy Grade

4.1.3. Semi-Refined Grade

4.2. By Application (In Value %)

4.2.1. Pharmaceuticals

4.2.2. Cosmetics and Personal Care

4.2.3. Food Industry

4.2.4. Plastics and Polymers

4.2.5. Rubber Processing

4.3. By End-Use Industry (In Value %)

4.3.1. Medical

4.3.2. Automotive

4.3.3. Industrial

4.3.4. Food and Beverage

4.3.5. Chemical Manufacturing

4.4. By Grade (In Value %)

4.4.1. Pharmaceutical Grade

4.4.2. Industrial Grade

4.4.3. Food-Grade

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. South Korea

4.5.5. Australia

5. Asia Pacific White Oil Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ExxonMobil Corporation

5.1.2. Royal Dutch Shell

5.1.3. Sinopec Corporation

5.1.4. Sasol Limited

5.1.5. TotalEnergies SE

5.1.6. Chevron Corporation

5.1.7. FUCHS Petrolub SE

5.1.8. Sonneborn LLC

5.1.9. Nynas AB

5.1.10. Petro-Canada Lubricants

5.1.11. H&R Group

5.1.12. JX Nippon Oil & Energy

5.1.13. Calumet Specialty Products Partners, L.P.

5.1.14. Seojin Chemical Co. Ltd.

5.1.15. Savita Oil Technologies Limited

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Market Share, Product Portfolio, End-Use Coverage, Geographic Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6. Asia Pacific White Oil Market Regulatory Framework

6.1. Industry-Specific Purity Standards

6.2. Compliance with Environmental Regulations

6.3. Certification Processes for End-Use Applications

7. Asia Pacific White Oil Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific White Oil Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-Use Industry (In Value %)

8.4. By Grade (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific White Oil Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

This phase involved mapping all key stakeholders in the Asia Pacific white oil market, including pharmaceutical companies, cosmetic product manufacturers, and food-grade oil consumers. Extensive desk research was conducted using proprietary databases and public sources to gather relevant market information.

Step 2: Market Analysis and Construction

Data from the last five years were analyzed to understand market penetration, white oil usage across various industries, and related revenue trends. Information on product performance was gathered through consultations with industry players to ensure the reliability of projections.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed based on historical data and then validated through interviews with industry experts from leading white oil manufacturers. These insights helped refine the market forecasts and provided practical insights into emerging trends and opportunities.

Step 4: Research Synthesis and Final Output

The final report synthesizes data from both primary and secondary research, validated through interactions with major manufacturers. The result is a comprehensive view of the Asia Pacific white oil market, providing accurate and actionable insights.

Frequently Asked Questions

01. How big is the Asia Pacific White Oil Market?

The Asia Pacific White Oil market is valued at USD 1,147 million, based on a five-year historical analysis. This market is driven by increasing demand from the pharmaceutical, cosmetic, and food industries, where white oil is widely used as a base for products such as ointments, lotions, and food-grade lubricants.

02. What are the major growth drivers for the Asia Pacific White Oil Market?

Key growth drivers include the rising demand for white oil in personal care and pharmaceutical applications, along with advancements in refining technologies that ensure high-quality, pure oils suitable for sensitive applications.

03. Who are the major players in the Asia Pacific White Oil Market?

Major players include ExxonMobil Corporation, Royal Dutch Shell, Sinopec Corporation, FUCHS Petrolub SE, and Sasol Limited, which dominate the market due to their extensive distribution networks and technological advancements.

04. What are the challenges in the Asia Pacific White Oil Market?

Challenges include price volatility in raw materials (crude oil), stringent regulatory requirements for purity, and the increasing focus on sustainability, which pressures manufacturers to adopt more eco-friendly practices.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.