Asia Pacific Wine Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD8691

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD8691

December 2024

88

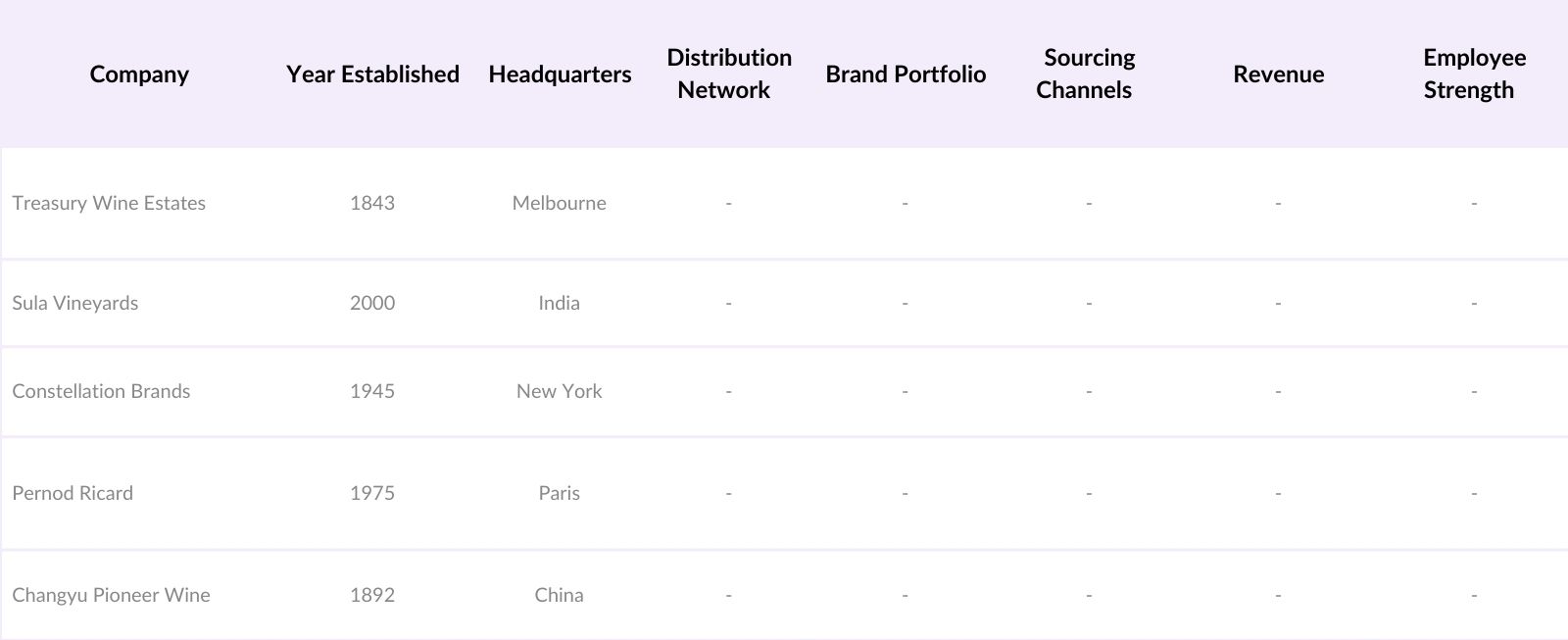

The Asia Pacific Wine Market is dominated by prominent companies, each leveraging a mix of local market knowledge and international standards to gain a competitive edge. The following table provides insights into five major players, their establishment year, headquarters, and market-specific parameters.

Over the next five years, the Asia Pacific Wine Market is expected to see considerable advancements, fueled by growing consumer interest in premium alcoholic beverages, the rise of e-commerce platforms, and evolving taste preferences. Investments in sustainable wine production and innovation across wine varieties will further shape the market, especially as brands expand their footprint in emerging regional markets.

|

Type |

Still Wines Sparkling Wines |

|

Distribution Channel |

Supermarkets/Hypermarkets Specialty Stores Online Retail |

|

Packaging |

Glass Bottles Bag-in-Box Tetra Packs |

|

Price Segment |

Premium Economy |

|

Country |

China Japan Australia India South Korea |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Consumer Preferences (Shift toward Premium Wines)

3.1.2 Increasing Disposable Income

3.1.3 Influence of Western Culture

3.1.4 Demand for Low-ABV (Alcohol by Volume) Products

3.2 Market Challenges

3.2.1 Regulatory Constraints (Alcohol Distribution Laws)

3.2.2 Competitive Pressure from Imported Brands

3.2.3 High Cost of Imported Wines

3.3 Opportunities

3.3.1 Expansion into Emerging Markets

3.3.2 Organic and Biodynamic Wine Production

3.3.3 Potential in Online Wine Sales

3.4 Trends

3.4.1 Rise of E-commerce in Wine Sales

3.4.2 Growing Wine Tourism

3.4.3 Increased Adoption of Wine Subscriptions

3.5 Government Regulations

3.5.1 Wine Labeling Standards

3.5.2 Import-Export Regulations

3.5.3 Health and Safety Guidelines

3.5.4 Promotional and Advertising Restrictions

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

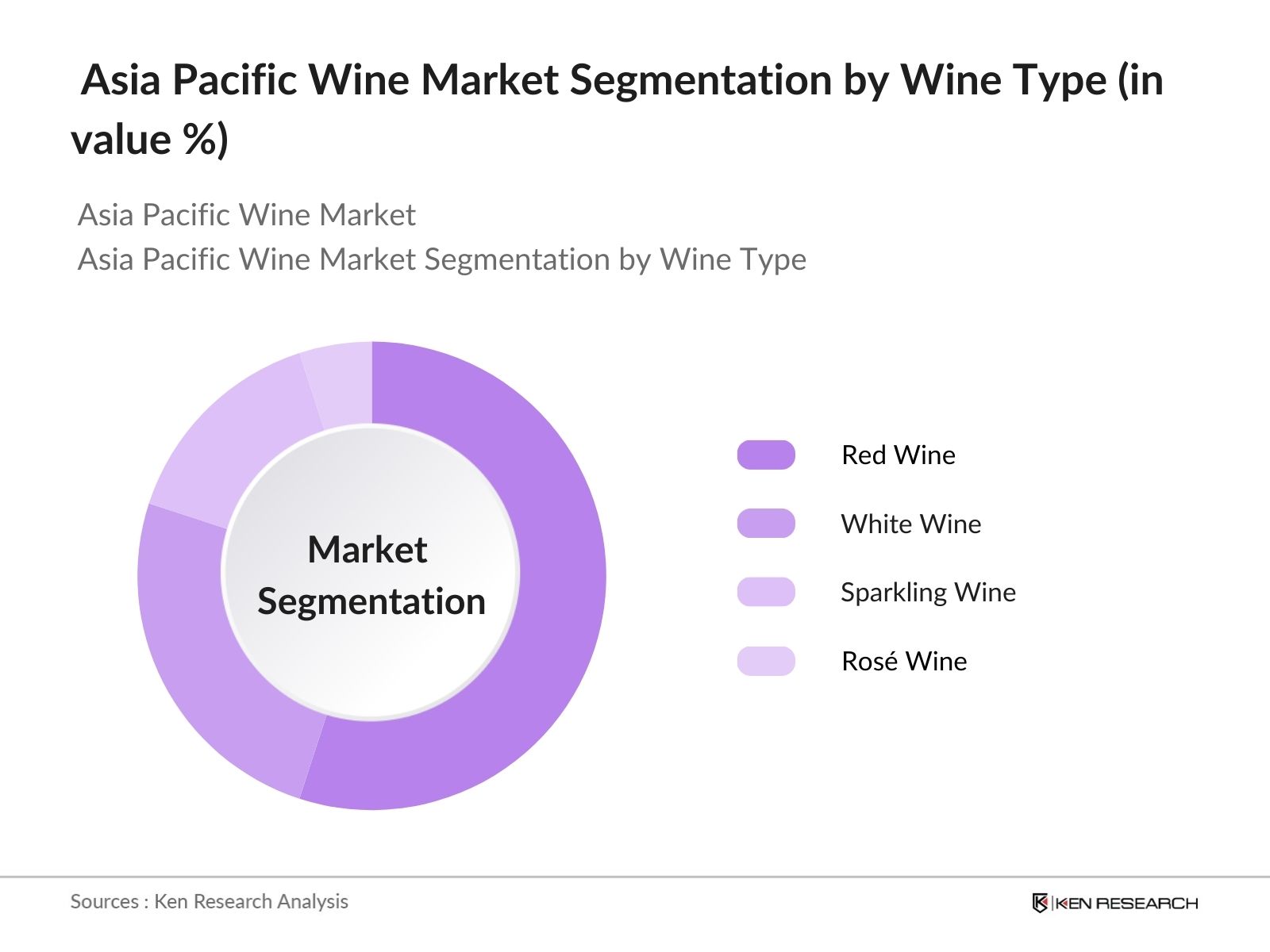

4.1 By Type (In Value %)

4.1.1 Still Wines

4.1.2 Sparkling Wines

4.1.3 Fortified Wines

4.1.4 Dessert Wines

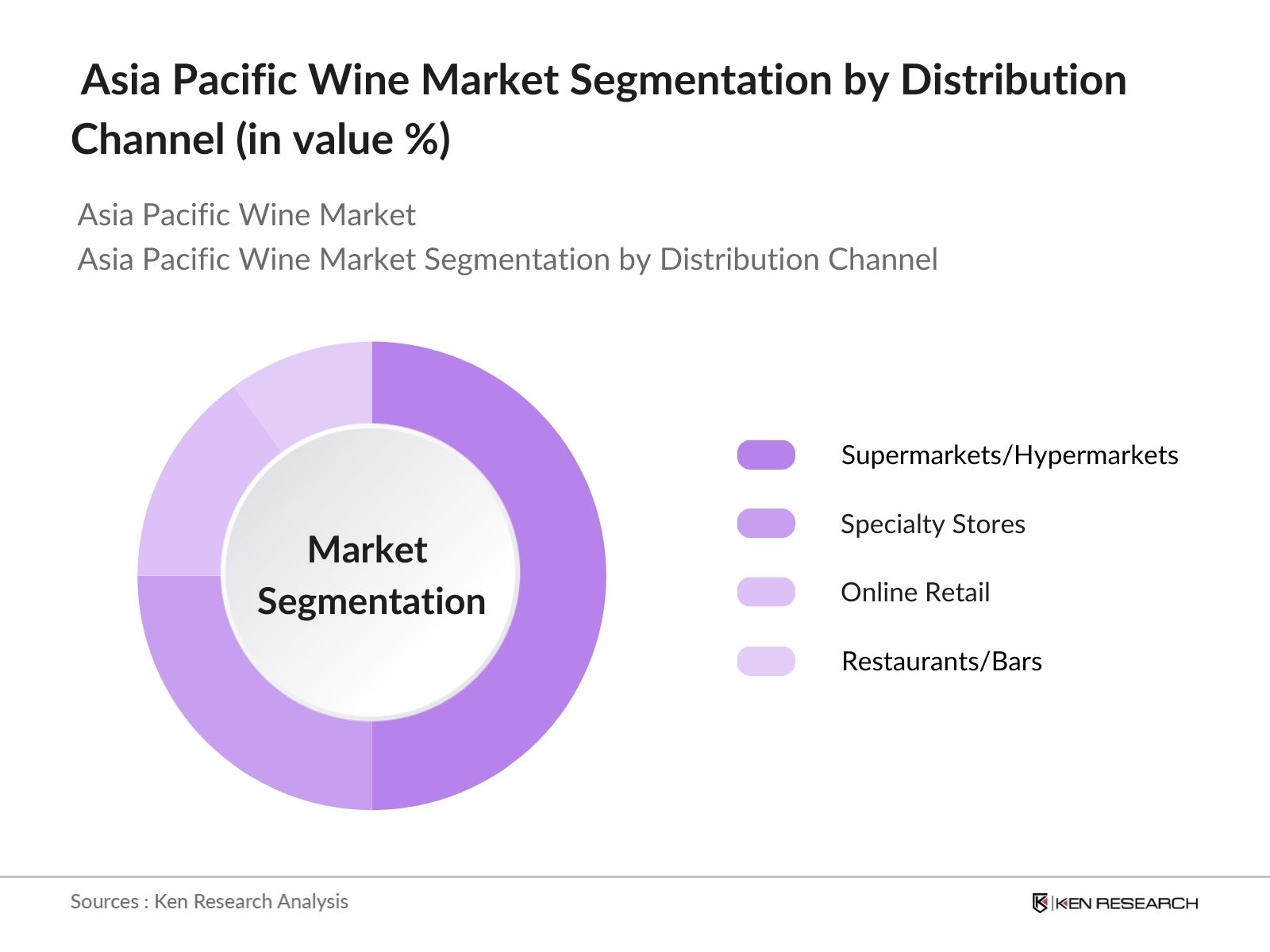

4.2 By Distribution Channel (In Value %)

4.2.1 Supermarkets/Hypermarkets

4.2.2 Specialty Stores

4.2.3 Online Retail

4.2.4 Hotels, Restaurants, and Cafs (HoReCa)

4.3 By Packaging (In Value %)

4.3.1 Glass Bottles

4.3.2 Bag-in-Box

4.3.3 Tetra Packs

4.3.4 Cans

4.4 By Price Segment (In Value %)

4.4.1 Premium

4.4.2 Mid-Range

4.4.3 Economy

4.5 By Country (In Value %)

4.5.1 China

4.5.2 Japan

4.5.3 Australia

4.5.4 India

4.5.5 South Korea

5.1 Detailed Profiles of Major Companies

5.1.1 Treasury Wine Estates

5.1.2 Accolade Wines

5.1.3 Casella Wines

5.1.4 Changyu Pioneer Wine

5.1.5 Sula Vineyards

5.1.6 Pernod Ricard

5.1.7 Diageo

5.1.8 Constellation Brands

5.1.9 Yantai North Andre Juice

5.1.10 Great Wall Wine

5.1.11 Thai Beverage

5.1.12 Yanghe Brewery

5.1.13 Kingfisher Boissons

5.1.14 Kweichow Moutai

5.1.15 Asahi Group

5.2 Cross Comparison Parameters

5.2.1 Number of Employees

5.2.2 Headquarters

5.2.3 Inception Year

5.2.4 Revenue

5.2.5 Market Share

5.2.6 Annual Growth Rate

5.2.7 Distribution Network

5.2.8 Product Portfolio

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Environmental Standards

6.2 Compliance Requirements

6.3 Certification Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Type (In Value %)

8.2 By Distribution Channel (In Value %)

8.3 By Packaging (In Value %)

8.4 By Price Segment (In Value %)

8.5 By Country (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsThe research begins with the development of a comprehensive ecosystem model covering all stakeholders in the Asia Pacific Wine Market. This step involves gathering primary data from industry sources and building a database to identify the most influential variables in the market.

Next, historical data is analyzed, focusing on consumer patterns, retail channel distribution, and wine consumption trends. Additional assessments are conducted on distribution efficiency and market penetration to ensure robust analysis.

To validate market hypotheses, expert consultations are conducted with industry veterans and wine market analysts. These interactions help confirm key insights and fill gaps in data collected, leading to a refined and comprehensive understanding.

The synthesis phase consolidates findings from primary research, statistical analyses, and expert input to produce a final report. This output includes segmented insights, detailed market metrics, and validated data covering the Asia Pacific Wine Market.

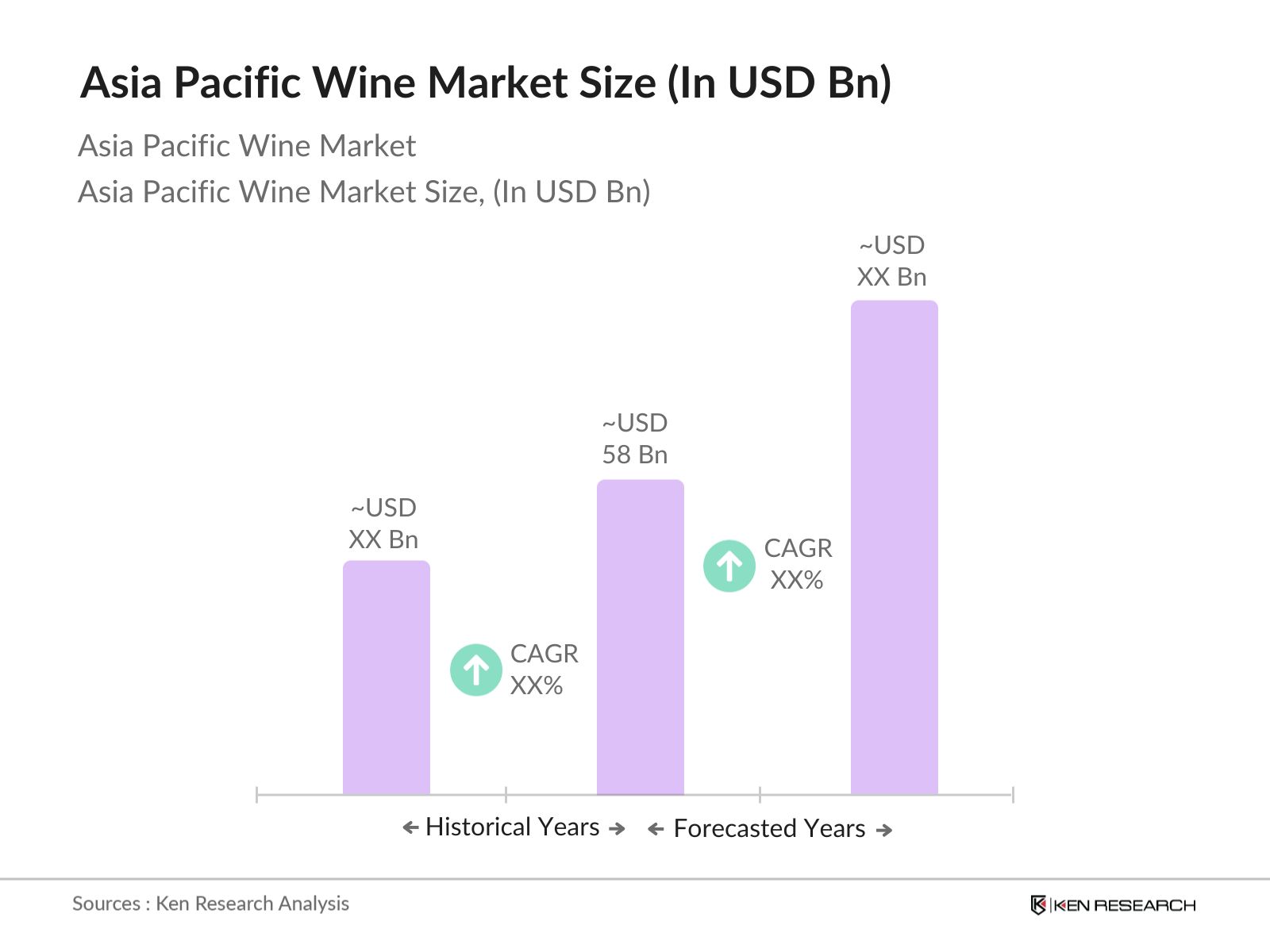

The Asia Pacific Wine Market is valued at USD 58 billion, supported by increasing demand for premium wines and expanded distribution networks across major countries.

Challenges include complex regulatory frameworks, high import tariffs in some countries, and logistical hurdles due to the fragmented nature of the region's distribution systems.

Leading players include Treasury Wine Estates, Sula Vineyards, Pernod Ricard, Constellation Brands, and Changyu Pioneer Wine, known for their extensive reach and diverse portfolios.

Growth is primarily driven by increasing consumer interest in wine culture, rising disposable income, and the popularity of wine tourism, especially in China, Japan, and Australia.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.