Australia Aluminum Facade Market Outlook to 2030

Region:Asia

Author(s):Sanjeev

Product Code:KROD2619

Region:Asia

Author(s):Sanjeev

Product Code:KROD2619

November 2024

83

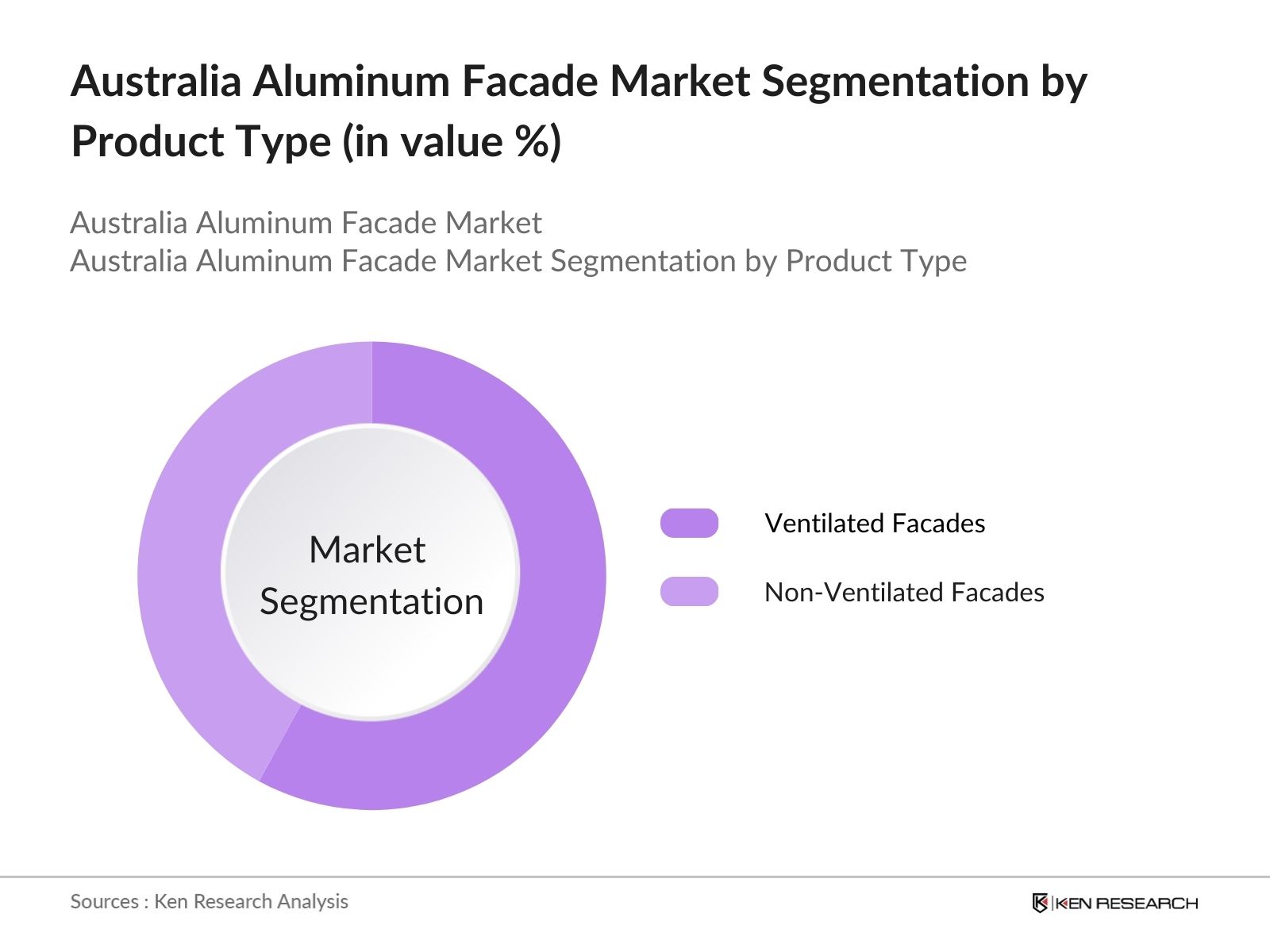

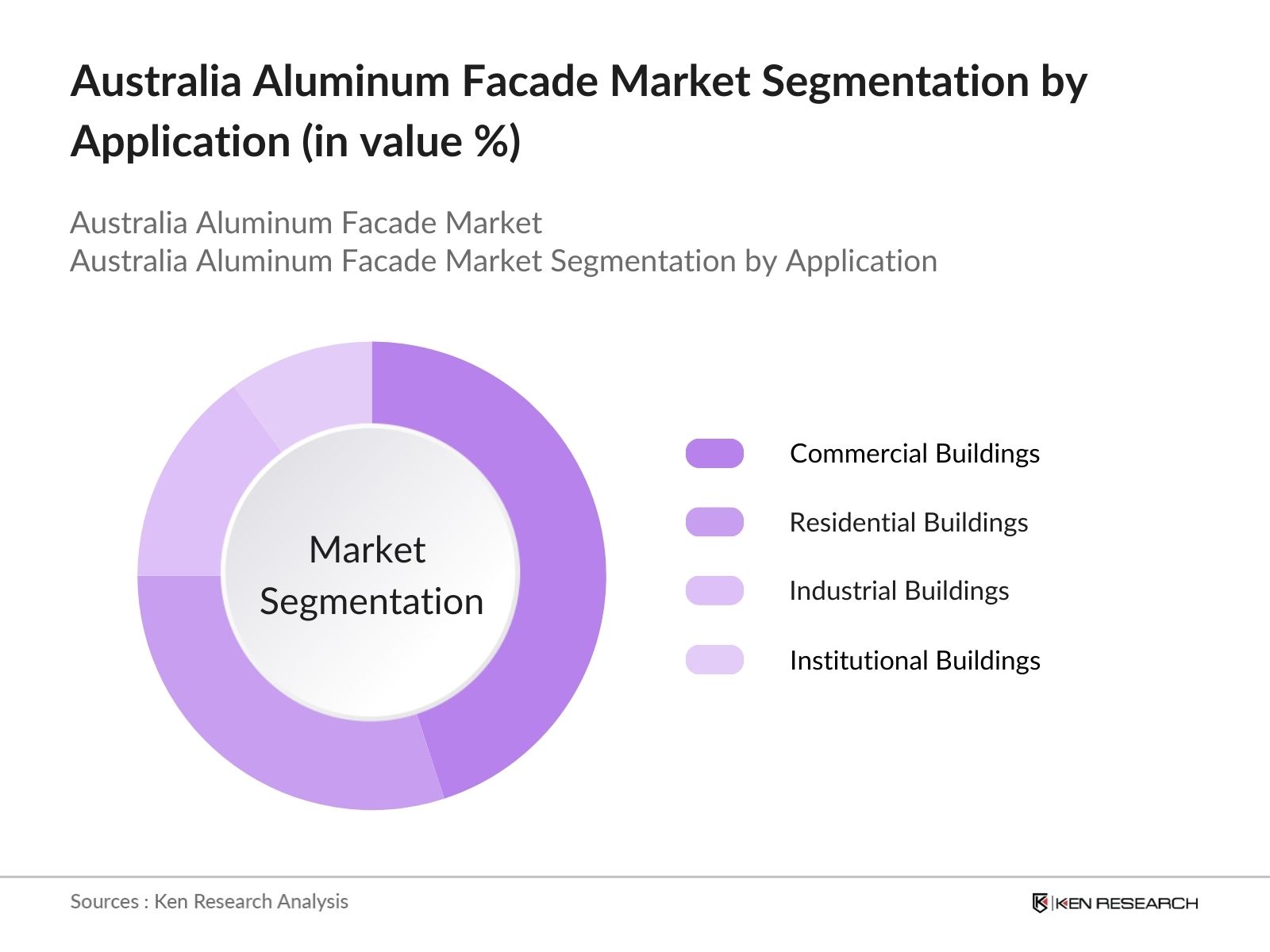

The Australia Aluminum Facade Market is segmented by product type and by application.

The Australia Aluminum Facade Market is dominated by several key players, both local and global, which highlights the competitive landscape within this market. The consolidation of these companies underscores their market influence through innovation, extensive product portfolios, and robust supply chains.

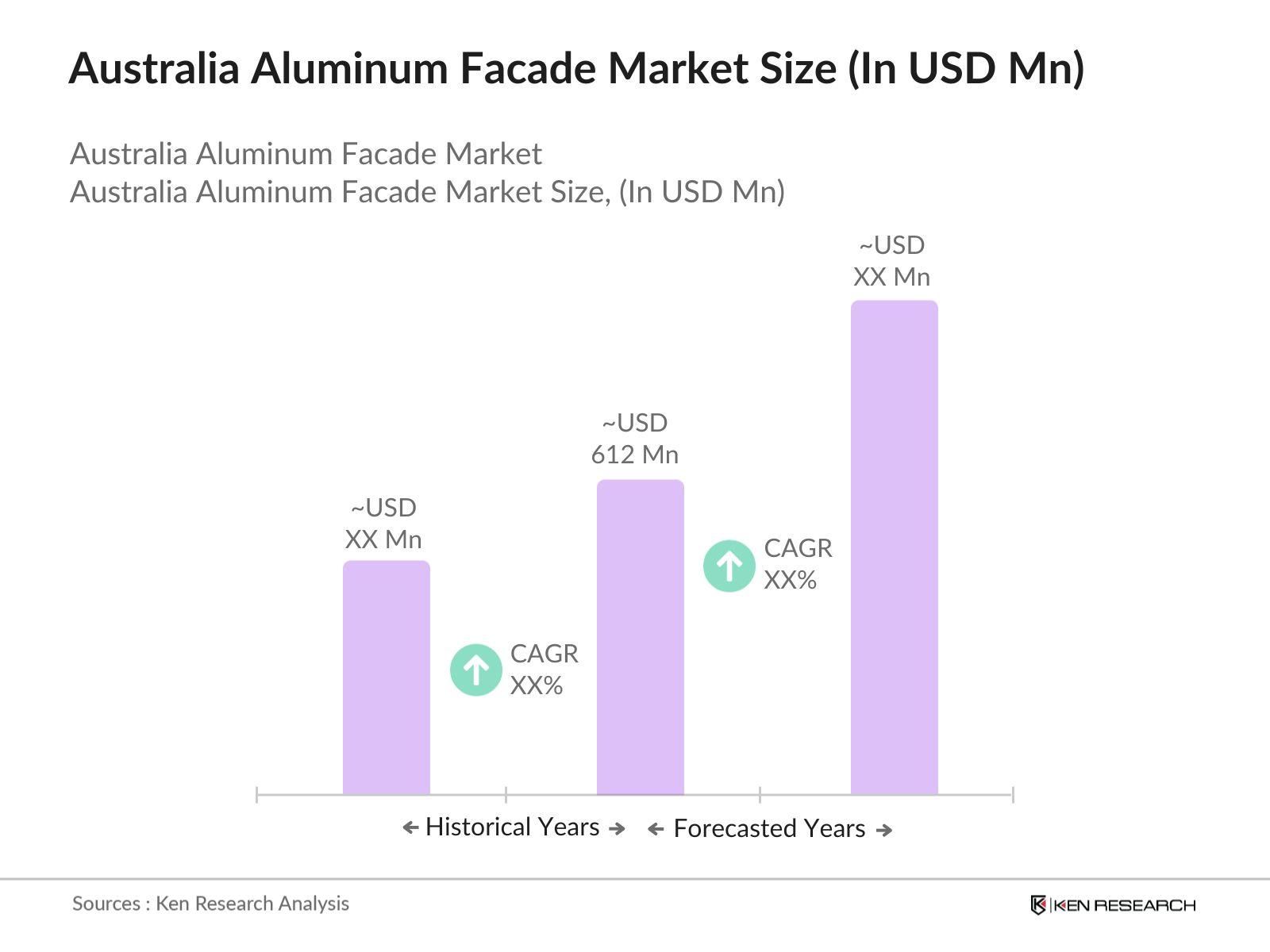

Over the next several years, the Australia Aluminum Facade Market is anticipated to experience substantial growth. This outlook is driven by factors such as government incentives for sustainable building materials, advances in facade technology, and a heightened awareness of environmental impact in construction. The ongoing urban expansion, particularly in Australias major cities, will likely sustain the demand for durable and energy-efficient aluminum facade systems.

|

Ventilated Facades Non-Ventilated Facades |

|

|

By Material |

Aluminum Composite Panels |

|

By Application |

Commercial Buildings |

|

By Installation Type |

New Construction |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Urbanization and Infrastructure Development

3.1.2 Advancements in Aluminum Facade Technologies

3.1.3 Emphasis on Energy Efficiency and Sustainability

3.1.4 Government Initiatives and Regulations

3.2 Market Challenges

3.2.1 High Initial Investment Costs

3.2.2 Fluctuations in Aluminum Prices

3.2.3 Technical Challenges in Installation and Maintenance

3.3 Opportunities

3.3.1 Technological Innovations in Facade Systems

3.3.2 Expansion into Emerging Urban Areas

3.3.3 Integration with Smart Building Technologies

3.4 Trends

3.4.1 Adoption of Modular Facade Systems

3.4.2 Use of Recyclable and Eco-Friendly Materials

3.4.3 Increased Demand for Customizable Facade Designs

3.5 Government Regulations

3.5.1 Building Code of Australia (BCA) Compliance

3.5.2 Energy Efficiency Standards

3.5.3 Fire Safety Regulations

3.5.4 Environmental Sustainability Guidelines

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4.1 By Product Type (In Value %)

4.1.1 Ventilated Facades

4.1.2 Non-Ventilated Facades

4.1.3 Others

4.2 By Material (In Value %)

4.2.1 Aluminum Composite Panels

4.2.2 Solid Aluminum Panels

4.2.3 Aluminum Mesh Panels

4.2.4 Others

4.3 By Application (In Value %)

4.3.1 Commercial Buildings

4.3.2 Residential Buildings

4.3.3 Industrial Buildings

4.3.4 Institutional Buildings

4.4 By Installation Type (In Value %)

4.4.1 New Construction

4.4.2 Renovation and Retrofit

4.5 By Region (In Value %)

4.5.1 New South Wales

4.5.2 Victoria

4.5.3 Queensland

4.5.4 Western Australia

4.5.5 South Australia

4.5.6 Tasmania

4.5.7 Australian Capital Territory

4.5.8 Northern Territory

6.1 Detailed Profiles of Major Companies

6.1.1 Alucobond Australia

6.1.2 Fairview Architectural

6.1.3 Ullrich Aluminium

6.1.4 Alspec

6.1.5 JWI Aluminum

6.1.6 Hunter Douglas

6.1.7 Kingspan Insulated Panels

6.1.8 BlueScope Steel Limited

6.1.9 CSR Limited

6.1.10 Capral Aluminium

6.1.11 G.James Glass & Aluminium

6.1.12 Viridian Glass

6.1.13 Austral Wright Metals

6.1.14 Locker Group

6.1.15 Revolution Roofing

6.2 Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Market Share, Regional Presence, Strategic Initiatives)

6.3 Market Share Analysis

6.4 Strategic Initiatives

6.5 Mergers and Acquisitions

6.6 Investment Analysis

6.7 Venture Capital Funding

6.8 Government Grants

6.9 Private Equity Investments

7.1 Building Code of Australia (BCA) Standards

7.2 Compliance Requirements

7.3 Certification Processes

8.1 Future Market Size Projections

8.2 Key Factors Driving Future Market Growth

9.1 By Product Type (In Value %)

9.2 By Material (In Value %)

9.3 By Application (In Value %)

9.4 By Installation Type (In Value %)

9.5 By Region (In Value %)

10.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

10.2 Customer Cohort Analysis

10.3 Marketing Initiatives

10.4 White Space Opportunity Analysis

The initial phase involves identifying the major stakeholders within the Australia Aluminum Facade Market. This stage entails comprehensive desk research using trusted secondary and proprietary databases to map market influencers, focusing on sustainable construction and facade innovations.

This step incorporates collecting historical data on aluminum facade demand, application distribution, and regional uptake. By evaluating market penetration and facade adoption trends, this phase ensures the accuracy and relevance of revenue estimates for the market.

Market hypotheses are formulated based on the data collected and validated through expert interviews with aluminum facade manufacturers and construction industry specialists. This process gathers insights on operational trends and market challenges from industry practitioners.

The final phase involves integrating findings from multiple data sources to develop a cohesive market report. This includes direct engagement with facade solution providers to refine segmentation and validate the analysis, ensuring a comprehensive view of the Australia Aluminum Facade Market.

The Australia Aluminum Facade Market was valued at approximately USD 612 million, largely propelled by urban development projects and a focus on sustainability within the construction sector.

Challenges include in Australia Aluminum Facade Market are fluctuating aluminum prices, high initial costs associated with facade installations, and the need for skilled installation professionals to maintain technical standards in large projects.

Key players in Australia Aluminum Facade Market include Alucobond Australia, Fairview Architectural, Ullrich Aluminium, Alspec, and Hunter Douglas, with these companies leveraging product innovation and strong distribution networks.

Australia Aluminum Facade Market Growth is driven by urban expansion, government incentives for sustainable materials, and advances in facade technologies that support energy efficiency in construction.

Aluminum facades are primarily used in commercial and residential buildings, with a growing presence in industrial and institutional buildings due to their durability and design flexibility.

Yes, aluminum facades contribute to sustainable construction by providing energy-efficient insulation and enabling the use of recyclable materials, aligning with environmental goals in Australia.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.