Australia Data Center Colocation Market Outlook to 2030

Region:Australia

Author(s):Sanjeev

Product Code:KROD4096

Region:Australia

Author(s):Sanjeev

Product Code:KROD4096

November 2024

94

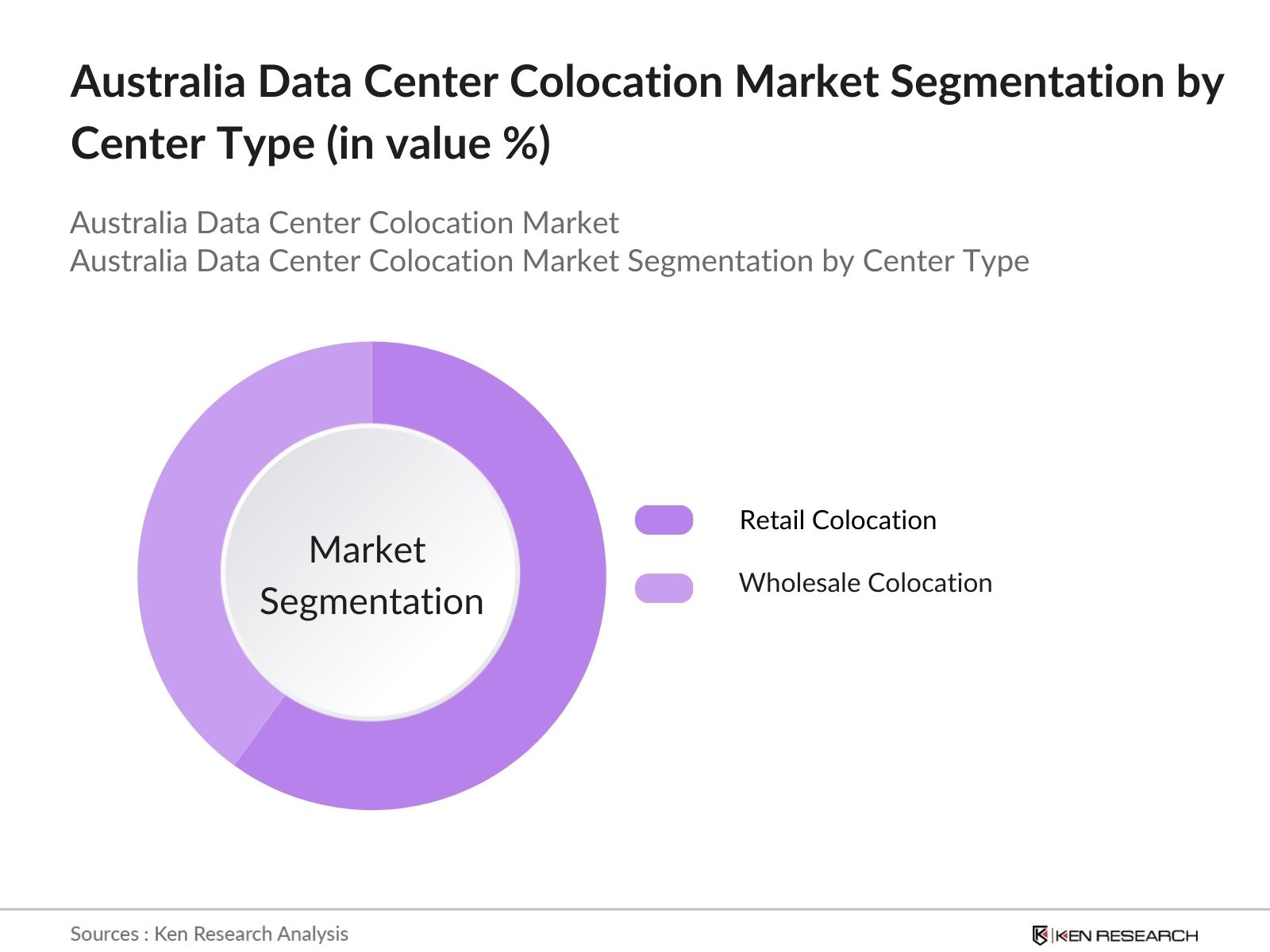

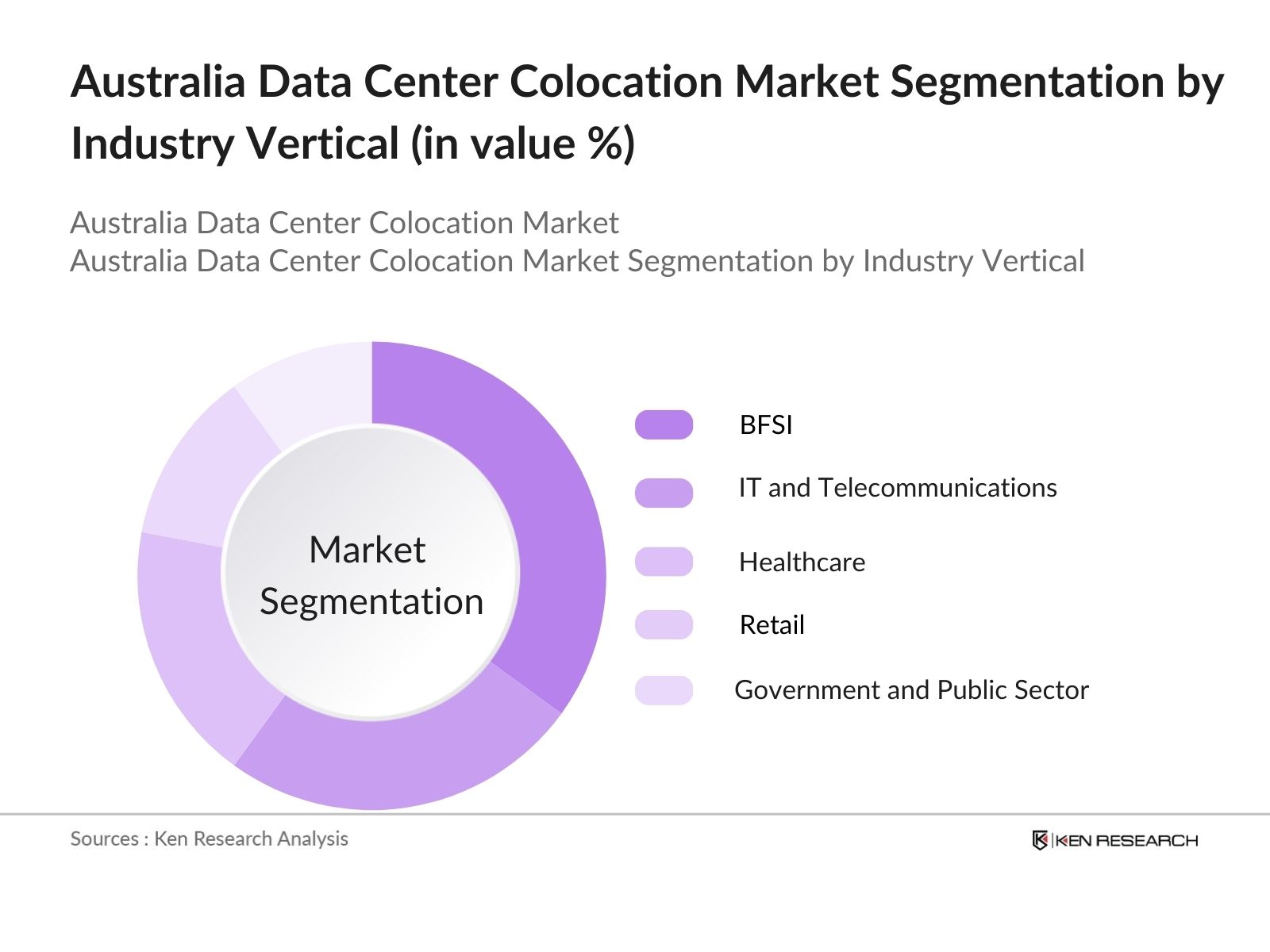

The Australia Data Center Colocation Market is segmented by center type and by industry vertical.

The Australia Data Center Colocation Market is characterized by the presence of several key players offering advanced infrastructure and tailored services. These companies emphasize sustainability, strategic partnerships, and scalability to meet the evolving demands of the digital economy. Below is an overview of five major players in the market:

|

Company Name |

Year Established |

Headquarters Location |

Data Center Capacity (MW) |

Number of Facilities |

Revenue (USD Billion) |

Key Clients |

|---|---|---|---|---|---|---|

|

Equinix, Inc. |

1998 |

Sydney, Australia |

||||

|

NEXTDC Ltd |

2010 |

Brisbane, Australia |

||||

|

Digital Realty Trust Inc. |

2004 |

Melbourne, Australia |

||||

|

Macquarie Telecom Group |

1992 |

Sydney, Australia |

||||

|

AirTrunk Pty Ltd |

2016 |

Sydney, Australia |

The Australia Data Center Colocation Market is set to witness substantial growth driven by continued digital transformation, the proliferation of IoT devices, and demand for energy-efficient solutions. Government policies supporting green energy integration and advanced technologies like edge computing are expected to propel the market further. Companies investing in hyperscale data centers and regional expansions will remain at the forefront of market growth.

|

Retail Colocation Wholesale Colocation |

|

|

By Enterprise Size |

Small and Medium-Sized Enterprises (SMEs) |

|

By Industry Vertical |

Information Technology (IT) and Telecommunications |

|

By Tier Standard |

Tier I & II |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Digital Transformation Initiatives

3.1.2 Cloud Adoption

3.1.3 Data Sovereignty Regulations

3.1.4 Expansion of IoT and AI Applications

3.2 Market Challenges

3.2.1 High Operational Costs

3.2.2 Energy Consumption Concerns

3.2.3 Limited Skilled Workforce

3.2.4 Regulatory Compliance

3.3 Opportunities

3.3.1 Green Data Center Initiatives

3.3.2 Edge Computing Expansion

3.3.3 Strategic Partnerships and Mergers

3.3.4 Government Incentives

3.4 Trends

3.4.1 Adoption of Hyperscale Data Centers

3.4.2 Integration of Renewable Energy Sources

3.4.3 Enhanced Security Measures

3.4.4 Deployment of Advanced Cooling Technologies

3.5 Government Regulations

3.5.1 Data Privacy Laws

3.5.2 Energy Efficiency Standards

3.5.3 Telecommunications Regulations

3.5.4 Environmental Compliance

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porter's Five Forces Analysis

3.9 Competitive Landscape

4.1 By Type (Value %)

4.1.1 Retail Colocation

4.1.2 Wholesale Colocation

4.2 By Enterprise Size (Value %)

4.2.1 Small and Medium-Sized Enterprises (SMEs)

4.2.2 Large Enterprises

4.3 By Industry Vertical (Value %)

4.3.1 Information Technology (IT) and Telecommunications

4.3.2 Banking, Financial Services, and Insurance (BFSI)

4.3.3 Healthcare

4.3.4 Retail

4.3.5 Government and Public Sector

4.3.6 Others

4.4 By Tier Standard (Value %)

4.4.1 Tier I & II

4.4.2 Tier III

4.4.3 Tier IV

4.5 By Region (Value %)

4.5.1 New South Wales

4.5.2 Victoria

4.5.3 Queensland

4.5.4 Western Australia

4.5.5 South Australia

4.5.6 Tasmania

4.5.7 Northern Territory

4.5.8 Australian Capital Territory

5.1 Detailed Profiles of Major Companies

5.1.1 Equinix, Inc.

5.1.2 Macquarie Telecom Group Ltd

5.1.3 Digital Realty Trust Inc.

5.1.4 Keppel Data Centres Pte Ltd

5.1.5 Servers Australia Pty Ltd

5.1.6 Zenlayer Inc.

5.1.7 Global Switch Ltd

5.1.8 Rackspace Technology Inc.

5.1.9 NEXTDC Ltd

5.1.10 Fujitsu Australia Ltd

5.1.11 AirTrunk Operating Pty Ltd

5.1.12 Vocus Group Ltd

5.1.13 Canberra Data Centres

5.1.14 DXN Limited

5.1.15 iseek Communications Pty Ltd

5.2 Cross-Comparison Parameters

5.3 Number of Employees

5.4 Headquarters Location

5.5 Year of Establishment

5.6 Revenue

5.7 Data Center Capacity (MW)

5.8 Number of Data Center Facilities

5.9 Service Offerings

5.10 Key Clients

5.11 Market Share Analysis

5.12 Strategic Initiatives

5.13 Mergers and Acquisitions

5.14 Investment Analysis

5.15 Venture Capital Funding

5.16 Government Grants

5.17 Private Equity Investments

6.1 Data Protection and Privacy Regulations

6.2 Energy Efficiency and Sustainability Standards

6.3 Telecommunications and Network Compliance

6.4 Environmental Impact Assessments

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Type (Value %)

8.2 By Enterprise Size (Value %)

8.3 By Industry Vertical (Value %)

8.4 By Tier Standard (Value %)

8.5 By Region (Value %)

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The research began by mapping the ecosystem of the Australia Data Center Colocation Market, involving all major stakeholders such as colocation providers, end-users, and regulatory bodies. Comprehensive desk research was conducted using secondary sources like industry reports, white papers, and proprietary databases to identify the critical variables influencing market dynamics, such as market size, growth drivers, challenges, and segmentation.

This phase involved compiling historical data to understand market penetration and revenue generation trends. Parameters such as the ratio of retail to wholesale colocation adoption, industry vertical demand, and regional capacities were evaluated. This ensured the development of a well-structured and reliable market model, accurately reflecting the markets current state.

The hypotheses developed from desk research were validated through interviews with industry experts, including data center operators, IT specialists, and regulatory consultants. These consultations provided actionable insights on operational efficiencies, customer demands, and technology adoption trends. Expert feedback was instrumental in corroborating and refining market estimates.

The final phase synthesized insights from secondary research, market analysis, and expert consultations to develop a comprehensive report. Direct engagement with leading colocation providers provided additional data on service offerings, client segmentation, and technological innovations. The report was further verified through a bottom-up approach to ensure accuracy and reliability.

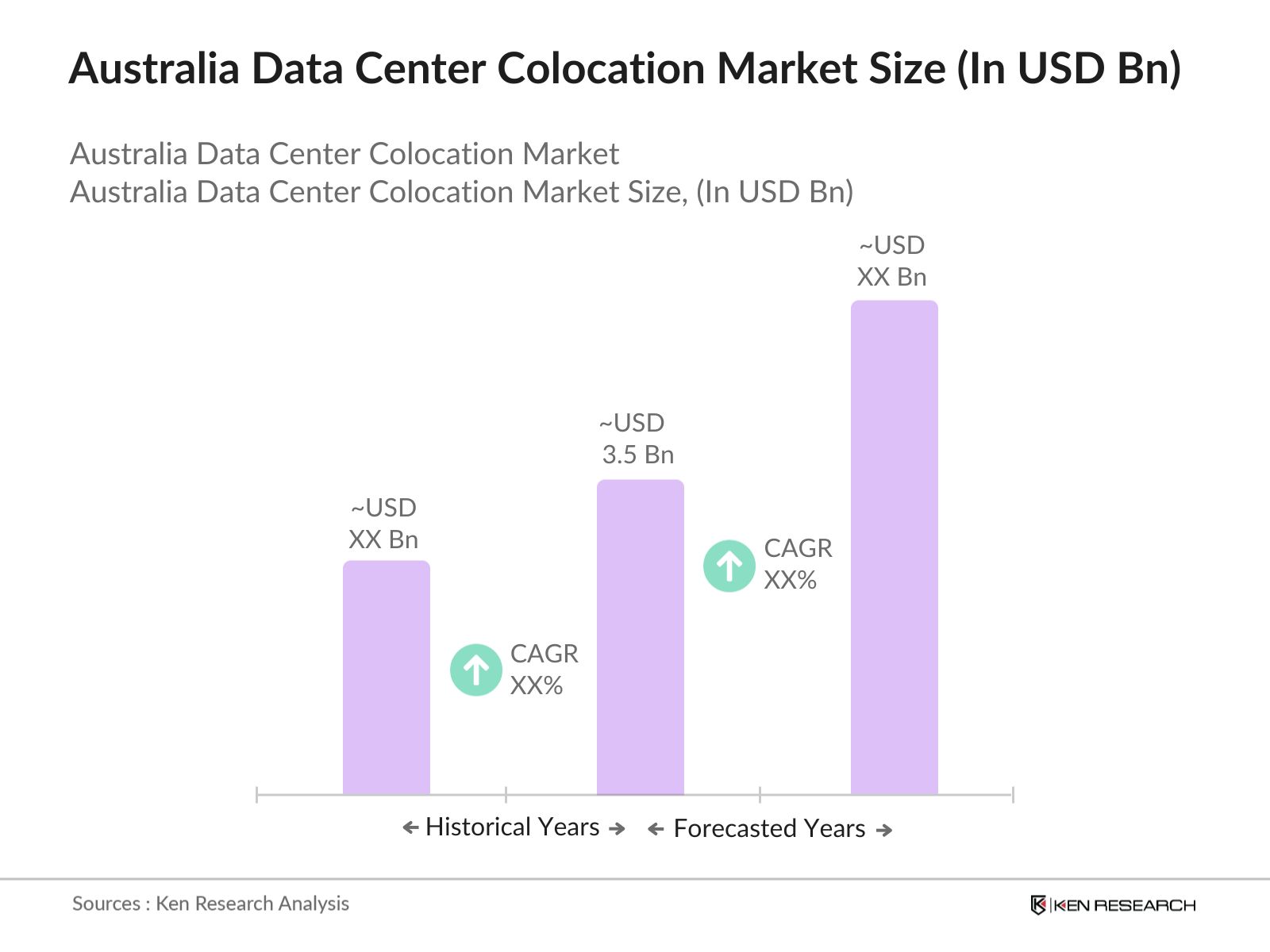

The Australia Data Center Colocation Market is valued at USD 3.5 billion, driven by the rising demand for cloud services, digital transformation, and robust IT infrastructure across industries.

Challenges include high operational costs, stringent regulatory requirements, and energy consumption concerns. Limited availability of skilled workforce also poses a significant barrier to market growth.

Key players include Equinix, NEXTDC, Digital Realty Trust, Macquarie Telecom, and AirTrunk. These companies dominate due to advanced infrastructure, scalability, and sustainability initiatives.

The demand is driven by factors like the proliferation of IoT, data sovereignty laws, the need for low-latency connectivity, and the increasing adoption of edge computing solutions.

Prominent trends include the integration of renewable energy, adoption of hyperscale data centers, and advancements in cooling technologies such as liquid cooling for energy efficiency.

The BFSI segment dominates the market due to stringent data protection regulations and the need for secure, scalable colocation facilities for disaster recovery and uptime assurance.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.