Australia E-Commerce Logistics Market Outlook to 2029

Region:Asia

Author(s):Aditi Tewari, Ananiya Bansal and Rajat Goyal

Product Code:KR1483

Region:Asia

Author(s):Aditi Tewari, Ananiya Bansal and Rajat Goyal

Product Code:KR1483

April 2025

80-100

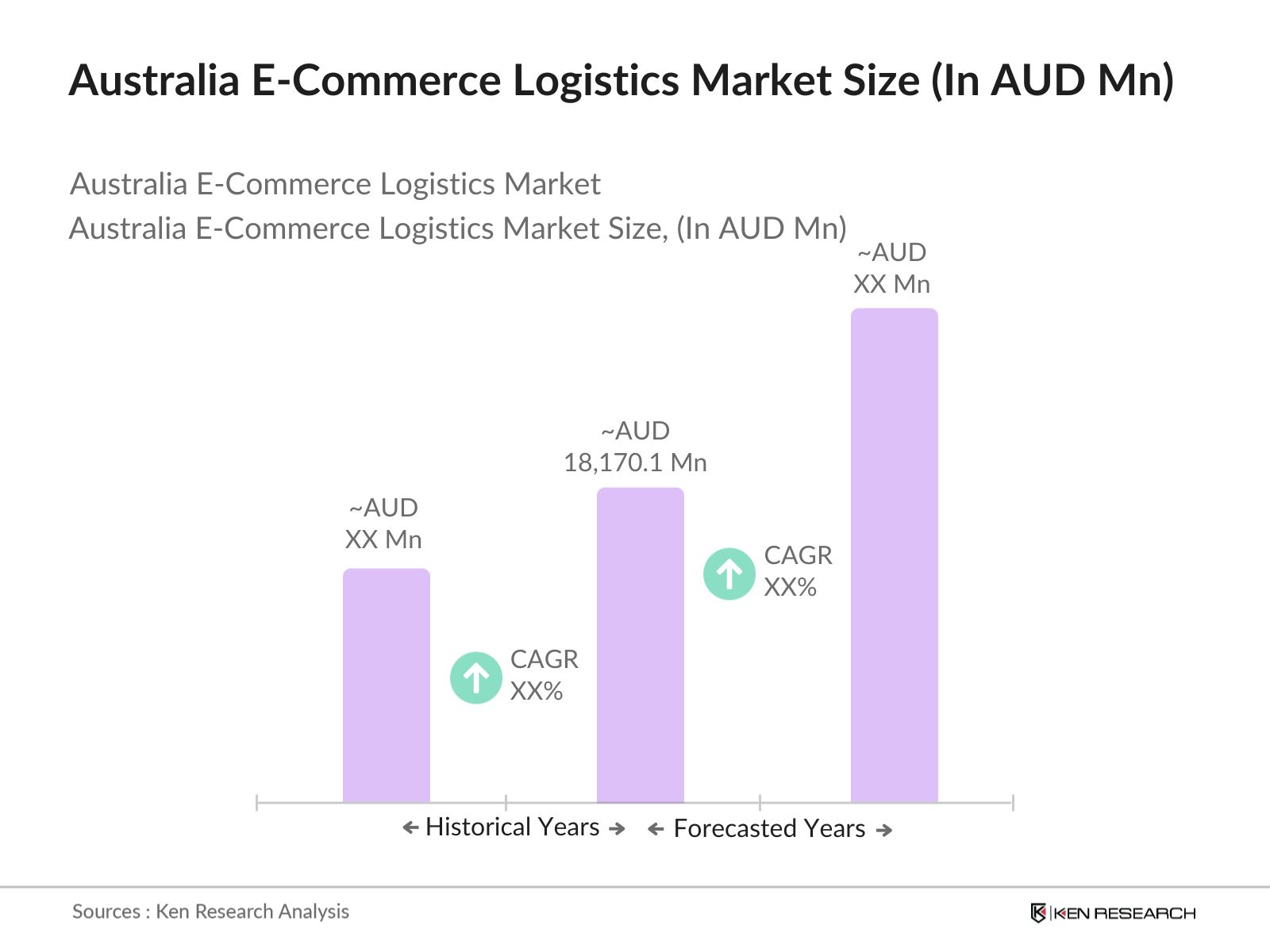

The Australia E-Commerce Logistics Market is valued at AUD 18,170.1 million in revenue terms, based on a five-year historical analysis. The market has grown steadily due to rising mobile commerce penetration, faster delivery expectations, and increasing cross-border purchasing. The order volume reached 623.1 million shipments, further reinforced by consumer preference for convenience, digital payments, and higher average order values. Retailers continue to expand their logistics operations to serve both metro and regional areas efficiently.

The domestic e-commerce logistics landscape in Australia is primarily dominated by regions such as Victoria, New South Wales, and Western Australia. These states benefit from population density, mature infrastructure, and proximity to last-mile delivery hubs. For instance, e-commerce transactions are highly concentrated around Sydney, Canberra, and Melbourne, where major promotional events like Black Friday and Cyber Monday drive order surges. Western Australias growing online order share is supported by higher income levels and robust regional delivery networks.

The e-commerce regulatory environment in Australia is shaped by digital transaction security and cross-border compliance frameworks. As of 2024, over 5.6 million Australian households make monthly online purchases, with 48.8% of total e-commerce transactions processed through platforms like PayPal. Government bodies are increasingly emphasizing digital retail growth through programs focused on cyber-security, consumer data privacy, and support for SMEs. Additionally, regional investment in delivery infrastructure and warehousing is fueling continued development in the logistics sector.

By Delivery Type:Australia E-Commerce Logistics Market is segmented by delivery type into standard delivery and express delivery. The market is dominated by standard delivery, catering to the majority of volume shipments due to balanced cost structures and wide geographic reach across urban and rural zones. Express delivery, while limited in volume, is widely used for time-sensitive segments such as electronics and fashion, especially in metro regions where rapid fulfillment justifies the premium.

By Shipment Weight:The Australia E-Commerce Logistics Market is segmented by parcel weight into lightweight parcels and heavyweight parcels. Lightweight parcels, typically under 3 kilograms, dominate the market, driven by high-frequency online purchases in categories like fashion, books, and cosmetics. These items require minimal storage and enable fast last-mile delivery. Heavyweight parcels, including electronics, furniture, and home appliances, form a smaller share due to bulk handling, larger dimensions, and need for specialized warehousing and delivery infrastructure.

The Australia e-commerce logistics market is highly consolidated, with the top three players handling the majority of total shipments. Australia Post maintains a dominant position, followed by Toll Group and Couriers Please, all of which are actively investing in parcel automation, smart locker systems, and express delivery services. Global players like DHL and FedEx focus primarily on cross-border logistics, with limited domestic operations.

Surge in E-Commerce GMV Driving Logistics Demand: The Australia e-commerce logistics market is witnessing accelerated momentum, with gross merchandise value reaching AUD 77,729 million and generating 1.19 billion shipments in FY24. The scale of online transactions across categories like fashion, electronics, and personal care is boosting demand for integrated logistics infrastructure especially in order fulfillment, last-mile delivery, and express parcel networks across both metropolitan and regional zones.

Omnichannel Retail Elevating Fulfillment Complexity: The rising adoption of omnichannel strategies by Australian retailers is reshaping logistics expectations. Services such as click-and-collect, store-to-door delivery, and real-time tracking are becoming essential. This evolution is pushing e-commerce logistics providers to develop integrated warehousing, flexible last-mile networks, and tech-enabled visibility systems to support seamless customer experiences across physical and digital retail touchpoints.

Regional Logistics Expansion Strengthening National Reach: Australia's e-commerce players are expanding fulfillment centers beyond metro cities to enhance delivery speed and cost efficiency. The development of cross-docking infrastructure and regional warehouses is enabling smoother rural access. Strategic alliances with logistics players like Australia Post and Toll Group are empowering platforms to achieve broader supply chain reach across tier-2 and tier-3 cities, strengthening the logistics backbone for sustained e-commerce growth.

High Cost of Last-Mile Delivery in Low-Density Areas: Australias low population density makes last-mile delivery expensive outside major metros. Long distances, low order concentration, and limited infrastructure in rural zones increase per-parcel costs. This challenges scalability for smaller logistics providers and limits the viability of same-day or next-day services in non-urban regions.

Limited Automation Among Small & Mid-Sized Players: While major logistics firms have adopted warehouse automation, smaller 3PL providers lag in robotics, AI, and order routing technologies. This leads to inefficiencies in sorting, fulfillment, and inventory management especially during seasonal peaks. Cost of tech integration remains a key barrier for mid-sized operators.

The Australia e-commerce logistics market is expected to witness robust advancement through the forecast period, supported by the expansion of regional fulfillment infrastructure and the rising adoption of automation in warehousing and delivery operations. As consumer expectations shift toward faster, more transparent, and flexible delivery services, logistics providers will focus on enhancing last-mile networks, leveraging technology, and scaling capacity across both metro and remote regions to meet evolving retail demand dynamics.

Expansion of Smart Lockers and Self-Service Pickup Models: Urban logistics in Australia is set to transform with widespread adoption of smart locker ecosystems. Logistics firms will increasingly collaborate with retail hubs and housing societies to deploy secure, 24/7 access lockers. This infrastructure will reduce delivery costs, improve drop success rates, and cater to time-sensitive consumers in dense metro clusters seeking contactless convenience.

Transition to Electric and Sustainable Delivery Fleets: Australias e-commerce logistics providers are poised to scale electric vehicle fleets, supported by green regulations and ESG-aligned investments. Strategic alliances with EV manufacturers and renewable warehousing developers will drive cleaner last-mile delivery. These initiatives will not only cut emissions but also align logistics networks with Australias 2050 net-zero vision and evolving consumer sustainability expectations.

|

By Delivery Type |

Standard Delivery |

|

By Shipment Weight |

Light Weight Parcels |

|

By Delivery Time Window |

Same Day & Next Day |

|

By Application |

Fashion & Apparel |

|

By Region |

Metro Cities |

Executive Summary

1.1. Market Overview of Australia E-Commerce Logistics Market

1.2. Ecosystem of Players in the Market

Australia E-Commerce Logistics Market Overview

2.1. Market Size and Shipment Volume Analysis

2.2. Growth in GMV, Urban and Regional Fulfillment

2.3. Key Developments in Technology and Delivery Models

2.4. Public-Private Infrastructure Push

Market Segmentation

3.1. By Delivery Type (Standard, Express)

3.2. By Shipment Weight (Light, Heavy)

3.3. By Delivery Time Window (Same-Day, 2–7 Day)

3.4. By Application (Fashion, Electronics, Others)

3.5. By Region (Metro, Tier-2, Rural)

Competitive Landscape

4.1. Competitive Structure of the Market

4.2. Cross-Comparison of Major Players

Market Growth Drivers

5.1. Surge in GMV and E-Commerce Order Volume

5.2. Adoption of Omnichannel Retail Strategies

5.3. Regional Logistics and Infrastructure Expansion

Market Challenges

6.1. High Last-Mile Cost in Low-Density Regions

6.2. Lack of Automation in Mid-Scale Logistics Firms

Market Future Outlook

7.1. Projected Market Growth and Volume Expansion to FY’29

7.2. Tech Integration and Service Evolution

Market Opportunities

8.1. Growth of Smart Lockers and Self-Pickup Solutions

8.2. Shift Toward Electric Vehicles and Sustainable Logistics

Scope of the Report

9.1. By Delivery Type

9.2. By Shipment Weight

9.3. By Delivery Time Window

9.4. By Application

9.5. By Region

Key Target Audience

10.1. Stakeholders in Logistics, Tech, Retail, and Infrastructure

Frequently Asked Questions

11.1. Market Size, Players, Challenges, and Segment Insights

Research Methodology

12.1. Step-by-Step Approach from Data Gathering to Final Output

Disclaimer

Contact Us

The study began with mapping Australia’s e-commerce logistics ecosystem including national couriers, 3PL providers, express parcel networks, and warehousing players. Secondary sources such as government publications, Australia Post reports, industry portals, and retail commerce datasets were used to define key variables like delivery type, shipment weight, delivery time window, and service regions.

Market sizing was executed using triangulation across e-commerce GMV, order volume, and average parcel revenue. Shipment data by weight and service type were cross-referenced with express delivery trends and customer preferences. Regional demand mapping and infrastructure investment data were applied to derive volumetric forecasts and segment-specific projections from FY24 to FY29F.

Primary interviews were conducted with 3040 stakeholders, including delivery executives, warehousing heads, and third-party logistics partners. Respondents from companies like Australia Post, Toll Group, and Couriers Please provided inputs on fleet size, tech adoption, operational challenges, and consumer behavior. Data was cross-validated through logistics tech vendors and regional distributors.

Data from stakeholder interviews and public sources was synthesized to finalize volume and value forecasts. Shipment splits by region, time window, and weight were benchmarked against 2024 data. Final outputs also integrated pricing trends, EV penetration, and fulfillment infrastructure to ensure a comprehensive and forward-looking market outlook through FY29.

The Australia E-Commerce Logistics Market was valued at AUD 18,170.1 million, driven by strong growth in shipment volumes and evolving consumer demand. The market is witnessing rapid transformation through regional warehouse expansion, digital retail acceleration, and advancements in last-mile delivery across both metropolitan and remote areas.

Key challenges of Australia E-Commerce Logistics Market include high last-mile delivery costs in low-density regions and limited automation adoption among small 3PLs. These factors impact scalability, service speed, and fulfillment efficiency, particularly for emerging players and rural e-commerce penetration.

Australia E-Commerce Logistics Market Top players include Australia Post, Toll Group, Couriers Please, DHL Express, and FedEx Australia. These companies handle over 80% of parcel volumes, offering services ranging from standard and express delivery to cross-border logistics and smart locker integration.

Australia E-Commerce Logistics Market Growth is driven by increased e-commerce GMV, omnichannel retail adoption, and regional infrastructure investment. Urban fulfillment optimization and rising B2C demand are accelerating expansion across service offerings and operational models.

Standard delivery remains the predominant mode of shipment in the Australia e-commerce logistics market, favored for its cost-efficiency and wide applicability across product categories. Express delivery continues to cater to urgent and high-value segments such as electronics and fashion. The majority of parcel volume consists of lightweight shipments, with metro and tier-2 cities driving demand due to dense consumer populations and frequent order cycles.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.