China Video Games Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD8550

December 2024

96

About the Report

China Video Games Market Overview

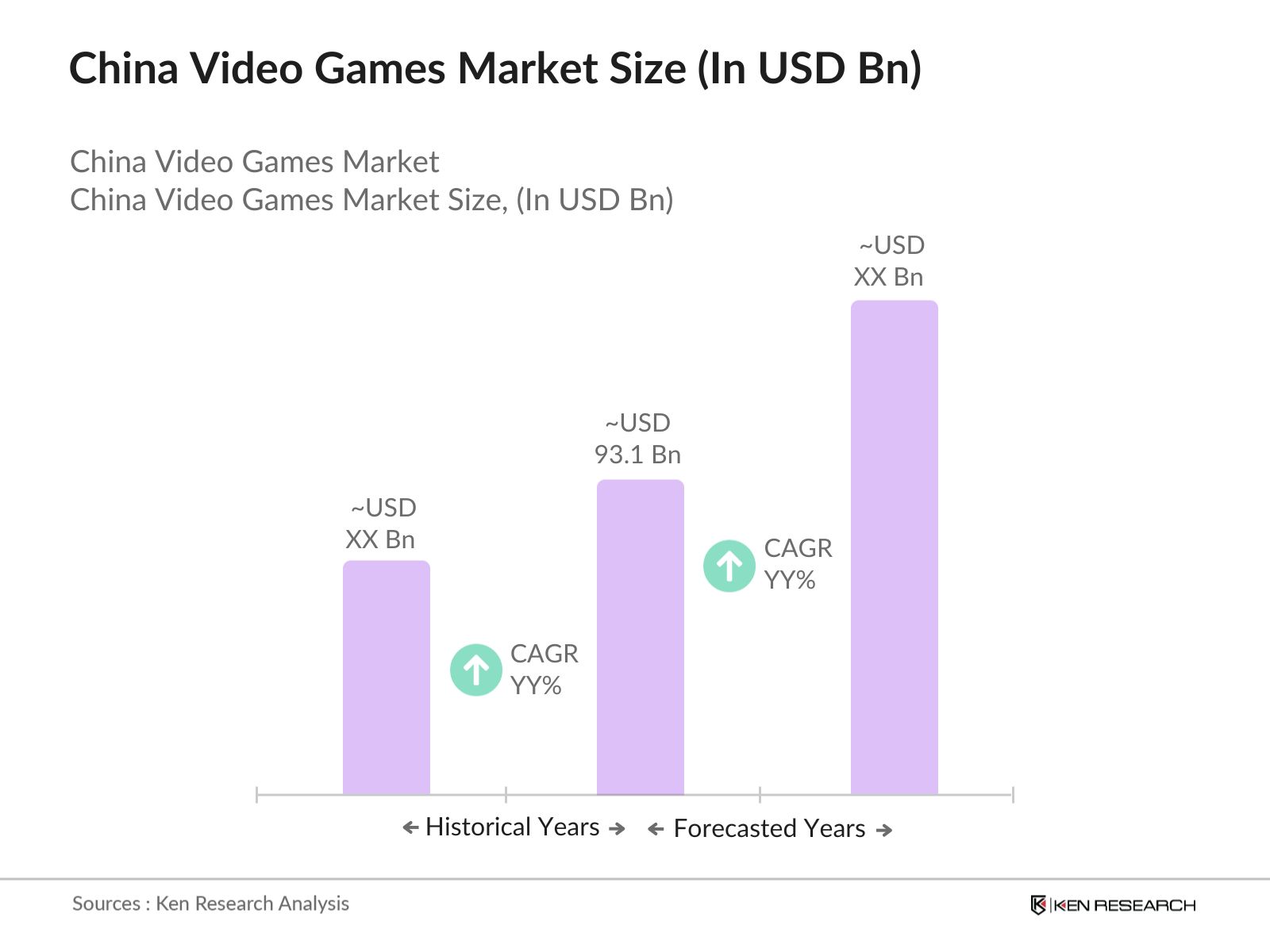

- The China Video Games Market is valued at USD 93.1 billion, supported by consistent user engagement and digital infrastructure. This value reflects a steady expansion, influenced primarily by the rising disposable income among younger demographics, coupled with the rapid adoption of digital gaming platforms. Key players have strategically diversified their portfolios, driving further market adoption and user engagement.

- Major metropolitan areas, including Beijing, Shanghai, and Guangzhou, are the dominant regions in the market due to their concentration of digital infrastructure, affluent populations, and high levels of internet penetration. These cities boast extensive gaming communities and serve as innovation hubs, fostering collaboration between tech firms and gaming studios, which has spurred local growth in game development and e-sports.

- The Chinese government enacted the Healthy Gaming Environment Act in 2024, allocating 500 million RMB to develop tools and resources that promote responsible gaming. This initiative is focused on curbing excessive gaming behaviors and creating a balanced ecosystem by promoting wellness and healthier gaming habits among players.

China Video Games Market Segmentation

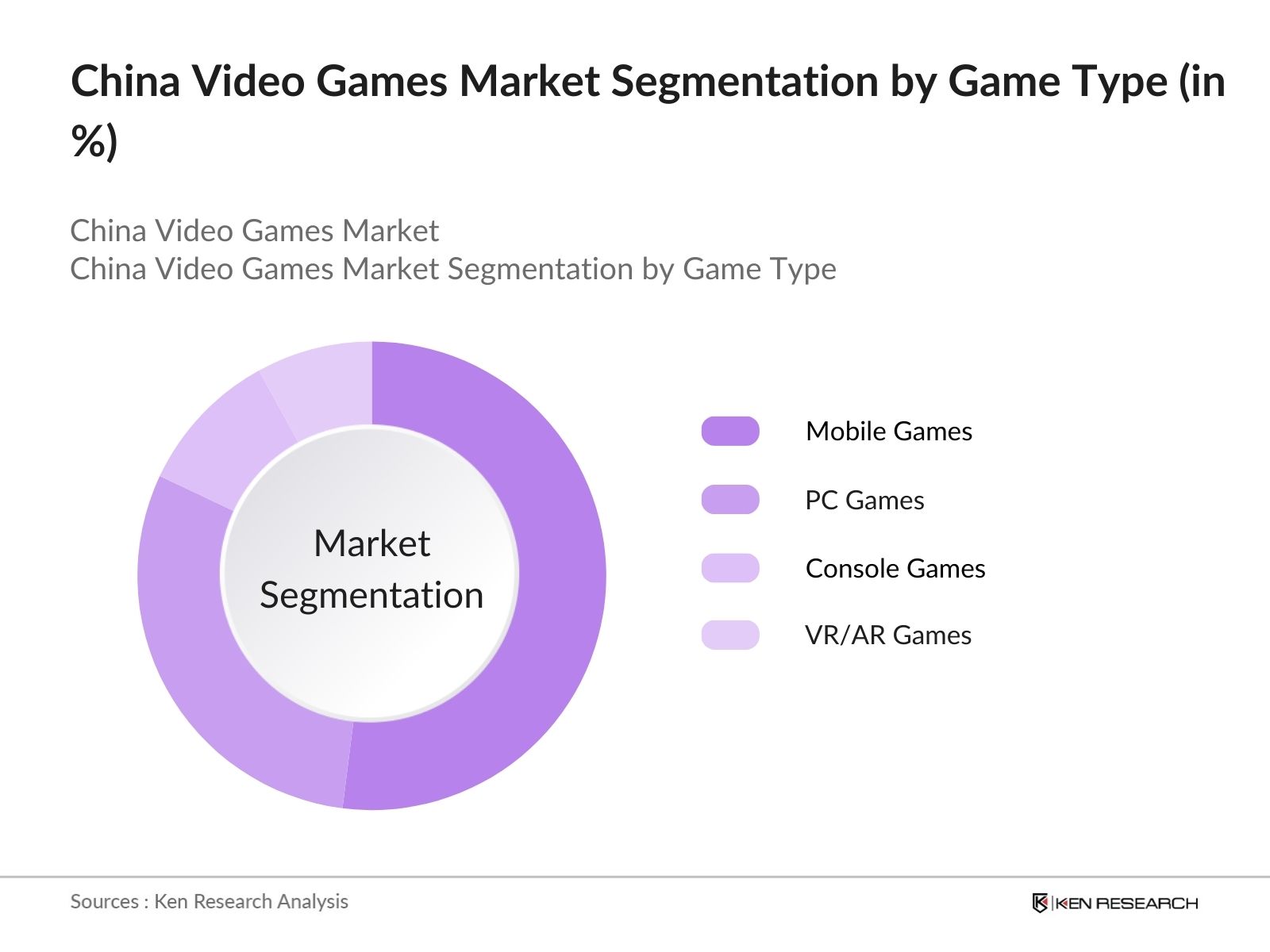

- By Game Type: The market is segmented by game type into mobile games, PC games, console games, and VR/AR games. Mobile games hold a dominant market share due to their accessibility, supported by the widespread use of smartphones. Gaming giants like Tencent and NetEase have capitalized on this trend by developing mobile-exclusive titles that appeal to both casual and hardcore gamers, leveraging the popularity of in-game microtransactions and limited-time events.

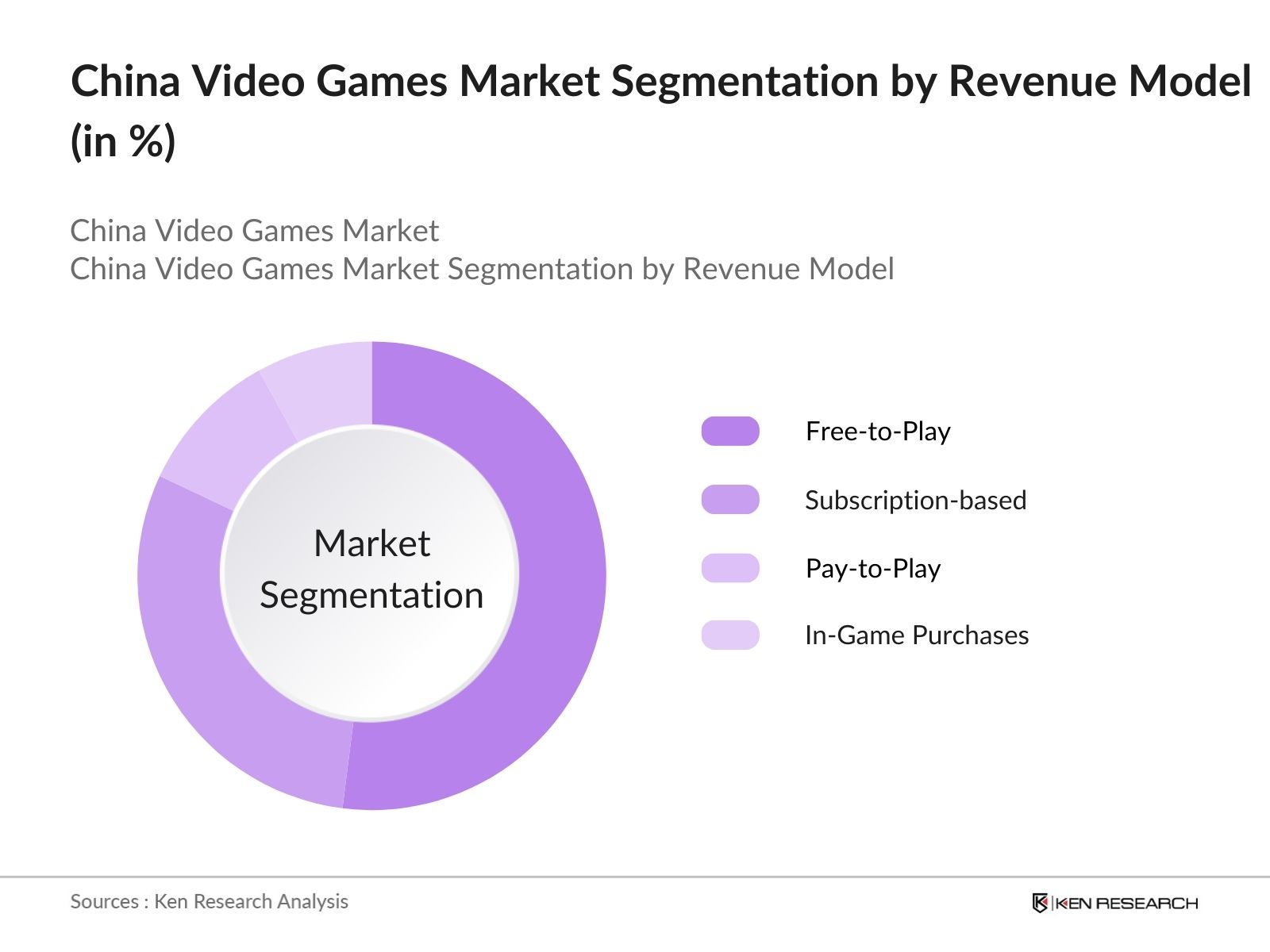

- By Revenue Model: The market is further segmented by revenue model into free-to-play, subscription-based, pay-to-play, and in-game purchases. The free-to-play model leads the segment, as it maximizes user reach and leverages in-app purchases. This approach allows for significant monetization through microtransactions, particularly in competitive games, where users invest in customizations and premium features to enhance their gaming experience.

China Video Games Market Competitive Landscape

The market is led by a concentrated group of influential players, with Tencent and NetEase maintaining substantial shares due to their well-established platforms and popular game titles. Their investment in AI, augmented reality (AR), and virtual reality (VR) demonstrates a commitment to innovation that sets high barriers for new entrants.

China Video Games Market Analysis

Market Growth Drivers

- Rising Consumer Demand for Mobile Gaming: Chinas mobile gaming market continues to see substantial growth, with over 680 million active mobile gamers in 2024. This increase in demand is driven largely by the expanding availability of affordable smartphones with high-performance capabilities that cater to gaming. The Chinese mobile gaming sector saw an increase of 12 million new gamers in 2024 compared to the previous year, reflecting both technological advancements and increased user access.

- Expansion of E-sports Infrastructure: E-sports is witnessing substantial infrastructure development in China. In 2024, the country invested over 60 billion RMB in new e-sports arenas and training facilities. Major cities like Shanghai and Beijing have become hubs for e-sports events, attracting thousands of local and international participants. These investments indicate the government's and industry stakeholders' commitment to making China a global e-sports leader, further fueling demand in the video game market.

- Increased Adoption of Subscription-Based Models: Subscription-based gaming models are gaining traction in China, with over 70 million gamers now subscribing to services such as Tencents Game Pass. This model has been particularly appealing to consumers, as it provides access to an extensive library of games at a fixed monthly cost. The revenue from subscriptions accounted for 20 billion RMB in 2024, showing the shift toward recurring revenue models in the industry.

Market Challenges

- Stringent Government Regulations on Game Content: In 2024, the Chinese government imposed restrictions on game content, particularly regarding violence and gambling elements, which led to the removal of over 1,000 games from local platforms. These regulations are aimed at protecting younger audiences but have resulted in increased compliance costs for developers and slowed the release of new titles.

- Time Limits on Minors Gaming: The Chinese government reinforced strict time limits for gamers under 18, allowing them to play only for three hours weekly. This restriction impacted over 130 million minor gamers in 2024, leading to a revenue decline of around 15 billion RMB in the youth gaming segment. This regulatory measure has had financial implications for companies relying on younger demographics.

China Video Games Market Future Outlook

Over the next five years, the China Video Games industry is anticipated to grow robustly, driven by advancements in mobile gaming, cloud infrastructure, and immersive technologies such as augmented and virtual reality.

Future Market Opportunities

- Rise of Cloud Gaming: Over the next five years, the adoption of 5G technology is expected to fuel cloud gaming, with over 150 million users projected by 2029. The increased accessibility of high-speed internet in rural areas and urban centers will make cloud-based gaming platforms more viable, allowing users to play high-quality games without high-end hardware.

- Growth in Educational Gaming: By 2029, educational gaming is expected to become a segment within the Chinese market, with government endorsement and a projected 50 million student gamers participating in learning-based gaming. With increasing investment in education technology, games tailored for skills and language learning are expected to gain traction in both schools and homes.

Scope of the Report

|

Game Type |

Mobile Games PC Games Console Games VR/AR Games |

|

Revenue Model |

Free-to-Play Subscription-based Pay-to-Play In-game Purchases |

|

Gamer Demographics |

Casual Gamers Professional Gamers E-sports Participants |

|

Platform |

Android iOS PC Console |

|

Region |

East China North China South China Central China Western China |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Gaming Hardware Manufacturers

E-sports Platforms and Organizers

Advertising Agencies

Payment Solution Providers

Mobile Device Manufacturers

Content Creators and Influencers

Investor and Venture Capitalist Firms

Government and Regulatory Bodies (National Press and Publication Administration)

Companies

Players Mentioned in the Report:

Tencent Games

NetEase Games

miHoYo

Perfect World

Lilith Games

YOOZOO Games

ByteDance (Nuverse)

Kingsoft Corporation

37 Interactive Entertainment

Bilibili Gaming

Table of Contents

1. China Video Games Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. China Video Games Market Size (in USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. China Video Games Market Analysis

3.1. Growth Drivers

3.1.1. Rising Internet Penetration

3.1.2. Increase in Disposable Income

3.1.3. Technological Advancements in Gaming Hardware

3.1.4. Popularity of E-sports

3.2. Market Challenges

3.2.1. Government Restrictions on Playtime

3.2.2. Regulatory Approvals for New Games

3.2.3. High Development Costs

3.3. Opportunities

3.3.1. Expansion into Emerging Markets

3.3.2. Cloud Gaming Growth

3.3.3. Cross-platform Gaming

3.4. Trends

3.4.1. Virtual Reality and Augmented Reality Integration

3.4.2. Increased Subscription-based Gaming

3.4.3. Rise of In-game Microtransactions

3.5. Government Regulations

3.5.1. Age-based Restrictions

3.5.2. Gaming License Regulations

3.5.3. Content Approval Standards

3.5.4. Health Impact Regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Overview

4. China Video Games Market Segmentation

4.1. By Game Type (in Value %)

4.1.1. Mobile Games

4.1.2. PC Games

4.1.3. Console Games

4.1.4. VR/AR Games

4.2. By Revenue Model (in Value %)

4.2.1. Free-to-Play

4.2.2. Subscription-based

4.2.3. Pay-to-Play

4.2.4. In-game Purchases

4.3. By Gamer Demographics (in Value %)

4.3.1. Casual Gamers

4.3.2. Professional Gamers

4.3.3. E-sports Participants

4.4. By Platform (in Value %)

4.4.1. Android

4.4.2. iOS

4.4.3. PC

4.4.4. Console

4.5. By Region (in Value %)

4.5.1. East China

4.5.2. North China

4.5.3. South China

4.5.4. Central China

4.5.5. Western China

5. China Video Games Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Tencent Games

5.1.2. NetEase Games

5.1.3. Perfect World

5.1.4. miHoYo

5.1.5. Lilith Games

5.1.6. YOOZOO Games

5.1.7. 37 Interactive Entertainment

5.1.8. ByteDance (Nuverse)

5.1.9. Kingsoft Corporation

5.1.10. CMGE Technology Group

5.1.11. iDreamSky Technology

5.1.12. Bilibili Gaming

5.1.13. JD.com (Gaming Division)

5.1.14. Baidu Games

5.1.15. Alibaba Games

5.2. Cross Comparison Parameters (Revenue, Market Share, R&D Investment, Distribution Network, Market Presence, Product Portfolio, Innovation Capabilities, E-sports Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. China Video Games Market Regulatory Framework

6.1. Gaming Content Standards

6.2. Licensing Requirements

6.3. Monetization Policies

6.4. Compliance Requirements

7. China Video Games Future Market Size (in USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. China Video Games Future Market Segmentation

8.1. By Game Type (in Value %)

8.2. By Revenue Model (in Value %)

8.3. By Gamer Demographics (in Value %)

8.4. By Platform (in Value %)

8.5. By Region (in Value %)

9. China Video Games Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This phase involved mapping the ecosystem of stakeholders in the China Video Games Market. Using comprehensive desk research, we identified key variables, such as market drivers, user demographics, and growth trends, integral to the market dynamics.

Step 2: Market Analysis and Construction

Historical data on the China Video Games Market was compiled, assessing user engagement levels, revenue generation per game type, and the ratio of mobile to PC/console users. This analysis allowed for accurate revenue and usage estimates across platforms.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed and validated through interviews with industry experts from top gaming firms. These insights provided detailed knowledge on user preferences, spending habits, and new technology adoption.

Step 4: Research Synthesis and Final Output

This stage involved direct feedback from gaming companies to verify data accuracy. The resulting analysis reflects verified and detailed insights into product segments, user spending, and future trends in the China Video Games Market.

Frequently Asked Questions

1. How big is the China Video Games Market?

The China Video Games Market is valued at USD 93.1 billion, underpinned by high internet penetration and increasing mobile usage.

2. What are the challenges in the China Video Games Market?

The primary challenges in the China Video Games Market include stringent regulatory measures, high development costs, and increasing competition among domestic and international players.

3. Who are the major players in the China Video Games Market?

Key players in the China Video Games Market include Tencent Games, NetEase Games, miHoYo, Perfect World, and Lilith Games, with significant influence due to innovation and strong user bases.

4. What are the growth drivers of the China Video Games Market?

Growth in the China Video Games Market is fueled by rising disposable income, expanding mobile device usage, and an increasing preference for digital gaming experiences.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.