China VR Headset Market Outlook to 2030

Region:China

Author(s):Sanjeev

Product Code:KROD9411

Region:China

Author(s):Sanjeev

Product Code:KROD9411

November 2024

88

The China VR Headset market is dominated by a mix of local and international players, with companies such as HTC, Oculus (Meta), and Pico Interactive leading the charge. This competitive landscape is characterized by constant innovation, heavy investments in R&D, and strategic partnerships to tap into growing consumer demand for VR technology.

|

Company |

Establishment Year |

Headquarters |

Product Portfolio |

R&D Investments |

Market Penetration |

Strategic Partnerships |

Revenue |

Technological Advancements |

|

HTC Corporation |

1997 |

Taiwan |

||||||

|

Oculus (Meta Platforms) |

2012 |

USA |

||||||

|

Pico Interactive |

2015 |

China |

||||||

|

Huawei Technologies Co., Ltd |

1987 |

China |

||||||

|

Lenovo Group |

1984 |

China |

Over the next five years, the China VR Headset market is expected to show growth driven by increasing adoption across consumer and enterprise applications. The rapid expansion of 5G networks, coupled with advancements in VR software and hardware, will further drive innovation. Additionally, the growing use of VR in industries like healthcare, education, and real estate presents a promising future for the market. Government support and subsidies for tech innovation will continue to encourage domestic manufacturers to push the boundaries of immersive technology.

|

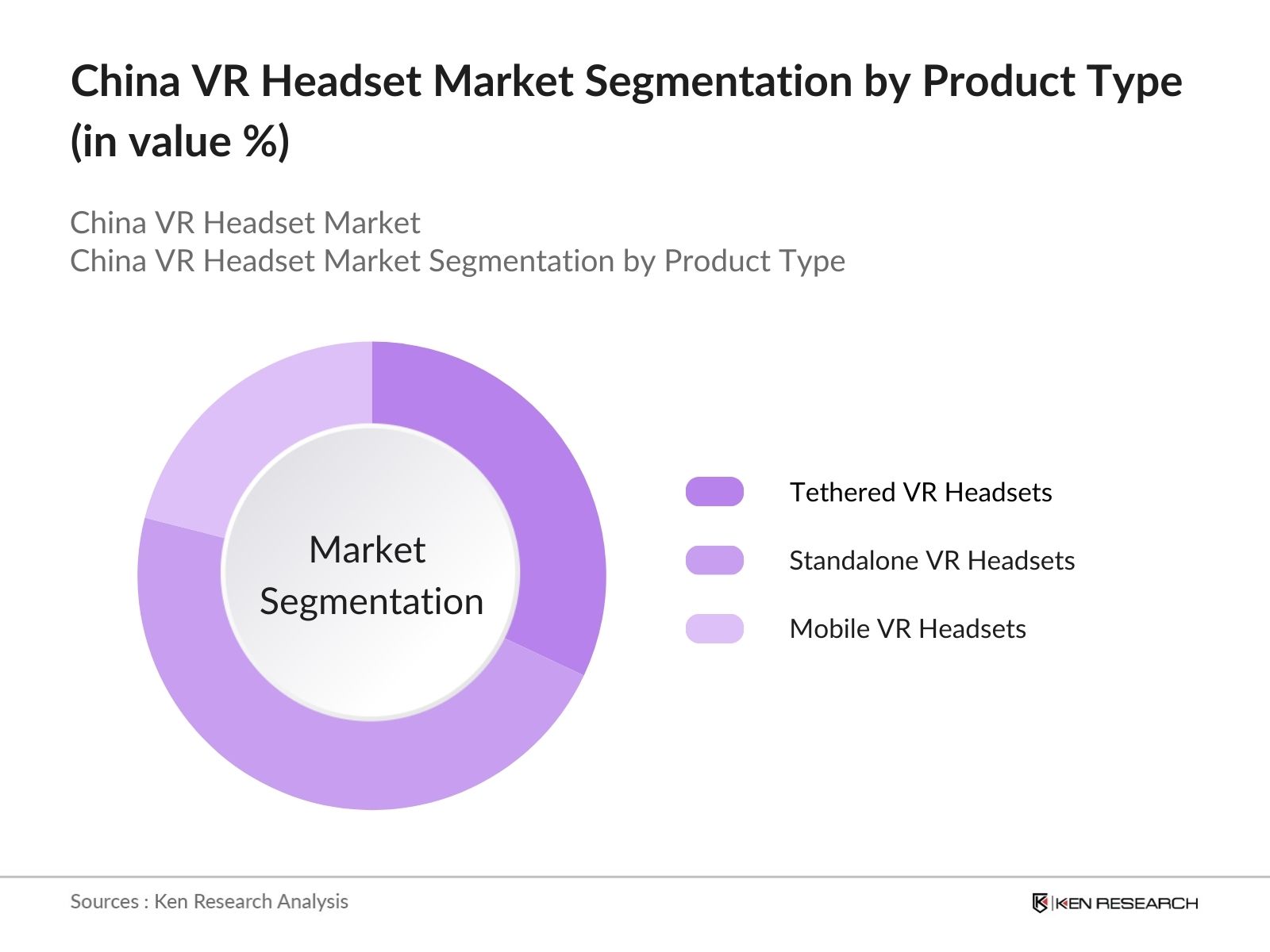

Tethered VR Headsets Standalone VR Headsets Mobile VR Headsets |

|

|

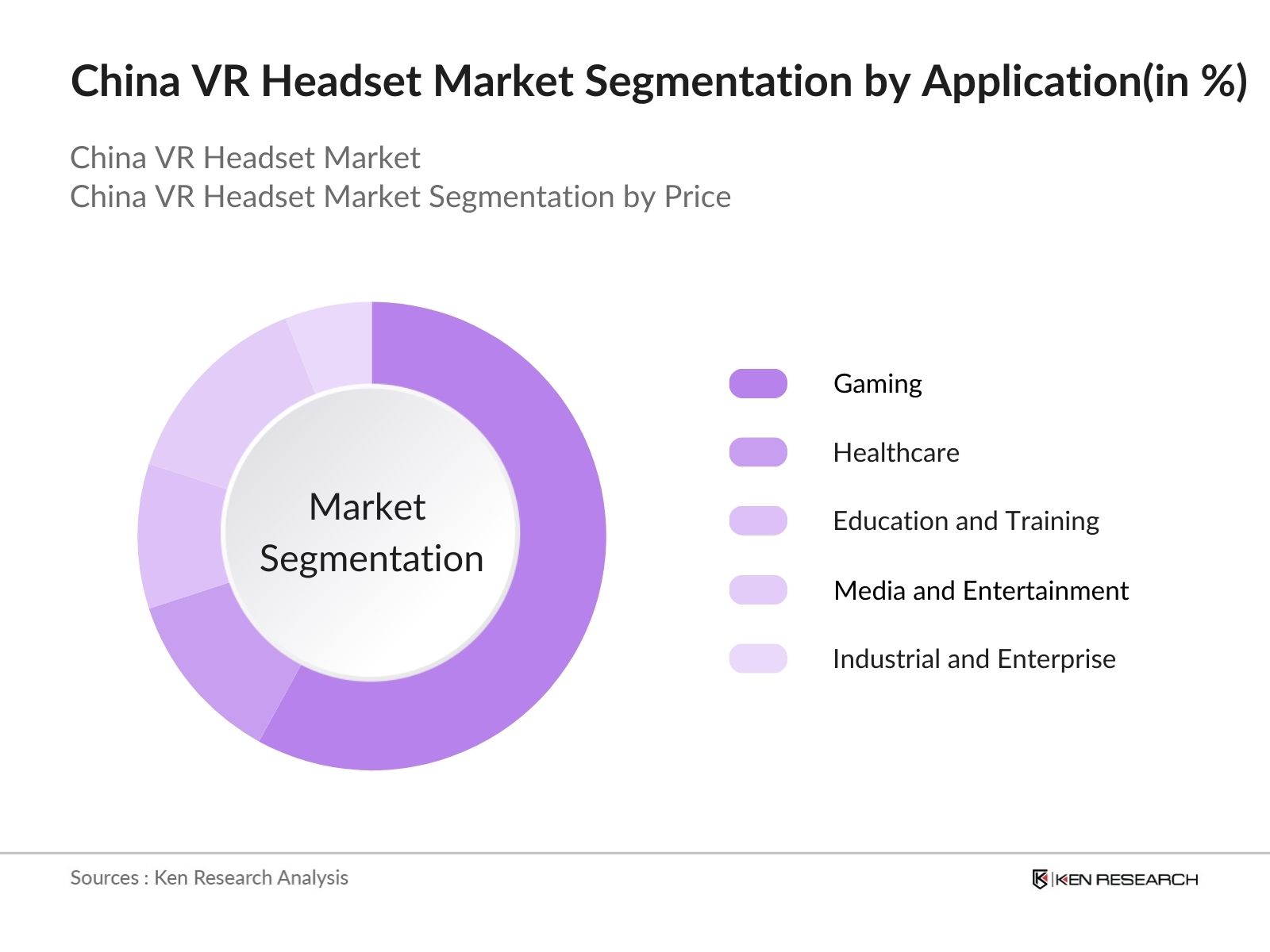

By Application |

Gaming Healthcare Education and Training Media and Entertainment Industrial and Enterprise |

|

By Technology |

3DoF (Three Degrees of Freedom) 6DoF (Six Degrees of Freedom) |

|

By Distribution Channel |

Online Retail Offline Retail |

|

By Region |

North East West South |

China VR Headset Market Major Players

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand in Gaming and Entertainment

3.1.2. Adoption in Healthcare and Education

3.1.3. Expanding 5G Infrastructure

3.1.4. Government Initiatives on Digital Innovation

3.2. Market Challenges

3.2.1. High Production Costs

3.2.2. Limited Content Availability

3.2.3. Consumer Skepticism on VR Health Impacts

3.3. Opportunities

3.3.1. Growth in Augmented Reality Integration

3.3.2. Expanding Corporate and Industrial Applications

3.3.3. Technological Advancements in Visual and Immersive Experiences

3.4. Trends

3.4.1. Integration with AI for Enhanced User Experience

3.4.2. Cloud VR Advancements

3.4.3. Social VR Platforms and Virtual Events

3.5. Government Regulations

3.5.1. National Digital Economy Policy

3.5.2. Guidelines for Consumer Safety and Health in VR Use

3.5.3. Support for VR Adoption in Education

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem Analysis

4.1. By Product Type (In Value %)

4.1.1. Tethered VR Headsets

4.1.2. Standalone VR Headsets

4.1.3. Mobile VR Headsets

4.2. By Application (In Value %) 4.2.1. Gaming

4.2.2. Healthcare

4.2.3. Education and Training

4.2.4. Media and Entertainment

4.2.5. Industrial and Enterprise

4.3. By Technology (In Value %)

4.3.1. 3DoF (Three Degrees of Freedom)

4.3.2. 6DoF (Six Degrees of Freedom)

4.4. By Distribution Channel (In Value %)

4.4.1. Online Retail

4.4.2. Offline Retail

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. HTC Corporation

5.1.2. Sony Corporation

5.1.3. Oculus (Meta Platforms)

5.1.4. Pico Interactive

5.1.5. Huawei Technologies Co., Ltd.

5.1.6. Lenovo Group

5.1.7. DPVR (Deepoon VR)

5.1.8. Xiaomi Corporation

5.1.9. Valve Corporation

5.1.10. Samsung Electronics Co., Ltd.

5.1.11. Microsoft Corporation

5.1.12. Google LLC

5.1.13. Pimax Technology

5.1.14. Qualcomm Technologies

5.1.15. Varjo Technologies

5.2. Cross Comparison Parameters

(Headquarters, Inception Year, Product Portfolio, Market Penetration, R&D Investment, Strategic Partnerships, Unit Shipments, Product Differentiation)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Safety and Consumer Protection Guidelines

6.2. Data Privacy and Security Standards for VR Applications

6.3. Government Incentives for VR Technology Development

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the China VR Headset market. Extensive desk research is performed, utilizing secondary and proprietary databases to gather comprehensive market information. The goal is to define the critical variables influencing market growth, such as 5G deployment and consumer trends.

This phase focuses on compiling and analyzing historical data regarding market size, product segmentation, and industry revenue generation. Evaluation of VR headset adoption by end-users will be conducted to ensure data reliability.

We validate the constructed market hypotheses through interviews with industry experts. These consultations offer operational and financial insights, which help refine the market data and trends analysis.

The final step entails direct engagement with VR manufacturers and industry players, which ensures a comprehensive understanding of product offerings and sales performance. This process helps in delivering a validated and holistic analysis of the market.

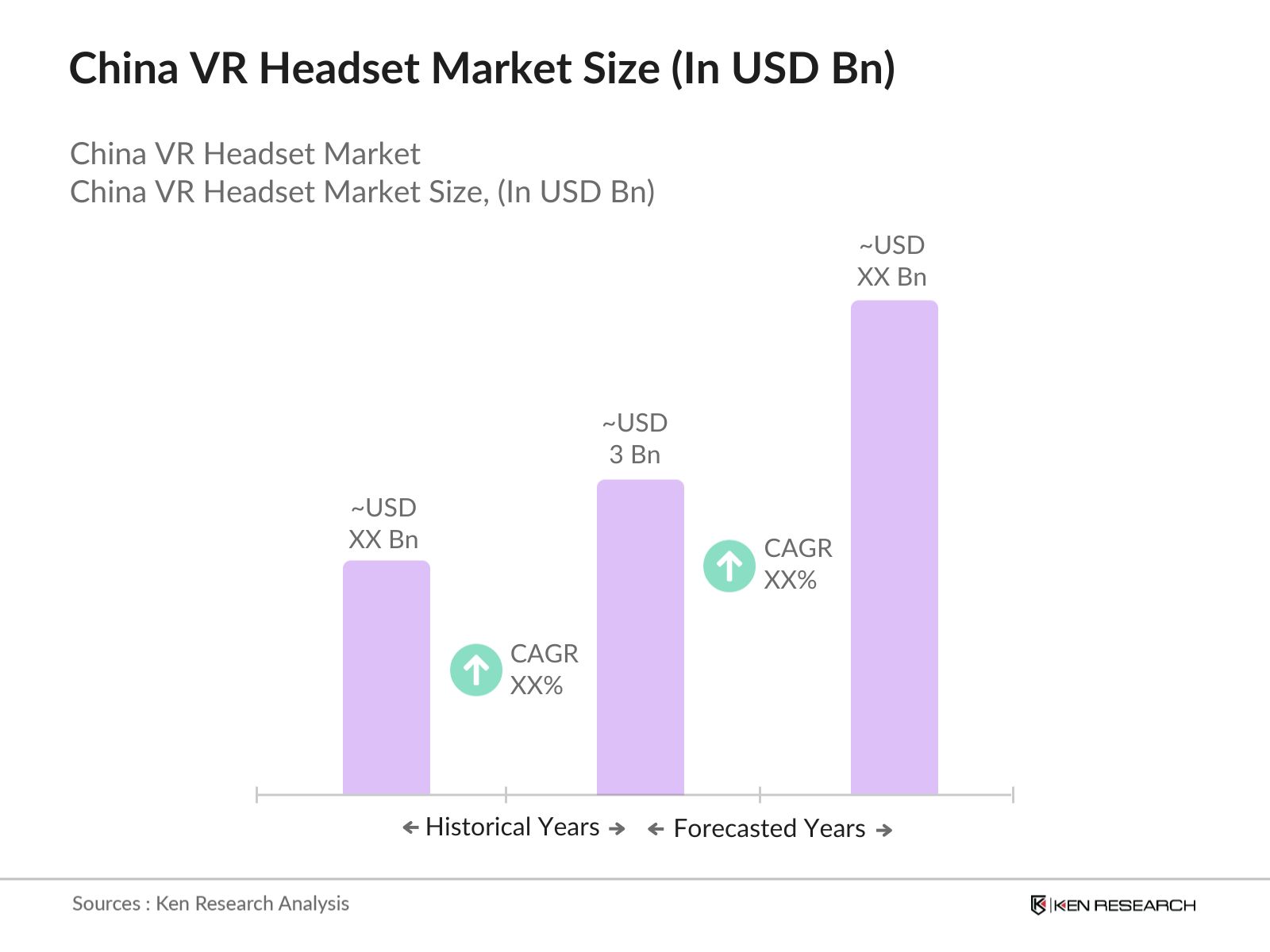

The China VR Headset market is valued at USD 3 billion, driven by increasing adoption in gaming, healthcare, and industrial applications, alongside investments in VR hardware and software innovations.

Key challenges in China VR Headset market include high production costs, limited high-quality content, and consumer health concerns related to prolonged VR usage. Additionally, there is a need for improved compatibility and comfort in headset design.

Key players in China VR Headset market include HTC Corporation, Oculus (Meta Platforms), Pico Interactive, Huawei Technologies Co., Ltd., and Lenovo Group. These companies dominate due to their strong product portfolios, R&D investments, and strategic partnerships.

The China VR Headset market is driven by advancements in 5G infrastructure, increasing demand for immersive entertainment experiences, and growing use in education, healthcare, and industrial training sectors.

Emerging trends in China VR Headset market include the integration of AI in VR systems for enhanced user experiences, cloud-based VR solutions, and the growth of social VR platforms for virtual events and interactions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.