Europe 3D Printing Market Outlook to 2030

Region:Europe

Author(s):Shreya Garg

Product Code:KROD5967

December 2024

98

About the Report

Europe 3D Printing Market Overview

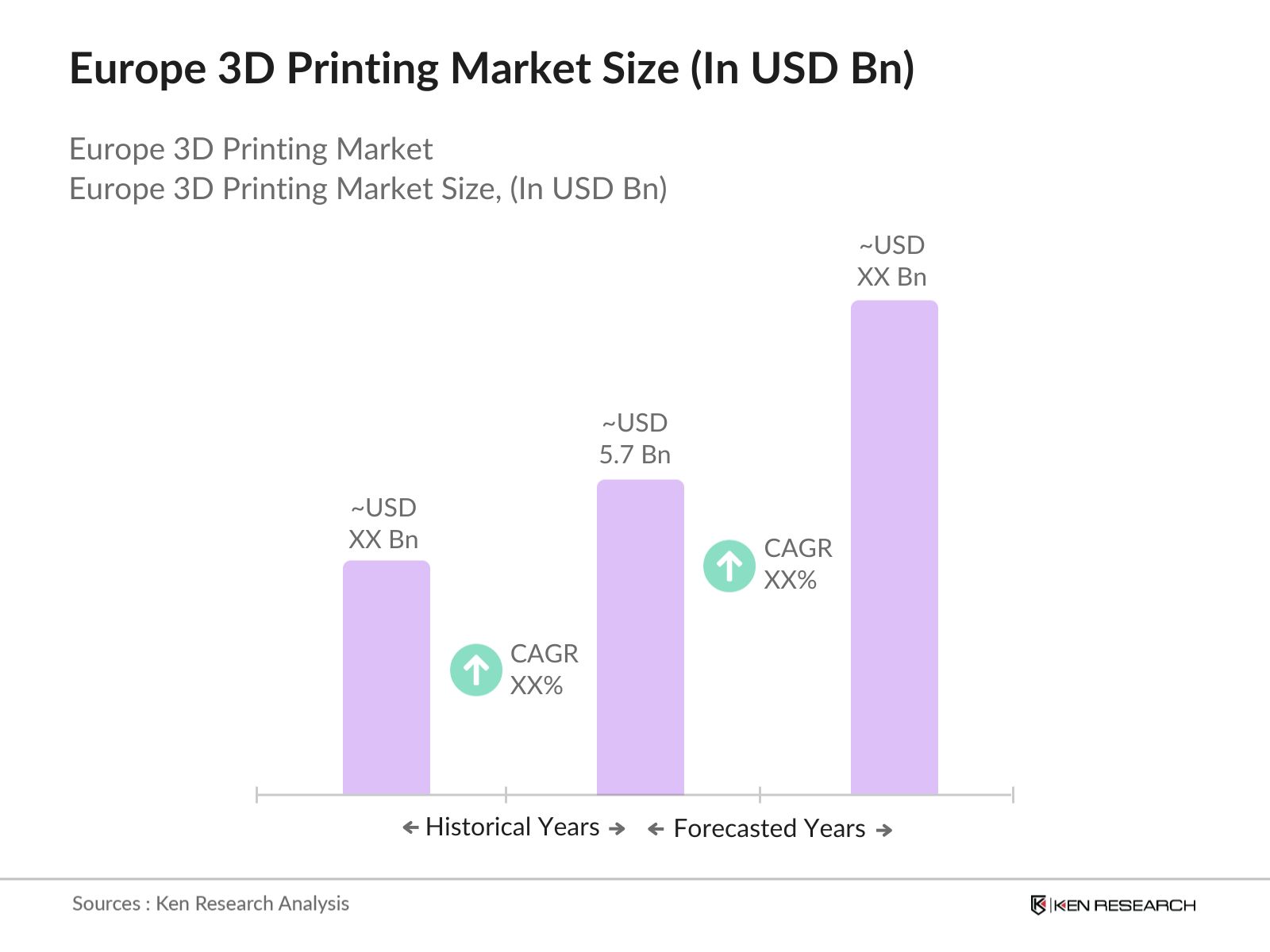

- The Europe 3D printing market has grown substantially, with a valuation of USD 5.7 billion based on a five-year historical analysis. This growth is attributed to increased demand for customized manufacturing solutions across industries such as aerospace, healthcare, and automotive. The integration of additive manufacturing techniques has significantly enhanced production efficiency, reducing material wastage and lead times. The expansion of 3D printing materials, particularly metals and composites, is also driving market adoption in Europe, especially in industrial manufacturing sectors. The markets growth trajectory reflects the region's increasing focus on technological advancements and sustainability in production.

- Germany, the United Kingdom, and France are the dominant players in the Europe 3D printing market. Germany's dominance stems from its strong industrial base, particularly in automotive and aerospace, where 3D printing has become integral to manufacturing processes. In the UK, the healthcare sector is a major driver, with the country leading in medical 3D printing applications, such as prosthetics and implants. Frances prominence comes from government investments in R&D and the growing adoption of 3D printing in the aerospace industry. These countries have fostered innovation ecosystems, making them market leaders in 3D printing technologies.

- The European Union mandates CE marking for 3D-printed products, ensuring they meet safety, health, and environmental standards. In 2023, over 10,000 3D-printed products underwent CE certification, ensuring compliance with EU regulations. This requirement is critical for industries like healthcare, where the safety of 3D-printed medical devices is paramount. The CE marking process is an essential step for manufacturers, ensuring that products meet regulatory standards before they enter the market.

Europe 3D Printing Market Segmentation

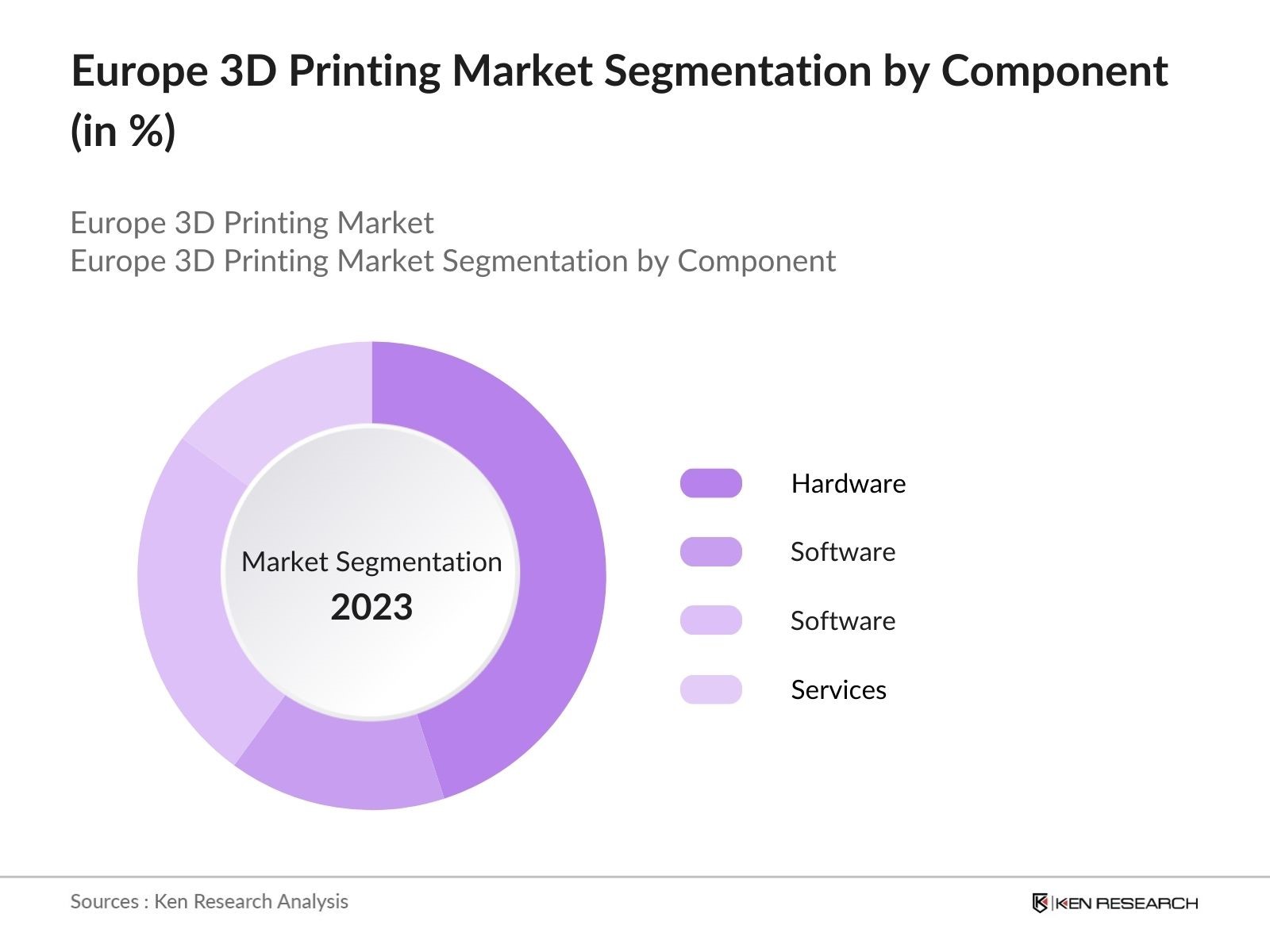

By Component: The market is segmented by component into hardware, software, materials, and services. Recently, hardware has held a dominant share due to its critical role in driving the adoption of 3D printers across industries. The availability of high-performance 3D printers, especially in metal 3D printing, has boosted demand in sectors like automotive and aerospace. With the rise of innovative 3D printers capable of handling multiple materials, the hardware sub-segment continues to grow in importance. This dominance is driven by the increasing demand for faster, more efficient machines that can handle complex designs.

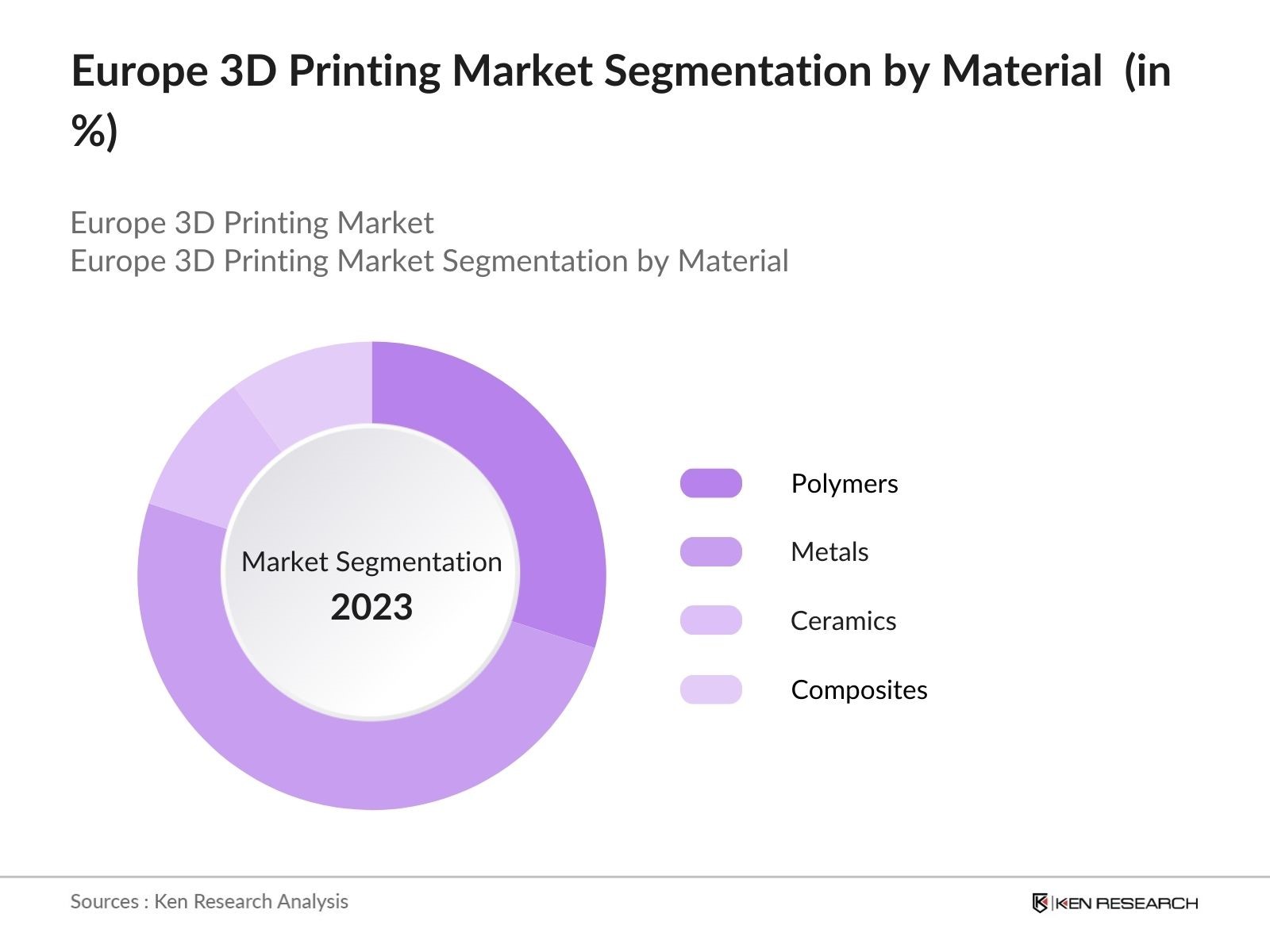

By Material: The market is also segmented by material into polymers, metals, ceramics, and composites. Metals have emerged as the dominant material in industrial 3D printing, especially in sectors like aerospace and automotive, where precision and durability are crucial. Metals such as aluminum and titanium are increasingly used for 3D-printed components due to their strength-to-weight ratio, making them ideal for applications in lightweight structures. The growing use of metal 3D printing in producing high-performance parts has solidified its leadership within the material segmentation.

Europe 3D Printing Market Competitive Landscape

The Europe 3D printing market is highly competitive, with key players focusing on technological advancements, product innovation, and strategic collaborations to maintain market dominance. The consolidation of market share by leading companies underscores their significant influence in shaping the industry. Global leaders such as Stratasys Ltd. and 3D Systems Corporation have established a robust presence, while regional companies such as EOS GmbH leverage their local expertise to cater to European manufacturers.

|

Company Name |

Establishment Year |

Headquarters |

Revenue |

R&D Expenditure |

Employee Count |

Product Portfolio |

Geographic Presence |

Strategic Initiatives |

|

Stratasys Ltd. |

1989 |

Israel |

||||||

|

3D Systems Corporation |

1986 |

USA |

||||||

|

EOS GmbH |

1989 |

Germany |

||||||

|

Materialise NV |

1990 |

Belgium |

||||||

|

Renishaw PLC |

1973 |

UK |

Europe 3D Printing Industry Analysis

Growth Drivers

- Expansion of Aerospace and Automotive Sectors: The aerospace and automotive sectors in Europe have seen substantial growth due to advancements in 3D printing. In 2022, the European automotive industry produced over 12 million vehicles, contributing significantly to regional economies. 3D printing's ability to create lightweight, durable parts has been instrumental in reducing manufacturing time and costs, enhancing the competitiveness of these industries. Similarly, the aerospace sector, valued at over 200 billion, leverages 3D printing for manufacturing complex components, which improves fuel efficiency and reduces waste. Both sectors are heavily investing in technology for customization and innovation.

- Growth in Healthcare Applications: The European healthcare industry is rapidly adopting 3D printing technologies for various applications, including prosthetics, implants, and personalized medical devices. With the healthcare market valued at 2 trillion, the demand for customized solutions is increasing. In 2023, over 1 million 3D-printed prosthetics were produced in Europe, aiding in the efficient treatment of patients with specific needs. This technology also enhances surgical planning by providing detailed, customized anatomical models, reducing surgery times by up to 50%, according to healthcare professionals.

- Advancements in 3D Printing Materials: New materials, such as advanced polymers, composites, and bio-compatible substances, are transforming the capabilities of 3D printing. Europe has become a leader in the production and innovation of these materials. In 2023, the European market for advanced 3D printing materials reached significant milestones, with over 2,000 tonnes of new materials developed. These advancements enable the production of stronger, lighter, and more versatile components, especially in aerospace, healthcare, and automotive sectors. Additionally, the development of recyclable materials is helping meet stringent environmental regulations.

Market Challenges

- Cost-Prohibitive Technologies: Despite the benefits of 3D printing, the high initial investment remains a barrier for widespread adoption, especially among small and medium enterprises (SMEs). In 2022, the average industrial 3D printer cost upwards of 300,000, making it inaccessible for many businesses. The high cost of raw materials, which can be 50% higher than traditional manufacturing inputs, further exacerbates this challenge. This limits the technology's penetration into mass markets where cost-efficiency is crucial.

- Intellectual Property Concerns: The rise of 3D printing poses significant intellectual property (IP) challenges. As technology enables the reproduction of complex designs, it becomes harder to protect proprietary products and processes. In 2022, over 500 IP infringement cases related to 3D printing were reported across Europe, creating a barrier to the technology's wider adoption. The lack of clear regulations surrounding digital manufacturing files further complicates the enforcement of IP rights, especially in industries like fashion, automotive, and healthcare.

Europe 3D Printing Market Future Outlook

Over the next five years, the Europe 3D printing market is expected to experience sustained growth, driven by continuous advancements in printing technologies and an increasing focus on sustainable manufacturing processes. The shift towards lightweight materials, particularly in the automotive and aerospace industries, will further fuel demand. Additionally, as governments across Europe emphasize reducing industrial waste and carbon emissions, 3D printing is positioned to play a pivotal role in achieving these goals. Expanding adoption in the healthcare sector, particularly for medical devices and implants, is another area where significant growth is anticipated.

Future Market Opportunities

- Technological Innovation in Materials: The European market is witnessing a surge in innovation surrounding 3D printing materials, with a focus on developing materials that are stronger, lighter, and more sustainable. In 2023, European R&D institutions created over 150 new types of materials tailored for 3D printing applications. These advancements are expected to fuel the growth of industries such as aerospace and healthcare, which require highly specialized materials for performance-critical applications.

- Expansion into New Industry Verticals: 3D printing is expanding into previously untapped sectors like construction, fashion, and food. In 2023, over 100 construction projects in Europe utilized 3D printing for building components, reducing construction times by 30%. The fashion industry, particularly in countries like Italy and France, has begun using 3D printing for creating sustainable and innovative designs. Additionally, the food industry is exploring 3D printing to create customized meals, particularly in catering to dietary restrictions and healthcare-related needs.

Scope of the Report

|

By Component |

Hardware Software Materials Services |

|

By Material |

Polymers Metals Ceramics Composites |

|

By Technology |

SLA FDM SLS EBM |

|

By Application |

Aerospace & Defense Healthcare Automotive Consumer Electronics |

|

By Country |

Germany France UK Italy Rest of Europe |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (EU Commission, National Standards Bodies)

3D Printing Hardware Manufacturers

Aerospace and Defense Companies

Automotive Manufacturers

Healthcare Providers (Medical Device Manufacturers, Hospitals)

Research and Development Institutes

Additive Manufacturing Service Providers

Banks and Financial Institutions

Companies

Major Players

Stratasys Ltd.

3D Systems Corporation

EOS GmbH

Materialise NV

Renishaw PLC

HP Inc.

SLM Solutions Group AG

Voxeljet AG

GE Additive

Protolabs

Ultimaker

ExOne

Markforged, Inc.

Carbon, Inc.

EnvisionTEC

Table of Contents

Europe 3D Printing Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

Europe 3D Printing Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

Europe 3D Printing Market Analysis

3.1 Growth Drivers (Increased Demand for Customization, Efficiency in Manufacturing)

3.1.1 Expansion of Aerospace and Automotive Sectors

3.1.2 Growth in Healthcare Applications

3.1.3 Rise in Government R&D Investments

3.1.4 Advancements in 3D Printing Materials

3.2 Market Challenges (High Cost of 3D Printers and Materials, Regulatory Concerns)

3.2.1 Cost-Prohibitive Technologies

3.2.2 Limited Adoption in Mass Production

3.2.3 Intellectual Property Concerns

3.3 Opportunities (Proliferation of Additive Manufacturing, Integration with AI)

3.3.1 Technological Innovation in Materials

3.3.2 Expansion into New Industry Verticals

3.3.3 Demand for On-Demand Production

3.4 Trends (Automation Integration, Growth in Metal 3D Printing)

3.4.1 Rise of Multi-Material 3D Printing

3.4.2 Increasing Adoption in Jewelry & Fashion Industry

3.4.3 Cloud-Based 3D Printing Services

3.5 Government Regulation (EU Regulatory Landscape for 3D Printing)

3.5.1 CE Marking and Safety Requirements

3.5.2 ISO Standards in 3D Printing

3.5.3 Environmental Regulations

Europe 3D Printing Market Segmentation

4.1 By Component (In Value %)

4.1.1 Hardware

4.1.2 Software

4.1.3 Materials

4.1.4 Services

4.2 By Material (In Value %)

4.2.1 Polymers

4.2.2 Metals

4.2.3 Ceramics

4.2.4 Composites

4.3 By Technology (In Value %)

4.3.1 Stereolithography (SLA)

4.3.2 Fused Deposition Modelling (FDM)

4.3.3 Selective Laser Sintering (SLS)

4.3.4 Electron Beam Melting (EBM)

4.4 By Application (In Value %)

4.4.1 Aerospace & Defense

4.4.2 Healthcare

4.4.3 Automotive

4.4.4 Consumer Electronics

4.5 By Country (In Value %)

4.5.1 Germany

4.5.2 France

4.5.3 UK

4.5.4 Italy

4.5.5 Rest of Europe

Europe 3D Printing Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Stratasys Ltd.

5.1.2 3D Systems Corporation

5.1.3 EOS GmbH

5.1.4 SLM Solutions Group AG

5.1.5 Materialise NV

5.1.6 Renishaw PLC

5.1.7 HP Inc.

5.1.8 GE Additive

5.1.9 Voxeljet AG

5.1.10 Protolabs

5.1.11 Ultimaker

5.1.12 ExOne

5.1.13 Markforged, Inc.

5.1.14 Carbon, Inc.

5.1.15 EnvisionTEC

5.2 Cross Comparison Parameters (Revenue, Headquarters, Inception Year, No. of Employees, Product Portfolio, R&D Expenditure, Market Share, Geographic Presence)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Funding Programs

5.8 Private Equity & Venture Capital Investment

Europe 3D Printing Market Regulatory Framework

6.1 EU Regulations on 3D Printing Materials

6.2 Compliance Requirements in Medical 3D Printing

6.3 Intellectual Property Framework

Europe 3D Printing Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

Europe 3D Printing Future Market Segmentation

8.1 By Component (In Value %)

8.2 By Material (In Value %)

8.3 By Technology (In Value %)

8.4 By Application (In Value %)

8.5 By Country (In Value %)

Europe 3D Printing Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Emerging Opportunities in Additive Manufacturing

9.3 Market Penetration Strategies

9.4 White Space Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase involved identifying and mapping key stakeholders within the Europe 3D printing ecosystem. This was achieved through extensive desk research, leveraging secondary databases and proprietary resources. The goal was to determine the factors influencing the dynamics of the 3D printing market, such as technological advancements, government initiatives, and material developments.

Step 2: Market Analysis and Construction

During this phase, we analyzed historical data, including market penetration, technology adoption rates, and revenue generation within the 3D printing industry. This step also involved assessing industry demand for 3D printing services and products in sectors like automotive, aerospace, and healthcare.

Step 3: Hypothesis Validation and Expert Consultation

We engaged in discussions with 3D printing experts from major manufacturers and research institutions to validate key assumptions about market trends, competitive dynamics, and growth opportunities. These insights helped refine the data and ensure its accuracy.

Step 4: Research Synthesis and Final Output

In the final phase, we synthesized all data points and integrated expert insights to produce a comprehensive analysis of the Europe 3D printing market. This phase also involved compiling quantitative insights on market segments, competitor analysis, and future projections.

Frequently Asked Questions

01. How big is the Europe 3D Printing Market?

The Europe 3D printing market is valued at USD 5.7 billion, driven by technological advancements in manufacturing, particularly in aerospace, automotive, and healthcare sectors.

02. What are the challenges in the Europe 3D Printing Market?

Challenges in the Europe 3D printing market include the high initial cost of 3D printers and materials, regulatory concerns regarding intellectual property, and the slow adoption of 3D printing for mass production in some sectors.

03. Who are the major players in the Europe 3D Printing Market?

Major players in the Europe 3D printing market include Stratasys Ltd., EOS GmbH, 3D Systems Corporation, Renishaw PLC, and Materialise NV. These companies dominate due to their extensive R&D efforts, innovative product offerings, and strategic partnerships.

04. What are the growth drivers of the Europe 3D Printing Market?

Key growth drivers in the Europe 3D printing market include the increasing demand for customized manufacturing solutions, advancements in printing technologies, and the adoption of 3D printing in the healthcare sector, particularly for medical devices.

05. What trends are shaping the Europe 3D Printing Market?

The Europe 3D printing market is witnessing trends like automation integration with 3D printing, increased use of metal printing, and the rise of cloud-based 3D printing services to streamline production processes.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.