Europe Agricultural Robots Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD3036

November 2024

94

About the Report

Europe Agricultural Robots Market Overview

- The Europe Agricultural Robots market is valued at USD 3 billion, supported by increasing adoption of automated solutions across farms and fields. Agricultural automation has gained traction due to labor shortages, rising costs, and the need to enhance crop yield. The demand is also driven by government incentives and policy shifts towards sustainable farming practices. The surge in smart farming techniques, including the use of AI-driven equipment, further contributes to the growing market.

- Western European countries such as Germany, France, and the Netherlands are dominant in this market due to their advanced agricultural infrastructure, strong R&D capabilities, and government support for automation in farming. These countries also have a long-standing focus on sustainable farming practices, which aligns with the increased adoption of agricultural robots. The dense concentration of technologically advanced farms in these regions has accelerated the adoption of robotic solutions.

- The European Union's Common Agricultural Policy (CAP) allocates substantial funding towards precision agriculture, with over USD 431 billion earmarked for 2023-2027. A significant portion of this funding supports robotic and AI-based farming technologies aimed at increasing crop productivity while reducing environmental harm. CAP emphasizes the use of precision farming tools to meet sustainability goals, which include reducing pesticide use by 50% and fertilizer use by 20% by 2030. Countries like France, Germany, and Italy have been the major beneficiaries of CAP funds, driving adoption in precision agriculture.

Europe Agricultural Robots Market Segmentation

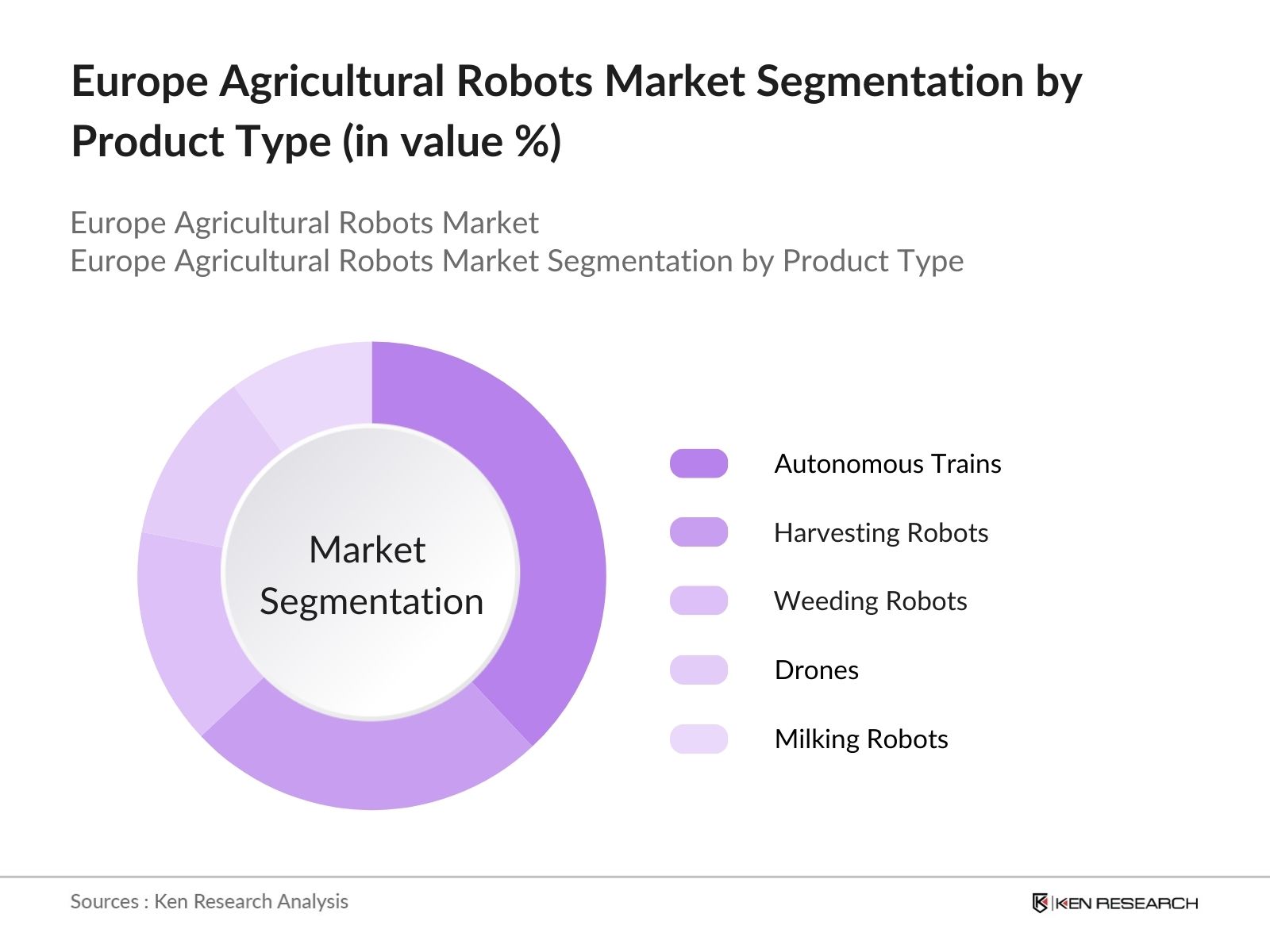

By Product Type: The Europe Agricultural Robots market is segmented by product type into autonomous tractors, harvesting robots, weeding robots, drones, and milking robots. Recently, autonomous tractors have a dominant market share due to their integration with advanced GPS systems and AI technologies, which allow for precision in fieldwork. This helps to reduce manual labor and improve efficiency, which is particularly valuable in regions experiencing agricultural labor shortages. Major players such as John Deere have been actively innovating in this area, further driving demand for autonomous tractors.

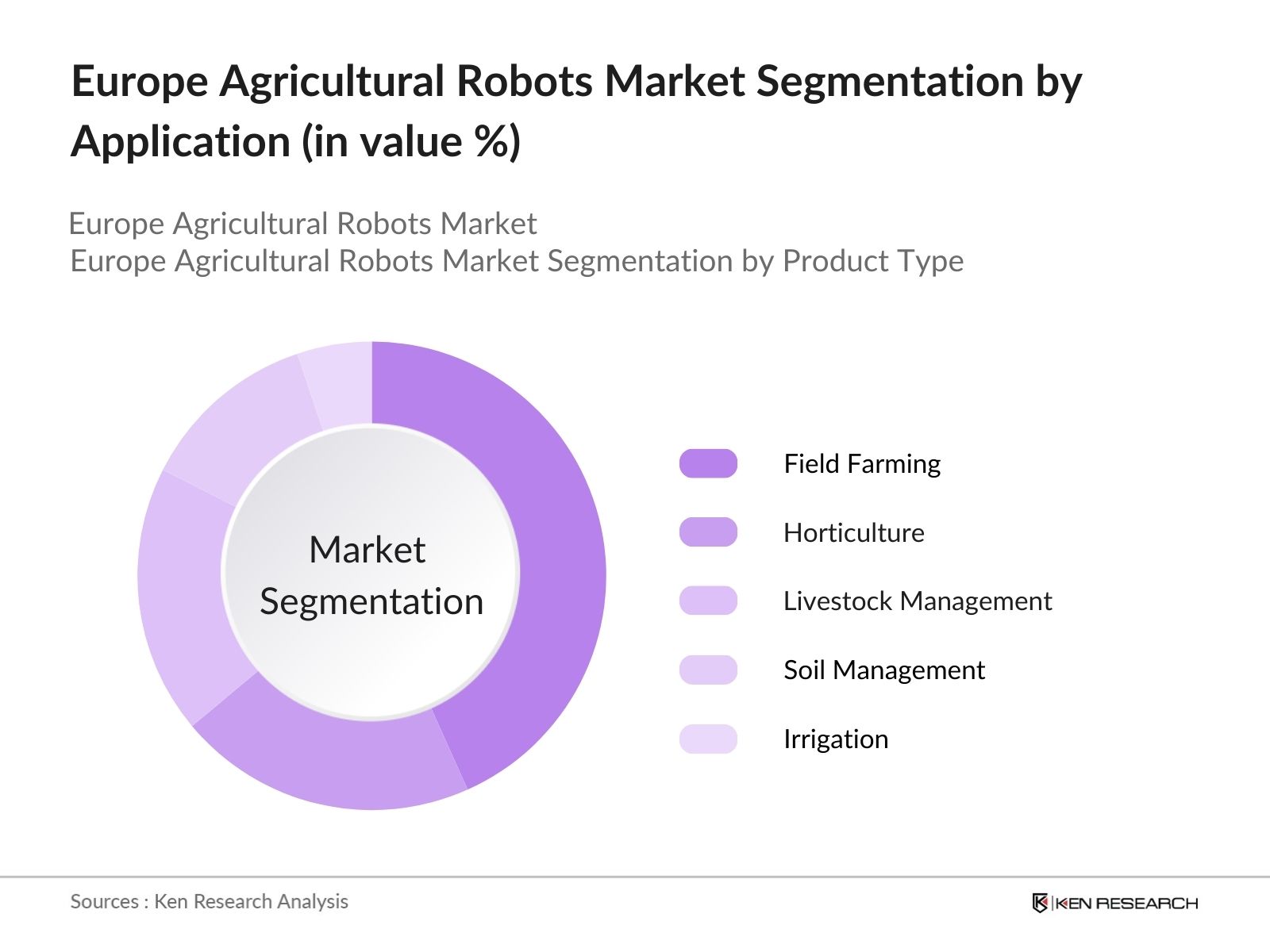

By Application: The market is also segmented by application into field farming, horticulture, livestock management, soil management, and irrigation. Field farming holds the largest share of the market due to the extensive use of robots for seeding, weeding, and harvesting across vast areas of land. The ability to automate tasks such as tillage and planting has made field farming the primary focus of agricultural robotics innovation, especially in countries like France and Germany, where large-scale farms benefit significantly from such technologies.

Europe Agricultural Robots Market Competitive Landscape

The Europe Agricultural Robots market is dominated by several key players who have strong technological capabilities and have heavily invested in R&D. Companies like John Deere, AGCO Corporation, and Kubota Corporation are leading the market with their innovative product portfolios. These companies leverage their extensive distribution networks, global presence, and strategic partnerships to maintain their market position.

|

Company |

Established |

Headquarters |

Product Portfolio |

Innovation Focus |

Revenue |

Market Presence |

Strategic Partnerships |

R&D Investment |

Customer Base |

|||

|

John Deere |

1837 |

Illinois, USA |

- |

- |

- |

- |

- |

- |

- |

|||

|

CNH Industrial |

1999 |

London, UK |

- |

- |

- |

- |

- |

- |

- |

|||

|

Kubota Corporation |

1890 |

Osaka, Japan |

- |

- |

- |

- |

- |

- |

- |

|||

|

AGCO Corporation |

1990 |

Georgia, USA |

- |

- |

- |

- |

- |

- |

- |

|||

|

Trimble Inc. |

1978 |

California, USA |

- |

- |

- |

- |

- |

- |

- |

|||

The competition in the market is characterized by a high level of technological advancements and strong focus on innovation, particularly in areas such as AI, IoT, and autonomous systems. As companies compete to develop more efficient and reliable robotic solutions, the market is expected to witness further consolidation, with major players acquiring smaller, specialized firms.

Europe Agricultural Robots Market Analysis

Growth Drivers

- Increased Demand for Precision Agriculture: Precision agriculture is transforming the European agricultural landscape by improving efficiency and crop yields. The EU has committed significant resources to promote the adoption of these technologies, with a pledge of USD 11.16 billion by 2030 for innovations in digital farming.This investment is part of broader efforts to improve agricultural efficiency and sustainability, aligning with the objectives of the EU Green Deal and the EU Digital Strategy. This technological integration is driven by the region's growing focus on sustainability.

- Shortage of Agricultural Workforce: Europe's agricultural sector has been facing a significant labor shortage, with a decline of 10 million agricultural workers between 2015 and 2024. This has fueled the need for automation to fill the gap. Countries like Spain and Italy, which rely heavily on seasonal labor, have seen a 15-25% reduction in available workers, intensifying the demand for robotic solutions to handle labor-intensive tasks such as harvesting, planting, and weeding. Robotic automation is increasingly viewed as the solution to maintain productivity amidst these workforce challenges.

- Rising Adoption of Smart Farming Practices: Smart farming practices powered by the Internet of Things (IoT) have surged across Europe, with 60,000 farms now integrating IoT-based solutions in 2024. Smart sensors monitor crop health, automate irrigation, and optimize fertilization, leading to increased efficiency in the agricultural process. The deployment of IoT devices has allowed farmers to remotely manage operations, reducing human intervention.

Challenges

- High Initial Investment Costs: The capital expenditure required for agricultural robotics remains a significant barrier for small and medium-sized farms in Europe. The European Investment Bank estimates that farmers face initial costs of USD 33,000 per unit for specialized robotic equipment, such as autonomous tractors or precision weeding robots. While larger farms can absorb these costs through scale, smaller operations often struggle with high upfront investments, limiting widespread adoption.

- Regulatory Concerns: The stringent regulations surrounding the use of robotics in agriculture create operational challenges for farmers. The EUs General Product Safety Directive, which includes guidelines for machine safety and autonomous systems, places substantial compliance burdens on agricultural robot manufacturers. In 2024, about 40% of agricultural robot manufacturers in Europe reported regulatory compliance as their top challenge, according to data from the European Commission.

Europe Agricultural Robots Future Market Outlook

Over the next five years, the Europe Agricultural Robots market is expected to grow significantly, driven by increasing automation in agriculture, advances in AI and machine learning technologies, and the implementation of government policies supporting sustainable farming. The expansion of smart farming technologies, especially the integration of IoT and AI-based systems, will further stimulate the market, making agricultural robots more accessible and efficient for farmers across Europe.

Market Opportunities

- Advances in AI and Machine Learning for Robotics: Artificial intelligence (AI) and machine learning (ML) technologies are revolutionizing the performance of agricultural robots, particularly drones. In 2024, there are over 5,000 AI-powered agricultural drones deployed across European farms, enabling precision tasks like real-time crop monitoring and yield prediction. These AI-driven solutions offer farmers the ability to make data-backed decisions, minimizing resource waste and maximizing crop output.

- Integration of 5G and IoT Networks: With the expansion of 5G networks, agricultural robots and IoT devices are becoming more integrated into Europes smart farming infrastructure. As of early 2024, the European Union reports thatbasic 5G coverageis available to approximately81% of the EU population. This enhanced connectivity allows real-time data transmission from robots to farmers, improving operational efficiency and decision-making. The integration of 5G with IoT devices in smart farms reduces latency issues in autonomous systems, providing instant insights on crop health, soil conditions, and environmental factors.

Scope of the Report

|

Segment |

Sub-Segments |

|

Product Type |

Autonomous Tractors |

|

Harvesting Robots |

|

|

Weeding Robots |

|

|

Drones |

|

|

Milking Robots |

|

|

Application |

Field Farming |

|

Horticulture |

|

|

Livestock Management |

|

|

Soil Management |

|

|

Irrigation |

|

|

Technology |

GPS Technology |

|

AI and Machine Learning |

|

|

Robotics & Automation Systems |

|

|

Vision Systems & Sensors |

|

|

IoT and Connectivity Solutions |

|

|

End-User |

Small & Medium-Sized Farms |

|

Large Farms |

|

|

Cooperative Farming |

|

|

Region |

Western Europe |

|

Eastern Europe |

|

|

Southern Europe |

|

|

Northern Europe |

|

|

Central Europe |

Products

Key Target Audience

Agricultural Equipment Manufacturers

Agriculture Technology (AgriTech) Companies

Drone Manufacturers

Precision Farming Solution Providers

Insurance Companies

Technology Providers (AI, IoT, and Robotics Solutions)

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (European Commission, National Agricultural Ministries)

Companies

Major Players in the Europe Agricultural Robots Market

John Deere

CNH Industrial

AGCO Corporation

Kubota Corporation

Trimble Inc.

AgEagle Aerial Systems

DeLaval

Boumatic Robotics

DJI

Nao Technologies

Autonomous Solutions Inc.

Fendt (AGCO)

Harvest Automation

Lely Industries N.V.

Robotic Harvesting

Table of Contents

1. Europe Agricultural Robots Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Europe Agricultural Robots Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Europe Agricultural Robots Market Analysis

3.1 Growth Drivers

3.1.1 Increased Demand for Precision Agriculture (Technological Integration in Farming)

3.1.2 Shortage of Agricultural Workforce (Automation to Compensate Labor Shortage)

3.1.3 Rising Adoption of Smart Farming Practices (IoT in Agriculture)

3.1.4 Government Incentives for Sustainable Farming (Subsidies for Robotic Solutions)

3.2 Market Challenges

3.2.1 High Initial Investment Costs (Capital Expenditure for Robotics Equipment)

3.2.2 Lack of Skilled Workforce for Robotic Operations (Technical Barriers for Farmers)

3.2.3 Regulatory Concerns (EU Robotics and Safety Regulations)

3.3 Opportunities

3.3.1 Advances in AI and Machine Learning for Robotics (AI in Agricultural Drones)

3.3.2 Integration of 5G and IoT Networks (Smart Farm Connectivity)

3.3.3 Expansion of Robotic Leasing Models (Cost-Effective Adoption for Small Farmers)

3.4 Trends

3.4.1 Adoption of Fully Autonomous Robots (Autonomous Weeding and Seeding Systems)

3.4.2 Increasing Use of Drones in Agriculture (Drone-Based Crop Monitoring and Spraying)

3.4.3 Vertical Farming and Robotics (Urban Agriculture Integration)

3.5 Government Regulation

3.5.1 EU Policies on Precision Agriculture (Common Agricultural Policy, CAP)

3.5.2 Subsidies for Robotic Implementations (Funding for Automation)

3.5.3 Environmental Regulations for Robotic Equipment (Carbon Emission Targets)

3.5.4 Data Protection Laws Impacting Smart Farms (GDPR Compliance for Data from Robots)

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. Europe Agricultural Robots Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Autonomous Tractors

4.1.2 Harvesting Robots

4.1.3 Weeding Robots

4.1.4 Drones

4.1.5 Milking Robots

4.2 By Application (In Value %)

4.2.1 Field Farming

4.2.2 Horticulture

4.2.3 Livestock Management

4.2.4 Soil Management

4.2.5 Irrigation

4.3 By Technology (In Value %)

4.3.1 GPS Technology

4.3.2 AI and Machine Learning

4.3.3 Robotics & Automation Systems

4.3.4 Vision Systems & Sensors

4.3.5 IoT and Connectivity Solutions

4.4 By End-User (In Value %)

4.4.1 Small & Medium-Sized Farms

4.4.2 Large Farms

4.4.3 Cooperative Farming

4.5 By Region (In Value %)

4.5.1 Western Europe

4.5.2 Eastern Europe

4.5.3 Southern Europe

4.5.4 Northern Europe

4.5.5 Central Europe

5. Europe Agricultural Robots Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 John Deere

5.1.2 CNH Industrial

5.1.3 Kubota Corporation

5.1.4 AGCO Corporation

5.1.5 Trimble Inc.

5.1.6 AgEagle Aerial Systems

5.1.7 DeLaval

5.1.8 Boumatic Robotics

5.1.9 DJI

5.1.10 Nao Technologies

5.1.11 Autonomous Solutions Inc.

5.1.12 Fendt (AGCO)

5.1.13 Harvest Automation

5.1.14 Lely Industries N.V.

5.1.15 Robotic Harvesting

5.2 Cross Comparison Parameters (Product Portfolio, Market Presence, Innovation Focus, Technology Capabilities, Revenue, Customer Base, Investment in R&D, Strategic Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Europe Agricultural Robots Market Regulatory Framework

6.1 Environmental Standards for Robotic Machinery

6.2 Compliance Requirements for Safety Standards

6.3 Certification Processes for Autonomous Systems

7. Europe Agricultural Robots Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Europe Agricultural Robots Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By Technology (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9. Europe Agricultural Robots Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase of research involved identifying the key variables within the Europe Agricultural Robots market by conducting extensive desk research and utilizing a combination of proprietary and secondary data sources. This phase involved constructing an ecosystem map that highlighted all stakeholders in the agricultural robotics industry.

Step 2: Market Analysis and Construction

Historical market data were analyzed to understand trends and identify the key drivers impacting market dynamics. An evaluation of farm sizes, technological adoption rates, and labor trends were carried out to estimate revenue and penetration rates across European countries.

Step 3: Hypothesis Validation and Expert Consultation

Interviews with industry experts, including robotic manufacturers and farm operators, were conducted to validate market hypotheses. These consultations offered direct insights into the market's operational challenges, opportunities, and financial performance.

Step 4: Research Synthesis and Final Output

The final phase synthesized all primary and secondary data to develop market forecasts and derive detailed insights into product segments, technological adoption, and revenue generation. These insights were verified through direct engagement with agricultural manufacturers and stakeholders.

Frequently Asked Questions

1. How big is the Europe Agricultural Robots Market?

The Europe Agricultural Robots market is valued at USD 3 billion and is driven by the increasing need for automation in agriculture due to labor shortages and the demand for more efficient farming practices.

2. What are the challenges in the Europe Agricultural Robots Market?

Challenges include high initial costs for robotic equipment, regulatory concerns related to the safety and operation of autonomous systems, and a lack of skilled workforce to manage advanced robotics on farms.

3. Who are the major players in the Europe Agricultural Robots Market?

Key players include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, and Trimble Inc., who dominate due to their technological advancements, large-scale operations, and global distribution networks.

4. What are the growth drivers of the Europe Agricultural Robots Market?

The market is propelled by the adoption of precision agriculture technologies, government support for sustainable farming practices, and technological advancements in AI and IoT, which make robotics more accessible to farmers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.