Europe Bioplastics Market Outlook to 2030

Region:Europe

Author(s):Sanjna

Product Code:KROD3740

December 2024

99

About the Report

Europe Bioplastic Market Overview

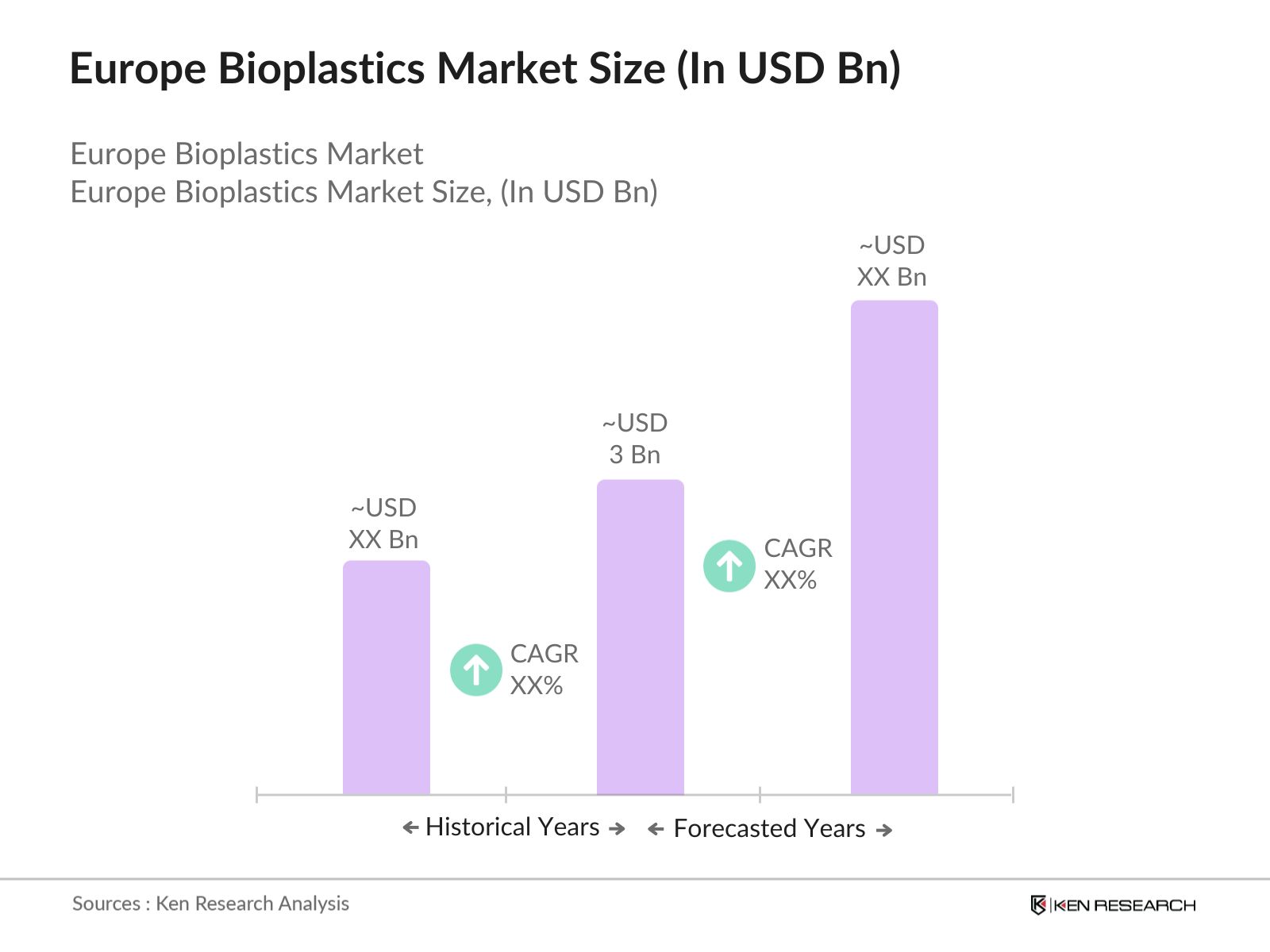

- The Europe Bioplastics market is valued at USD 3 billion, driven by increasing environmental concerns, strict government regulations, and rising consumer demand for sustainable packaging alternatives. The market is benefiting from initiatives to reduce carbon emissions, plastic waste, and reliance on fossil fuels. Factors such as advancements in bio-based polymer technology and growing investments in R&D are fueling the markets growth.

- Countries like Germany, France, and Italy dominate the European bioplastics market. This dominance is attributed to their well-established industrial sectors, a robust commitment to environmental policies, and significant investments in innovation within the plastics and packaging industries. Germany, in particular, has a strong network of bioplastics manufacturers and research institutions, making it a key player in this industry.

- The European Unions Directive on Single-Use Plastics (SUP), adopted in 2019, has been a significant regulatory driver for the bioplastics market. The directive aims to reduce the environmental impact of plastic waste by banning certain single-use plastic items, such as cutlery, plates, and straws, by 2021. This has paved the way for bioplastic alternatives, which meet the EUs sustainability criteria. In addition, the directive mandates member states to achieve a 90% collection rate for plastic bottles by 2029, boosting demand for bio-based materials in packaging.

Europe Bioplastics Market Segmentation

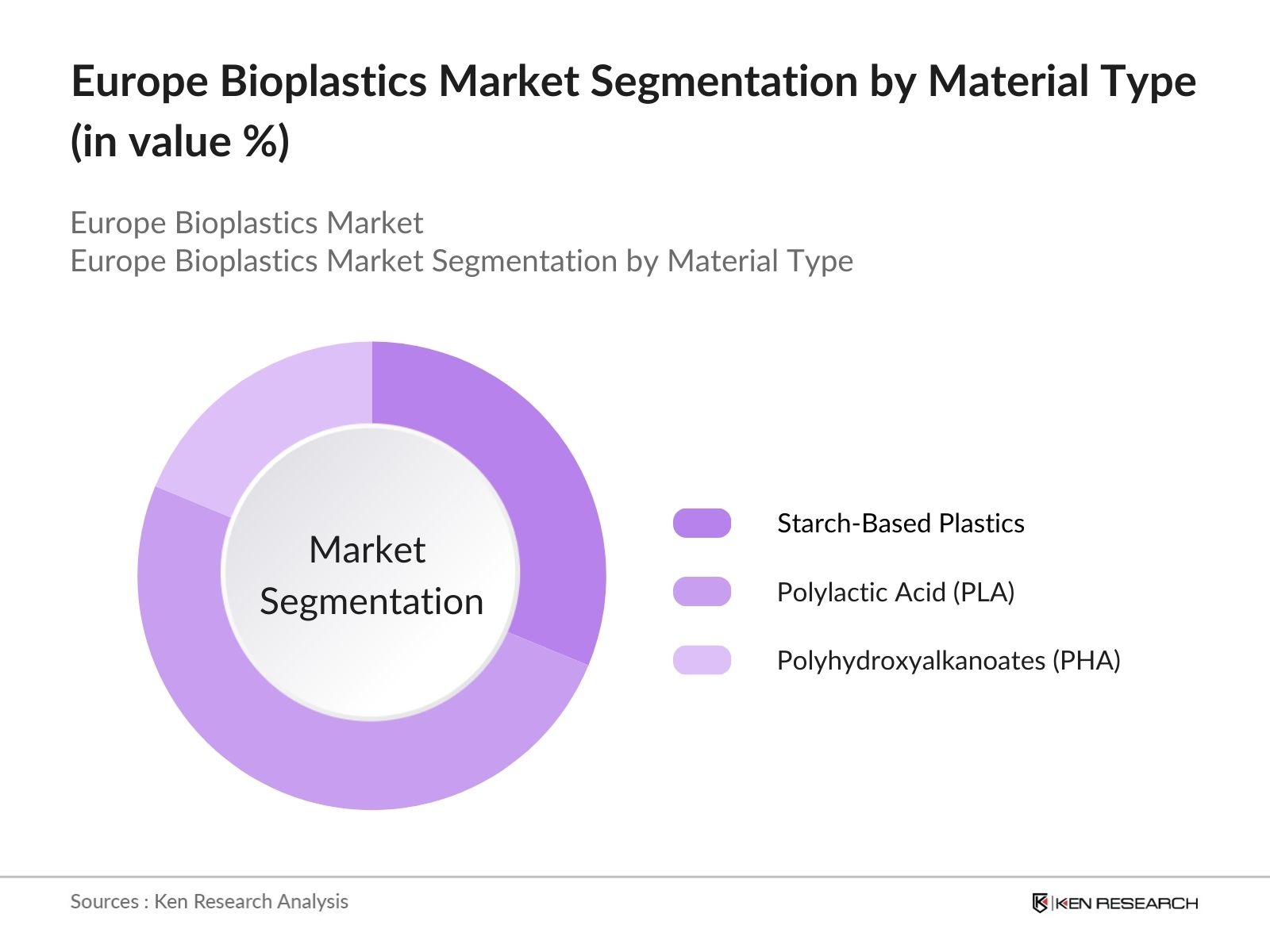

By Material Type: The Europe Bioplastics market is segmented by material type into starch-based plastics, polylactic acid (PLA), polyhydroxyalkanoates (PHA), and bio-polyethylene (Bio-PE). Among these, PLA is gaining significant traction due to its biodegradability and versatility in applications such as packaging and consumer goods. Major corporations are increasingly adopting PLA to meet sustainability goals and regulatory requirements, pushing this material type to hold the largest share in the market.

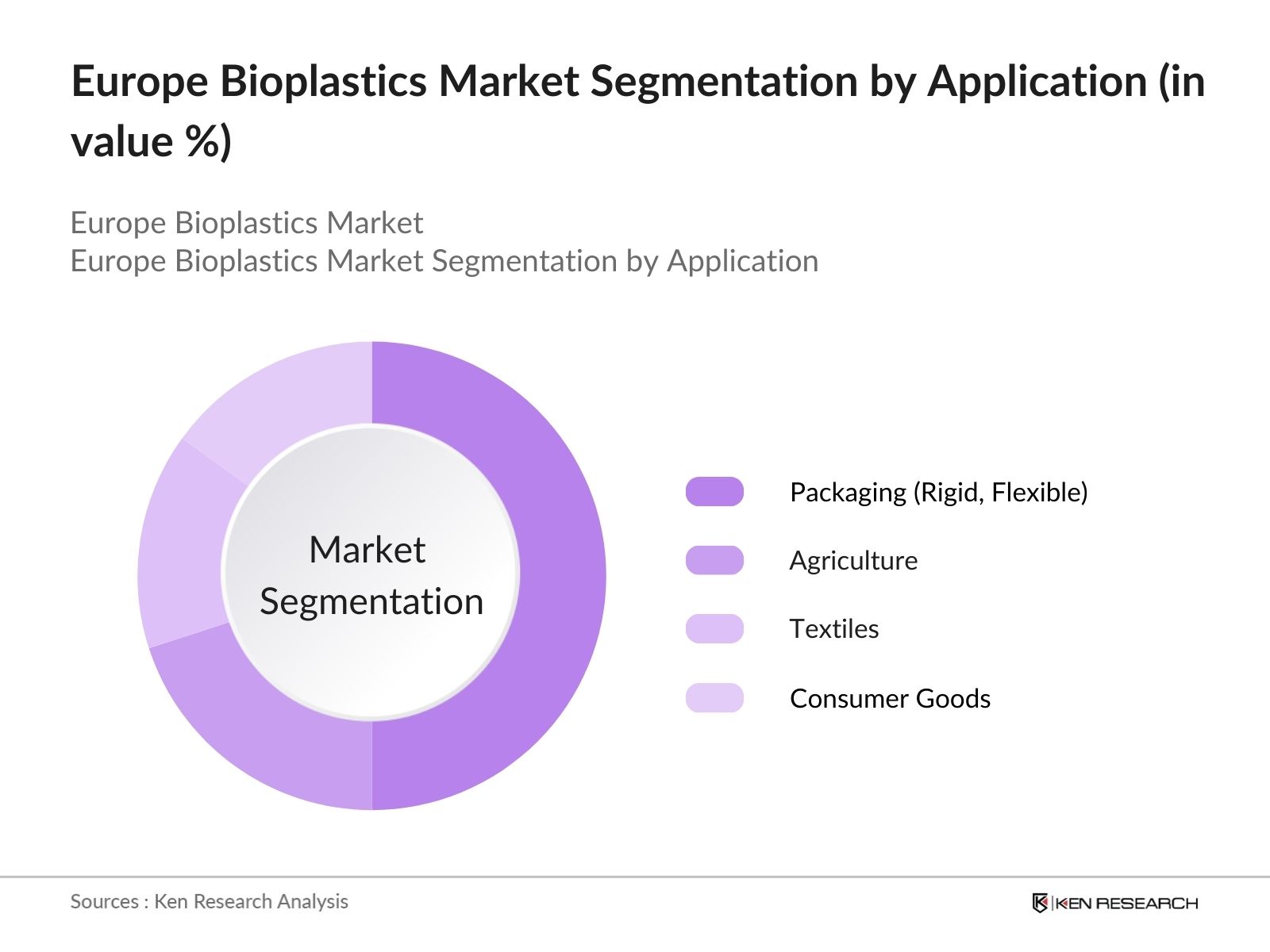

By Application: The bioplastics market in Europe is segmented by application into packaging (rigid and flexible), agriculture, textiles, and consumer goods. Packaging, particularly in the food and beverage sector, has the largest market share due to stringent regulations on single-use plastics. The increasing demand for sustainable packaging solutions in retail and consumer products has led to widespread adoption of bioplastics in this segment.

Europe Bioplastics Market Competitive Landscape

The Europe Bioplastics market is characterized by the presence of key players who are heavily investing in research and development to bring innovative, sustainable bioplastics solutions to the market. These companies are leveraging partnerships and strategic collaborations to expand their footprint. NatureWorks LLC, and Total Corbion PLA, who continue to strengthen their positions through innovation and collaborations with research institutions. This has led to a highly competitive environment, driving the advancement of bio-based polymers and increasing production capacities.

Europe Bioplastics Market Analysis

Growth Drivers

- Consumer Shift to Eco-friendly Products: The growing awareness among European consumers about the environmental impact of plastic waste has significantly increased the demand for eco-friendly products. Consumers are now opting for biodegradable and compostable alternatives, driving demand for bioplastics. A Eurobarometer survey showed that 87% of EU citizens are concerned about the environmental effects of plastics, and this sentiment has pushed industries to adopt greener materials like bioplastics.

- EU Green Deal and Legislative Support: The EU Green Deal, which aims to make Europe the first climate-neutral continent by 2050, is a critical driver for the bioplastics market. The legislation encourages the use of sustainable materials and imposes stricter regulations on non-biodegradable plastics, fostering growth in the bioplastics sector. The EU Circular Economy Action Plan, part of the Green Deal, also promotes sustainable materials, thereby encouraging investment in biodegradable and bio-based plastics.

- Advancements in Biodegradable Polymers: Significant technological advancements in biodegradable polymers like polylactic acid (PLA) and polyhydroxyalkanoates (PHA) are driving growth in the bioplastics market. These materials have become increasingly viable due to improvements in mechanical properties, processing capabilities, and environmental benefits. The European Bioplastics Association noted that over 60% of bioplastic production in Europe is dedicated to innovative biodegradable materials, ensuring a competitive edge in various sectors.

Challenges

- High Production Costs: Bioplastics production remains significantly more expensive compared to conventional plastics. Factors such as the cost of raw materials, limited economies of scale, and the relatively complex production processes contribute to these high costs. A report by the European Union on industrial bioplastics noted that production costs could be up to 50% higher than petroleum-based plastics, posing a substantial challenge for wider market adoption, particularly in cost-sensitive sectors.

- Limited Industrial Composting Infrastructure: The lack of sufficient industrial composting infrastructure in Europe poses a significant hurdle for the bioplastics market. While bioplastics are compostable, many countries lack the necessary facilities to manage their end-of-life processing. A study by the European Compost Network (ECN) found that only 25% of the EUs waste management facilities are equipped to handle compostable plastics, slowing the adoption of bioplastics, especially in regions with inadequate composting systems.

Europe Bioplastics Market Future Outlook

Europe Bioplastics market is expected to experience substantial growth. This growth will be driven by the increasing pressure from governments and environmental groups to adopt sustainable solutions, technological advancements in bioplastic materials, and rising consumer awareness regarding eco-friendly products. The ongoing innovation in biodegradable materials, along with the rising need for compostable packaging, is set to reshape the landscape of the bioplastics industry in Europe. Furthermore, major manufacturers are expanding their production capacities to meet growing demand, indicating a promising future for the market.

Market Opportunities

- Growth of Bio-based PET and PHA Markets: The bio-based polyethylene terephthalate (PET) and polyhydroxyalkanoates (PHA) markets are rapidly growing, providing substantial opportunities for innovation and commercialization. Bio-based PET, used predominantly in the packaging industry, is gaining traction as companies seek sustainable alternatives. Additionally, PHA, a biodegradable polymer, is experiencing increased demand due to its versatility in various applications. According to the European Bioplastics Association, bio-based PET production capacity is expected to grow by over 30% between 2023 and 2025, offering significant market opportunities.

- Increasing Demand in Packaging and Agriculture Sectors: Bioplastics are witnessing growing demand in the packaging and agricultural sectors, where their environmental benefits are crucial. The European bioplastics market is expected to expand rapidly in food packaging due to the push for reducing plastic waste. In agriculture, bioplastics are increasingly used for mulch films, which biodegrade and prevent soil contamination. According to a report by the European Commission, these two sectors alone could account for 40% of bioplastics demand in the next five years, presenting a significant growth opportunity.

Scope of the Report

|

Segment |

Sub-segment |

|

Material Type |

Starch-Based Plastics |

|

Polylactic Acid (PLA) |

|

|

Polyhydroxyalkanoates (PHA) |

|

|

Bio-Polyethylene (Bio-PE) |

|

|

Application |

Packaging (Rigid, Flexible) |

|

Agriculture |

|

|

Textiles |

|

|

Consumer Goods |

|

|

End-Use Industry |

Food and Beverage Packaging |

|

Automotive and Transportation |

|

|

Healthcare and Pharmaceuticals |

|

|

Agriculture and Horticulture |

|

|

Processing Method |

Injection Molding |

|

Blow Molding |

|

|

Thermoforming |

|

|

Country |

Germany |

|

France |

|

|

Italy |

|

|

United Kingdom |

|

|

Spain |

Products

Key Target Audience

Bioplastics Manufacturers

Packaging Companies

Food and Beverage Companies

Automotive Manufacturers

Agriculture Industry Stakeholders

Consumer Goods Companies

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (European Commission, Environmental Ministries)

Companies

Players Mentioned in the Report:

BASF SE

NatureWorks LLC

Total Corbion PLA

Novamont S.p.A

Danimer Scientific

Braskem

Futerro SA

Avantium N.V.

Biome Bioplastics

Cardia Bioplastics

Table of Contents

1. Europe Bioplastics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Bioplastics Industry Landscape

1.4. Market Segmentation Overview

2. Europe Bioplastics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Developments and Market Milestones

3. Europe Bioplastics Market Analysis

3.1. Growth Drivers (Sustainability, Environmental Regulations, Circular Economy)

3.1.1. Consumer Shift to Eco-friendly Products

3.1.2. EU Green Deal and Legislative Support

3.1.3. Advancements in Biodegradable Polymers

3.2. Market Challenges (Cost Competitiveness, Performance Limitations)

3.2.1. High Production Costs

3.2.2. Limited Industrial Composting Infrastructure

3.3. Opportunities (Innovation, Public-Private Partnerships, New Material Development)

3.3.1. Growth of Bio-based PET and PHA Markets

3.3.2. Increasing Demand in Packaging and Agriculture Sectors

3.4. Trends (Sustainable Packaging, Consumer Preferences)

3.4.1. Emergence of Bio-based Polymers in Automotive Sector

3.4.2. Partnerships for Bioplastics Innovations

3.5. Government Regulation (EU Directives, National Action Plans)

3.5.1. EU Directive on Single-Use Plastics

3.5.2. National Policies Encouraging Compostable Plastics

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Europe Bioplastics Market Segmentation

4.1. By Material Type (In Value %)

4.1.1. Starch-Based Plastics

4.1.2. Polylactic Acid (PLA)

4.1.3. Polyhydroxyalkanoates (PHA)

4.1.4. Bio-Polyethylene (Bio-PE)

4.2. By Application (In Value %)

4.2.1. Packaging (Rigid, Flexible)

4.2.2. Agriculture

4.2.3. Textiles

4.2.4. Consumer Goods

4.3. By End-Use Industry (In Value %)

4.3.1. Food and Beverage Packaging

4.3.2. Automotive and Transportation

4.3.3. Healthcare and Pharmaceuticals

4.3.4. Agriculture and Horticulture

4.4. By Processing Method (In Value %)

4.4.1. Injection Molding

4.4.2. Blow Molding

4.4.3. Thermoforming

4.5. By Country (In Value %)

4.5.1. Germany

4.5.2. France

4.5.3. Italy

4.5.4. United Kingdom

4.5.5. Spain

5. Europe Bioplastics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. NatureWorks LLC

5.1.2. BASF SE

5.1.3. Total Corbion PLA

5.1.4. Novamont S.p.A

5.1.5. Danimer Scientific

5.1.6. Futerro SA

5.1.7. Avantium N.V.

5.1.8. Braskem

5.1.9. Cardia Bioplastics

5.1.10. Biome Bioplastics

5.2. Cross Comparison Parameters (Headquarters, Inception Year, Production Capacity, Sustainability Certifications, Number of Patents, R&D Investment, Market Presence, Revenue)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment and Funding Analysis

6. Europe Bioplastics Market Regulatory Framework

6.1. EU Environmental Legislation

6.2. Certifications and Labelling Standards

6.3. Compliance and Recycling Requirements

7. Europe Bioplastics Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Europe Bioplastics Future Market Segmentation

8.1. By Material Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-Use Industry (In Value %)

8.4. By Processing Method (In Value %)

8.5. By Country (In Value %)

9. Europe Bioplastics Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Product Innovation Opportunities

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This phase focuses on mapping the bioplastics ecosystem in Europe, identifying key stakeholders such as manufacturers, regulatory bodies, and end-use industries. Extensive desk research and proprietary databases are utilized to gather critical variables influencing market dynamics.

Step 2: Market Analysis and Construction

The historical data on bioplastics production, demand, and technological advancements are analyzed to construct a robust market model. This includes a detailed evaluation of market penetration and bioplastics adoption across various sectors, ensuring accuracy in market projections.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding the markets future growth potential are validated through consultations with industry experts, including manufacturers, regulators, and sustainability consultants. These insights provide valuable input for refining the market analysis.

Step 4: Research Synthesis and Final Output

The final synthesis involves gathering insights from bioplastics manufacturers to refine the data. This step ensures a comprehensive understanding of the market, validated through a combination of primary and secondary research sources.

Frequently Asked Questions

01. How big is the Europe Bioplastics Market?

The Europe Bioplastics market is valued at USD 3 billion, driven by environmental concerns, stringent government regulations, and consumer demand for sustainable packaging solutions.

02. What are the challenges in the Europe Bioplastics Market?

Challenges in Europe Bioplastics market include high production costs, limited industrial composting infrastructure, and the lack of scalability of certain bioplastic materials compared to conventional plastics.

03. Who are the major players in the Europe Bioplastics Market?

Key players in Europe Bioplastics market include BASF SE, NatureWorks LLC, Total Corbion PLA, and Novamont S.p.A. These companies lead the market through significant investments in R&D and strategic partnerships.

04. What are the growth drivers of the Europe Bioplastics Market?

Europe Bioplastics market is propelled by rising environmental concerns, government regulations banning single-use plastics, and advancements in bioplastic technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.