Europe Cat Food Market Outlook to 2030

Region:France

Author(s):Sanjeev

Product Code:KROD1820

Region:France

Author(s):Sanjeev

Product Code:KROD1820

September 2024

85

Listen to the audio summary

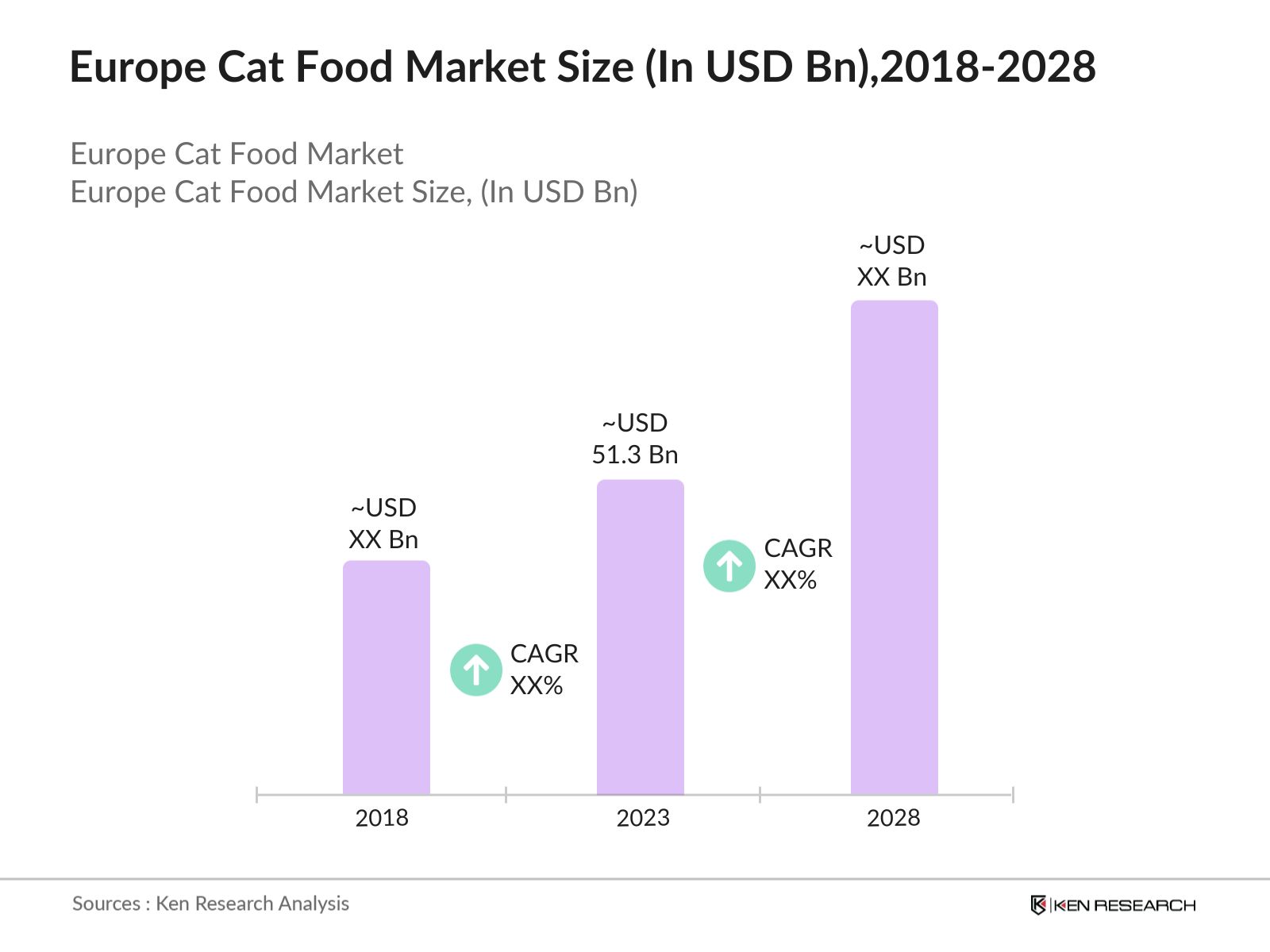

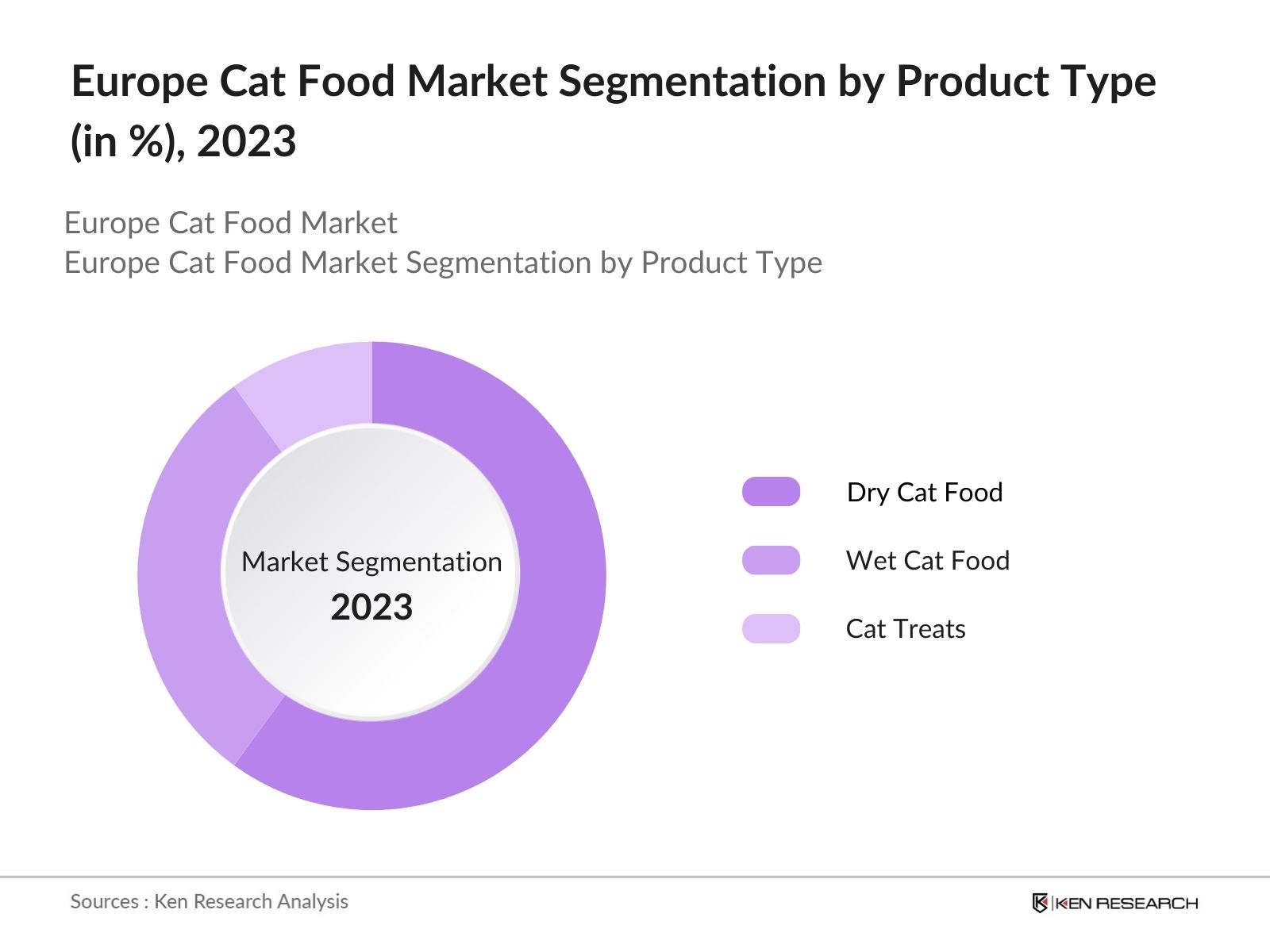

The Europe Cat Food Market was valued at USD 51.3 billion in 2023, driven by the increasing number of pet cat ownership, the growing trend of pet humanization, and a rising awareness of the importance of nutrition in pet diets. The market is segmented into dry cat food, wet cat food, and cat treats, with dry cat food being the most dominant due to its convenience and affordability.

The Europe Cat Food Market can be segmented by product type, sales channel, and region:

By Product Type: The market is segmented into dry cat food, wet cat food, and cat treats. In 2023, dry cat food remains the most dominant product type due to its convenience and longer shelf life. However, wet cat food is gaining popularity for its higher moisture content, which is beneficial for cats' hydration, especially in older cats. The demand for cat treats is also on the rise, driven by increasing consumer interest in pet training and indulgence.

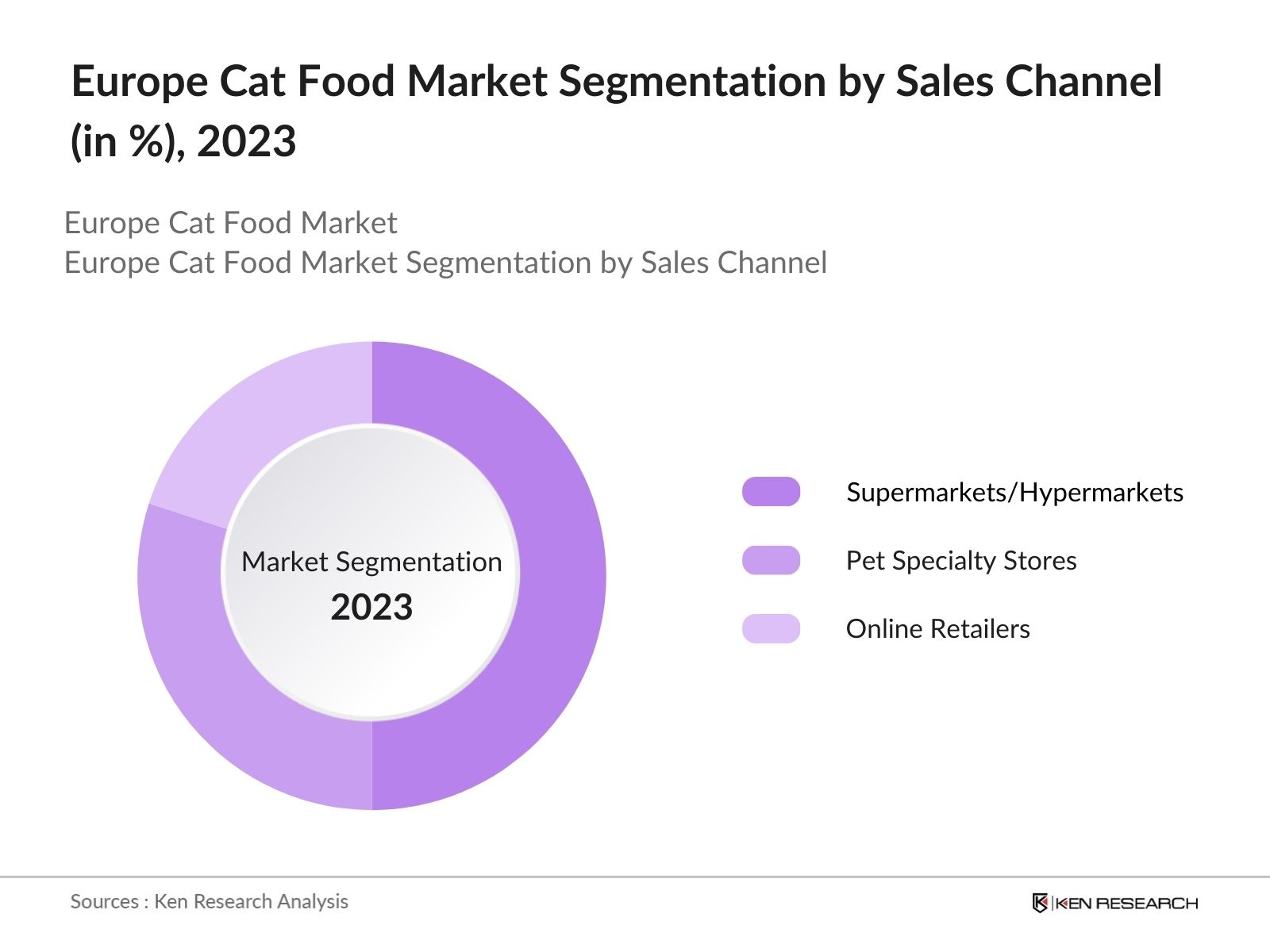

By Sales Channel: The market is segmented by sales channel into supermarkets/hypermarkets, pet specialty stores, and online retailers. In 2023, supermarkets and hypermarkets dominate the market due to their wide reach and availability of a variety of brands. However, online retailers are rapidly growing in market share, driven by the convenience of home delivery and the ability to access a wide range of products. Pet specialty stores also hold a significant share, catering to the demand for premium and specialized cat food.

By Region: The Europe market is segmented regionally into West, East, North, and South. In 2023, Western Europe leads the market due to high disposable incomes, a strong preference for premium pet food, and a large population of pet owners. Northern Europe is also a significant market, driven by the high levels of pet ownership and the demand for organic and sustainable cat food options.

|

Company |

Establishment Year |

Headquarters |

|

Mars Petcare |

1932 |

McLean, USA |

|

Nestlé Purina |

1894 |

St. Louis, USA |

|

Hill's Pet Nutrition |

1907 |

Topeka, USA |

|

Royal Canin |

1968 |

Aimargues, France |

|

Blue Buffalo |

2002 |

Wilton, USA |

European Union’s Farm to Fork Strategy: The European Union's Farm to Fork Strategy, a core component of the European Green Deal, aims to make food systems fair, healthy, and environmentally-friendly. With a budget of EUR 10 billion which is USD 11 billion, the strategy includes specific initiatives to promote sustainable and organic farming practices, which directly impact the pet food industry. The strategy encourages the production and consumption of organic cat food, aligning with the rising consumer demand for natural and sustainably sourced pet products. This initiative is expected to drive innovation and sustainability within the cat food market, pushing companies to adopt more eco-friendly practices.

The Europe Cat Food Market is expected to continue its steady growth, driven by the increasing trend of pet humanization, the expansion of e-commerce, and innovation in product offerings.

|

By Region |

West East North South |

|

By Sales Channel |

Supermarkets/Hypermarkets Pet Specialty Stores Online Retailers |

|

By Price Segment |

Economy Mid-range Premium |

|

By Product Type |

Dry Cat Food Wet Cat Food Cat Treats |

|

By Packaging Type |

Cans Pouches Bags Trays |

Historical Period: 2018-2023

Players Mentioned in the Report:

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Pet Ownership

3.1.2. Trend of Pet Humanization

3.1.3. Innovation in Cat Food Products

3.2. Restraints

3.2.1. Rising Raw Material Costs

3.2.2. Regulatory Constraints

3.2.3. Increasing Competition

3.3. Opportunities

3.3.1. Technological Advancements

3.3.2. Expansion into New Markets

3.3.3. Growing Demand for Organic Products

3.4. Trends

3.4.1. Growth of Subscription-based Services

3.4.2. Increased Focus on Pet Health

3.4.3. Integration of Functional Ingredients

3.5. Government Regulation

3.5.1. European Union’s Farm to Fork Strategy

3.5.2. Germany’s National Program for Sustainable Animal Nutrition

3.5.3. Sustainable Packaging Initiatives

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competitive Ecosystem

4.1. By Product Type (in Value %)

4.1.1. Dry Cat Food

4.1.2. Wet Cat Food

4.1.3. Cat Treats

4.2. By Sales Channel (in Value %)

4.2.1. Supermarkets/Hypermarkets

4.2.2. Pet Specialty Stores

4.2.3. Online Retailers

4.3. By Region (in Value %)

4.3.1. Western Europe

4.3.2. Eastern Europe

4.3.3. Northern Europe

4.3.4. Southern Europe

4.4. By Price Segment (in Value %)

4.4.1. Economy

4.4.2. Mid-range

4.4.3. Premium

4.5. By Packaging Type (in Value %)

4.5.1. Cans

4.5.2. Pouches

4.5.3. Bags

4.5.4. Trays

5.1 Detailed Profiles of Major Companies

5.1.1. Mars Petcare

5.1.2. Nestlé Purina

5.1.3. Hill's Pet Nutrition

5.1.4. Royal Canin

5.1.5. Blue Buffalo

5.1.6. Whiskas

5.1.7. Felix

5.1.8. Applaws

5.1.9. Perfect Fit

5.1.10. IAMS

5.1.11. Sheba

5.1.12. Arden Grange

5.1.13. Acana

5.1.14. Almo Nature

5.1.15. James Wellbeloved

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Product Type (in Value %)

9.2. By Sales Channel (in Value %)

9.3. By Region (in Value %)

9.4. By Price Segment (in Value %)

9.5. By Packaging Type (in Value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

We begin by referencing multiple secondary and proprietary databases to conduct desk research. This includes gathering industry-level information on market drivers, challenges, key players, consumer behavior, and nutritional trends. We also assess regulatory impacts and market dynamics specific to the European market.

We collect historical data on market size, growth rates, product segmentation (dry cat food, wet cat food, and cat treats), and the distribution of sales channels (supermarkets, online, pet specialty stores). We also analyze market share and revenue generated by leading brands, emerging trends in pet food nutrition, and consumer preferences to ensure accuracy and reliability in the data presented.

We perform Computer-Assisted Telephone Interviews (CATIs) with industry experts, including representatives from leading pet food manufacturers, distributors, and retailers. These interviews validate the statistics collected and provide insights into operational and financial aspects, such as pricing strategies, supply chain management, and consumer buying patterns.

Our team interacts with cat food manufacturers, veterinarians, pet owners, and market analysts to understand the dynamics of market segments, evolving consumer preferences, and sales trends. This process helps validate the derived statistics using a bottom-to-top approach, ensuring that the final data accurately reflects the actual market conditions.

In 2023, the Europe Cat Food Market was valued at approximately USD 51.3 billion. The market's growth is driven by the increasing number of pet cat ownership, rising awareness of pet nutrition, and the trend of pet humanization, which encourages spending on premium and specialized cat food products.

Challenges in the Europe Cat Food Market include rising raw material costs, which affect pricing and profit margins for manufacturers, as well as stringent regulatory requirements for product safety and labeling. Additionally, competition among established brands and new entrants, along with the increasing demand for sustainable and organic products, poses significant challenges.

Major players in the Europe Cat Food Market include Mars Petcare, Nestlé Purina, Hill's Pet Nutrition, Royal Canin, and Blue Buffalo. These companies lead the market with extensive product portfolios, strong brand recognition, and continuous innovation in cat food formulations.

Key growth drivers include the growing trend of pet humanization, which leads to increased spending on high-quality, nutritionally balanced cat food. The expansion of e-commerce platforms and the rise in online shopping for pet products also contribute to market growth. Additionally, innovations in cat food formulations, such as functional foods targeting specific health issues, are fueling demand.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.