Europe Clinical Trials Market Outlook to 2030

Region:Global

Author(s):Shreya

Product Code:KROD3313

October 2024

93

About the Report

Europe Clinical Trials Market Overview

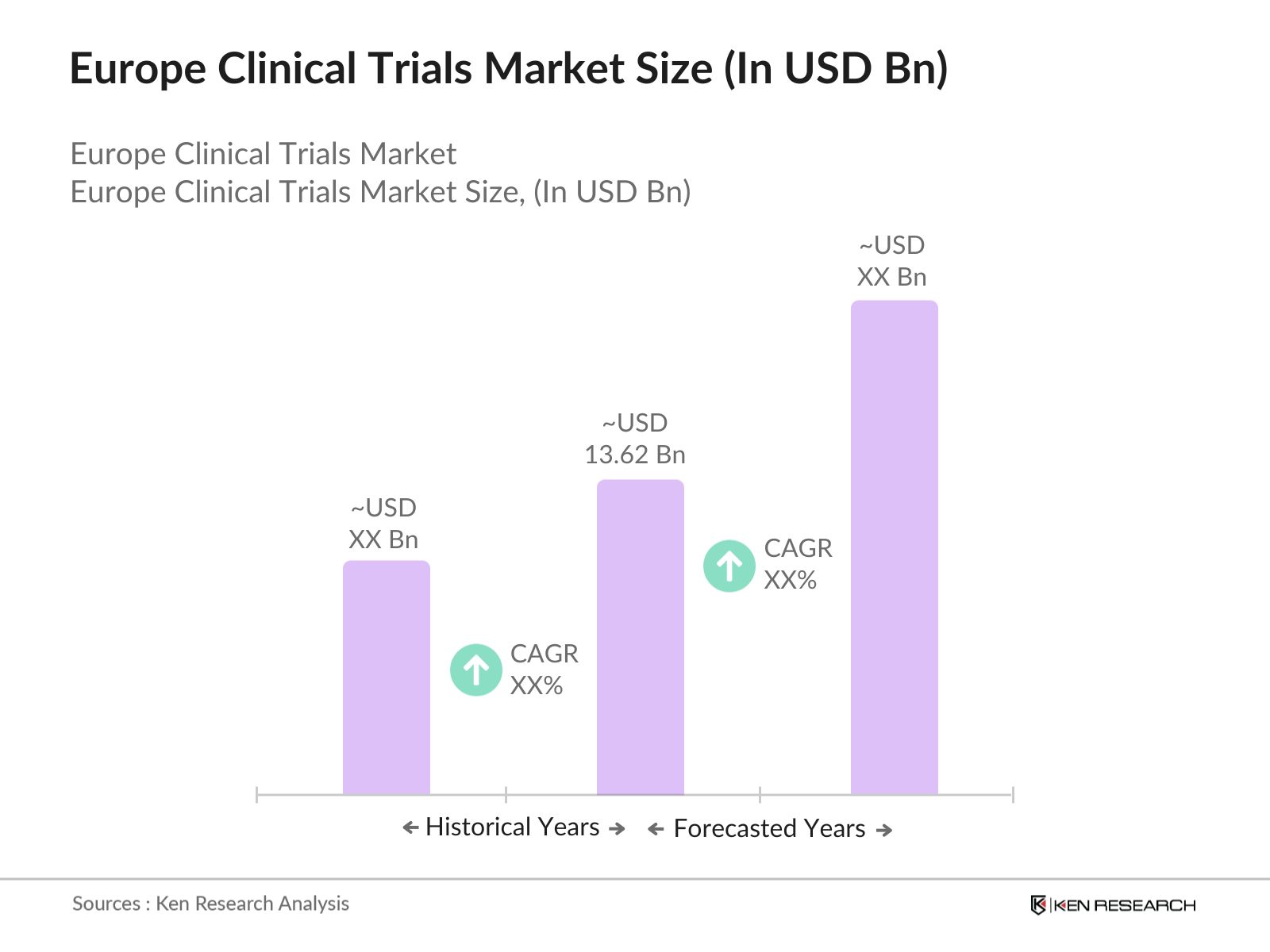

- The Europe Clinical Trials market is valued at USD 13.62 billion, based on a detailed five-year historical analysis. The market is primarily driven by the significant rise in pharmaceutical and biotechnology research across the region, coupled with the growing number of chronic diseases such as cancer and cardiovascular conditions. Additionally, increasing patient recruitment for personalized medicines and the adoption of new trial designs have accelerated growth, with technological advancements like artificial intelligence and big data also playing a crucial role in streamlining trial processes.

- Dominant countries in the Europe Clinical Trials market include Germany, the United Kingdom, and France. Germany leads the market due to its robust healthcare infrastructure, strong pharmaceutical industry, and government support for clinical research. The UK remains a key player, driven by its favorable regulatory environment post-Brexit, while France has become a hub due to its increasing investments in healthcare and R&D. These countries also benefit from highly skilled workforces and advanced medical facilities, which support the execution of complex clinical trials.

- The EU Clinical Trials Regulation (CTR), which came into full effect in January 2022, aims to harmonize the approval process for clinical trials across Europe. By 2024, the CTR has reduced trial approval times by an average of 25 days, enhancing the speed of clinical research in the region. The regulation also requires greater transparency in trial results, making it easier for researchers and the public to access data. The centralized portal for clinical trial submissions has simplified the administrative process, benefiting both sponsors and regulatory authorities.

Europe Clinical Trials Market Segmentation

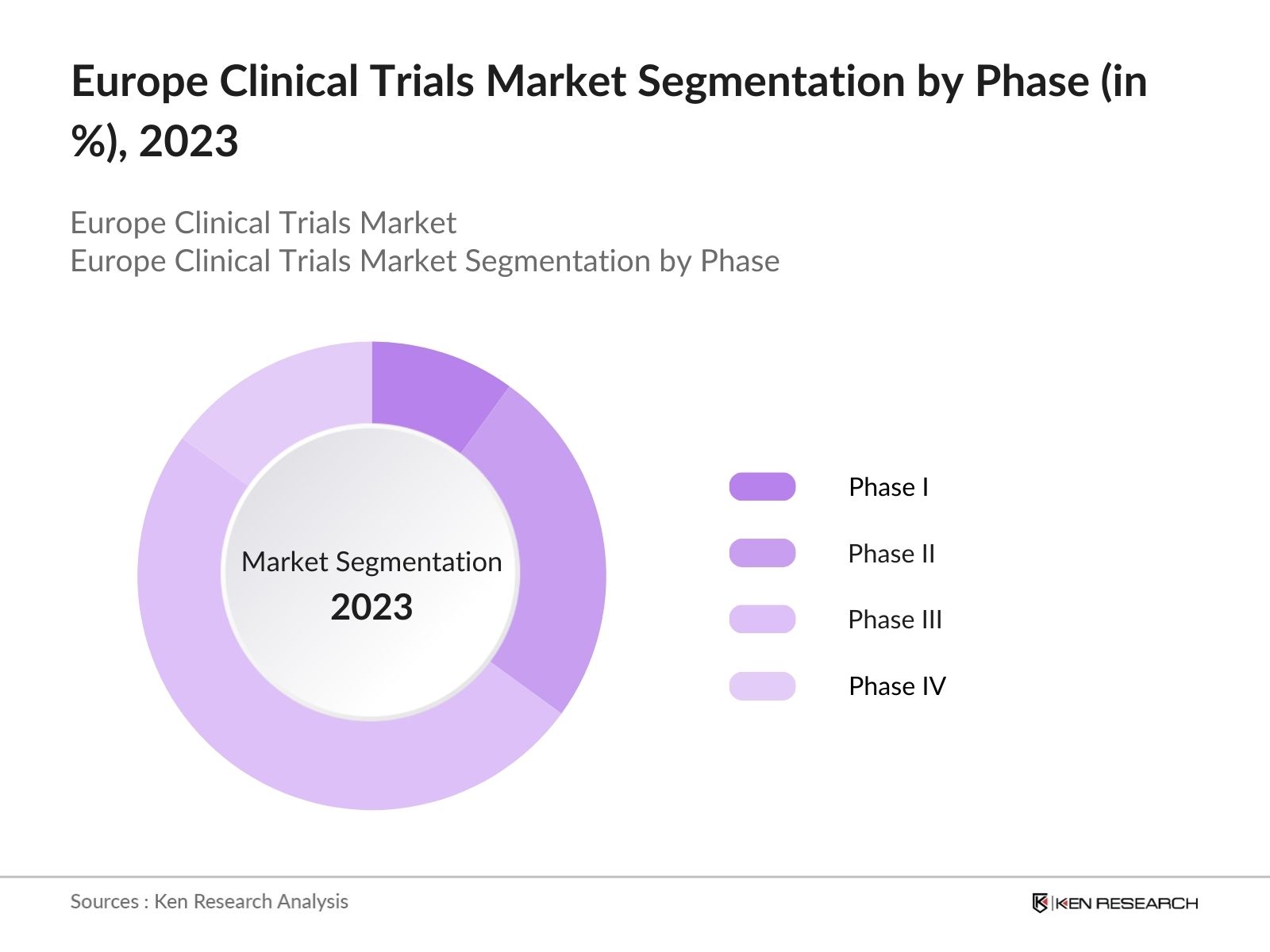

- By Phase: The market is segmented by trial phase into Phase I, Phase II, Phase III, and Phase IV. Recently, Phase III trials have dominated the market, as they require extensive patient recruitment and involve large-scale testing to determine the efficacy and safety of new treatments. Pharmaceutical companies focus more on this phase because it is critical for the approval of new drugs by regulatory authorities. The high cost and complexity of Phase III trials contribute significantly to their dominant market share.

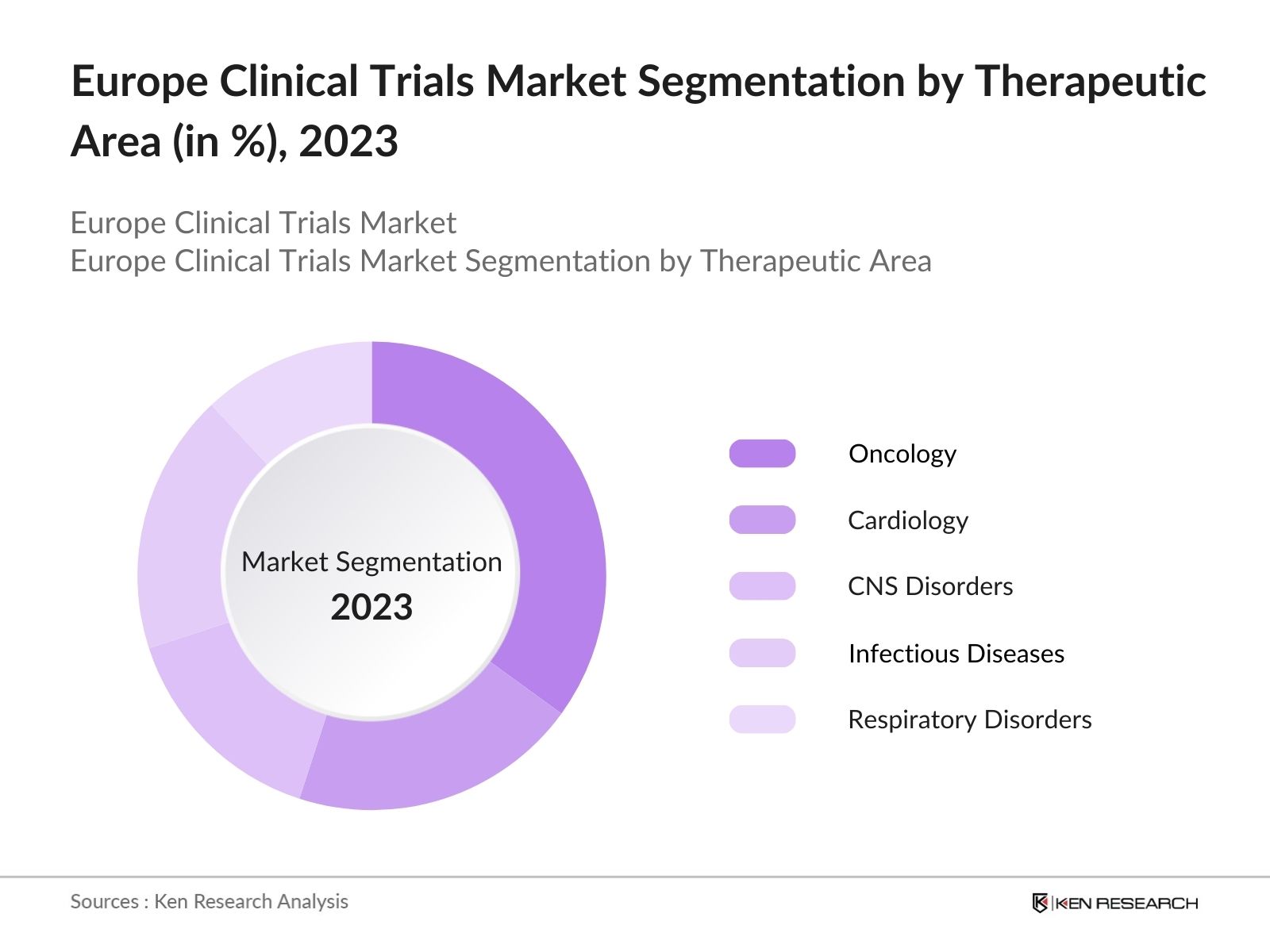

- By Therapeutic Area: The market is also segmented by therapeutic area into oncology, cardiology, central nervous system (CNS) disorders, infectious diseases, and respiratory disorders. Oncology remains the leading sub-segment due to the increasing number of cancer cases in Europe, which drives the demand for innovative treatments and therapies. Clinical trials in oncology are more frequent and longer, with multiple endpoints to assess the effectiveness of drugs in treating various cancer types, making it a high-demand area for clinical trials.

Europe Clinical Trials Market Competitive Landscape

The Europe Clinical Trials market is dominated by both global and local companies, highlighting the competitive landscape's consolidation. Several key players are involved in contract research organizations (CROs) and full-service clinical trial solutions. The market sees active participation from pharmaceutical giants and biotech firms collaborating with CROs to expedite drug development processes. Additionally, players like Syneos Health and Covance have grown by diversifying their service offerings and focusing on therapeutic areas such as CNS disorders and cardiology, which are seeing increased trial activities.

|

Company Name |

Establishment Year |

Headquarters |

Therapeutic Focus |

No. of Employees |

Revenue (USD Bn) |

No. of Active Trials |

Global Presence |

Collaboration Network |

Regulatory Certifications |

|---|---|---|---|---|---|---|---|---|---|

|

ICON PLC |

1990 |

Ireland |

|||||||

|

IQVIA |

1982 |

USA |

|||||||

|

Syneos Health |

1998 |

USA |

|||||||

|

Covance |

1968 |

USA |

|||||||

|

Charles River Laboratories |

1947 |

USA |

Europe Clinical Trials Industry Analysis

Growth Drivers

- Rising Healthcare Investments: The Europe clinical trials market is benefiting from increases in healthcare investments. In 2023, the European Unions Horizon Europe Program allocated over 7 billion for health-related research, focusing on clinical trials and medical innovations. These investments are boosting clinical trials by providing the necessary funding for both public and private sectors. Countries like Germany and France have set aside substantial portions of their healthcare budgets for clinical research, with Germany alone contributing 3.5 billion towards health research in 2024. These funds are crucial for advancing new therapies and improving patient care outcomes.

- Increased Demand for Personalized Medicine: The demand for personalized medicine is growing rapidly, driven by the increasing availability of genetic data and advanced technologies. In 2024, over 1,200 clinical trials related to personalized medicine are active across Europe, a sharp rise from 900 trials in 2022. With countries like the UK and Switzerland leading in genomic research, the need for targeted treatments is pushing clinical trials into specialized fields like oncology and rare diseases. Personalized treatments, particularly in cancer therapies, are a key area of focus, influencing the clinical trial landscape.

- Government Funding for Clinical Research: In 2023, European governments collectively contributed more than 2.7 billion to clinical research, particularly in areas like oncology, rare diseases, and vaccines. Germanys Federal Ministry of Education and Research (BMBF) alone allocated 570 million for clinical trials related to infectious diseases and cancer therapies. This substantial public funding enables the initiation of numerous clinical trials, particularly in emerging fields such as immunotherapy and gene editing. These government-supported initiatives are vital to fostering medical innovations and expediting the introduction of new treatments in the market.

Market Challenges

- High Operational Costs: Operating clinical trials in Europe is often hindered by high costs. In 2024, the average cost of conducting a phase III clinical trial in Europe is estimated at approximately 20 million, with significant expenditures in labor, compliance, and technology. This financial burden is especially challenging for smaller biotech companies, limiting their ability to bring innovative therapies to market. Moreover, the rising inflation rates in key European economies like Germany (4.6% in 2023) contribute to escalating operational expenses, adding further strain on clinical research budgets.

- Regulatory Hurdles Across Regions: Europes fragmented regulatory environment poses a challenge for clinical trials, with each country having different rules and approval processes. In 2024, the average time to obtain clinical trial approval in the EU varies between 60 to 90 days, depending on the member state, with additional delays from varying ethical and safety assessments. Despite the EU Clinical Trials Regulation aiming to streamline this process, many trials still face delays due to bureaucratic bottlenecks. These regulatory discrepancies increase costs and extend the time needed to bring new therapies to market.

Europe Clinical Trials Market Future Outlook

Over the next five years, the Europe Clinical Trials market is expected to show substantial growth, driven by continuous advancements in clinical trial technologies, such as the use of artificial intelligence, remote monitoring, and decentralized trials. Moreover, increased government funding for research and development, coupled with the rising demand for personalized and precision medicine, will further support market growth. Patient-centric approaches and the integration of real-world data will also play a crucial role in shaping the future of clinical trials across Europe.

Future Market Opportunities

- Growing Adoption of Decentralized Trials: Decentralized clinical trials (DCTs) are gaining traction in Europe, with over 700 trials adopting this model in 2023. DCTs allow trials to be conducted remotely, reducing the need for physical site visits and enabling wider patient participation. The European Medicines Agency (EMA) has endorsed the use of decentralized methods, particularly in rare disease and oncology trials, where patient recruitment can be challenging. By 2024, it is estimated that nearly 25% of all new trials in Europe will use decentralized models, providing an efficient alternative to traditional trial frameworks.

- Emergence of Patient-Centric Trials: Patient-centric trials are transforming the clinical trial landscape in Europe by involving patients more directly in the trial process. By 2023, over 800 trials across Europe were categorized as patient-centric, emphasizing patient engagement, remote monitoring, and personalized treatment approaches. This model enhances patient recruitment and retention, as patients are more willing to participate in trials that cater to their individual needs. The rise of digital health platforms and wearable devices has further fueled the adoption of patient-centric approaches, allowing real-time monitoring and improved data accuracy.

Scope of the Report

|

Segment |

Sub-Segments |

|---|---|

|

Phase |

Phase I Phase II Phase III Phase IV |

|

Study Design |

Interventional Observational Expanded Access |

|

Therapeutic Area |

Oncology Cardiology CNS Infectious Respiratory |

|

Sponsor Type |

Pharma Biotech Academic CRO |

|

Region |

West East North South |

Products

Key Target Audience

Pharmaceutical Companies

Biotech Firms

Contract Research Organizations (CROs)

Healthcare Providers

Government and Regulatory Bodies (European Medicines Agency, UK Medicines and Healthcare products Regulatory Agency)

Banks and Financial Institues

Venture Capital and Investment Firms

Hospital Networks and Clinical Centers

Healthcare Technology Providers

Companies

List of Major Players

ICON PLC

IQVIA

Syneos Health

Covance

Charles River Laboratories

PRA Health Sciences

Medpace

Labcorp Drug Development

Parexel

SGS Life Sciences

Worldwide Clinical Trials

KCR

PSI CRO

Veristat

TFS International

Table of Contents

1. Europe Clinical Trials Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Clinical Trials Regulatory Framework

1.4. Market Segmentation Overview

2. Europe Clinical Trials Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Developments and Milestones

3. Europe Clinical Trials Market Analysis

3.1. Growth Drivers

3.1.1. Rising Healthcare Investments

3.1.2. Increased Demand for Personalized Medicine

3.1.3. Government Funding for Clinical Research

3.1.4. Rising Chronic Disease Prevalence

3.2. Market Challenges

3.2.1. High Operational Costs

3.2.2. Regulatory Hurdles Across Regions

3.2.3. Ethical and Legal Complexities

3.3. Opportunities

3.3.1. Growing Adoption of Decentralized Trials

3.3.2. Technological Advancements in Data Management (AI, Blockchain)

3.3.3. Emergence of Patient-Centric Trials

3.4. Trends

3.4.1. Increased Use of Adaptive Trial Designs

3.4.2. Integration of Real-World Data in Trials

3.4.3. Expansion of Clinical Trials in Central & Eastern Europe

3.5. Government Regulation

3.5.1. EU Clinical Trials Regulation (CTR)

3.5.2. EMA Guidelines

3.5.3. GDPR Impact on Data Collection in Trials

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Pharmaceuticals, CROs, Academic Institutes, Regulatory Bodies)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Europe Clinical Trials Market Segmentation

4.1. By Phase (In Value %)

4.1.1. Phase I

4.1.2. Phase II

4.1.3. Phase III

4.1.4. Phase IV

4.2. By Study Design (In Value %)

4.2.1. Interventional Trials

4.2.2. Observational Studies

4.2.3. Expanded Access Trials

4.3. By Therapeutic Area (In Value %)

4.3.1. Oncology

4.3.2. Cardiology

4.3.3. CNS Disorders

4.3.4. Infectious Diseases

4.3.5. Respiratory Disorders

4.4. By Sponsor Type (In Value %)

4.4.1. Pharmaceutical Companies

4.4.2. Biotech Firms

4.4.3. Government/Academic Institutes

4.4.4. Contract Research Organizations (CROs)

4.5. By Region (In Value %)

4.5.1. West

4.5.2. East

4.5.3. North

4.5.4. South

5. Europe Clinical Trials Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ICON PLC

5.1.2. IQVIA

5.1.3. Syneos Health

5.1.4. Covance

5.1.5. Charles River Laboratories

5.1.6. Medpace

5.1.7. PRA Health Sciences

5.1.8. Labcorp Drug Development

5.1.9. Parexel

5.1.10. PPD

5.1.11. SGS Life Sciences

5.1.12. Worldwide Clinical Trials

5.1.13. KCR

5.1.14. PSI CRO

5.1.15. Veristat

5.2. Cross Comparison Parameters (Therapeutic Focus, Trial Locations, Revenue, Number of Active Trials)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Europe Clinical Trials Market Regulatory Framework

6.1. EMA Approval Process

6.2. Clinical Trial Application (CTA) Processes

6.3. Compliance with ICH-GCP Guidelines

6.4. Harmonization Across EU Member States

7. Europe Clinical Trials Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Europe Clinical Trials Future Market Segmentation

8.1. By Phase (In Value %)

8.2. By Study Design (In Value %)

8.3. By Therapeutic Area (In Value %)

8.4. By Sponsor Type (In Value %)

8.5. By Region (In Value %)

9. Europe Clinical Trials Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Patient Recruitment Strategies

9.3. CRO Partnership Recommendations

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involved mapping the ecosystem of the Europe Clinical Trials market. This includes extensive desk research to gather key insights from both public and proprietary databases, focusing on stakeholders such as CROs, pharma companies, and regulatory bodies. Variables such as trial duration, patient recruitment rates, and regulatory hurdles were identified as key factors influencing the market.

Step 2: Market Analysis and Construction

We then collected historical market data and analyzed it to understand the trends and performance of different market segments. This phase included assessing clinical trial activities, trial success rates, and revenue generation across various therapeutic areas.

Step 3: Hypothesis Validation and Expert Consultation

After developing initial market hypotheses, we validated them by conducting in-depth interviews with industry experts, including trial managers, regulatory consultants, and executives from CROs. This consultation phase provided real-world insights that helped refine the market analysis and projections.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing all research findings and presenting a consolidated view of the market. By triangulating multiple sources of data, we ensured that our final report is accurate and reliable, delivering key insights that are valuable for stakeholders across the clinical trial ecosystem.

Frequently Asked Questions

01. How big is the Europe Clinical Trials Market?

The Europe Clinical Trials market is valued at USD 13.62 billion, driven by increasing investments in healthcare research and the growing prevalence of chronic diseases across the region.

02. What are the challenges in the Europe Clinical Trials Market?

Key challenges in the Europe Clinical Trials market include high operational costs, complex regulatory environments across different countries, and patient recruitment difficulties, which can delay trials.

03. Who are the major players in the Europe Clinical Trials Market?

Top players in the Europe Clinical Trials market include ICON PLC, IQVIA, Syneos Health, Covance, and Charles River Laboratories, which dominate due to their extensive trial portfolios and global operations.

04. What are the growth drivers of the Europe Clinical Trials Market?

The Europe Clinical Trials market is driven by the increasing number of pharmaceutical and biotechnology R&D projects, government support for clinical research, and the adoption of innovative trial designs, including decentralized trials.

05. What therapeutic areas dominate the Europe Clinical Trials Market?

Oncology is the dominant therapeutic area in the Europe Clinical Trials market, driven by the rising incidence of cancer and the need for innovative treatment options to combat the disease.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.