Europe Coffee Market Outlook to 2030

Region:Albania

Author(s):Paribhasha Tiwari

Product Code:KROD9495

Region:Albania

Author(s):Paribhasha Tiwari

Product Code:KROD9495

December 2024

80

Listen to the audio summary

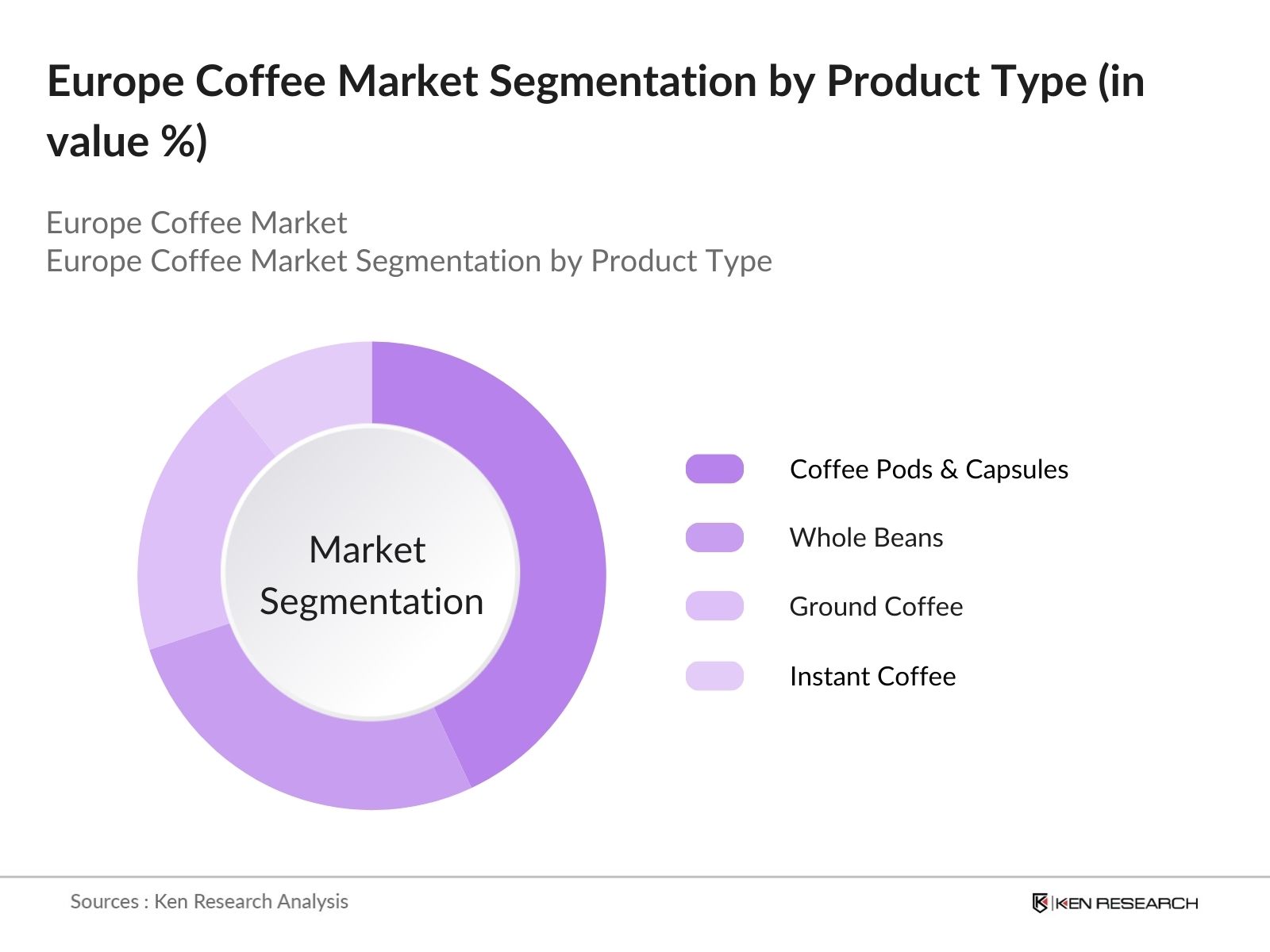

By Product Type: The Market is segmented by product type into whole beans, ground coffee, instant coffee, and coffee pods & capsules. Coffee pods and capsules dominate the market due to their convenience, consistent quality, and brand offerings that cater to diverse flavor preferences. Brands like Nespresso and Keurig have established strong market loyalty with premium products, influencing the adoption rate of this segment.

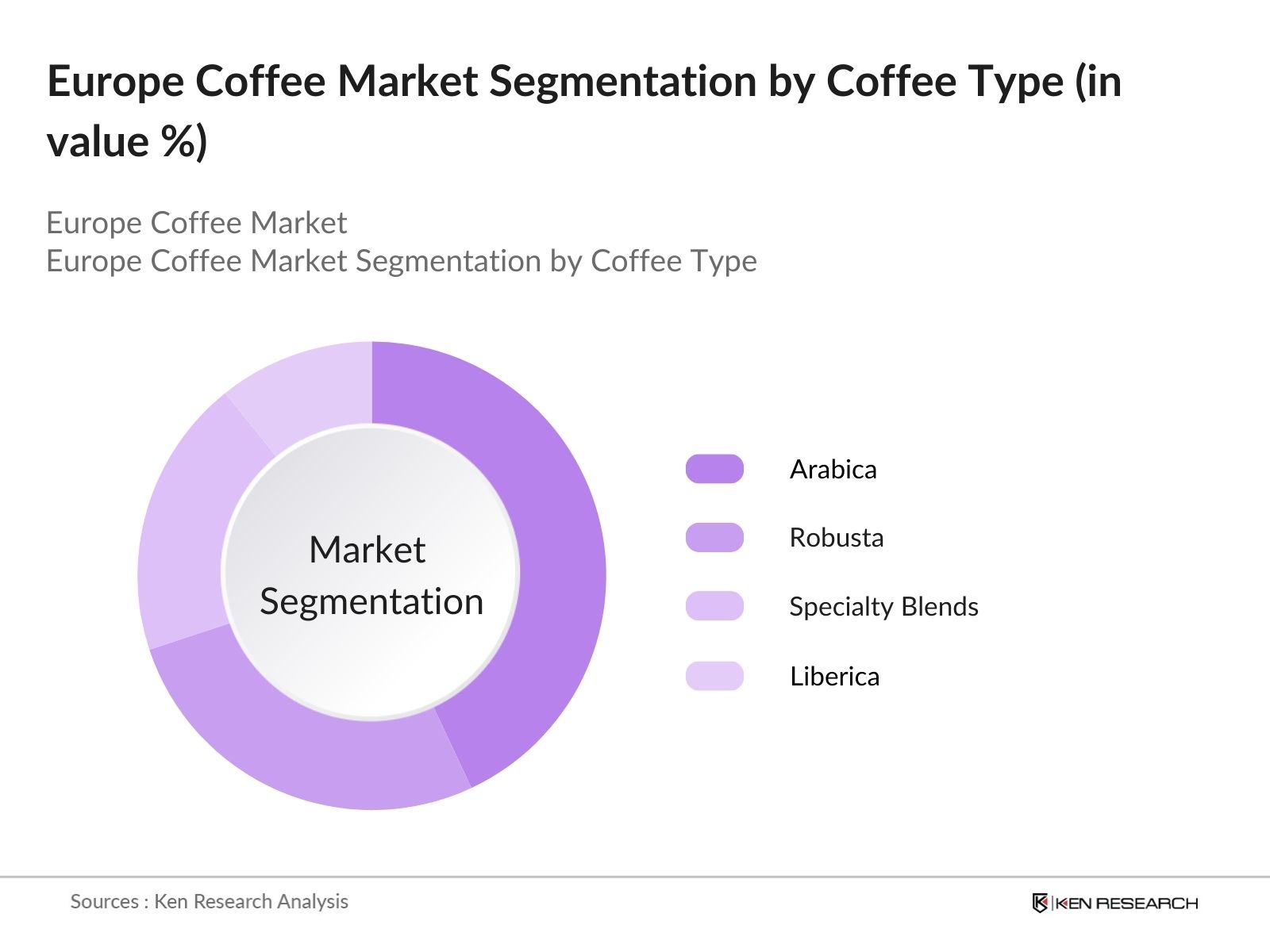

By Coffee Type: The coffee type segment includes Arabica, Robusta, Liberica, and specialty blends. Arabica coffee holds a dominant market share due to its smoother, less bitter flavor profile, which is preferred by European consumers. The increased awareness of Arabica's quality and its alignment with premium and specialty coffee trends in Europe contribute significantly to its market dominance.

The Europe Coffee Market is dominated by key players who leverage brand recognition, diversified offerings, and extensive distribution networks to maintain their positions. Companies like Nestl S.A., Lavazza Group, and Starbucks Corporation drive the market through sustained investments in premium and specialty coffee lines, innovative flavors, and strategic collaborations.

Over the next five years, the Europe Coffee Market is anticipated to experience steady growth, driven by the increasing demand for specialty coffee, the expansion of sustainable and ethically sourced coffee products, and continued innovation in brewing technologies. This growth will likely be further supported by rising health-conscious trends, with consumers increasingly opting for high-quality, organic, and environmentally friendly options.

| By Product Type |

Whole Beans Ground Coffee Instant Coffee Coffee Pods & Capsules |

| By Coffee Type |

Arabica Robusta Liberica Specialty Blends |

| By Distribution Channel |

Supermarkets & Hypermarkets Specialty Stores Online Platforms Convenience Stores Coffee Shops |

| By End User |

Household Commercial (Hotels, Restaurants, Cafés, Offices) |

| By Packaging Type |

Jars Sachets Bottles Pods Bags |

| By Region |

Germany United Kingdom France Italy Spain Netherlands Rest of Europe |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Coffee Consumption

3.1.2. Expansion of Specialty Coffee Shops

3.1.3. Rising Demand for Premium Coffee Products

3.1.4. Technological Advancements in Coffee Machines

3.2. Market Challenges

3.2.1. Fluctuating Coffee Bean Prices

3.2.2. Stringent Environmental Regulations

3.2.3. Competition from Alternative Beverages

3.2.4. Supply Chain Disruptions

3.3. Opportunities

3.3.1. Growth in Ready-to-Drink Coffee Segment

3.3.2. Expansion into Emerging European Markets

3.3.3. Development of Sustainable Coffee Products

3.3.4. Collaboration with E-commerce Platforms

3.4. Trends

3.4.1. Increasing Popularity of Organic and Fair-Trade Coffee

3.4.2. Rise in Home Brewing Practices

3.4.3. Adoption of Subscription-Based Coffee Services

3.4.4. Integration of Smart Technology in Coffee Machines

3.5. Regulatory Landscape

3.5.1. EU Food Safety Regulations

3.5.2. Import Tariffs and Trade Policies

3.5.3. Environmental Compliance Standards

3.5.4. Labeling and Packaging Requirements

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Whole Beans

4.1.2. Ground Coffee

4.1.3. Instant Coffee

4.1.4. Coffee Pods & Capsules

4.2. By Coffee Type (In Value %)

4.2.1. Arabica

4.2.2. Robusta

4.2.3. Liberica

4.2.4. Specialty Blends

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets & Hypermarkets

4.3.2. Specialty Stores

4.3.3. Online Platforms

4.3.4. Convenience Stores

4.3.5. Coffee Shops

4.4. By End User (In Value %)

4.4.1. Household

4.4.2. Commercial (Hotels, Restaurants, Cafés, Offices)

4.5. By Region (In Value %)

4.5.1. Germany

4.5.2. United Kingdom

4.5.3. France

4.5.4. Italy

4.5.5. Spain

4.5.6. Netherlands

4.5.7. Rest of Europe

5.1. Detailed Profiles of Major Companies

5.1.1. Nestlé S.A.

5.1.2. JAB Holding Company

5.1.3. Starbucks Corporation

5.1.4. Luigi Lavazza S.p.A.

5.1.5. Tchibo GmbH

5.1.6. Strauss Group Ltd.

5.1.7. The Kraft Heinz Company

5.1.8. Dunkin’ Brands Group, Inc.

5.1.9. Keurig Dr Pepper Inc.

5.1.10. Melitta Group

5.1.11. UCC Ueshima Coffee Co. Ltd.

5.1.12. Massimo Zanetti Beverage Group

5.1.13. Illycaffè S.p.A.

5.1.14. Peet’s Coffee

5.1.15. Caribou Coffee Company

5.2. Cross Comparison Parameters

5.2.1. Revenue (USD Million)

5.2.2. Market Share (%)

5.2.3. Product Portfolio Diversity

5.2.4. Distribution Network Reach

5.2.5. R&D Investment (% of Revenue)

5.2.6. Sustainability Initiatives

5.2.7. Brand Equity and Recognition

5.2.8. Digital Presence and E-commerce Integration

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Coffee Type (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value%)

The initial phase involves mapping the Europe Coffee Market ecosystem, focusing on major stakeholders including manufacturers, distributors, and end-consumers. Data is collected from secondary databases, government reports, and credible industry publications to determine influential variables in the coffee market.

In this phase, historical data on coffee consumption, retail sales, and production volumes are compiled. This includes analyzing the share of premium and specialty coffee segments, pricing trends, and shifts in consumer preferences across different regions within Europe.

Market hypotheses are validated through interviews with industry experts, including coffee roasters, caf owners, and industry analysts. This consultation phase provides insights into market trends, operational challenges, and growth opportunities, complementing the quantitative data.

The final step involves synthesizing qualitative and quantitative data from all sources, producing an accurate and comprehensive overview of the Europe Coffee Market. Detailed insights into product segments, pricing strategies, and growth factors are compiled, with the final report validated by industry experts.

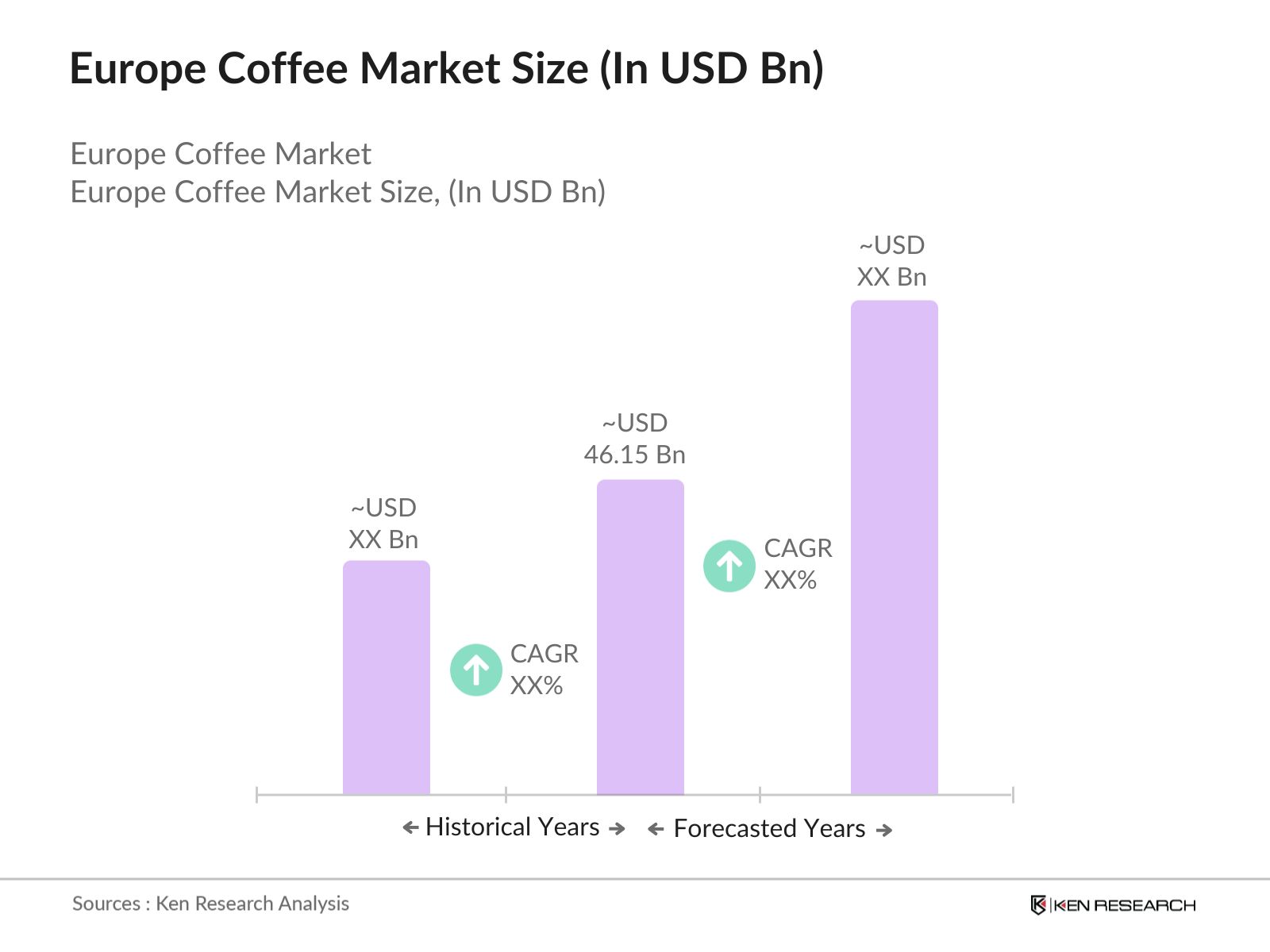

The Europe Coffee Market is valued at USD 46.15 billion, supported by a strong consumer preference for premium coffee and the expanding caf culture across the continent.

Challenges in the Europe Coffee Market include price volatility due to supply chain disruptions and climate impact on coffee crop yields, as well as competition from alternative beverages gaining popularity.

Key players in the Europe Coffee Market include Nestl S.A., Lavazza Group, Starbucks Corporation, JDE Peet's N.V., and Illycaff S.p.A., all of which have strong brand presence and extensive distribution networks across Europe.

The Europe Coffee Market is driven by a preference for specialty and high-quality coffee, the rise of sustainable coffee products, and increasing consumer awareness about ethically sourced options.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.