Europe Cold Chain Market Outlook to 2030

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD2783

October 2024

88

About the Report

Europe Cold Chain Market Overview

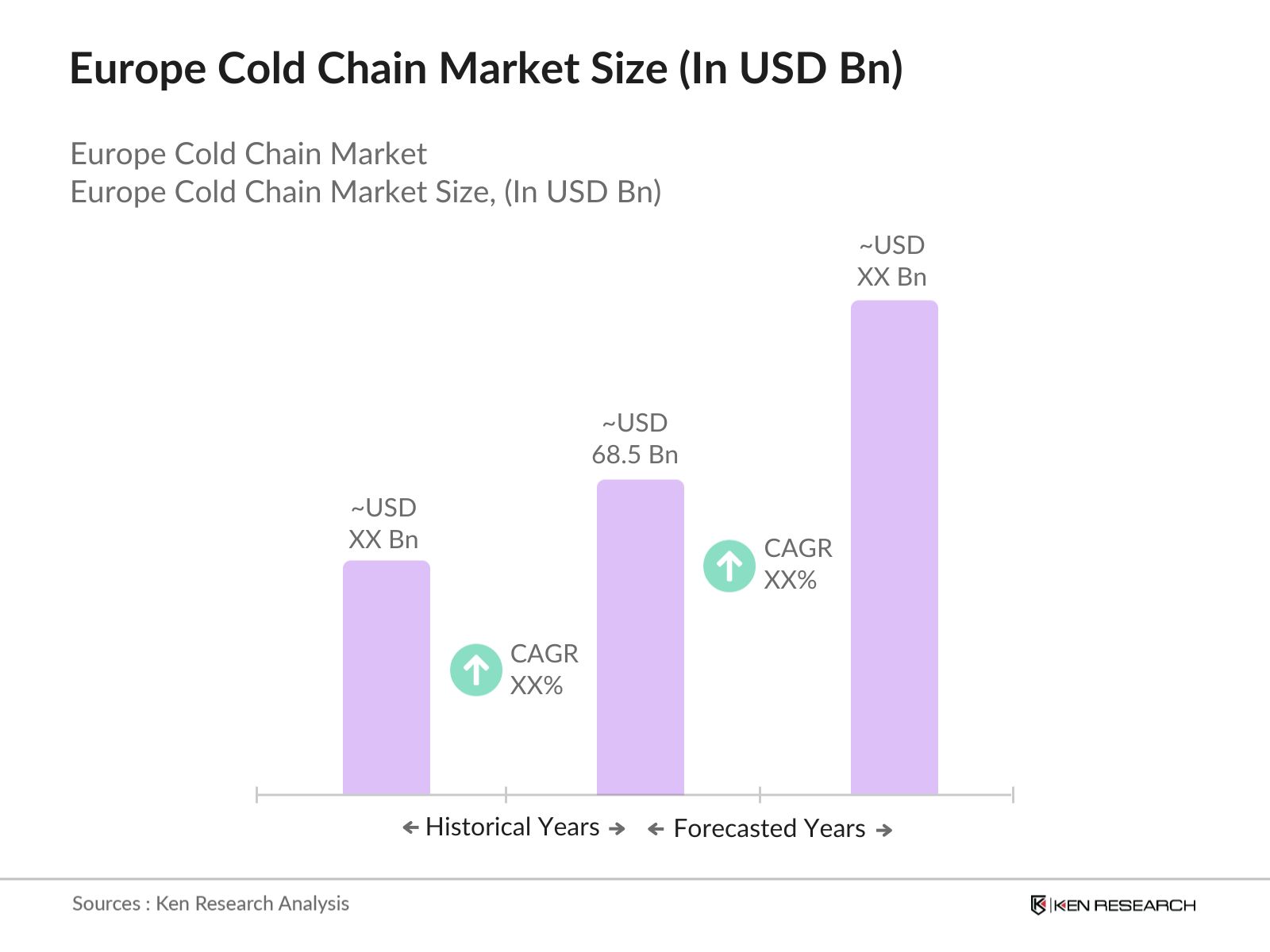

- The Europe cold chain market is valued at USD 68.5 billion, driven by increasing demand for temperature-controlled logistics in sectors such as food and pharmaceuticals. The markets growth is propelled by technological advancements in refrigeration, the growing consumption of perishable food products, and rising healthcare needs for biopharmaceuticals and vaccines. Major industries, particularly pharmaceuticals, rely on precise cold chain logistics to maintain product integrity, especially with the rise of complex vaccines like mRNA types, further fueling demand in the market.

- The market is dominated by countries like Germany, the Netherlands, and France due to their well-developed logistics infrastructure, strategic locations as transportation hubs, and high standards of food safety regulations. Germany's advanced industrial base and the Netherlands' role as a critical logistics gateway to the rest of Europe make them dominant players. Additionally, strong governmental support and efficient supply chains in these countries contribute to their leadership in the European cold chain market.

- The European cold chain market is adopting renewable energy solutions. Cold storage facilities are increasingly integrating solar and wind-powered refrigeration systems to reduce operational costs and carbon emissions. As of 2023, around 15% of cold storage units in Europe had adopted renewable energy sources, driven by EU regulations under the European Green Deal, which mandates the reduction of carbon emissions and supports investment in sustainable energy solutions.

Europe Cold Chain Market Segmentation

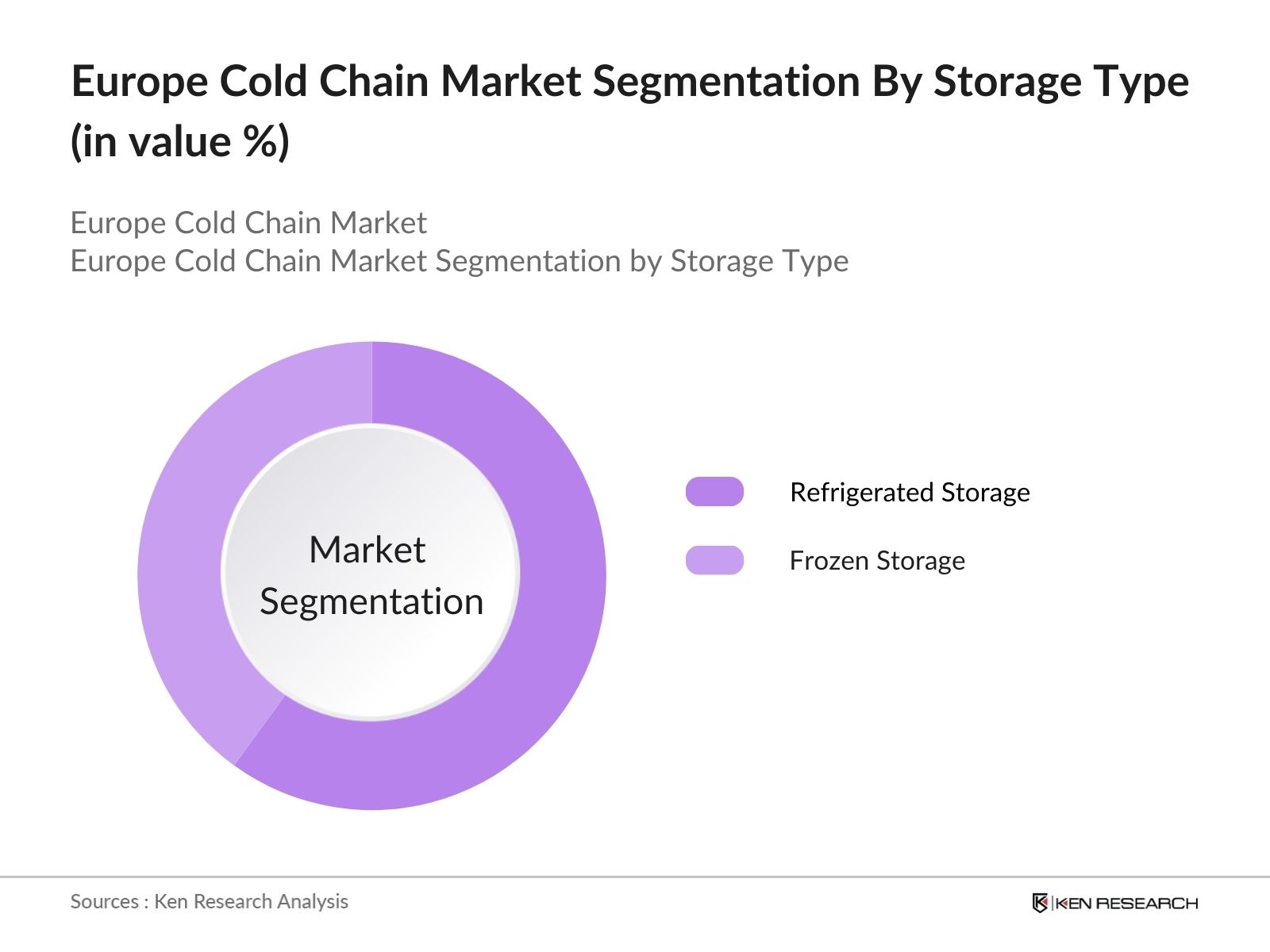

By Storage Type: The Europe cold chain market is segmented by storage type into refrigerated storage and frozen storage. Among these, refrigerated storage holds the dominant market share due to its widespread application in storing fresh produce, dairy, and pharmaceutical products. The growth of the pharmaceutical sector, especially in the context of storing temperature-sensitive vaccines and biologics, has been a significant driver for refrigerated storage. Moreover, consumer preferences for fresh, minimally processed foods have bolstered the demand for this storage type, particularly for dairy, fruits, and vegetables.

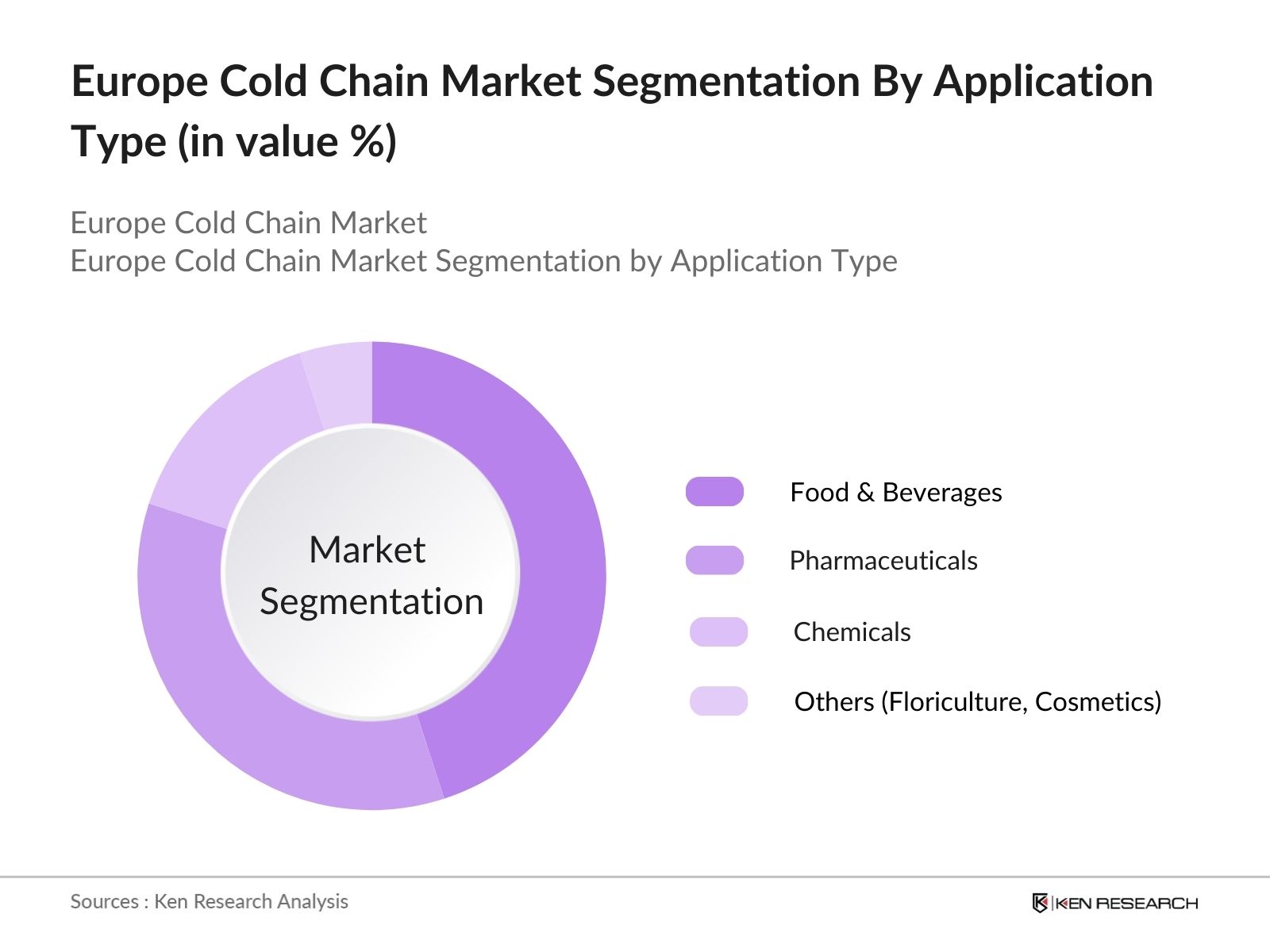

By Application: The Europe cold chain market is segmented by application into food & beverages, pharmaceuticals, chemicals, and others (such as floriculture and cosmetics). Pharmaceuticals lead the market share due to the rise of biopharmaceuticals and stringent regulations around the handling and transportation of temperature-sensitive medicines and vaccines. With the expansion of global vaccine distribution and the growing importance of personalized medicine, this segment has seen significant growth in the demand for ultra-cold chain logistics, especially for biopharmaceutical products that require precise temperature control to maintain efficacy.

Europe Cold Chain Market Competitive Landscape

The Europe cold chain market is dominated by several key players that have established strong infrastructures and logistical capabilities. Companies like Lineage Logistics and NewCold have invested heavily in technology to ensure efficient temperature management and inventory tracking. The competitive landscape is characterized by consolidation, with major companies expanding through mergers and acquisitions to enhance their market presence and operational capacity.

|

Company Name |

Establishment Year |

Headquarters |

Storage Capacity |

Fleet Size |

Geographical Reach |

Energy Efficiency |

Technology Integration |

Cold Chain Certifications |

Company Name |

|

Lineage Logistics |

2008 |

Novi, Michigan, USA |

|||||||

|

NewCold |

2012 |

Breda, Netherlands |

|||||||

|

AGRO Merchants Group |

2013 |

Rotterdam, Netherlands |

|||||||

|

Americold Logistics |

1931 |

Atlanta, Georgia, USA |

|||||||

|

Kloosterboer |

1925 |

Rotterdam, Netherlands |

Europe Cold Chain Market Analysis

Growth Drivers

- Increasing Demand for Temperature-Sensitive Products (e.g., Pharmaceuticals, Perishable Foods): The European market has seen a surge in demand for temperature-sensitive products, driven by pharmaceuticals and perishable foods. By 2024, Europe is projected to require over 60 million cubic meters of cold storage capacity to maintain the integrity of food and pharmaceuticals, according to European Commission reports on food storage. The increasing need for COVID-19 vaccines and biologics, which must be stored at precise temperatures, further stresses the cold chain logistics system. Governmental initiatives ensure that these products are safely stored and distributed, increasing cold chain investments.

- Expansion of E-commerce and Online Grocery Sales: E-commerce and online grocery sales in Europe have seen significant growth in recent years. In 2023, online food sales accounted for 151.88 billion, according to the European Unions e-commerce statistics. The increased use of online grocery services, driven by pandemic habits, now requires extensive cold chain logistics to handle perishable goods. Countries like Germany and France have experienced a near 20% increase in demand for refrigerated warehouses, supported by their expanding online grocery sector.

- Technological Innovations in Cold Chain Logistics (e.g., IoT-enabled Monitoring Systems): IoT and digital monitoring technologies have revolutionized cold chain logistics in Europe. According to a report by the European Commission on digital transformation, over 30% of European cold storage facilities now employ IoT-enabled sensors, which track temperature, humidity, and location in real-time. These advancements have reduced spoilage rates by 15%, providing more accurate monitoring and control during transportation. IoT has proven essential in optimizing the efficiency of cold chains for perishable goods.

Challenges

- High Energy and Infrastructure Costs (Energy Consumption, Infrastructure Investment): Energy consumption remains a critical challenge for Europes cold chain market, with cold storage facilities consuming roughly 2% of Europes electricity annually. According to data from the International Energy Agency (IEA), electricity costs in Europe increased by 7% in 2023, making energy efficiency a priority for cold storage operators. Investment in energy-efficient technologies like solar-powered refrigeration systems is crucial, though initial infrastructure costs pose a barrier for small to mid-sized operators.

- Complex Regulatory Environment (Food Safety, Carbon Emissions): Europes cold chain sector faces a complicated regulatory environment, with stringent rules regarding food safety and carbon emissions. The European Unions Green Deal aims to reduce carbon emissions by 55% by 2030, creating new challenges for cold chain operators to comply. According to the European Environment Agency (EEA), the cold chain industry was responsible for 5 million tons of CO2 emissions in 2023, pushing operators to invest in eco-friendly technology.

Europe Cold Chain Market Future Outlook

Over the next few years, the Europe cold chain market is expected to grow significantly, driven by the continued expansion of e-commerce in food and grocery deliveries, advancements in cold storage technologies, and stricter government regulations on food safety and pharmaceutical logistics. The increasing adoption of IoT and blockchain technology to improve traceability and efficiency in temperature-controlled logistics will also drive market growth. Moreover, the European Green Deals emphasis on reducing carbon emissions is pushing companies to adopt more energy-efficient technologies in cold chain facilities.

Market Opportunities

- Growth in Biopharmaceuticals and Vaccine Distribution (COVID-19, mRNA Vaccines): The biopharmaceutical industrys reliance on cold storage for vaccine distribution has grown significantly since the COVID-19 pandemic. Europe distributed over 2.5 billion vaccine doses between 2020 and 2023, necessitating a robust cold chain. The introduction of mRNA vaccines, which require sub-zero storage, has further expanded the need for cold chain logistics. According to the World Health Organization (WHO), the biopharmaceutical sector will continue to depend on highly efficient cold storage solutions to ensure vaccine efficacy.

- Adoption of Renewable Energy Solutions in Cold Chain Facilities: There is a growing trend toward adopting renewable energy solutions in cold storage facilities. The European Commission's Renewable Energy Directive mandates that 40% of Europes energy must come from renewable sources by 2030, creating opportunities for the cold chain sector to invest in solar and wind-powered refrigeration units. In 2023, renewable energy powered 10% of Europe's cold chain facilities, reducing carbon emissions and lowering long-term operational costs.

Scope of the Report

|

By Type of Storage |

Refrigerated Storage Frozen Storage |

|

By Temperature Range |

Chilled (2C - 8C) Frozen (-18C and below) Ultra-low Temperature (-80C) |

|

By Application |

Food & Beverages (Dairy, Meat, Fruits & Vegetables) Pharmaceuticals (Vaccines, Biopharma Products) Chemicals (Temperature-sensitive Materials) Others (Floral, Cosmetics) |

|

By Logistics Type |

Cold Storage Cold Transportation |

|

By Region |

Western Europe Eastern Europe Central Europe Northern Europe Southern Europe |

Products

Key Target Audience

Cold Chain Service Providers

Logistics and Transportation Companies

Biopharmaceutical Manufacturers

Frozen Food Producers

Supermarkets and Grocery Chains

Government and Regulatory Bodies (e.g., European Food Safety Authority, European Medicines Agency)

Investment and Venture Capitalist Firms

Environmental Agencies (e.g., European Environmental Agency)

Companies

Players mentioned in the report:

Lineage Logistics

NewCold Advanced Cold Logistics

AGRO Merchants Group

Americold Logistics

Kloosterboer

VersaCold Logistics Services

DHL Supply Chain

XPO Logistics

Nichirei Logistics Group

Maersk Line

Ryder System, Inc.

Deutsche Post DHL Group

Thermo King Corporation

Carrier Transicold

JBT Corporation

Table of Contents

1. Europe Cold Chain Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Europe Cold Chain Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Europe Cold Chain Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for Temperature-Sensitive Products (e.g., Pharmaceuticals, Perishable Foods)

3.1.2. Expansion of E-commerce and Online Grocery Sales

3.1.3. Government Regulations Promoting Food Safety and Storage

3.1.4. Technological Innovations in Cold Chain Logistics (e.g., IoT-enabled Monitoring Systems)

3.2. Market Challenges

3.2.1. High Energy and Infrastructure Costs (Energy Consumption, Infrastructure Investment)

3.2.2. Complex Regulatory Environment (Food Safety, Carbon Emissions)

3.2.3. Skills Shortage in Cold Chain Management (Training, Technological Literacy)

3.3. Opportunities

3.3.1. Growth in Biopharmaceuticals and Vaccine Distribution (COVID-19, mRNA Vaccines)

3.3.2. Adoption of Renewable Energy Solutions in Cold Chain Facilities

3.3.3. Development of Cold Chain in Emerging Markets (Eastern Europe, Russia)

3.4. Trends

3.4.1. Blockchain for Cold Chain Traceability

3.4.2. Automation and Robotics in Cold Storage Warehouses

3.4.3. Growing Focus on Carbon Footprint Reduction

3.5. Government Regulation

3.5.1. European Food Safety Authority (EFSA) Guidelines

3.5.2. European Green Deal and Sustainability Initiatives

3.5.3. EU-28 Cold Chain Compliance Standards

3.6. SWOT Analysis

3.7. Stake Ecosystem (Supply Chain Structure, Key Stakeholders)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem (Market Fragmentation, Key Competitors)

4. Europe Cold Chain Market Segmentation

4.1. By Type of Storage (In Value %)

4.1.1. Refrigerated Storage

4.1.2. Frozen Storage

4.2. By Temperature Range (In Value %)

4.2.1. Chilled (2C - 8C)

4.2.2. Frozen (-18C and below)

4.2.3. Ultra-low Temperature (-80C)

4.3. By Application (In Value %)

4.3.1. Food & Beverages (Dairy, Meat, Fruits & Vegetables)

4.3.2. Pharmaceuticals (Vaccines, Biopharma Products)

4.3.3. Chemicals (Temperature-sensitive Materials)

4.3.4. Others (Floral, Cosmetics)

4.4. By Logistics Type (In Value %)

4.4.1. Cold Storage

4.4.2. Cold Transportation

4.5. By Region (In Value %)

4.5.1. Western Europe

4.5.2. Eastern Europe

4.5.3. Central Europe

4.5.4. Northern Europe

4.5.5. Southern Europe

5. Europe Cold Chain Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Lineage Logistics

5.1.2. AGRO Merchants Group

5.1.3. Americold Logistics

5.1.4. Kloosterboer

5.1.5. Nichirei Logistics Group

5.1.6. VersaCold Logistics Services

5.1.7. NewCold Advanced Cold Logistics

5.1.8. DHL Supply Chain

5.1.9. XPO Logistics

5.1.10. Ryder System, Inc.

5.1.11. Deutsche Post DHL Group

5.1.12. Maersk Line

5.1.13. JBT Corporation

5.1.14. Thermo King Corporation

5.1.15. Carrier Transicold

5.2. Cross Comparison Parameters (Number of Warehouses, Fleet Size, Temperature Range, Total Capacity, Global Reach, Automation Level, Energy Efficiency, Revenue)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Funding and Grants

5.8. Private Equity Investments

6. Europe Cold Chain Market Regulatory Framework

6.1. EU Food Safety Standards and Compliance (HACCP, EFSA Guidelines)

6.2. Sustainability Regulations (European Green Deal)

6.3. Cold Chain Certification Processes (GDP, ISO 22000)

7. Europe Cold Chain Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Rising Demand for Frozen Foods, Vaccine Distribution Growth)

8. Europe Cold Chain Future Market Segmentation

8.1. By Type of Storage (In Value %)

8.2. By Temperature Range (In Value %)

8.3. By Application (In Value %)

8.4. By Logistics Type (In Value %)

8.5. By Region (In Value %)

9. Europe Cold Chain Market Analysts Recommendations

9.1. Total Addressable Market (TAM)/Serviceable Available Market (SAM)/Serviceable Obtainable Market (SOM) Analysis

9.2. Cold Chain Digital Transformation Strategy

9.3. White Space Opportunity Analysis

9.4. Marketing Initiatives for Key Stakeholders

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

This step involves mapping the cold chain market ecosystem, identifying key stakeholders such as cold chain service providers, logistics companies, and regulatory bodies. Secondary data sources, including industry reports and government publications, were used to define the critical variables affecting market dynamics, such as storage capacity, temperature range, and fleet size.

Step 2: Market Analysis and Construction

Historical data related to the cold chain market was collected, including details on storage type segmentation, logistics providers, and industry revenue. This analysis was followed by a review of service quality metrics to verify the accuracy of financial data and to assess market penetration rates for various sub-segments.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through interviews with industry professionals, including cold chain logistics managers and biopharmaceutical supply chain experts. These consultations provided firsthand insights into operational trends and helped to refine the market forecasts.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing data from various sources, including cold storage operators and technology providers, to ensure the accuracy of projections. A bottom-up approach was used to validate findings, followed by an expert review to ensure a comprehensive analysis of the Europe cold chain market.

Frequently Asked Questions

01. How big is the Europe Cold Chain Market?

The Europe cold chain market is valued at USD 68.5 billion and is driven by the rising demand for temperature-controlled logistics, particularly in the pharmaceutical and food sectors.

02. What are the challenges in the Europe Cold Chain Market?

Challenges in the Europe cold chain market include high energy and infrastructure costs, a complex regulatory environment, and the skills shortage required to manage advanced cold chain logistics.

03. Who are the major players in the Europe Cold Chain Market?

Key players in the Europe cold chain market include Lineage Logistics, NewCold, AGRO Merchants Group, Americold, and Kloosterboer, which dominate due to their large storage capacities, technological integration, and global reach.

04. What are the growth drivers of the Europe Cold Chain Market?

The Europe cold chain market is driven by the expansion of e-commerce, growing demand for biopharmaceutical products, and increased investment in cold chain technologies such as IoT and blockchain.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.