Europe Connected Car Market Outlook to 2030

Region:Europe

Author(s):Sanjna

Product Code:KROD2743

December 2024

83

About the Report

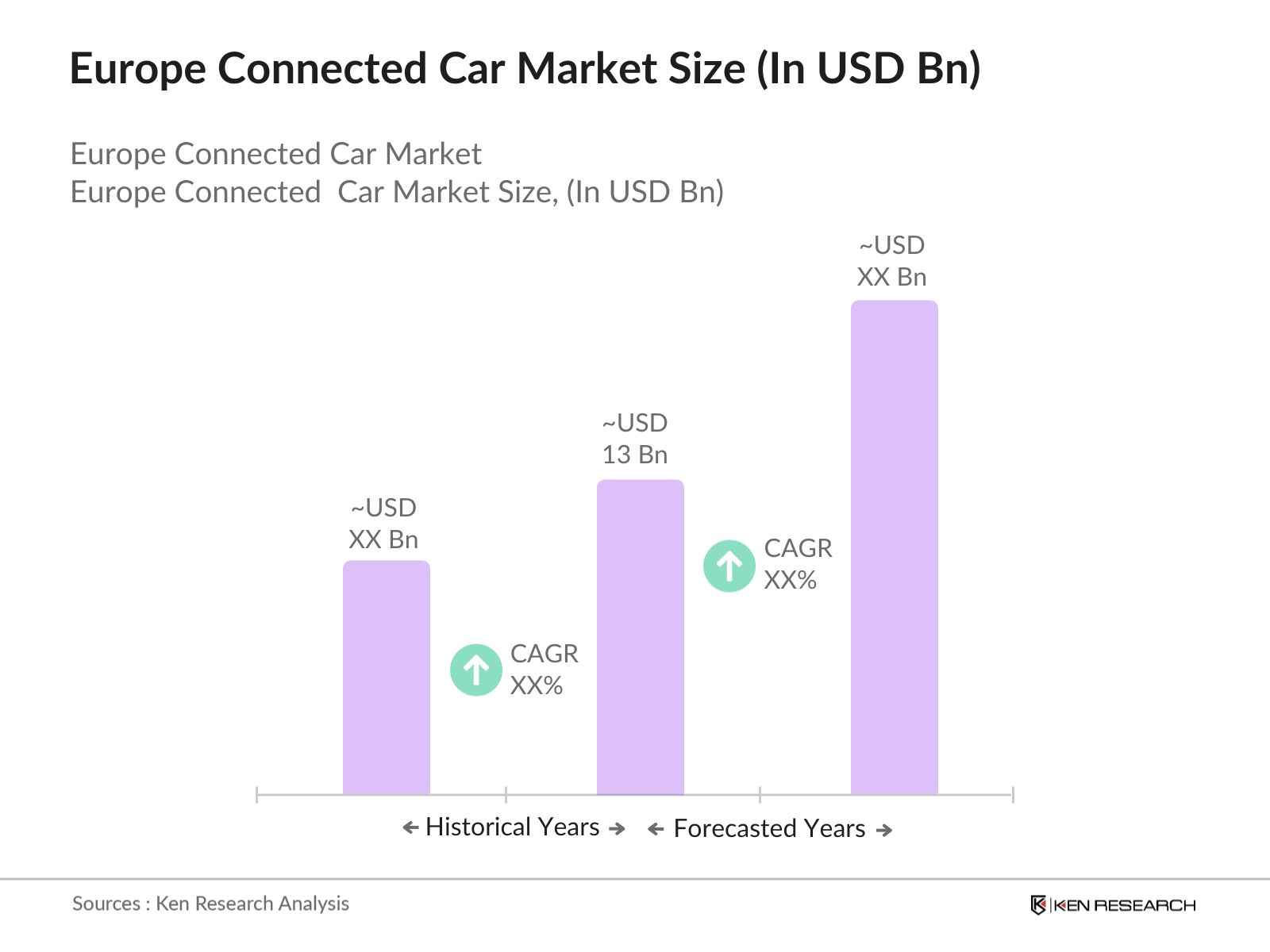

Europe Connected Car Market Overview

- The Europe Connected Car market, valued at USD 13 billion, is driven by a combination of rising consumer demand for enhanced in-vehicle experiences and government initiatives promoting vehicle connectivity for safety and efficiency. Technological advancements such as 5G networks and advanced telematics play a significant role in enhancing real-time vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication, making driving more connected and automated.

- Western Europe, particularly Germany, France, and the UK, dominates the market due to the presence of automotive giants like BMW, Volkswagen, and Daimler AG, coupled with significant investments in automotive research and innovation. Germany leads because of its strong automotive manufacturing base and the government's focus on smart mobility and intelligent transportation systems. These countries have advanced digital infrastructures, creating an ideal environment for the adoption of connected car technologies.

- The Sustainable and Smart Mobility Strategy, presented by the European Commission in December 2020, aims to transform the EU transport system towards a greener, smarter, and more resilient future. This strategy includes an Action Plan with 82 initiatives designed to achieve significant reductions in transport emissionstargeting a 90% reduction by 2050. These regulations encourage collaboration among stakeholders while promoting investment into innovative mobility solutions that align with sustainability goals.

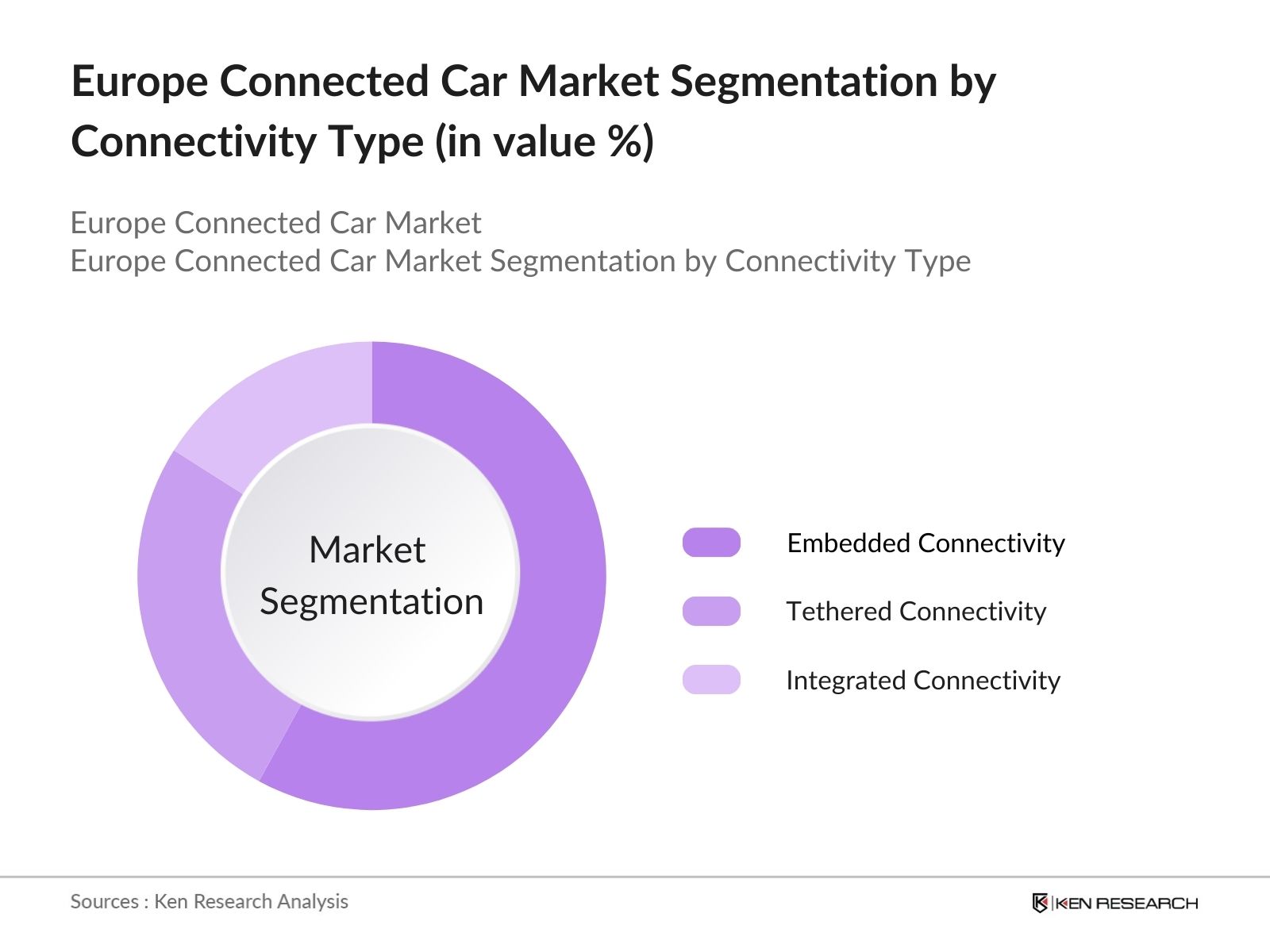

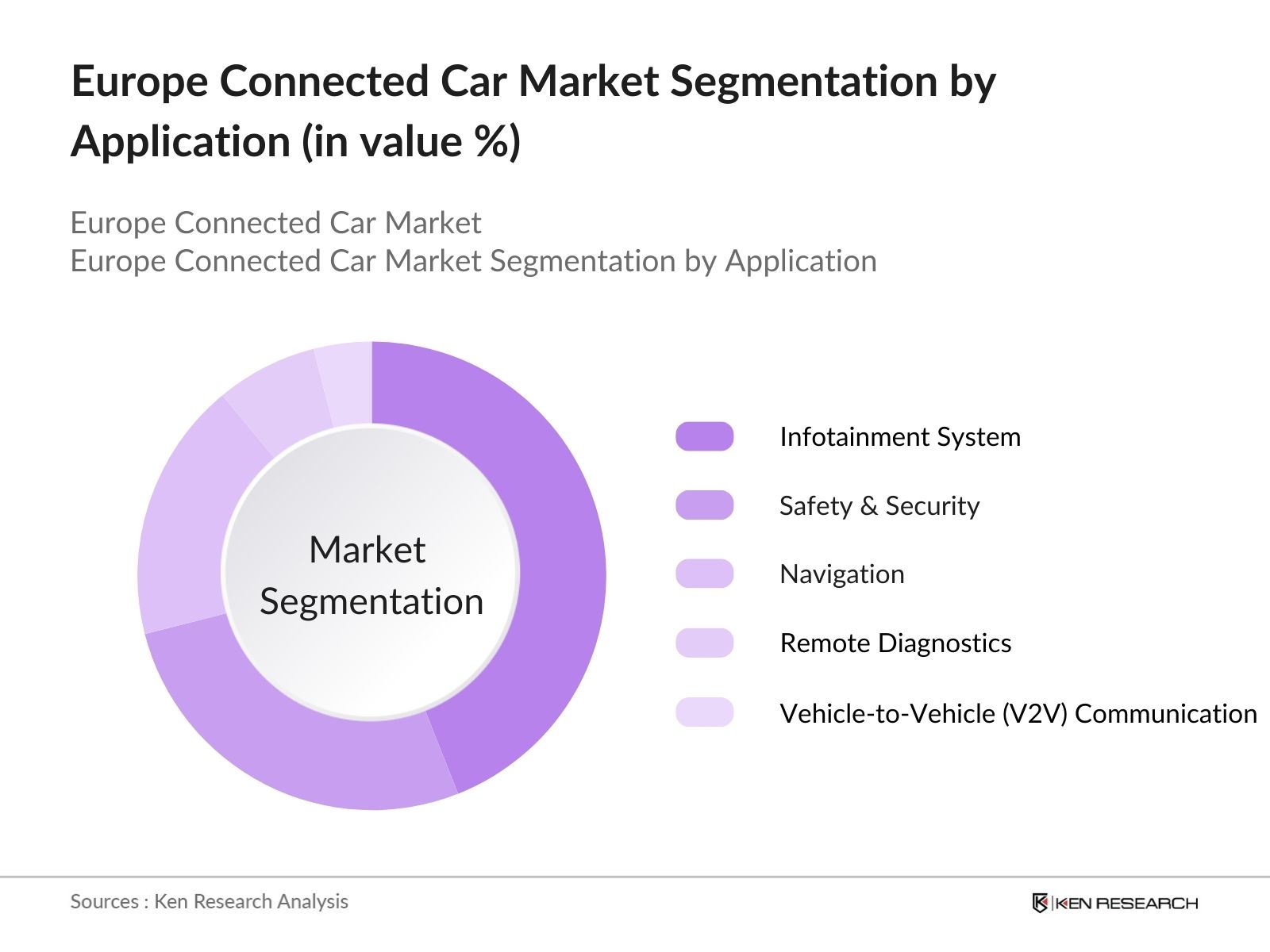

Europe Connected Car Market Segmentation

By Connectivity Type: The Europe Connected Car market is segmented by connectivity type into embedded connectivity, tethered connectivity, and integrated connectivity. Embedded connectivity holds the largest market share, driven by regulatory mandates for emergency call systems and real-time data exchange capabilities. The European Union's eCall mandate, requiring all new cars to be equipped with a system that automatically calls emergency services in the event of a crash, has been a key driver for embedded solutions.

By Application: Under the application segment, infotainment systems have captured a dominant market share due to increasing consumer demand for personalized entertainment, navigation, and internet access while driving. Major automakers are focusing on creating user-friendly in-car systems that allow seamless integration of smartphones, providing apps and streaming services in real-time. This trend is further fueled by partnerships between automakers and technology companies such as Apple and Google.

Europe Connected Car Market Competitive Landscape

The Europe Connected Car market is dominated by several key players that leverage technological innovations and strategic partnerships to gain a competitive edge. European automakers lead the market, followed by global tech companies entering the space through collaborations with traditional automakers. The competitive landscape reveals a strong European presence, led by local champions BMW, Daimler, and Volkswagen, who have heavily invested in connected car technologies. These firms are increasingly collaborating with technology companies such as Intel, Nvidia, and Microsoft to integrate artificial intelligence (AI) and machine learning capabilities into vehicles, enabling advanced autonomous driving features.

|

Company |

Establishment Year |

Headquarters |

R&D Spending |

Product Portfolio |

Strategic Collaborations |

Innovation Index |

Revenue |

Autonomous Driving Initiatives |

Market Share |

|---|---|---|---|---|---|---|---|---|---|

|

BMW AG |

1916 |

Munich, Germany |

- | - | - | - | - | - | - |

|

Daimler AG |

1926 |

Stuttgart, Germany |

- | - | - | - | - | - | - |

|

Volkswagen Group |

1937 |

Wolfsburg, Germany |

- | - | - | - | - | - | - |

|

Continental AG |

1871 |

Hanover, Germany |

- | - | - | - | - | - | - |

|

Bosch Mobility Solutions |

1886 |

Gerlingen, Germany |

- | - | - | - | - | - | - |

Europe Connected Car Market Analysis

Growth Drivers

- Increase in Vehicle Connectivity: The rise in vehicle connectivity in Europe is driven by increasing consumer demand for connected services in vehicles. In 2022, around 30% of the global connected car fleet was located in Europe, reflecting a robust market presence. This trend is supported by the deployment of 5G networks, which are projected to cover 90% of the EU population by 2025. The digital economy, growing by 160 billion annually across the region, underscores the increasing reliance on connected technologies.

- Government Initiatives on Autonomous Driving: European governments are pushing for autonomous driving technologies, leading to growth in the connected car market. The European Union has set a target to reduce road fatalities by 50% by the year 2030, as part of its Road Safety Policy Framework for 2021-2030. This initiative aims to significantly lower the number of road deaths and serious injuries, with an overarching goal of achieving close to zero fatalities by 2050. These investments and regulatory advancements are projected to substantially increase demand for connected vehicle platforms.

- Integration of 5G for Enhanced Connectivity: The rollout of 5G networks across Europe has been a critical factor in improving vehicle connectivity. The European Commission has emphasized the importance of deploying 5G infrastructure to enable Connected and Automated Mobility (CAM), which is critical for applications like Vehicle-to-Everything (V2X) communication. This transition is expected to enhance road safety and reduce emissions, aligning with the broader goals of the EU's digital and green transitions.

Challenges

- Data Privacy and Cybersecurity Concerns: The growing integration of connected services in vehicles has raised significant concerns about data privacy and cybersecurity. There are data breach incidents in the automotive industry across Europe, highlighting the challenges in protecting user information. The cost of a single breach can reach USD 3.96 million prompting the need for improved cybersecurity protocols in connected vehicles.

- High Initial Infrastructure Costs: The deployment of connected vehicle infrastructure, such as 5G towers and smart traffic systems, involves significant upfront costs. These high costs deter smaller economies in Eastern Europe from investing in the necessary infrastructure, which could slow the adoption of connected vehicles in these regions. Western Europe, particularly Germany and France, accounts for the majority of connected vehicle infrastructure investments.

Europe Connected Car Future Market Outlook

Over the next five years, the Europe Connected Car market is expected to experience substantial growth, driven by continuous advancements in 5G technology, expanding electric vehicle (EV) infrastructure, and increasing demand for vehicle-to-everything (V2X) communication. Governments across Europe are also playing a crucial role in facilitating market growth through initiatives like smart city projects and autonomous vehicle testing regulations.

Market Opportunities

- Adoption of AI and Machine Learning in Connected Car Ecosystem: Artificial Intelligence (AI) and Machine Learning (ML) are transforming the connected car ecosystem. The European Commission has invested USD 1.82 billion into AI research as part of its Horizon Europe program, positioning AI as a key growth driver in the connected vehicle market. AI's role in autonomous driving is also expected to enhance vehicle-to-vehicle communication, leading to safer, more efficient road transport systems.

- Expansion of Vehicle-to-Everything (V2X) Technologies: The expansion of Vehicle-to-Everything (V2X) technologies is providing opportunities for market growth. As of late 2020, there were approximately 0.7 million vehicles equipped with V2X technology, and projections suggest this number could reach around 35.1 million by 2025. This technology enhances road safety and traffic efficiency. The rapid adoption of V2X technology is poised to revolutionize connected vehicle ecosystems, paving the way for smarter, safer, and more efficient transportation systems globally.

Scope of the Report

|

By Connectivity Type |

Embedded Connectivity Tethered Connectivity Integrated Connectivity |

|

By Application |

Infotainment Systems Safety & Security Navigation Remote Diagnostics V2V Communication |

|

By Communication Type |

Vehicle-to-Vehicle (V2V) Vehicle-to-Infrastructure (V2I) Vehicle-to-Pedestrian (V2P) |

|

By Technology |

4G/LTE Connectivity 5G Connectivity Satellite Communication DSRC |

|

By Region |

Western Europe Eastern Europe Northern Europe Southern Europe |

Products

Key Target Audience: Organisations & Entities who can benefit from Subscribing this Report

Original Equipment Manufacturers (OEMs)

Automotive Suppliers

Technology Providers (e.g., Intel, Google)

Telecommunications Providers

Fleet Management Companies

Insurance Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., European Commission, UNECE)

Companies

Major Players Mentioned in the Report

BMW AG

Daimler AG

Volkswagen Group

Continental AG

Bosch Mobility Solutions

Aptiv PLC

Qualcomm Technologies

Harman International

NXP Semiconductors

ZF Friedrichshafen AG

Ericsson AB

Tesla Inc.

Ford Motor Company

Volvo Group

Renault Group

Table of Contents

1. Europe Connected Car Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Europe Connected Car Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Europe Connected Car Market Analysis

3.1 Growth Drivers

3.1.1 Increase in Vehicle Connectivity

3.1.2 Government Initiatives on Autonomous Driving

3.1.3 Integration of 5G for Enhanced Connectivity

3.1.4 Growing Demand for In-Vehicle Infotainment Systems

3.2 Market Challenges

3.2.1 Data Privacy and Cybersecurity Concerns

3.2.2 High Initial Infrastructure Costs

3.2.3 Regulatory Hurdles for Autonomous Vehicles

3.3 Opportunities

3.3.1 Adoption of AI and Machine Learning in Connected Car Ecosystem

3.3.2 Expansion of Vehicle-to-Everything (V2X) Technologies

3.3.3 Growing Integration of Telematics in Fleet Management

3.4 Trends

3.4.1 Rise of Subscription-Based Connected Car Services

3.4.2 Growing Penetration of Over-the-Air (OTA) Updates

3.4.3 Increasing Collaborations Between Automakers and Tech Giants

3.5 Government Regulations

3.5.1 EU Mandates on Smart Transportation Systems

3.5.2 CO2 Emission Reduction Standards for Automakers

3.5.3 Deployment of Intelligent Transport Systems (ITS)

3.5.4 Data Protection and GDPR Compliance

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (OEMs, Tech Companies, Regulatory Bodies)

3.8 Porters Five Forces

3.9 Competition Ecosystem

4. Europe Connected Car Market Segmentation

4.1 By Connectivity Type (In Value %)

4.1.1 Embedded Connectivity

4.1.2 Tethered Connectivity

4.1.3 Integrated Connectivity

4.2 By Application (In Value %)

4.2.1 Infotainment Systems

4.2.2 Safety & Security

4.2.3 Navigation

4.2.4 Remote Diagnostics

4.2.5 Vehicle-to-Vehicle (V2V) Communication

4.3 By Communication Type (In Value %)

4.3.1 Vehicle-to-Vehicle (V2V)

4.3.2 Vehicle-to-Infrastructure (V2I)

4.3.3 Vehicle-to-Pedestrian (V2P)

4.4 By Technology (In Value %)

4.4.1 4G/LTE Connectivity

4.4.2 5G Connectivity

4.4.3 Satellite Communication

4.4.4 DSRC (Dedicated Short Range Communication)

4.5 By Region (In Value %)

4.5.1 Western Europe

4.5.2 Eastern Europe

4.5.3 Northern Europe

4.5.4 Southern Europe

5. Europe Connected Car Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Continental AG

5.1.2 Bosch Mobility Solutions

5.1.3 Aptiv PLC

5.1.4 Qualcomm Technologies

5.1.5 Harman International

5.1.6 TomTom N.V.

5.1.7 NXP Semiconductors

5.1.8 ZF Friedrichshafen AG

5.1.9 Valeo SA

5.1.10 Ericsson AB

5.1.11 Tesla Inc.

5.1.12 Ford Motor Company

5.1.13 BMW AG

5.1.14 Daimler AG

5.1.15 General Motors

5.2 Cross Comparison Parameters (R&D Spending, Connectivity Partnerships, Autonomous Driving Initiatives, Revenue, Market Share, Innovation Index, Product Portfolio, Strategic Collaborations)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Europe Connected Car Market Regulatory Framework

6.1 Safety and Compliance Standards

6.2 Vehicle Data Management

6.3 Connectivity and Spectrum Regulations

6.4 Autonomous Vehicle Testing Regulations

7. Europe Connected Car Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Europe Connected Car Future Market Segmentation

8.1 By Connectivity Type (In Value %)

8.2 By Application (In Value %)

8.3 By Communication Type (In Value %)

8.4 By Technology (In Value %)

8.5 By Region (In Value %)

9. Europe Connected Car Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Consumer Behavior Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involves mapping the ecosystem of the Europe Connected Car market, identifying key players, such as OEMs, technology suppliers, and regulatory bodies. This is done through desk research, utilizing proprietary and public databases to gain a comprehensive understanding of market dynamics, including key drivers and restraints.

Step 2: Market Analysis and Construction

Historical data on market growth, penetration rates of connected car technologies, and sales figures from leading automotive manufacturers are analyzed to estimate the current market size and forecast future trends. The focus is on data-driven insights that outline how the market has evolved and how it is likely to progress.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from leading companies, such as BMW and Continental, are consulted to validate market trends and provide insights into operational challenges. These consultations are conducted through structured interviews to ensure that the data collected is robust and credible.

Step 4: Research Synthesis and Final Output

The final phase synthesizes all the data collected, verifying it against inputs from automotive manufacturers and technology providers. This helps refine the final report, ensuring that market forecasts and segmentation are aligned with real-world data.

Frequently Asked Questions

01. How big is the Europe Connected Car Market?

The Europe Connected Car market is valued at USD 13 billion, driven by increasing consumer demand for connectivity features and government mandates on vehicle safety and real-time communication systems.

02. What are the challenges in the Europe Connected Car Market?

Key challenges of Europe Connected Car Market include high infrastructure costs, data privacy concerns, and regulatory hurdles surrounding autonomous driving and connectivity. Additionally, ensuring cybersecurity in an increasingly connected automotive ecosystem is a growing concern.

03. Who are the major players in the Europe Connected Car Market?

Leading players of Europe Connected Car Market include BMW AG, Daimler AG, Volkswagen Group, Continental AG, and Bosch Mobility Solutions. These companies dominate the market due to their innovation in connected technologies and partnerships with tech companies.

04. What are the growth drivers of the Europe Connected Car Market?

Growth of Europe Connected Car Market is driven by advancements in 5G technology, the development of autonomous driving features, and the increasing adoption of infotainment and safety systems. Government regulations mandating vehicle connectivity also play a crucial role.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.