Europe Construction Market Outlook to 2030

Region:Europe

Author(s):Shreya Garg

Product Code:KROD9918

December 2024

93

About the Report

Europe Construction Market Overview

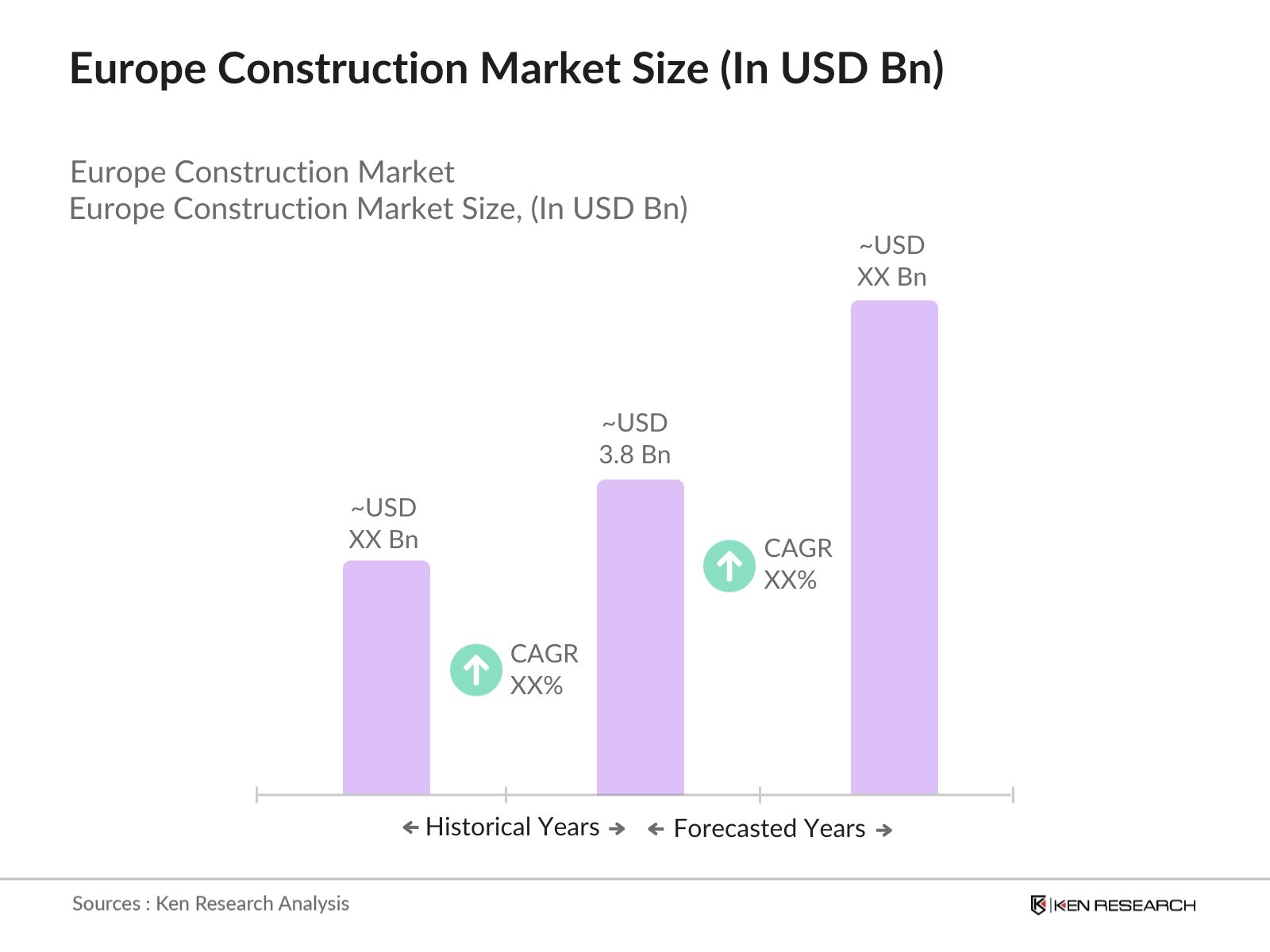

- The Europe Construction Market is currently valued at USD 3.8 billion, based on a five-year historical analysis. This market size is primarily driven by the increasing investments in infrastructure development across several key European countries, alongside the adoption of advanced construction technologies such as Building Information Modeling (BIM) and prefabrication. The demand for sustainable and energy-efficient buildings has also spurred growth, as government regulations encourage greener construction practices and energy-saving projects.

- Key dominant countries in the Europe Construction Market include Germany, the United Kingdom, and France. Germany leads due to its large-scale infrastructure projects and strong economic base, especially in commercial and industrial construction. The United Kingdom dominates because of urbanization, infrastructure investment, and renovation projects. France's dominance stems from government initiatives to drive affordable housing projects and renovation of historical infrastructure, making these three countries the powerhouses of the European construction industry.

- The EUs sustainable construction policy is shaping the future of the construction sector, mandating that all new buildings must meet nearly zero-energy standards by 2025. This directive has already influenced 70% of new commercial builds in Europe by 2023. Additionally, the European Commission has allocated 30 billion in incentives to encourage sustainable construction practices, particularly targeting energy efficiency and the use of renewable materials

Europe Construction Market Segmentation

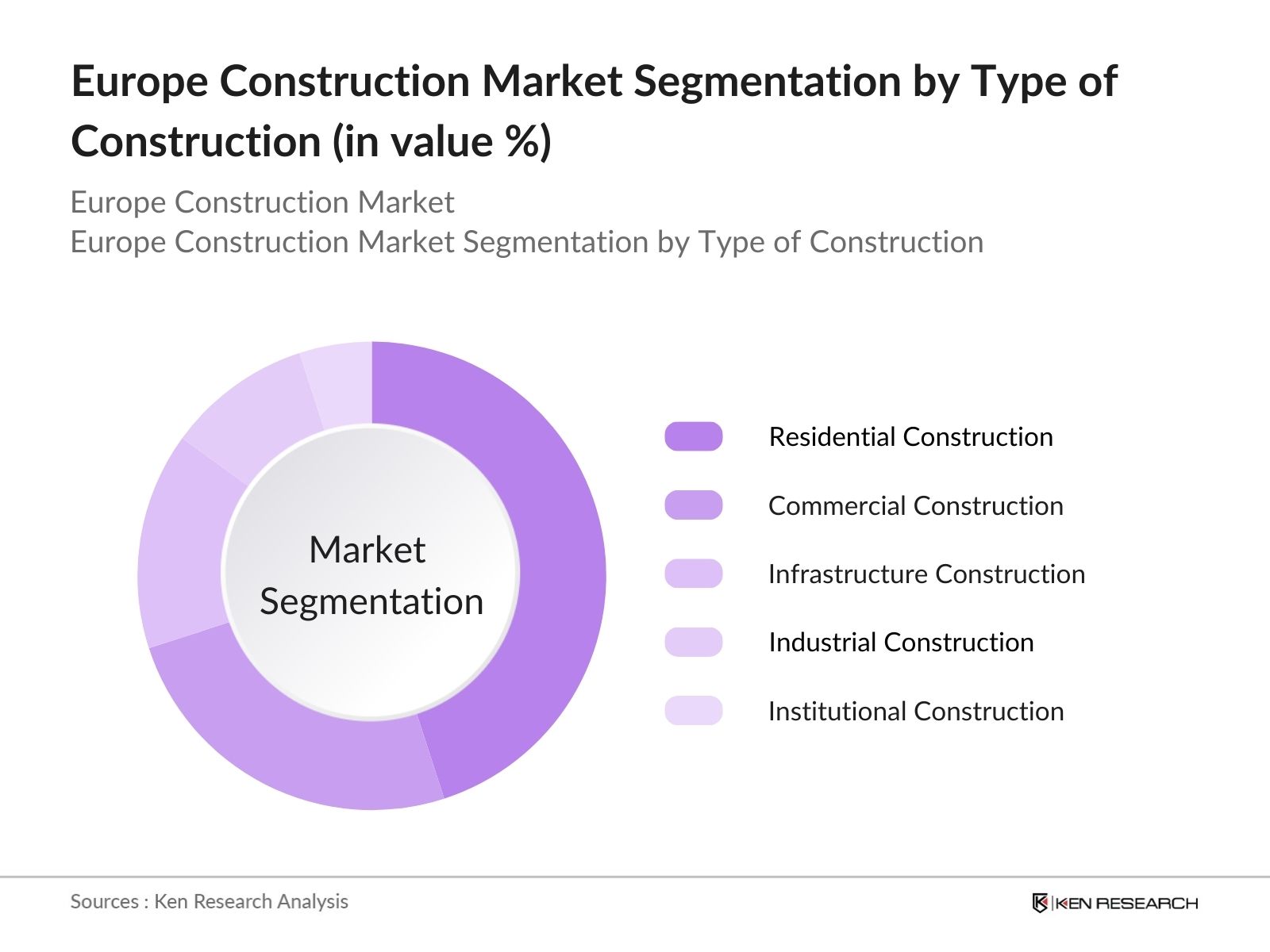

By Type of Construction: The Market is segmented by type of construction into residential, commercial, infrastructure, industrial, and institutional construction. Recently, residential construction has been dominating the market under this segmentation, largely due to increased government initiatives to develop affordable housing and urban regeneration projects. As urban populations grow, there is increasing demand for residential spaces in both metropolitan and suburban areas, driving significant growth in this segment. Furthermore, low-interest rates and supportive housing policies have made residential construction a highly lucrative segment.

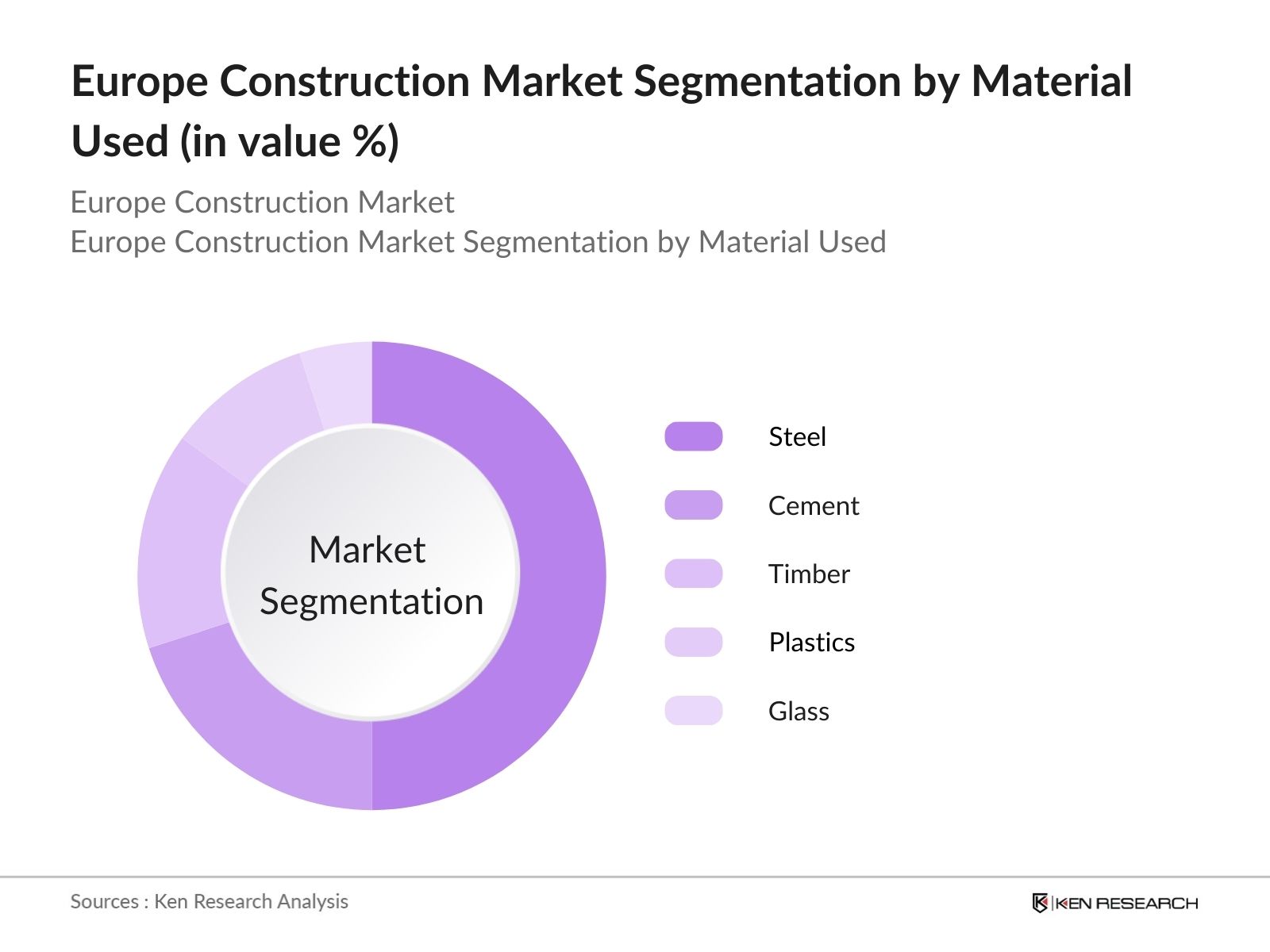

By Material Used: The Market is also segmented by materials used into steel, cement, timber, plastics, and glass. Steel remains the dominant sub-segment due to its versatility, strength, and cost-efficiency in both residential and commercial construction projects. Its ability to support large structures while maintaining design flexibility has made it essential in high-rise buildings, bridges, and industrial facilities. The growing focus on prefabrication and modular construction has further boosted demand for steel, which is seen as a highly sustainable material in modern construction practices.

Europe Construction Market Competitive Landscape

The Europe Construction Market is dominated by several major players, both regional and global, with strong ties to governmental and commercial projects. These key players often leverage partnerships with subcontractors and suppliers to maintain a significant portion of the market. The competitive landscape has seen increased consolidation with mergers and acquisitions aimed at expanding capabilities and geographic reach. The construction industry in Europe is highly competitive, with large firms dominating due to their expansive networks and access to large-scale projects.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

No. of Employees |

No. of Projects |

Market Capitalization (USD Bn) |

Sustainability Initiatives |

Technological Investments |

Key Markets |

|

Vinci SA |

1899 |

France |

|||||||

|

Skanska AB |

1887 |

Sweden |

|||||||

|

STRABAG SE |

1835 |

Austria |

|||||||

|

Bouygues SA |

1952 |

France |

|||||||

|

Balfour Beatty PLC |

1909 |

United Kingdom |

Europe Construction Industry Analysis

Growth Drivers

- Urbanization and Infrastructure Development: Europe's urban population is increasing at a rapid rate, with over 75% of its population living in cities in 2023. Countries such as Germany, France, and the United Kingdom have seen significant infrastructure expansion projects, driven by urbanization. For example, Germany has invested approximately 14 billion in its national transportation infrastructure between 2022 and 2024. This trend toward urbanization is accelerating the demand for commercial and residential buildings, especially in countries like Poland, which has committed 15 billion to its urban infrastructure projects over the same period. Government data sources indicate continued focus on modernization and expansion.

- Green Building Initiatives: Green construction practices are becoming a central focus across Europe, with 27% of all new construction projects integrating sustainable materials by 2023, according to data from the European Commission. The European Union's Green Deal includes 1 trillion investments targeting energy-efficient buildings and carbon-neutral construction by 2030, with over 150 billion already allocated in 2023. This investment boosts demand for sustainable building materials, such as recycled steel and energy-efficient insulation, with these materials becoming essential components in both residential and commercial projects.

- Technological Advancements: Technological innovation is transforming the European construction industry. The adoption of Building Information Modeling (BIM) is expected to be mandatory in 21 EU member states by the end of 2024. By 2023, approximately 70% of large-scale construction projects across the UK and France utilize BIM, significantly reducing design errors and increasing efficiency. Additionally, 3D printing technology has been employed in 15% of new infrastructure projects across Europe, cutting construction times by nearly 30% for certain types of builds.

Market Challenges

- Labor Shortages and Wage Inflation: Labor shortages have significantly impacted the construction sector, with an estimated shortage of 2.5 million skilled workers across Europe in 2023, based on Eurostat data. The aging workforce is exacerbating this shortage, particularly in countries like Italy, where 20% of the construction workforce is over 50 years old. Consequently, wage inflation in the construction sector has increased by 6-8% between 2022 and 2024, straining profit margins for construction companies across Germany, Spain, and other major economies.

- Regulatory Barriers: Navigating Europes regulatory landscape presents challenges, as complex building codes and zoning laws often delay project approvals. For example, in 2023, it took an average of 18 months to receive construction permits in Italy and 14 months in France. Zoning laws in urban areas, especially in densely populated countries like the Netherlands, have restricted the supply of buildable land, driving up land acquisition costs and stalling residential and commercial development.

Europe Construction Market Future Outlook

Over the next five years, the Europe Construction Market is expected to show considerable growth, driven by a combination of green building initiatives, ongoing government infrastructure projects, and increasing urbanization. The need for energy-efficient buildings and sustainable construction practices will push companies to innovate with new materials and construction methods, such as prefabrication and the use of renewable resources. In addition, digitalization of construction processes, such as the integration of BIM, is anticipated to streamline project management and efficiency.

As cities continue to expand and infrastructure ages, significant opportunities will arise for both renovation and new projects, with governments providing necessary funding. The emphasis on sustainability and the European Union's environmental goals will also play a crucial role in shaping future market trends.

Future Market Opportunities

- Integration of Smart Technology in Buildings: The adoption of smart building technologies is surging, with approximately 3.2 million smart homes constructed in Europe by 2023. These homes are equipped with advanced energy management systems, automated lighting, and smart security systems, driving demand for intelligent infrastructure solutions. The European Commission has supported these advancements by allocating 1.2 billion in funding towards smart city projects across member states, with over 50 new smart city projects launched in 2023.

- Modular and Prefabricated Construction Techniques: Modular and prefabricated construction techniques are gaining popularity in Europe, with 11% of all new building projects utilizing these methods in 2023, according to European industry data. These methods reduce construction time by up to 50% and lower labor costs, offering solutions to the labor shortage crisis. Sweden is leading the modular construction market, with nearly 20% of its new homes being prefabricated. This trend is accelerating across Western Europe as it promises efficiency and cost-effectiveness.

Scope of the Report

|

Type of Construction |

Residential Commercial Infrastructure Industrial Institutional |

|

Material Used |

Cement Steel Timber Plastics Glass |

|

Technology |

BIM 3D Printing Drones and Robotics AR/VR Smart Materials |

|

Construction Method |

On-Site Prefabrication Offsite Manufacturing |

|

Region |

Western Europe Central and Eastern Europe Northern Europe Southern Europe Balkans |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (European Commission, National Planning Authorities)

Real Estate Developers

Construction Equipment Manufacturers

Urban Development Agencies

Raw Material Suppliers (Steel, Cement, Timber Producers)

Green Building Certification Bodies (LEED, BREEAM)

Public-Private Partnerships (Infrastructure and Housing Projects)

Companies

Major Players

Vinci SA

Skanska AB

STRABAG SE

Bouygues SA

Balfour Beatty PLC

Laing ORourke

Hochtief AG

Ferrovial SA

Eiffage SA

BAM Group

Implenia AG

Kier Group

Salini Impregilo SpA

ACS Group

Colas Group

Table of Contents

1. Europe Construction Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Construction Industry Growth Rate

1.4. Market Segmentation Overview

2. Europe Construction Market Size (In EUR Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Construction Developments and Milestones

3. Europe Construction Market Analysis

3.1. Growth Drivers

3.1.1 Urbanization and Infrastructure Development

3.1.2 Green Building Initiatives (Energy Efficiency, Sustainable Materials)

3.1.3 Technological Advancements (BIM, 3D Printing)

3.1.4 Government Investment in Housing and Public Projects

3.2. Market Challenges

3.2.1 Labor Shortages and Wage Inflation

3.2.2 Regulatory Barriers (Building Codes, Zoning Laws)

3.2.3 Supply Chain Disruptions (Materials Shortage)

3.2.4 Rising Raw Material Costs (Steel, Concrete)

3.3. Opportunities

3.3.1 Integration of Smart Technology in Buildings

3.3.2 Modular and Prefabricated Construction Techniques

3.3.3 Renovation and Retrofitting of Existing Infrastructure

3.3.4 Cross-border Construction Projects

3.4. Trends

3.4.1 Growth in Green and Sustainable Construction

3.4.2 Shift Toward Digital Construction and Automation

3.4.3 Increased Adoption of Offsite Construction

3.4.4 Rise of Public-Private Partnerships

3.5. Government Regulations

3.5.1 EU Sustainable Construction Policy

3.5.2 Tax Incentives for Green Buildings

3.5.3 Construction Safety Standards

3.5.4 Carbon Emission Reduction Targets

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Government, Private Sector, Regulatory Bodies, End Users)

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem (Key Players, New Entrants, Subcontractors)

4. Europe Construction Market Segmentation

4.1. By Type of Construction

4.1.1 Residential Construction

4.1.2 Commercial Construction

4.1.3 Infrastructure Construction

4.1.4 Industrial Construction

4.1.5 Institutional Construction

4.2. By Material Used

4.2.1 Cement

4.2.2 Steel

4.2.3 Timber

4.2.4 Plastics

4.2.5 Glass

4.3. By Technology

4.3.1 Building Information Modeling (BIM)

4.3.2 3D Printing

4.3.3 Drones and Robotics

4.3.4 Augmented Reality (AR)/Virtual Reality (VR)

4.3.5 Smart Construction Materials

4.4. By Construction Method

4.4.1 Traditional On-Site Construction

4.4.2 Prefabrication and Modular Construction

4.4.3 Offsite Manufacturing

4.5. By Region

4.5.1 Western Europe

4.5.2 Central and Eastern Europe

4.5.3 Northern Europe

4.5.4 Southern Europe

4.5.5 Balkans

5. Europe Construction Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1 Vinci SA

5.1.2 Skanska AB

5.1.3 STRABAG SE

5.1.4 Bouygues SA

5.1.5 Balfour Beatty PLC

5.1.6 Laing ORourke

5.1.7 Hochtief AG

5.1.8 Ferrovial SA

5.1.9 Eiffage SA

5.1.10 BAM Group

5.1.11 Implenia AG

5.1.12 Kier Group

5.1.13 Salini Impregilo SpA

5.1.14 ACS Group

5.1.15 Colas Group

5.2. Cross Comparison Parameters

5.2.1 Revenue

5.2.2 Headquarters

5.2.3 No. of Employees

5.2.4 Market Share

5.2.5 Market Capitalization

5.2.6 No. of Ongoing Projects

5.2.7 Investment in Innovation

5.2.8 Environmental and Sustainability Initiatives

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers, Acquisitions, Joint Ventures)

5.5. Investment Analysis (Venture Capital, Private Equity)

5.6. Technological Innovation Funding

5.7. Government Grants and Subsidies

6. Europe Construction Market Regulatory Framework

6.1. EU Construction Standards

6.2. Environmental Compliance and Certifications (LEED, BREEAM)

6.3. Labor Laws and Safety Regulations

6.4. Taxation Policies for Construction Industry

7. Europe Construction Future Market Size (In EUR Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8. Europe Construction Future Market Segmentation

8.1. By Type of Construction

8.2. By Material Used

8.3. By Technology

8.4. By Construction Method

8.5. By Region

9. Europe Construction Market Analysts Recommendations

9.1. Market Entry Strategies

9.2. Risk Mitigation Strategies

9.3. Growth Strategies for New Entrants

9.4. Innovation and Sustainability Initiatives

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step involves mapping out key stakeholders across the Europe Construction Market. Secondary and proprietary databases are utilized to gather comprehensive industry insights, focusing on crucial factors like government regulations, technological advancements, and consumer demand for construction materials and services.

Step 2: Market Analysis and Construction

In this step, historical data is analyzed, including market penetration rates, growth in construction segments, and profitability margins of major players. The construction ratio of public vs. private projects is evaluated to understand market revenue streams.

Step 3: Hypothesis Validation and Expert Consultation

We develop hypotheses regarding construction trends, which are validated through expert consultations using CATI (Computer-Assisted Telephone Interviews). These experts provide operational insights that are critical to fine-tuning our market estimations and analysis.

Step 4: Research Synthesis and Final Output

Finally, direct engagement with construction companies is conducted to gather detailed insights into project segments, regional performance, and construction practices. This ensures that the final report reflects the most accurate and comprehensive market overview.

Frequently Asked Questions

01. How big is the Europe Construction Market?

The Europe Construction Market is valued at USD 3.8 billion, driven by increasing urbanization and significant investments in infrastructure projects across major European countries.

02. What are the challenges in the Europe Construction Market?

Challenges in the Europe Construction Market include labor shortages, rising raw material costs, and regulatory hurdles associated with environmental and safety standards. These factors could affect the profitability of the market.

03. Who are the major players in the Europe Construction Market?

Key players in the Europe Construction Market include Vinci SA, Skanska AB, STRABAG SE, Bouygues SA, and Balfour Beatty PLC. These companies dominate due to their extensive project portfolios and strong presence in both public and private construction sectors.

04. What are the growth drivers of the Europe Construction Market?

The Europe Construction Market is propelled by increasing infrastructure development, growing urban populations, and government initiatives promoting sustainable and green construction practices.

05. What are the opportunities in the Europe Construction Market?

Opportunities in the Europe Construction Market lie in the adoption of new construction technologies such as BIM, 3D printing, and prefabrication methods, alongside an increasing demand for sustainable and energy-efficient buildings.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.