Europe Frozen Dessert Market Outlook to 2030

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD9777

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD9777

November 2024

87

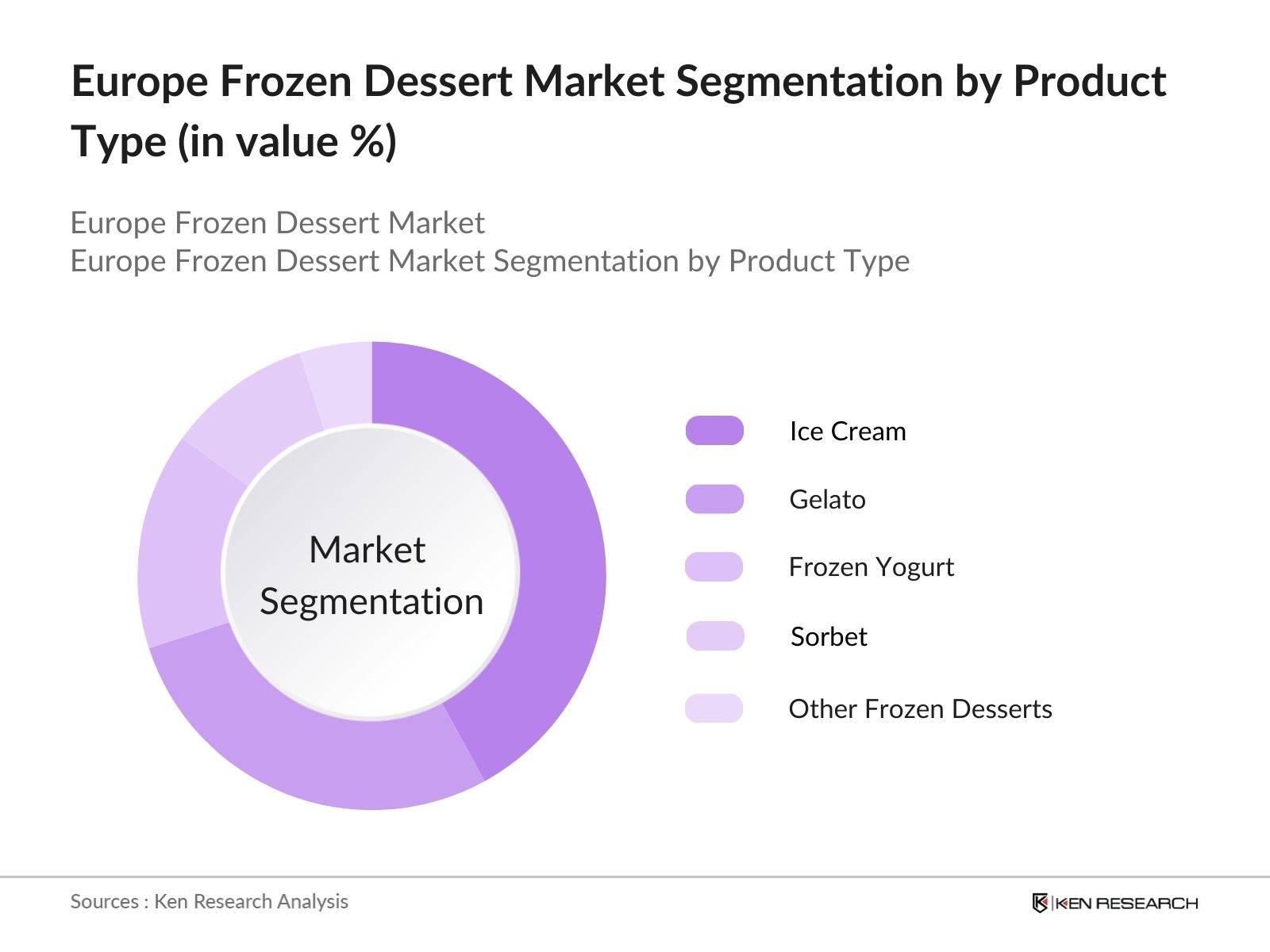

By Product Type: The Europe Frozen Dessert market is segmented by product type into ice cream, gelato, frozen yogurt, sorbet, and other frozen desserts. Among these, ice cream holds the dominant market share due to its established popularity and wide range of flavors. Ice cream's engrained presence in European culture and the increasing availability of premium varieties have ensured its sustained dominance. Innovations such as dairy-free ice cream and the introduction of exotic flavors have also contributed to maintaining this segments top position.

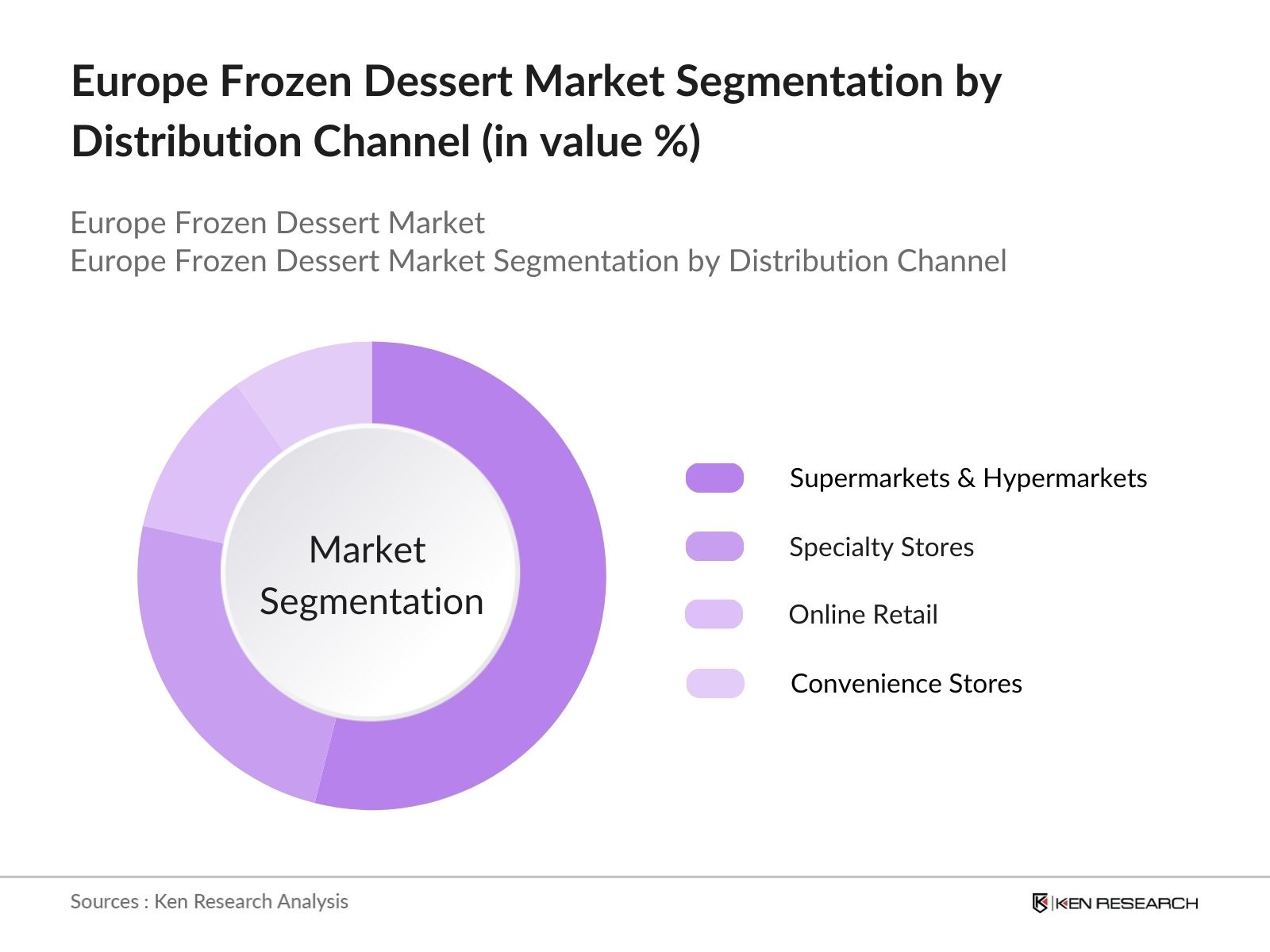

By Distribution Channel: Europes frozen dessert market is also segmented by distribution channels, including supermarkets & hypermarkets, specialty stores, online retail, and convenience stores. Supermarkets & hypermarkets dominate this segment due to their vast network, large product offerings, and discounts. Consumers often prefer these stores because they offer a wide range of frozen desserts, including both premium and budget-friendly options, all under one roof, which makes them a preferred choice for frozen dessert purchases.

The Europe Frozen Dessert market is dominated by several key players, including both global giants and regional specialists. The landscape is characterized by strong competition, innovation, and constant product diversification. Companies are expanding their portfolios to include healthier options, with a focus on plant-based and organic ingredients. This competition is fueled by changing consumer preferences, leading to a constant push for new flavors and sustainable packaging.

Over the next five years, the Europe Frozen Dessert market is expected to exhibit significant growth, driven by the increasing consumer demand for healthier, low-sugar, and dairy-free alternatives. The rise of plant-based diets and the premiumization of frozen dessert products are also anticipated to drive this growth. Companies are likely to invest in research and development to offer innovative flavors and sustainable packaging solutions, further enhancing the consumer appeal of frozen desserts.

|

By Product Type |

Ice Cream Gelato Sorbet Frozen Yogurt Other Frozen Desserts |

|

By Distribution Channel |

Supermarkets & Hypermarkets Specialty Stores Online Retail Convenience Stores |

|

By End Consumer |

Retail Consumers Foodservice & Hospitality |

|

By Ingredient Type |

Dairy-Based Plant-Based (Vegan) Low-Fat & Low-Sugar |

|

By Region |

West East South North |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Market Growth Rate (in Value %)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Consumer Demand for Healthier Dessert Options (Increased consumer preference for plant-based ingredients)

3.1.2. Technological Advancements in Freezing Techniques (Impact on production efficiency)

3.1.3. Expansion of Retail Chains and E-Commerce Platforms (Broader market access)

3.1.4. Shift Towards Premium Products (Higher spending on luxury frozen desserts)

3.2. Market Challenges

3.2.1. Seasonal Dependency (High summer demand, low winter sales)

3.2.2. High Energy Consumption in Cold Storage (Rising energy costs impacting profitability)

3.2.3. Supply Chain Disruptions (Impact of temperature-sensitive logistics)

3.2.4. Regulatory Standards on Food Additives (Adapting to changing regulations)

3.3. Opportunities

3.3.1. Increasing Demand for Organic and Vegan Products (Expanding the product portfolio)

3.3.2. New Flavors and Ingredient Innovation (Customization and flavor experiments)

3.3.3. Partnerships with Grocery Retail Chains (Strategic distribution alliances)

3.3.4. Growth in Private Label Brands (Retailers expanding frozen dessert offerings)

3.4. Trends

3.4.1. Rising Popularity of Artisanal Frozen Desserts (Niche market growth)

3.4.2. Demand for Dairy-Free and Low-Sugar Variants (Targeting health-conscious consumers)

3.4.3. Adoption of Sustainable Packaging Solutions (Focus on eco-friendly packaging)

3.4.4. Increasing Penetration of Plant-Based Frozen Desserts (Vegan products)

3.5. Government Regulations

3.5.1. EU Food Safety Standards (Compliance with EU regulations)

3.5.2. Packaging Waste Regulations (Reduction of plastic usage)

3.5.3. Nutrition Labeling Requirements (Impact on product labeling)

3.5.4. Tax on Sugary Products (Implications of health-focused taxation)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Retailers, manufacturers, distributors)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Ice Cream

4.1.2. Gelato

4.1.3. Sorbet

4.1.4. Frozen Yogurt

4.1.5. Other Frozen Desserts

4.2. By Distribution Channel (In Value %)

4.2.1. Supermarkets & Hypermarkets

4.2.2. Specialty Stores

4.2.3. Online Retail

4.2.4. Convenience Stores

4.3. By End Consumer (In Value %)

4.3.1. Retail Consumers

4.3.2. Foodservice & Hospitality

4.4. By Ingredient Type (In Value %)

4.4.1. Dairy-Based

4.4.2. Plant-Based (Vegan)

4.4.3. Low-Fat & Low-Sugar

4.5. By Region (In Value %)

4.5.1. Western Europe

4.5.2. Eastern Europe

4.5.3. Southern Europe

4.5.4. Northern Europe

5.1. Detailed Profiles of Major Companies

5.1.1. Unilever

5.1.2. Nestl S.A.

5.1.3. Froneri International Ltd

5.1.4. General Mills Inc.

5.1.5. Mars, Incorporated

5.1.6. Valsoia S.p.A

5.1.7. Ledo Plus

5.1.8. Lotus Bakeries

5.1.9. Amorino Gelato

5.1.10. Emmi Group

5.1.11. Gelatelli (ALDI)

5.1.12. Yeo Valley

5.1.13. R&R Ice Cream

5.1.14. Danone

5.1.15. Frusco Gelato

5.2. Cross Comparison Parameters (Revenue, Product Portfolio, Distribution Network, Sustainability Initiatives, Regional Presence, Innovation Capabilities, Number of Employees, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers & Acquisitions, Partnerships, New Product Launches)

5.5. Investment and Funding Overview

5.6. Venture Capital Funding

5.7. Government Grants

5.8. Private Equity Investments

6.1. EU Food Safety and Hygiene Standards

6.2. Sugar Reduction Policies

6.3. Compliance Requirements for Plant-Based and Dairy-Free Labels

6.4. Packaging Regulations and Sustainability Goals

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Distribution Channel (In Value %)

8.3. By End Consumer (In Value %)

8.4. By Ingredient Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior Insights (Vegan and Health-Conscious Segment)

9.3. Branding and Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase of research includes mapping the ecosystem of the Europe Frozen Dessert Market. Primary research sources include desk reviews, government databases, and proprietary resources. Critical variables such as consumer behavior, distribution channels, and market dynamics are identified for further analysis.

In this phase, historical market data is analyzed to construct a detailed picture of market dynamics. Factors such as penetration rate, product distribution, and revenue from various distribution channels are considered to ensure accurate analysis.

Market hypotheses are validated using expert interviews with key industry players, including manufacturers, distributors, and food industry experts. Insights gathered from these consultations offer deeper operational understanding, helping refine market forecasts and trend analysis.

The final stage involves synthesizing the collected data with insights from direct consultations. This ensures that the output is accurate and reflective of the real-world scenario of the Europe Frozen Dessert Market. The analysis will also include cross-verification with market performance data to ensure comprehensive and validated results.

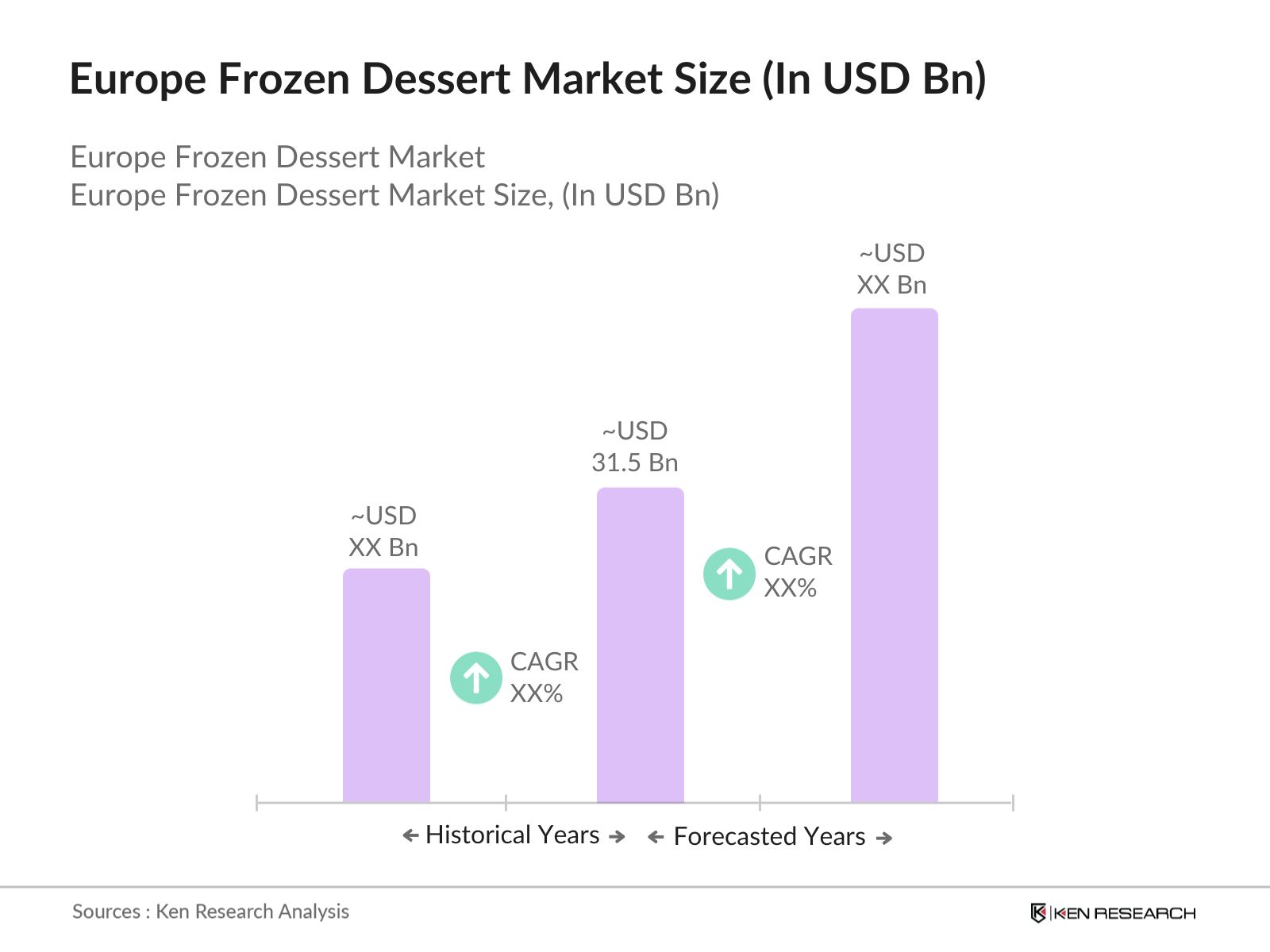

The Europe Frozen Dessert Market was valued at USD 31.5 billion, driven by consumer demand for healthier dessert options and the rise of vegan and low-sugar alternatives.

Challenges in the Europe Frozen Dessert Market include high energy consumption in cold storage, fluctuating raw material prices, and the need for compliance with stringent EU food safety and packaging regulations.

Key players include Unilever, Nestl S.A., Froneri International Ltd, General Mills Inc., and Mars, Incorporated. These companies lead due to their diverse product offerings and strong brand presence.

Growth of Europe Frozen Dessert Market is driven by rising consumer demand for dairy-free, organic, and low-sugar frozen desserts. The increasing adoption of plant-based diets and innovative product offerings also fuel market expansion.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.