Europe Gypsum Market Outlook to 2030

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD6610

November 2024

85

About the Report

Europe Gypsum Market Overview

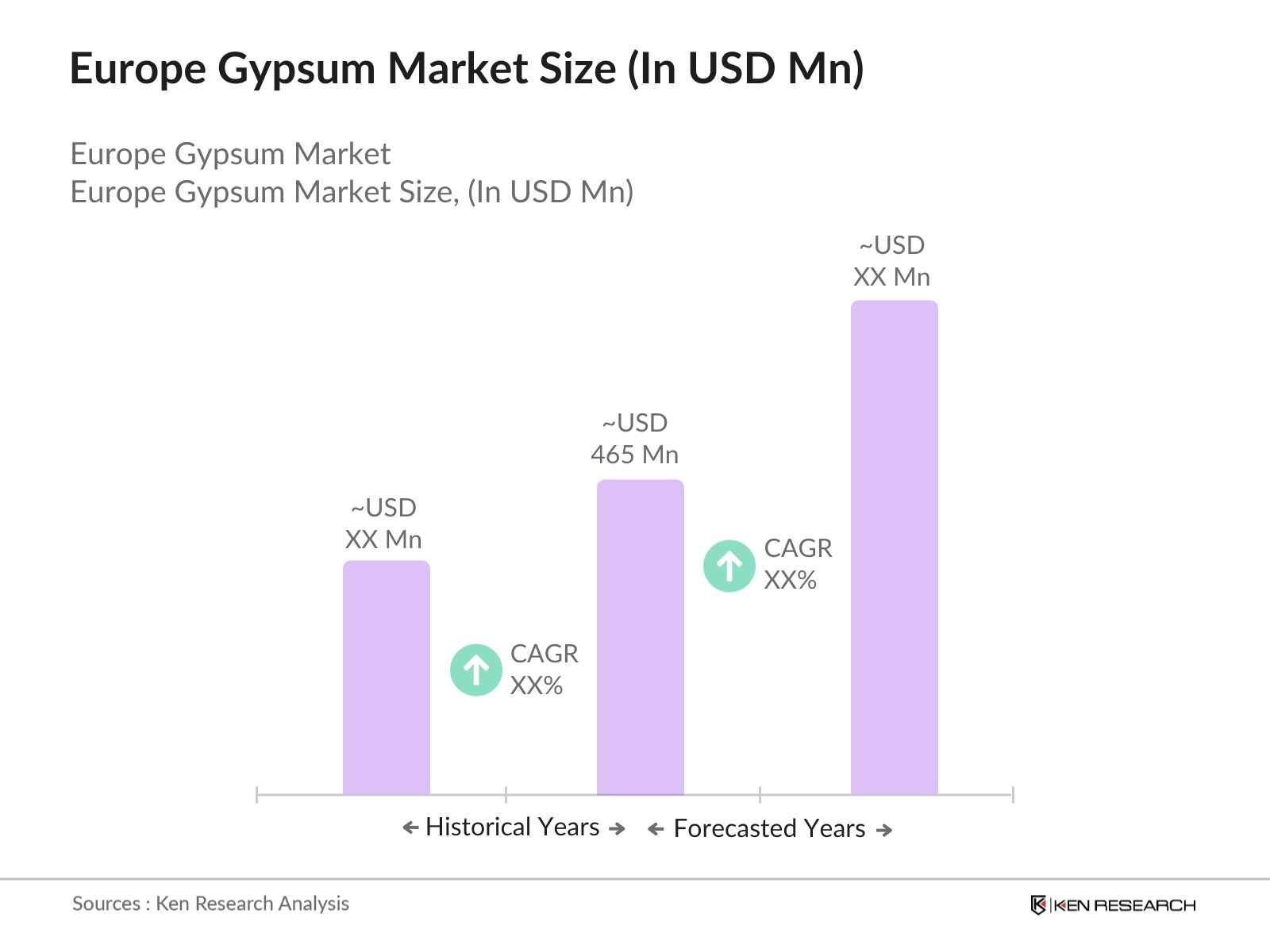

- The Europe gypsum market, valued at USD 465 Million based on a five-year historical analysis, is primarily driven by increasing construction activities across the region. Demand for gypsum is fueled by its critical role in producing drywall and plaster, widely used in both residential and commercial construction projects. In particular, the drive towards more sustainable building materials has bolstered the adoption of gypsum due to its eco-friendly nature and recyclability. The market has witnessed steady growth, with accelerated demand for energy-efficient building materials.

- Countries like Germany, the UK, and France dominate the Europe gypsum market due to their robust construction sectors and stringent environmental regulations. Germany, in particular, benefits from advanced infrastructure and innovation in the construction materials sector, while the UKs booming residential market drives gypsum consumption. Frances stringent green building codes further amplify the demand for gypsum-based materials, reinforcing these countries' positions as leaders in the market.

- The European Union's Circular Economy Action Plan, introduced in 2020, has led to stringent regulations on the recycling and sustainable use of construction materials, including gypsum. By 2024, the EU had imposed a minimum recycling rate of 70% for construction and demolition waste, pushing manufacturers to increase their use of recycled gypsum. This government initiative is anticipated to further boost the demand for gypsum recycling systems in the coming years.

Europe Gypsum Market Segmentation

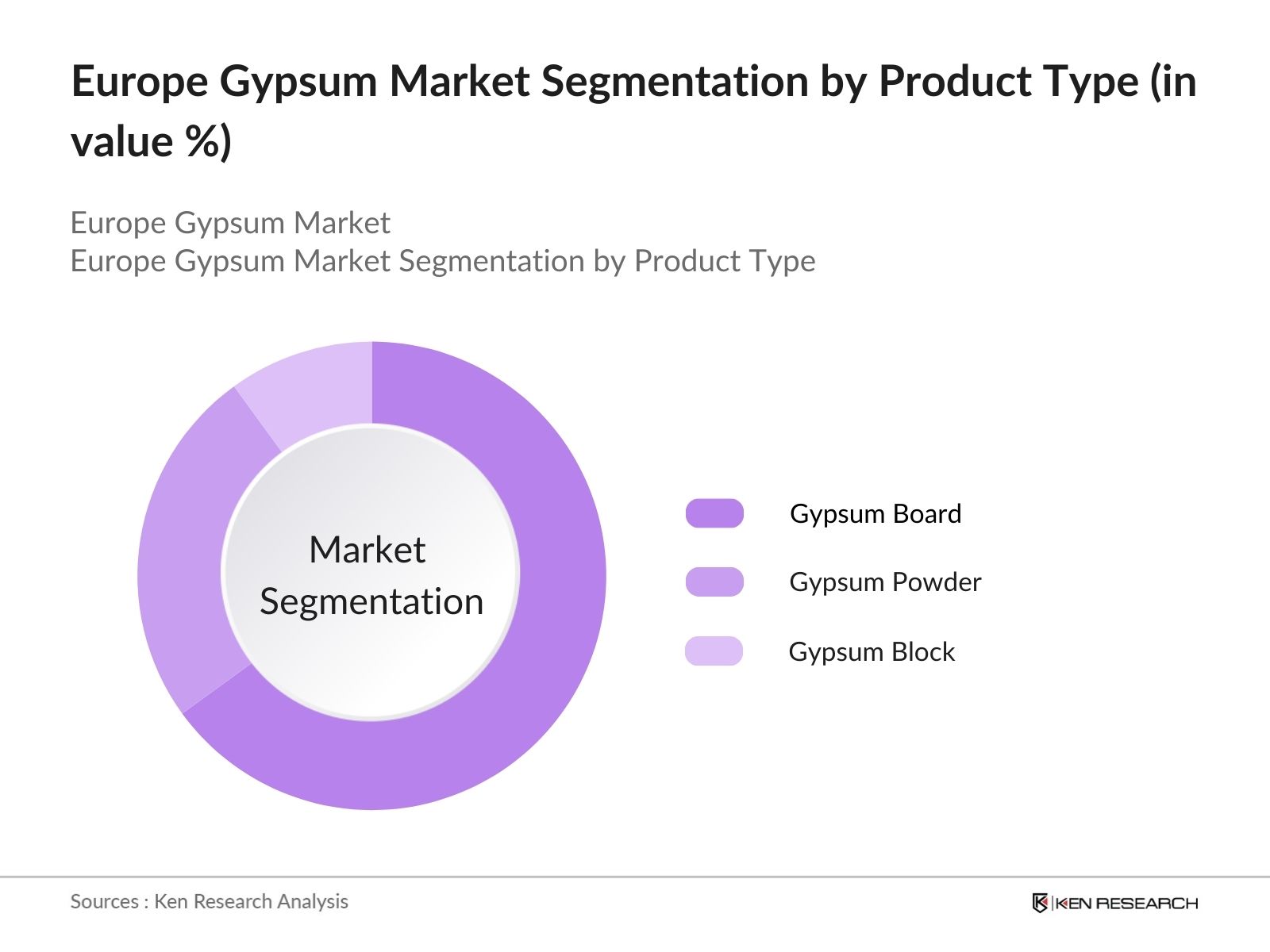

- By Product Type: The Europe gypsum market is segmented by product type into gypsum boards, gypsum powder, and gypsum blocks. Gypsum boards currently hold the dominant market share under this segmentation. This dominance is attributed to the materials extensive use in the construction of walls and ceilings, particularly in the residential and commercial sectors. Additionally, the demand for fire-resistant and soundproof materials has propelled the adoption of gypsum boards. With rising construction standards and the increasing need for lightweight building materials, gypsum boards continue to dominate the product type segment.

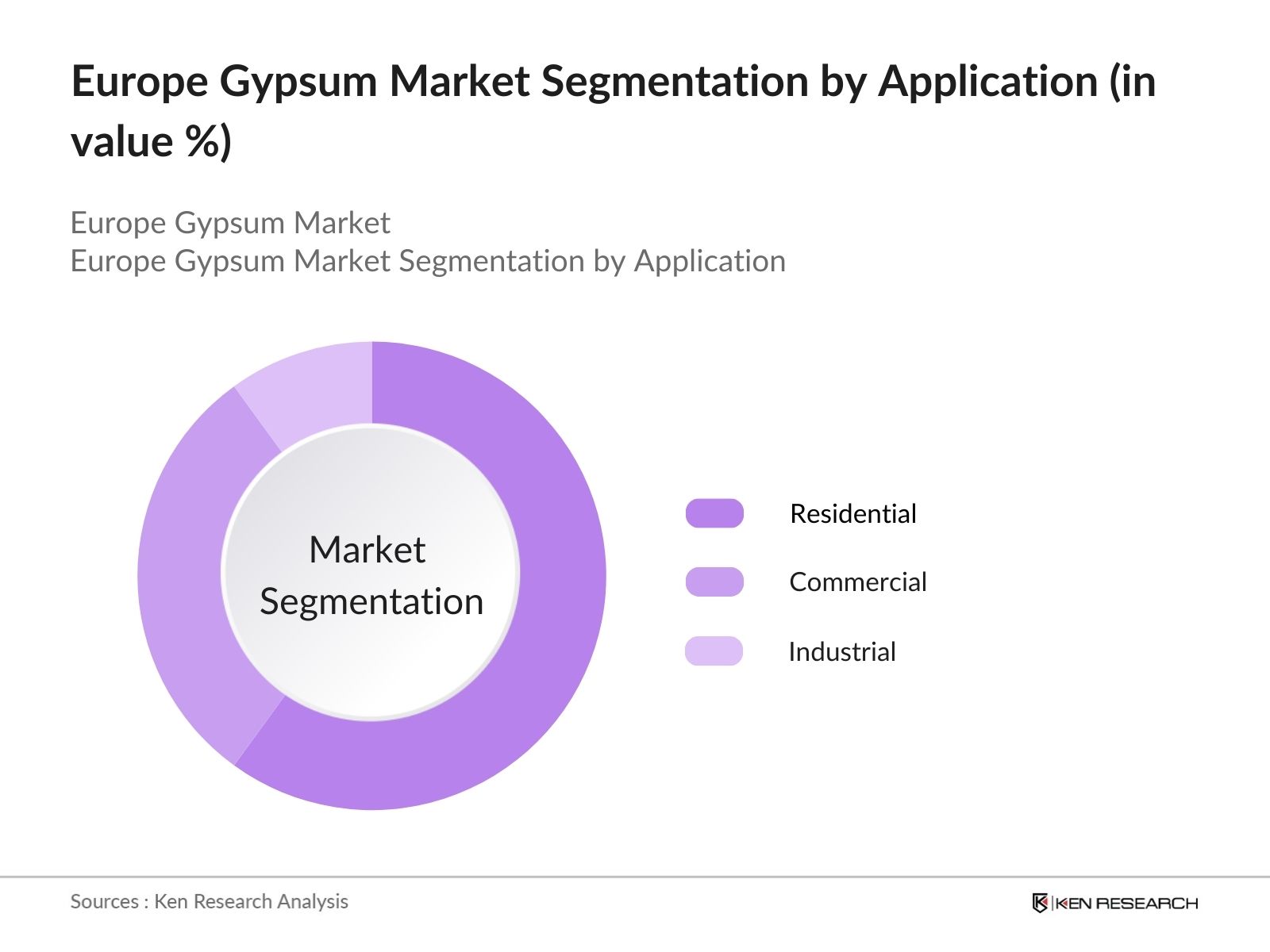

- By Application: The market is further segmented by application into residential construction, commercial construction, and industrial construction. Residential construction dominates this segment due to a high demand for drywall and plaster in building homes, renovations, and energy-efficient building projects. With growing urbanization and a focus on sustainability, gypsum-based materials are preferred for their recyclable nature and ease of use in residential building frameworks. In particular, the trend towards modular housing and pre-fabricated structures has solidified the position of residential applications in the gypsum market.

Europe Gypsum Market Competitive Landscape

The Europe gypsum market is dominated by several key players, with a competitive landscape shaped by innovation, sustainability initiatives, and the ability to meet the increasing demand for energy-efficient building materials. These companies are positioned strategically to benefit from both regional and global demand for gypsum products.

|

Company Name |

Year of Establishment |

Headquarters |

Production Capacity (Million Tons) |

Number of Employees |

Sustainability Initiatives |

R&D Investment (USD Mn) |

Regional Presence |

M&A Activities |

Product Portfolio |

|

Saint-Gobain |

1665 |

Paris, France |

- | - | - | - | - | - | - |

|

Knauf |

1932 |

Iphofen, Germany |

- | - | - | - | - | - | - |

|

Etex Group |

1905 |

Zaventem, Belgium |

- | - | - | - | - | - | - |

|

Fermacell GmbH |

1971 |

Dsseldorf, Germany |

- | - | - | - | - | - | - |

|

USG Boral |

2014 |

Kuala Lumpur, Malaysia |

- | - | - | - | - | - | - |

Europe Gypsum Market Analysis

Market Growth Drivers

- Sustainable Construction Demand: The demand for sustainable construction materials in Europe has surged due to stricter environmental policies aimed at reducing carbon emissions in the building sector. Gypsum, a low-carbon material, has gained traction as a preferred choice for sustainable construction. In 2024, the European Union reported a significant increase in the use of gypsum in construction, with over 12 million tons of gypsum products consumed in sustainable building projects. The material's recyclability, combined with its energy-efficient production process, positions it as a cornerstone for sustainable construction practices across Europe.

- Rising Gypsum Recycling Initiatives: Governments across Europe are increasingly encouraging gypsum recycling to reduce waste and promote circular economy models. In 2023, France alone recycled over 600,000 tons of gypsum waste, primarily from the construction and demolition sectors. Recycling gypsum is both economically viable and environmentally friendly, as it reduces the need for quarrying, lowering environmental degradation. This initiative is supported by EU directives that incentivize the recycling of construction materials, further driving the recycling rates across the region.

- Government Regulations on Carbon Reduction: In 2024, new EU regulations focusing on carbon footprint reduction have propelled the adoption of gypsum-based materials in the construction industry. Gypsum plasterboard is being increasingly used because of its low energy requirements during production and its role in reducing carbon emissions in buildings. Government mandates are pushing construction companies to adopt materials that align with green building standards, leading to a higher demand for gypsum-based products. This regulatory environment is forecast to further boost gypsum use in construction projects through 2025.

Market Challenges

- Volatility in Raw Material Prices (Gypsum, Cement): The gypsum market in Europe has faced challenges due to the volatility in raw material prices, particularly the cost of gypsum and cement. In 2024, the price of raw gypsum experienced fluctuations, ranging between 45 and 65 per ton, which impacted the production costs for gypsum-based products. This price volatility is influenced by several factors, including energy costs, transportation expenses, and supply chain disruptions, making it difficult for manufacturers to maintain consistent profit margins.

- High Transportation Costs (Region-Specific Logistics): Transportation costs for gypsum are particularly high in countries with limited local gypsum production, such as the UK and Italy, where materials must be imported from other regions. In 2024, logistics costs for transporting gypsum within Europe ranged from 10 to 20 per ton, depending on the distance and the country's logistics infrastructure. This high cost is further exacerbated by increasing fuel prices and regulatory measures on CO2 emissions from freight transportation, making logistics a major cost driver for gypsum manufacturers.

Europe Gypsum Market Future Outlook

Over the next five years, the Europe gypsum market is expected to experience significant growth driven by an increasing focus on green building materials, stringent energy efficiency regulations, and growing investments in urban infrastructure. Governments in the region continue to push for sustainable development, leading to higher demand for eco-friendly construction materials like gypsum. Innovation in recycling and the circular economy will further boost the market as manufacturers adopt waste reduction practices, improving both environmental impact and profitability.

Market Opportunities

- Innovation in Lightweight Gypsum Boards: The development of lightweight gypsum boards presents an opportunity for manufacturers to meet the growing demand for energy-efficient and easy-to-install construction materials. In 2023, European manufacturers launched new gypsum board products weighing between 15% to 30% less than traditional boards, reducing transportation costs and installation time. This innovation is particularly beneficial for high-rise buildings and complex architectural designs, offering a competitive advantage for companies that adopt these advanced products.

- Increased Use in Green Buildings: The EUs focus on green building initiatives has created a substantial opportunity for gypsum manufacturers. In 2024, it was reported that 1.2 million square meters of green building projects across Europe incorporated gypsum-based products due to their energy efficiency and recyclability. This trend is expected to continue, with the European Commission setting ambitious targets for green building certifications that include mandatory use of low-emission materials such as gypsum.

Scope of the Report

|

By Product Type |

Gypsum Board Gypsum Plaster Gypsum Powder Gypsum Blocks |

|

By Application |

Residential Construction Commercial Construction Industrial, Infrastructure |

|

By End-User |

New Construction Renovation Activities |

|

By Distribution Channel |

Direct Sales Distributors and Retailers Online Sales |

|

By Region |

West East North South |

Products

Key Target Audience

Gypsum Manufacturers

Construction and Infrastructure Companies

Real Estate Developers

Interior Design Firms

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (European Environment Agency, European Commission)

Recycling Firms

Energy-Efficient Product Innovators

Companies

Players Mentioned in the Report:

Saint-Gobain

Knauf Gips KG

Etex Group

USG Boral

Fermacell GmbH

Siniat Ltd.

Promat International

Gypfor

Pladur Gypsum

ArcelorMittal

Table of Contents

1. Europe Gypsum Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Europe Gypsum Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Europe Gypsum Market Analysis

3.1. Growth Drivers

3.1.1. Sustainable Construction Demand

3.1.2. Rising Gypsum Recycling Initiatives

3.1.3. Government Regulations on Carbon Reduction

3.1.4. Expansion of Urban Infrastructure

3.2. Market Challenges

3.2.1. Volatility in Raw Material Prices (Gypsum, Cement)

3.2.2. High Transportation Costs (Region-Specific Logistics)

3.2.3. Environmental Impact of Quarrying Activities

3.3. Opportunities

3.3.1. Innovation in Lightweight Gypsum Boards

3.3.2. Increased Use in Green Buildings

3.3.3. Collaboration with Recyclers and Sustainability Initiatives

3.4. Trends

3.4.1. Use of Gypsum in Fire-Resistant Construction

3.4.2. Expansion of Pre-Fabricated Construction Materials

3.4.3. Growth in Gypsum-Based Interior Finishes

3.5. Government Regulation

3.5.1. EU Construction Product Regulation (CPR)

3.5.2. Circular Economy Action Plan Compliance

3.5.3. Waste Framework Directive on Gypsum Recycling

3.5.4. Building Emission Standards in Key European Countries

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Gypsum Manufacturers, Recyclers, Contractors)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Europe Gypsum Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Gypsum Board

4.1.2. Gypsum Plaster

4.1.3. Gypsum Powder

4.1.4. Gypsum Blocks

4.2. By Application (In Value %)

4.2.1. Residential Construction

4.2.2. Commercial Construction

4.2.3. Industrial

4.2.4. Infrastructure

4.3. By End-User (In Value %)

4.3.1. New Construction

4.3.2. Renovation Activities

4.4. By Distribution Channel (In Value %)

4.4.1. Direct Sales

4.4.2. Distributors and Retailers

4.4.3. Online Sales

4.5. By Region (In Value %)

4.5.1. Western Europe

4.5.2. Eastern Europe

4.5.3. Northern Europe

4.5.4. Southern Europe

5. Europe Gypsum Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Saint-Gobain

5.1.2. Knauf Gips KG

5.1.3. Etex Group

5.1.4. Fermacell GmbH

5.1.5. USG Boral

5.1.6. Siniat Ltd.

5.1.7. Gypfor

5.1.8. Pladur Gypsum

5.1.9. Promat International

5.1.10. Global Gypsum Co.

5.1.11. ArcelorMittal

5.1.12. Gyproc Iberica

5.1.13. El-Khayyat Gypsum

5.1.14. Volma

5.1.15. Georgia-Pacific

5.2. Cross Comparison Parameters (Revenue, Market Share, Sustainability Initiatives, Regional Presence, Product Portfolio, Innovation Capabilities, Mergers & Acquisitions, Production Capacity)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Government Funding

5.8. Sustainability Investments

6. Europe Gypsum Market Regulatory Framework

6.1. European Union Regulations on Gypsum Products

6.2. Compliance Requirements (Fire Safety Standards, Environmental Laws)

6.3. Certification Processes (ISO 14001, CE Marking, BBA Certification)

7. Europe Gypsum Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Europe Gypsum Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9. Europe Gypsum Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step in the research involved developing an extensive ecosystem map to identify major stakeholders in the Europe Gypsum market, including manufacturers, distributors, construction companies, and regulatory bodies. Secondary research was conducted through reputable databases, including industry reports and government publications, to define critical variables affecting market growth.

Step 2: Market Analysis and Construction

In this phase, historical data on gypsum production, consumption patterns, and regional market penetration was compiled and analyzed. The analysis included evaluating the market's production-to-consumption ratio and pricing trends across key countries. The revenue impact was estimated based on verified data sources.

Step 3: Hypothesis Validation and Expert Consultation

We conducted interviews with industry experts using computer-assisted telephone interviews (CATI) to validate initial hypotheses and gather additional insights on market trends, competition, and production constraints. These expert consultations ensured accurate data collection for the European market.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing primary and secondary data to deliver a comprehensive analysis of the Europe Gypsum market. Insights from industry leaders, product innovation trends, and market performance were consolidated to provide a well-rounded market overview.

Frequently Asked Questions

01. How big is the Europe Gypsum Market?

The Europe Gypsum market is valued at USD 465 Million, driven by the increasing demand for sustainable construction materials and advancements in gypsum recycling technology.

02. What are the challenges in the Europe Gypsum Market?

Challenges in the Europe Gypsum market include volatility in raw material prices, particularly for gypsum and associated transportation costs, and the environmental concerns related to gypsum quarrying activities.

03. Who are the major players in the Europe Gypsum Market?

Key players in the Europe Gypsum market include Saint-Gobain, Knauf Gips KG, Etex Group, USG Boral, and Fermacell GmbH, all of which dominate due to their established production capacities, innovation, and strong distribution networks.

04. What are the growth drivers of the Europe Gypsum Market?

Growth drivers in the Europe Gypsum market include the rise in sustainable construction practices, government regulations targeting carbon reduction, and increasing urbanization, particularly in key markets such as Germany, France, and the UK.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.