Europe HVAC Market Outlook to 2030

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD3945

December 2024

99

About the Report

Europe HVAC Market Overview

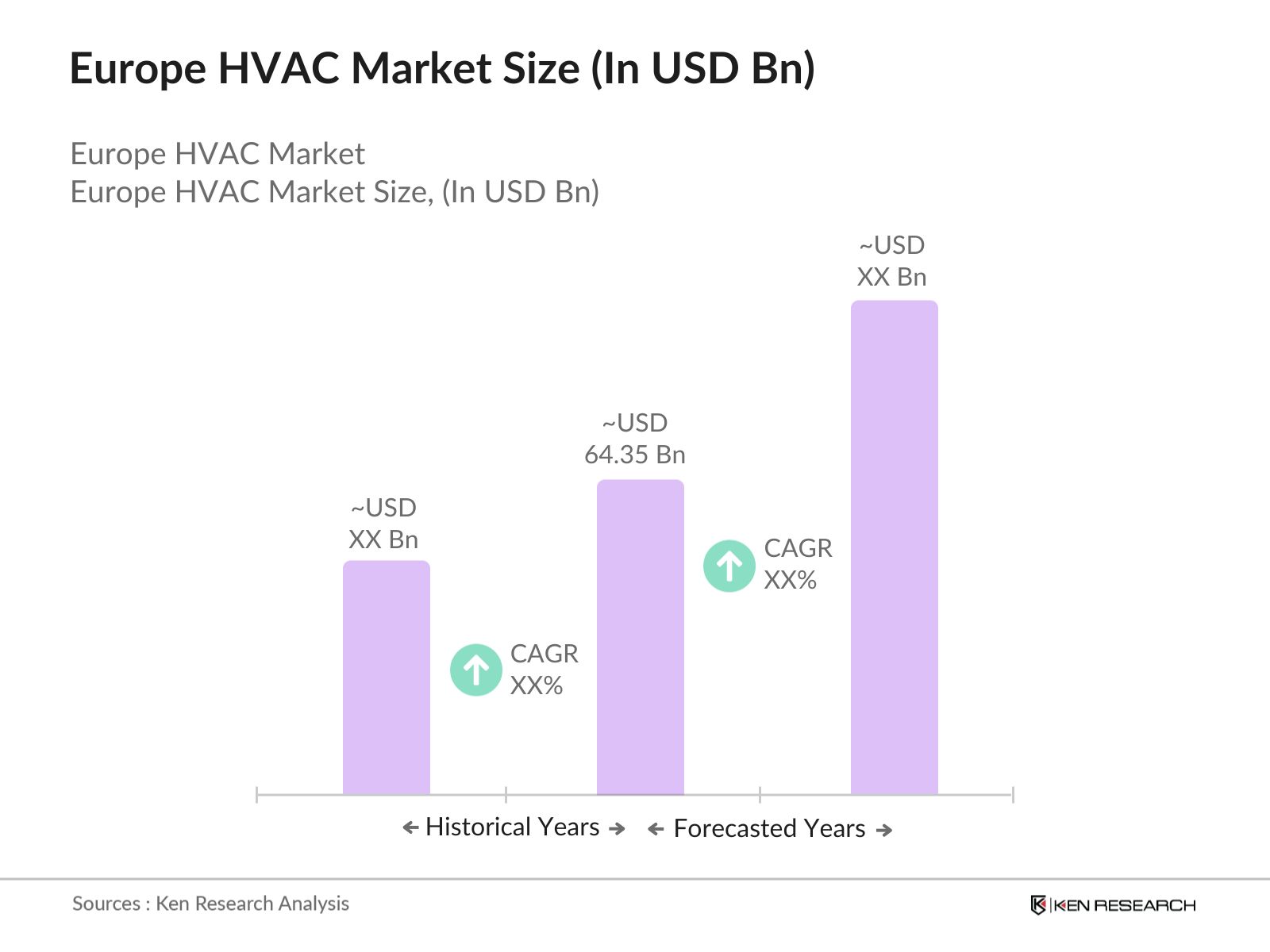

- The Europe HVAC market is valued at USD 64.35 billion, based on a five-year historical analysis. This market is primarily driven by the rising demand for energy-efficient systems, supported by stringent government regulations promoting sustainability. Increasing investments in green infrastructure and growing consumer awareness about climate change have further accelerated market growth. In addition, urbanization and retrofitting of older buildings with modern HVAC systems have boosted market demand.

- Germany, the United Kingdom, and France dominate the European HVAC market. Germany leads due to its industrial strength, high emphasis on energy efficiency, and government incentives for renewable technologies. The UKs market dominance stems from its advanced construction industry and focus on smart cities. France follows closely due to supportive policies, particularly around reducing carbon emissions, and a robust real estate sector.

- The EU's "Fit for 55" package, launched in July 2021, includes measures to reduce greenhouse gas emissions by 55% by 2030. Part of this initiative focuses on improving energy efficiency in buildings, encouraging the adoption of advanced HVAC systems across member states.

Europe HVAC Market Segmentation

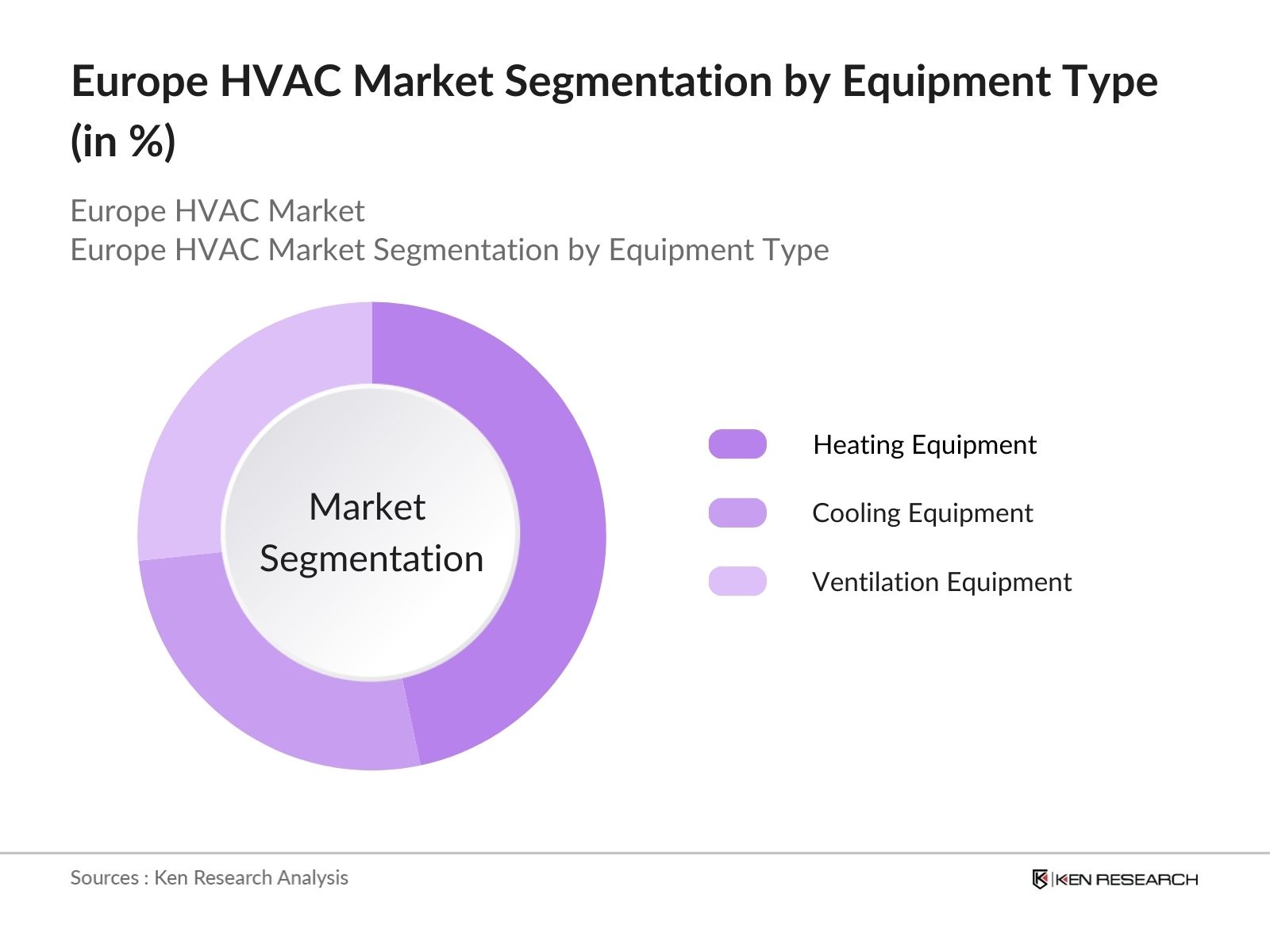

By Equipment Type: The Europe HVAC market is segmented by equipment type intoHeating Equipment,Cooling Equipment, andVentilation Equipment.Heating equipment, particularly heat pumps, holds a dominant share in the market. This is due to the increasing focus on energy efficiency and the European Unions regulations encouraging the adoption of renewable heating solutions. Heat pumps are extensively used in residential and commercial buildings for their dual functionality of heating and cooling.

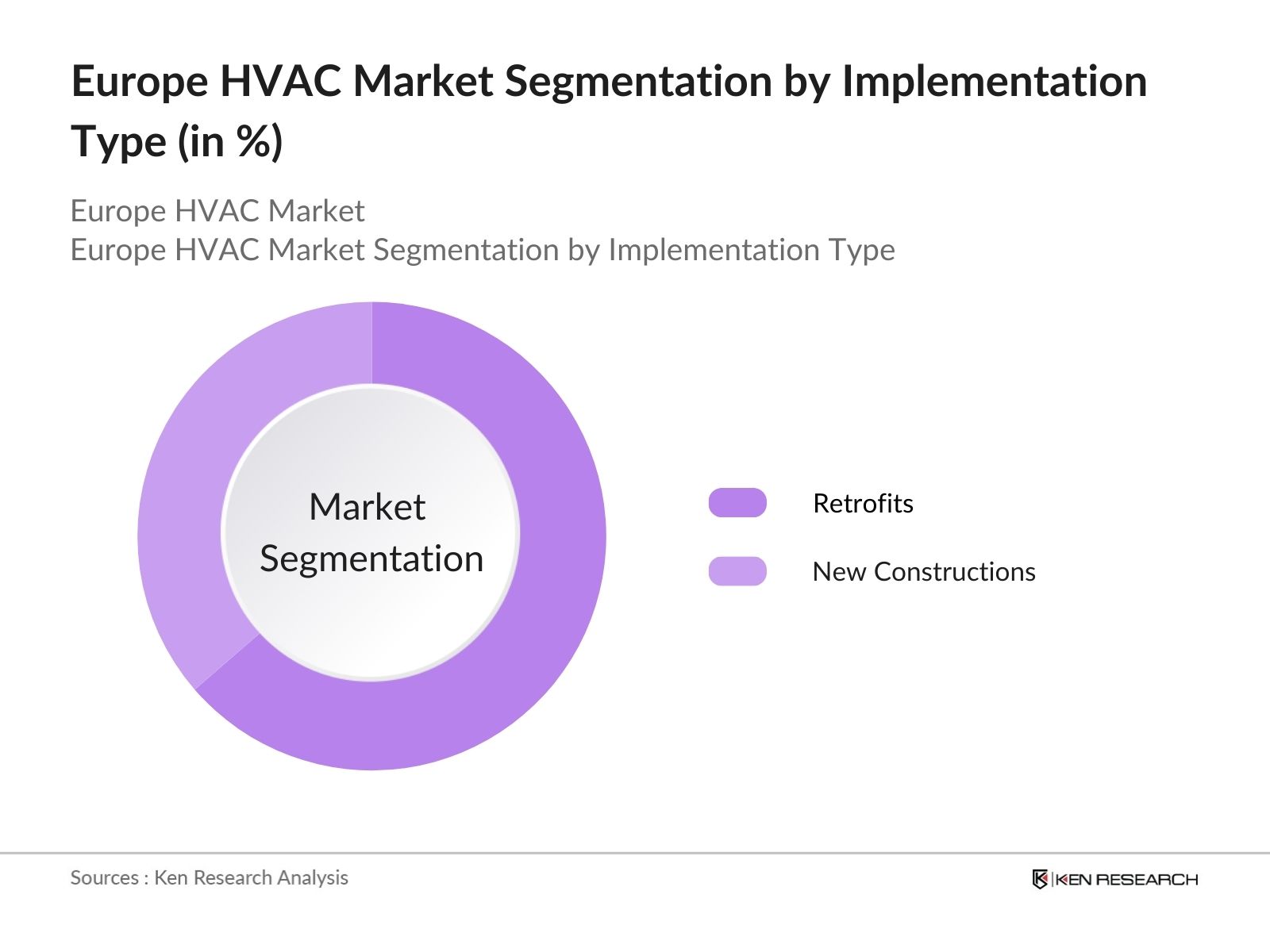

By Implementation Type: The market is segmented by implementation type intoNew ConstructionsandRetrofits. Retrofits dominate the segment due to widespread efforts to modernize aging infrastructure in Europe. The regions drive toward achieving zero-energy buildings by incorporating advanced HVAC systems plays a critical role in this trend.

Europe HVAC Market Competitive Landscape

The Europe HVAC market is dominated by major global and regional players. These companies drive innovation, expand their product portfolios, and integrate smart technologies to meet consumer demand.

Europe HVAC Market Market Analysis

Growth Drivers

- Energy Efficiency Regulations: Governments worldwide are implementing stringent energy efficiency standards for HVAC systems to reduce energy consumption and greenhouse gas emissions. For instance, the U.S. Department of Energy's updated energy conservation standards for residential HVAC equipment are projected to save approximately 2.3 quadrillion British thermal units (BTUs) of energy over 30 years, equivalent to the annual energy consumption of about 12 million homes. These regulations are compelling manufacturers to develop more efficient HVAC solutions, driving market growth.

- Climate Change and Rising Temperatures: The increasing frequency of extreme weather events and rising global temperatures are boosting the demand for HVAC systems. According to the National Oceanic and Atmospheric Administration (NOAA), the average global temperature in 2023 was among the highest on record, leading to heightened demand for cooling solutions in both residential and commercial sectors.

- Technological Advancements: Innovations such as smart thermostats, variable refrigerant flow (VRF) systems, and advanced air filtration technologies are enhancing the efficiency and functionality of HVAC systems. The integration of Internet of Things (IoT) technologies allows for real-time monitoring and control, improving energy management and user comfort. For example, the adoption of smart HVAC systems is expected to increase by over 20 million units globally by 2025, driven by consumer demand for energy savings and convenience.

Market Challenges

- High Installation and Maintenance Costs: The upfront costs associated with purchasing and installing advanced HVAC systems can be substantial. For instance, the average cost of installing a central air conditioning system in the U.S. ranges from $5,000 to $10,000, depending on the system's complexity and home size. Additionally, regular maintenance is essential to ensure optimal performance, adding to the overall expense for consumers.

- Regulatory Compliance: Adhering to varying regional regulations and standards poses a challenge for HVAC manufacturers and service providers. For example, the European Union's F-Gas Regulation mandates a phasedown of hydrofluorocarbons (HFCs), requiring companies to transition to low-global-warming-potential refrigerants. Compliance necessitates significant investment in research, development, and training.

Europe HVAC Market Future Outlook

Over the next five years, the Europe HVAC market is expected to experience steady growth. This expansion will be driven by technological advancements, the integration of IoT into HVAC systems, and government incentives for energy-efficient buildings. Furthermore, growing concerns about environmental sustainability will lead to increased adoption of green HVAC solutions.

Market Opportunities

- Integration of IoT and Smart Technologies: The adoption of IoT-enabled HVAC systems is on the rise, offering features like remote monitoring, predictive maintenance, and energy optimization. The global smart HVAC market is expected to reach $28 billion by 2025, driven by consumer demand for connected home solutions and energy efficiency.

- Expansion into Emerging Markets: Rapid urbanization and industrialization in countries like India, China, and Brazil are creating significant opportunities for HVAC market expansion. For example, India's HVAC market is projected to grow substantially, with the residential air conditioning segment expected to add over 5 million units annually by 2025, driven by rising incomes and increasing temperatures.

Scope of the Report

|

By Equipment Type |

Heat Pumps Boilers Furnaces Air Handling Units VRF Systems Chillers |

|

By Implementation Type |

New Constructions Retrofits |

|

By End Use |

Residential Commercial Industrial |

|

By Technology Type |

Smart HVAC Systems Traditional HVAC Systems |

|

By Country |

Germany United Kingdom France Italy Spain Netherlands Rest of Europe |

Products

Key Target Audience

HVAC Manufacturers

Real Estate Developers

Energy Management Firms

Government and Regulatory Bodies (e.g., European Commission, National Energy Agencies)

Investors and Venture Capitalist Firms

Construction and Infrastructure Companies

Renewable Energy Solution Providers

Smart City Project Developers

Companies

Players Mentioned in the Market:

Daikin Industries Ltd.

Carrier Global Corporation

Johnson Controls International plc

Mitsubishi Electric Corporation

Trane Technologies plc

Bosch Thermotechnik GmbH

Vaillant Group

LG Electronics Inc.

Panasonic Corporation

Fujitsu General Limited

Table of Contents

1. Europe HVAC Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Europe HVAC Market Size (USD Billion)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Europe HVAC Market Analysis

3.1 Growth Drivers

3.1.1 Urbanization and Infrastructure Development

3.1.2 Energy Efficiency Regulations

3.1.3 Technological Advancements

3.1.4 Climate Change and Rising Temperatures

3.2 Market Challenges

3.2.1 High Installation and Maintenance Costs

3.2.2 Regulatory Compliance

3.2.3 Skilled Labor Shortage

3.3 Opportunities

3.3.1 Integration of IoT and Smart Technologies

3.3.2 Expansion into Emerging Markets

3.3.3 Renewable Energy Integration

3.4 Trends

3.4.1 Adoption of Green Building Standards

3.4.2 Demand for Indoor Air Quality Solutions

3.4.3 Shift Towards Heat Pump Technologies

3.5 Government Regulations

3.5.1 EU Energy Performance of Buildings Directive

3.5.2 F-Gas Regulations

3.5.3 National Renewable Energy Action Plans

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

4. Europe HVAC Market Segmentation

4.1 By Equipment Type (Value %)

4.1.1 Heating Equipment

4.1.1.1 Heat Pumps

4.1.1.2 Boilers

4.1.1.3 Furnaces

4.1.1.4 Others

4.1.2 Ventilation Equipment(Value %)

4.1.2.1 Air Handling Units

4.1.2.2 Air Filters and Purifiers

4.1.2.3 Ventilation Fans

4.1.2.4 Dehumidifiers and Humidifiers

4.1.2.5 Others

4.1.3 Cooling Equipment(Value %)

4.1.3.1 Unitary Air Conditioners

4.1.3.2 VRF Systems

4.1.3.3 Chillers

4.1.3.4 Coolers

4.1.3.5 Cooling Towers

4.1.3.6 Others

4.2 By Implementation Type (Value %)

4.2.1 New Constructions

4.2.2 Retrofits

4.3 By End Use (Value %)

4.3.1 Residential

4.3.2 Commercial

4.3.3 Industrial

4.4 By Country (Value %)

4.4.1 Germany

4.4.2 United Kingdom

4.4.3 France

4.4.4 Italy

4.4.5 Spain

4.4.6 Netherlands

4.4.7 Rest of Europe

5. Europe HVAC Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Daikin Industries Ltd.

5.1.2 Carrier Global Corporation

5.1.3 Johnson Controls International plc

5.1.4 Mitsubishi Electric Corporation

5.1.5 Trane Technologies plc

5.1.6 LG Electronics Inc.

5.1.7 Samsung Electronics Co., Ltd.

5.1.8 Lennox International Inc.

5.1.9 Bosch Thermotechnik GmbH

5.1.10 Vaillant Group

5.1.11 Danfoss A/S

5.1.12 Gree Electric Appliances Inc.

5.1.13 Midea Group Co., Ltd.

5.1.14 Fujitsu General Limited

5.1.15 Panasonic Corporation

5.2 Cross Comparison Parameters (Revenue, Market Share, Product Portfolio, Geographic Presence, R&D Investment, Strategic Initiatives, Number of Employees, Headquarters)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.6.1 Venture Capital Funding

5.6.2 Government Grants

5.6.3 Private Equity Investments

6. Europe HVAC Market Regulatory Framework

6.1 Environmental Standards

6.2 Compliance Requirements

6.3 Certification Processes

7. Europe HVAC Future Market Size (USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Europe HVAC Future Market Segmentation

8.1 By Equipment Type (Value %)

8.2 By Implementation Type (Value %)

8.3 By End Use (Value %)

8.4 By Country (Value %)

9. Europe HVAC Market Analysts Recommendations

9.1 Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Europe HVAC market. This step utilizes extensive desk research and secondary databases to gather industry-level information, identifying the critical variables influencing market dynamics.

Step 2: Market Analysis and Construction

This phase compiles and analyzes historical data on market penetration, implementation trends, and revenue generation. Evaluations of product efficiency and service quality further validate market insights.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and validated through interviews with industry experts from leading HVAC manufacturers. These insights refine data accuracy and add depth to market trends.

Step 4: Research Synthesis and Final Output

The final phase integrates data from manufacturers and proprietary tools to provide a comprehensive, validated analysis of the Europe HVAC market, including segmentation, growth drivers, and competitive dynamics.

Frequently Asked Questions

1. How big is the Europe HVAC Market?

The Europe HVAC market is valued at USD 64.35 billion, primarily driven by government regulations promoting sustainability and increasing investments in green technologies.

2. What are the challenges in the Europe HVAC Market?

Challenges in the Europe HVAC market include high installation costs, regulatory compliance requirements, and a shortage of skilled labor to install and maintain modern HVAC systems.

3. Who are the major players in the Europe HVAC Market?

Major players in the Europe HVAC market include Daikin Industries Ltd., Carrier Global Corporation, Johnson Controls International plc, Mitsubishi Electric Corporation, and Trane Technologies plc.

4. What are the growth drivers for the Europe HVAC Market?

Key drivers in the Europe HVAC market include advancements in energy-efficient technologies, government incentives for green buildings, and rising consumer awareness about climate change.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.