Europe Industrial Gases Market Outlook to 2030

Region:Europe

Author(s):Sanjeev

Product Code:KROD5712

Region:Europe

Author(s):Sanjeev

Product Code:KROD5712

November 2024

95

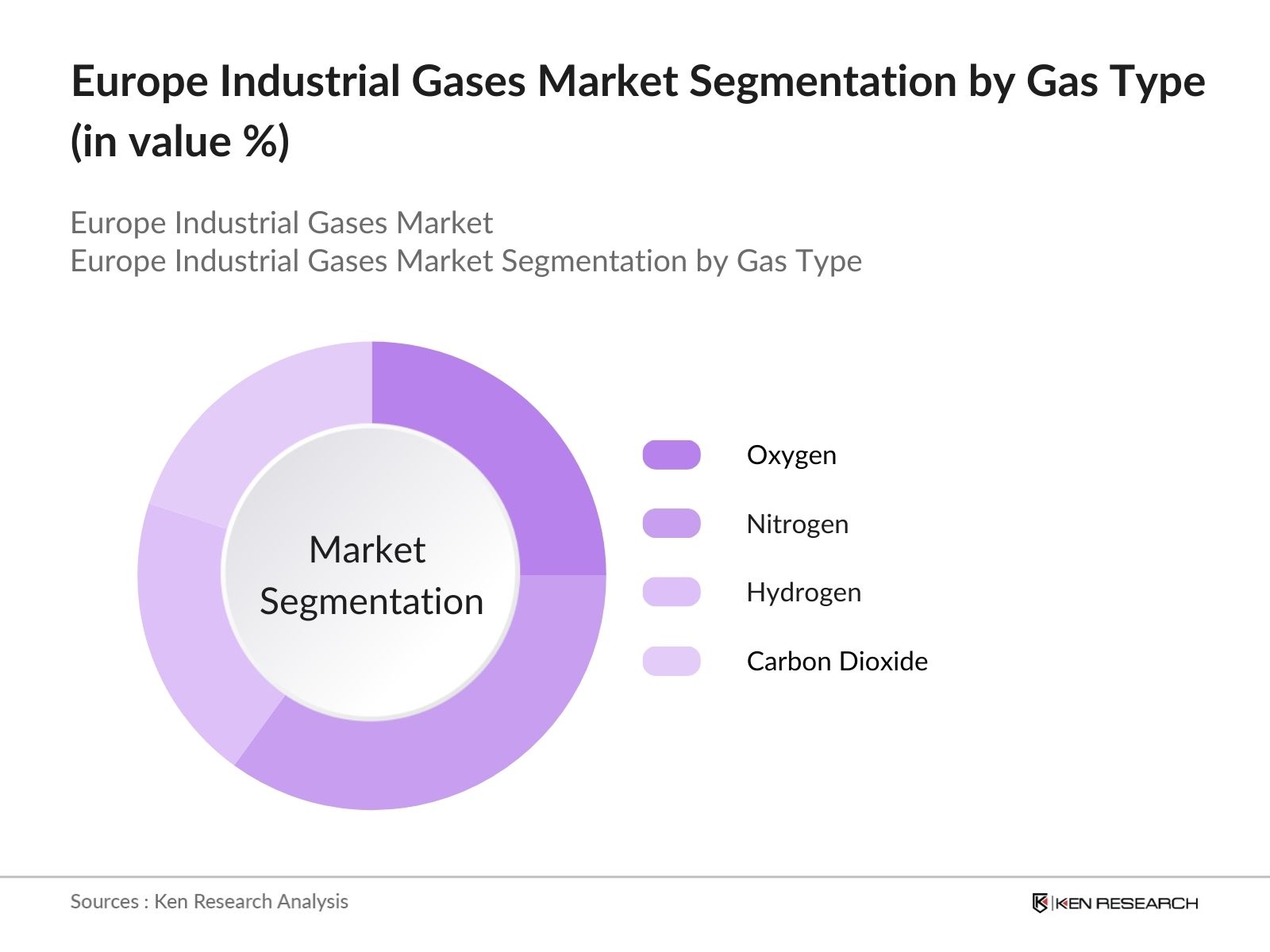

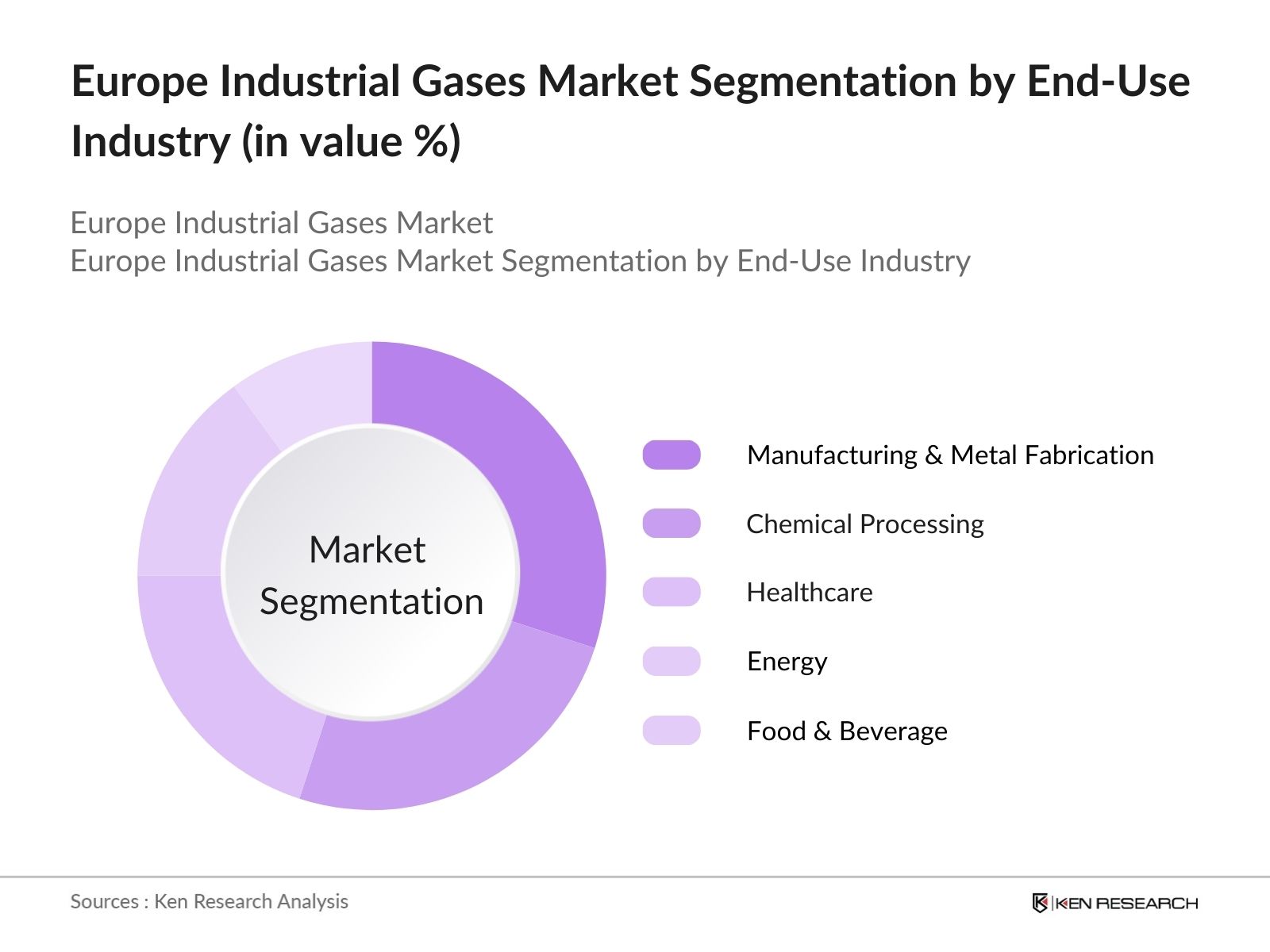

Europe's industrial gases market is segmented by gas type and by end-use industry.

The Europe industrial gases market is dominated by a few key players, with companies such as Linde plc, Air Liquide, and Messer Group leading in terms of innovation and strategic expansions. This consolidation underscores the influence of these companies and their established distribution networks across the region.

Over the coming years, the Europe industrial gases market is expected to experience significant growth due to the rise of green energy projects, increased adoption of hydrogen as an alternative fuel, and expanding applications in healthcare and environmental sectors. As industries prioritize sustainability, the demand for clean gases is likely to rise, making this sector integral to Europes green transition and circular economy initiatives.

|

Oxygen Nitrogen Argon Hydrogen Carbon Dioxide |

|

|

By End-Use Industry |

Manufacturing and Metal Fabrication Chemical Processing Food & Beverage Healthcare, Energy Sector |

|

By Production Technology |

Cryogenic Air Separation Non-Cryogenic Air Separation Hydrogen Production |

|

By Supply Mode |

Packaged Bulk On-Site Generation |

|

By Region |

North East West South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Key Market Dynamics

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Expanding Manufacturing Sector

3.1.2 Rise in Clean Energy Initiatives

3.1.3 Growth in the Food & Beverage Industry

3.1.4 Increased Demand in the Healthcare Sector

3.2 Market Challenges

3.2.1 High Storage and Transportation Costs

3.2.2 Stringent Regulatory Policies

3.2.3 Infrastructure Limitations

3.3 Opportunities

3.3.1 Emerging Applications in Electronics and Automotive Sectors

3.3.2 Government Support for Hydrogen Fuel Initiatives

3.3.3 Expansion of Carbon Capture and Utilization (CCU)

3.4 Trends

3.4.1 Increasing Adoption of On-Site Gas Generation Systems

3.4.2 Technological Advancements in Gas Purification

3.4.3 Shift towards Renewable Energy Sources for Gas Production

3.5 Regulatory Landscape

3.5.1 Emission Control Standards

3.5.2 European Union Regulations on Industrial Gases

3.5.3 Health and Safety Standards

3.5.4 Permits and Licensing Requirements

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape Mapping

4.1 By Gas Type (In Value %)

4.1.1 Oxygen

4.1.2 Nitrogen

4.1.3 Argon

4.1.4 Hydrogen

4.1.5 Carbon Dioxide

4.2 By End-Use Industry (In Value %)

4.2.1 Manufacturing and Metal Fabrication

4.2.2 Chemical Processing

4.2.3 Food & Beverage

4.2.4 Healthcare

4.2.5 Energy Sector

4.3 By Production Technology (In Value %)

4.3.1 Cryogenic Air Separation

4.3.2 Non-Cryogenic Air Separation

4.3.3 Hydrogen Production

4.4 By Supply Mode (In Value %)

4.4.1 Packaged

4.4.2 Bulk

4.4.3 On-Site Generation

4.5 By Region (In Value %)

4.5.1 Western Europe

4.5.2 Eastern Europe

4.5.3 Northern Europe

4.5.4 Southern Europe

4.5.5 Central Europe

5.1 Detailed Profiles of Major Companies

5.1.1 Linde plc

5.1.2 Air Liquide

5.1.3 Messer Group GmbH

5.1.4 Praxair Technology, Inc.

5.1.5 Air Products and Chemicals, Inc.

5.1.6 Nippon Gases Europe

5.1.7 SOL Group

5.1.8 SIAD Group

5.1.9 Iwatani Corporation

5.1.10 BASF SE (Industrial Gases Division)

5.1.11 The Linde Group (Industrial Gases Division)

5.1.12 Taiyo Nippon Sanso Corporation

5.1.13 Air Water Inc.

5.1.14 Gulf Cryo

5.1.15 Atlas Copco AB

5.2 Cross-Comparison Parameters (Annual Revenue, Market Share %, No. of Production Facilities, Distribution Network Size, Innovations in Gas Technologies, Strategic Partnerships, Environmental Sustainability Initiatives, Market Penetration by Region)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment and Expansion Plans

5.7 Government and Private Sector Investments

5.8 R&D Spending Analysis

6.1 Emission Reduction Mandates

6.2 Compliance Standards for Production and Safety

6.3 Industry Certifications

6.4 Regional Environmental Policies and Initiatives

7.1 Future Market Size Projections

7.2 Key Drivers Shaping Future Market Growth

8.1 By Gas Type (In Value %)

8.2 By End-Use Industry (In Value %)

8.3 By Production Technology (In Value %)

8.4 By Supply Mode (In Value %)

8.5 By Region (In Value %)

9.1 Total Addressable Market (TAM) and Serviceable Market (SAM) Analysis

9.2 Key Customer Segment Insights

9.3 Innovation and Product Development Strategies

9.4 Unexplored Market Opportunities Analysis

The initial phase involves mapping out all critical stakeholders in the Europe Industrial Gases Market, supported by in-depth desk research. This stage also involves categorizing variables impacting market dynamics using a combination of proprietary and secondary databases to ensure a comprehensive market understanding.

Historical data related to market penetration, distribution trends, and end-use applications is compiled. This phase also examines industry growth patterns in alignment with economic indicators, ensuring accuracy in estimating historical and future growth rates.

Developed market hypotheses are validated through consultations with industry professionals via computer-assisted telephone interviews (CATI). Insights from these discussions refine our understanding of operational practices, financial stability, and market dynamics.

The final phase includes verification of segmented data through engagement with key industry players. This helps confirm data accuracy, particularly regarding market-specific parameters, ensuring a robust analysis of the Europe Industrial Gases Market.

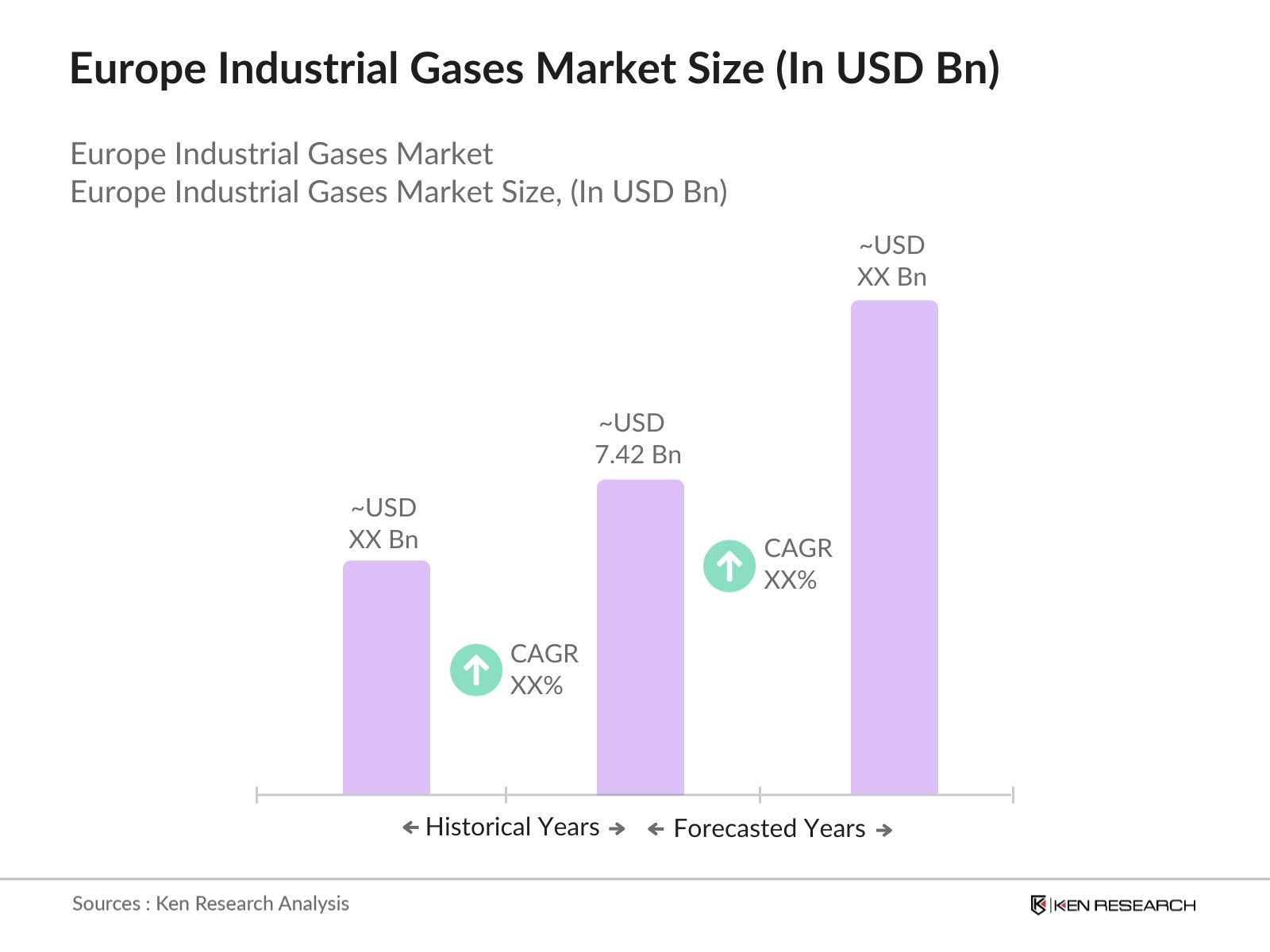

The Europe industrial gases market is valued at approximately USD 7.42 billion, driven by high demand across industries such as manufacturing and healthcare.

Challenges in Europe industrial gases market include stringent regulatory compliance, high transportation costs, and the need for significant storage infrastructure, which can impact the operational efficiency of market players.

Key companies in Europe industrial gases market include Linde plc, Air Liquide, Messer Group GmbH, Praxair Technology, and Air Products and Chemicals, Inc., with significant influence due to their established production and distribution networks.

The Europe industrial gases market growth is propelled by increased demand from manufacturing, food processing, and healthcare sectors, as well as the rising adoption of hydrogen as a clean energy source.

The nitrogen segment holds a dominant share due to its extensive use across industries, particularly in food preservation, electronics, and metal fabrication.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.