Europe Industrial Refrigeration Market Outlook to 2030

Region:Albania

Author(s):Shreya Garg

Product Code:KROD1060

Region:Albania

Author(s):Shreya Garg

Product Code:KROD1060

November 2024

97

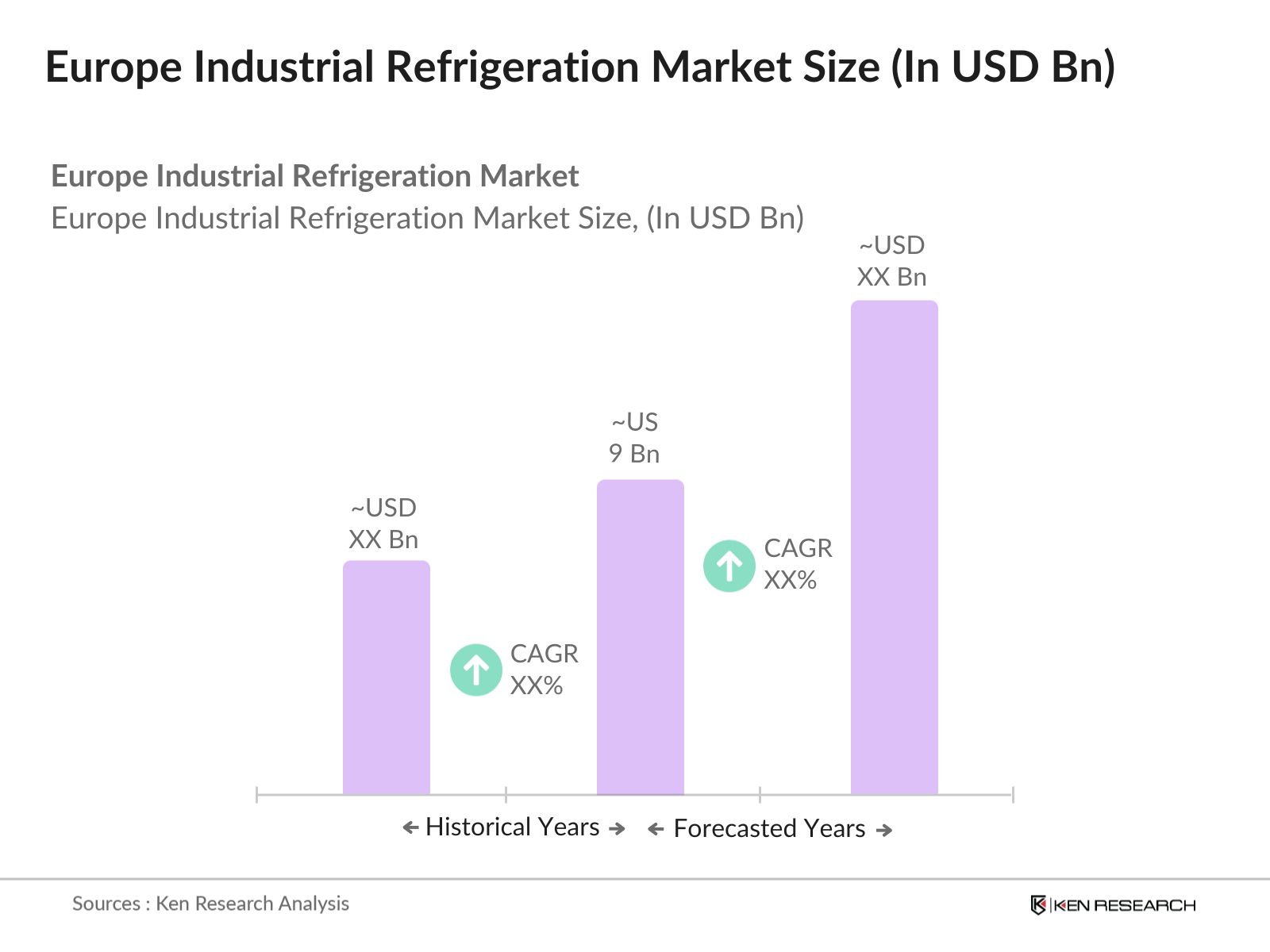

The Europe Industrial Refrigeration Market has witnessed growth over the past few years, driven by increasing demand for cold storage facilities and advancements in refrigeration technologies. The industrial refrigeration market in Europe was valued at USD 9 billion in 2023 it has expanded due to the rising demand for refrigerated storage solutions in the food and beverage industry, particularly in cold storage warehouses, meat processing plants, and dairy facilities.

Leading players in the Europe industrial refrigeration market include Johnson Controls International, GEA Group, Daikin Industries, Danfoss, and Emerson Electric. These companies dominate the market due to their extensive product portfolios, strong customer bases, and continuous investment in R&D.

In 2023, Johnson Controls International announced the acquisition of Hybrid Energy, which focuses on high-temperature industrial heat pumps utilizing ammonia-based technology. This acquisition aligns with Johnson Controls' commitment to sustainability and energy efficiency, particularly in the context of European decarbonization efforts and compliance with regulations such as the European Union's F-Gas regulations.

Germany is the leading country in the market in 2023. The country's dominance is due to its robust food and beverage industry, which is the largest in Europe, and its strong commitment to energy efficiency. Additionally, Germany's favorable regulatory environment and government incentives for green technologies have further bolstered its position in the market.

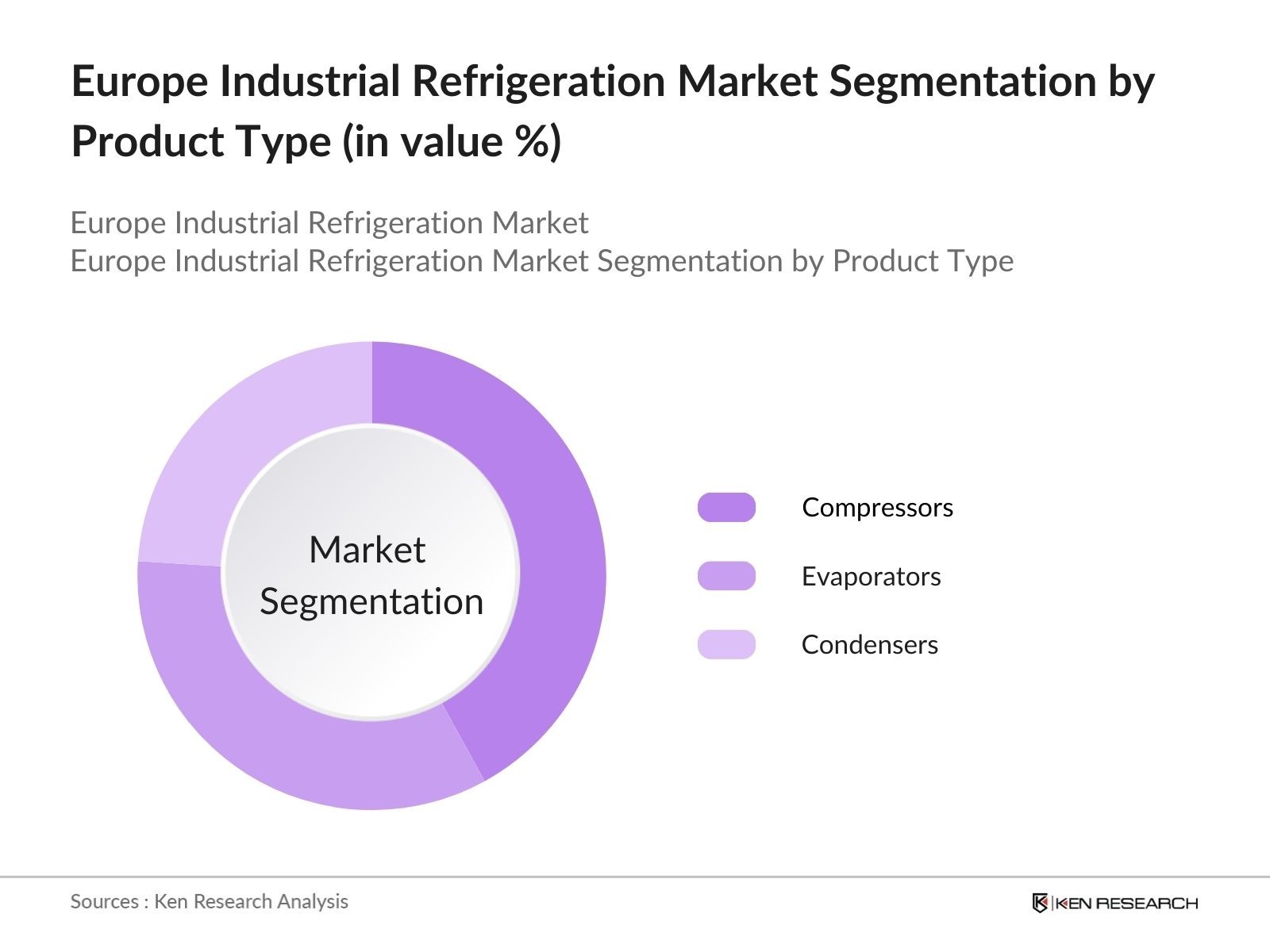

By Product Type: The market is segmented by product type into compressors, evaporators, and condensers. In 2023, compressors held a dominant market share. The dominance of compressors is attributed to their crucial role in the refrigeration cycle, providing the necessary pressure to circulate refrigerant throughout the system. The increasing adoption of energy-efficient compressors, which can reduce energy consumption by up to 30%, has further driven their market share.

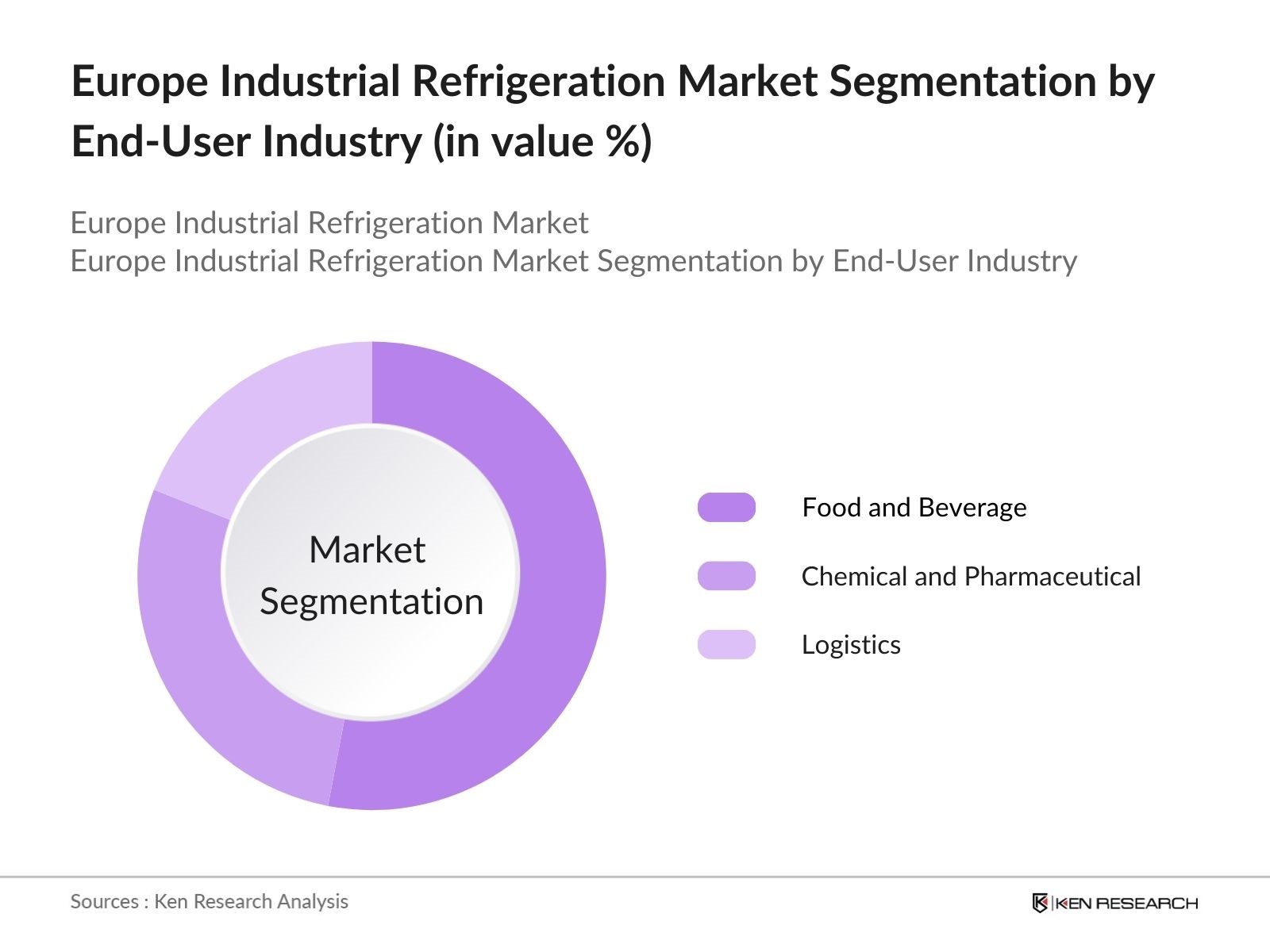

2. By End-User Industry: The market is segmented by end-user industry into food and beverage, chemical and pharmaceutical, and logistics. In 2023, the food and beverage industry held a dominant market share. This dominance is due to the industry's reliance on industrial refrigeration for the safe storage and processing of perishable goods. Also, there is growing demand for frozen and chilled foods, coupled with stringent food safety regulations.

By Region: The market is segmented by region into Germany, France, United Kingdom, Sweden, Italy and rest of Europe. Germany holds the dominant position in the Europe Industrial Refrigeration market share in 2023. The country's leadership in the market can be attributed to its robust industrial base, particularly in the food and beverage sectors, which are major consumers of industrial refrigeration systems.

|

Company Name |

Establishment Year |

Headquarters |

|

Johnson Controls International |

1885 |

Cork, Ireland |

|

GEA Group |

1881 |

Dsseldorf, Germany |

|

Daikin Industries |

1924 |

Osaka, Japan |

|

Danfoss |

1933 |

Nordborg, Denmark |

|

Emerson Electric |

1890 |

St. Louis, USA |

The Europe industrial refrigeration market is expected to continue growing at a steady pace by 2028, driven by increasing demand for energy-efficient refrigeration systems, the expansion of the food and beverage industry, and the adoption of smart refrigeration technologies that offer enhanced monitoring and control capabilities.

|

By Product Type |

Compressors Evaporators Condensers |

|

By End User |

Food And Beverage Chemical And Pharmaceutical Logistic |

|

By Region |

Germany France United Kingdom Sweden Italy Rest of Europe |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Expansion of Cold Chain Infrastructure

3.1.2. Stringent Environmental Regulations

3.1.3. Increasing Investments in Food Processing Industries

3.1.4. Technological Advancements in Refrigeration Systems

3.2. Challenges

3.2.1. High Initial Costs of Advanced Refrigeration Systems

3.2.2. Complex Regulatory Environment

3.2.3. Shortage of Skilled Labor

3.2.4. Supply Chain Disruptions

3.3. Opportunities

3.3.1. Rising Demand for Energy-Efficient Solutions

3.3.2. Expansion into Emerging Markets

3.3.3. Growth in Cold Chain Logistics

3.3.4. Government Support and Incentives

3.4. Trends

3.4.1. Adoption of Smart Refrigeration Systems

3.4.2. Shift Towards Natural Refrigerants

3.4.3. Integration with IoT and AI Technologies

3.4.4. Increasing Focus on Sustainability

3.5. Government Initiatives

3.5.1. EU Green Deal for Industry

3.5.2. Frances Refrigeration Modernization Program

3.5.3. Germanys Energy Efficiency Incentive Program

3.5.4. UKs Industrial Strategy for Refrigeration

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Competition Ecosystem

4.1. By Product Type (in Value %)

4.1.1. Compressors

4.1.2. Evaporators

4.1.3. Condensers

4.2. By End-User Industry (in Value %)

4.2.1. Food and Beverage

4.2.2. Chemical and Pharmaceutical

4.2.3. Logistics

4.3. By Region (in Value %)

4.3.1. North

4.3.2. South

4.3.3. East

4.3.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. Johnson Controls International

5.1.2. GEA Group

5.1.3. Daikin Industries

5.1.4. Danfoss

5.1.5. Emerson Electric

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9.1. By Product Type (in Value %)

9.2. By End-User Industry (in Value %)

9.3. By Region (in Value %)

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on in the Europe Industrial Refrigeration Market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for in the Europe Industrial Refrigeration Market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different Industrial Refrigeration companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple Industrial Refrigeration suppliers and distributors companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from Industrial Refrigeration manufacturers.

The Europe Industrial Refrigeration Market was valued at USD 9 billion, driven by the increasing demand for cold storage facilities, stringent environmental regulations, and advancements in refrigeration technologies.

Challenges in the Europe Industrial Refrigeration Market include high initial costs of advanced refrigeration systems, a complex regulatory environment, a shortage of skilled labor, and supply chain disruptions affecting the availability of key components.

Key players in the Europe Industrial Refrigeration Market include Johnson Controls International, GEA Group, Daikin Industries, Danfoss, and Emerson Electric. These companies dominate the market due to their extensive product portfolios, technological innovations, and strong market presence.

The Europe Industrial Refrigeration market is propelled by the expansion of cold chain infrastructure, stringent environmental regulations, increasing investments in food processing industries, and technological advancements in refrigeration systems that enhance efficiency and reduce energy consumption.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.