Europe LFP Batteries Market Outlook to 2030

Region:Albania

Author(s):Paribhasha Tiwari

Product Code:KROD4478

Region:Albania

Author(s):Paribhasha Tiwari

Product Code:KROD4478

November 2024

83

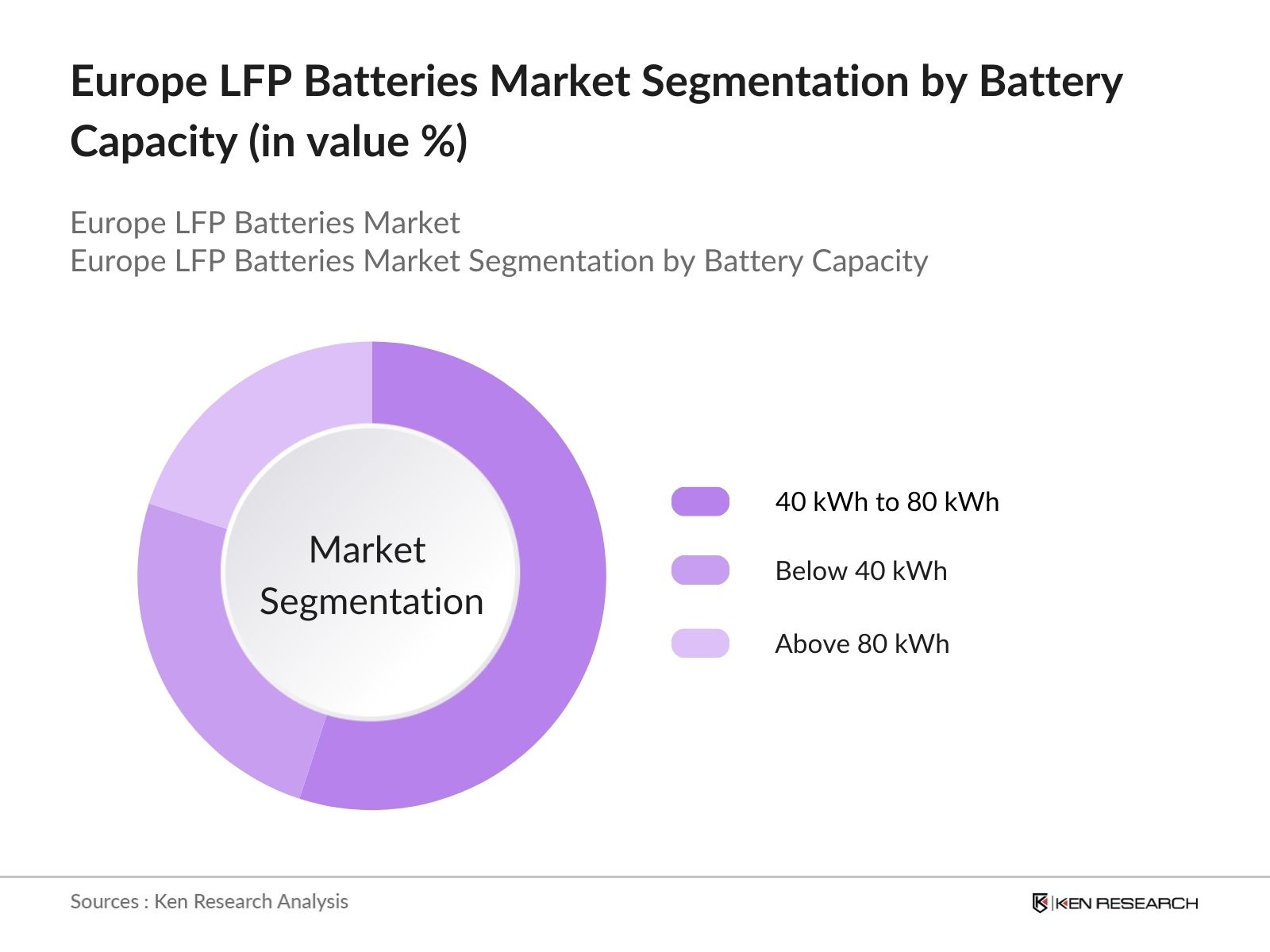

By Battery Capacity: The Europe LFP battery market is segmented by battery capacity into below 40 kWh, 40 kWh to 80 kWh, and above 80 kWh. The segment of 40 kWh to 80 kWh holds the dominant market share due to its applicability in electric vehicles (EVs) and commercial energy storage systems. The growing adoption of mid-range electric vehicles across Europe, coupled with the increasing demand for reliable energy storage for renewable power generation, is driving this segment. Mid-capacity batteries offer a balance between cost, weight, and energy output, making them suitable for a wide range of applications.

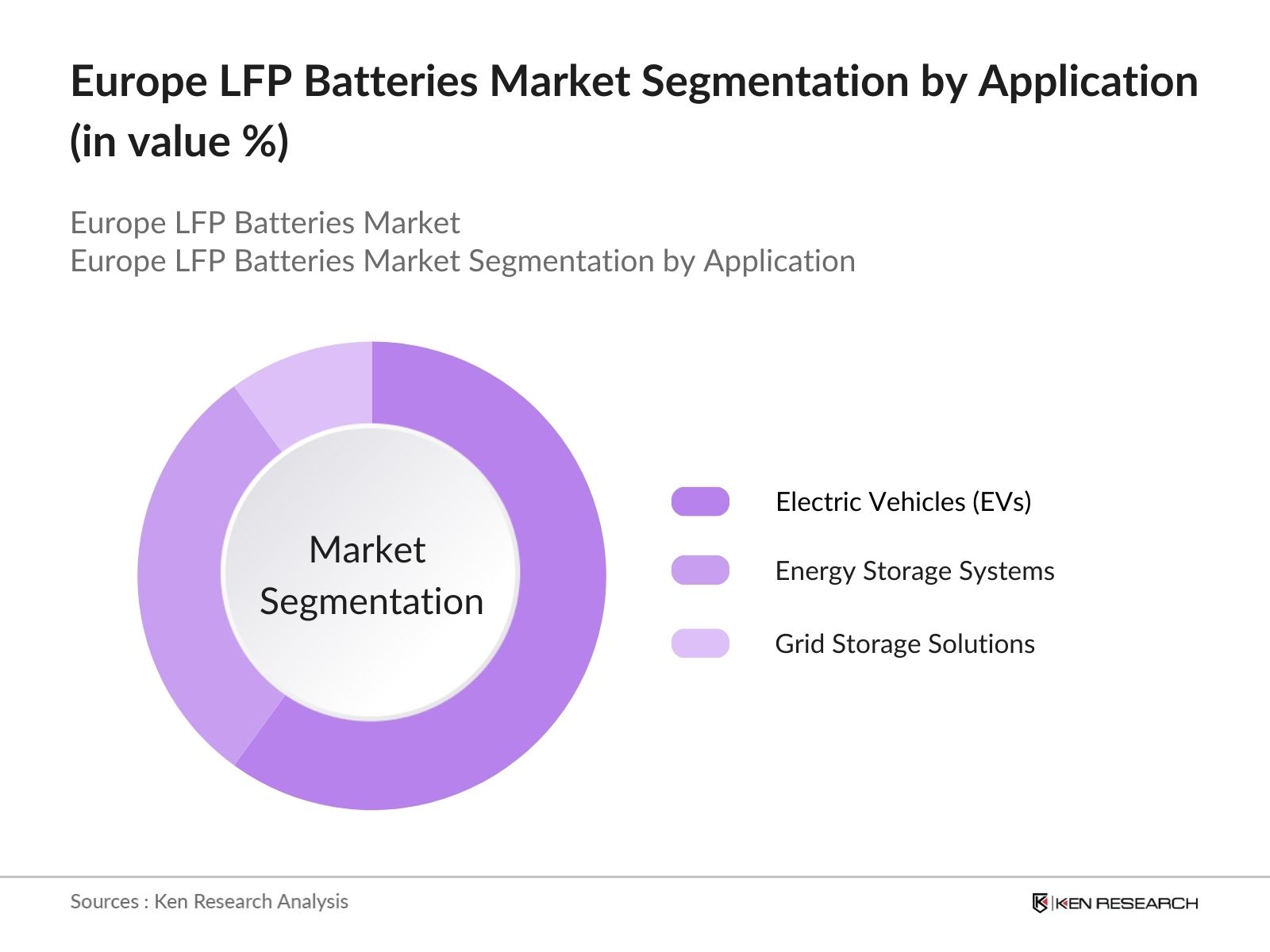

By Application: The market is also segmented by application into electric vehicles (EVs), energy storage systems, and grid storage solutions. Electric vehicles dominate the market due to rising consumer demand for eco-friendly transportation solutions and the European Union's strict emission regulations. The ability of LFP batteries to provide a safer, cost-effective alternative with a longer lifecycle makes them ideal for the EV industry, propelling this sub-segment to the forefront of market demand.

The Europe LFP battery market is consolidated, with major players focusing on technological innovations and capacity expansion. The entry of new players, such as ElevenEs with its LFP gigafactory in Serbia, is reshaping the market by increasing production capacity and enhancing competition. Key players include well-established battery manufacturers and emerging companies, positioning themselves to cater to the growing demand from the EV and energy storage sectors.

|

Company |

Established |

Headquarters |

No. of Employees |

Revenue (2023) |

Product Focus |

R&D Spending |

Patents |

Partnerships |

|

BYD Company Ltd. |

1995 |

China |

- | - | - | - | - | - |

|

ElevenEs |

2017 |

Serbia |

- | - | - | - | - | - |

|

Northvolt AB |

2016 |

Sweden |

- | - | - | - | - | - |

|

LG Energy Solution |

2020 |

South Korea |

- | - | - | - | - | - |

|

Contemporary Amperex Tech |

2011 |

China |

- | - | - | - | - | - |

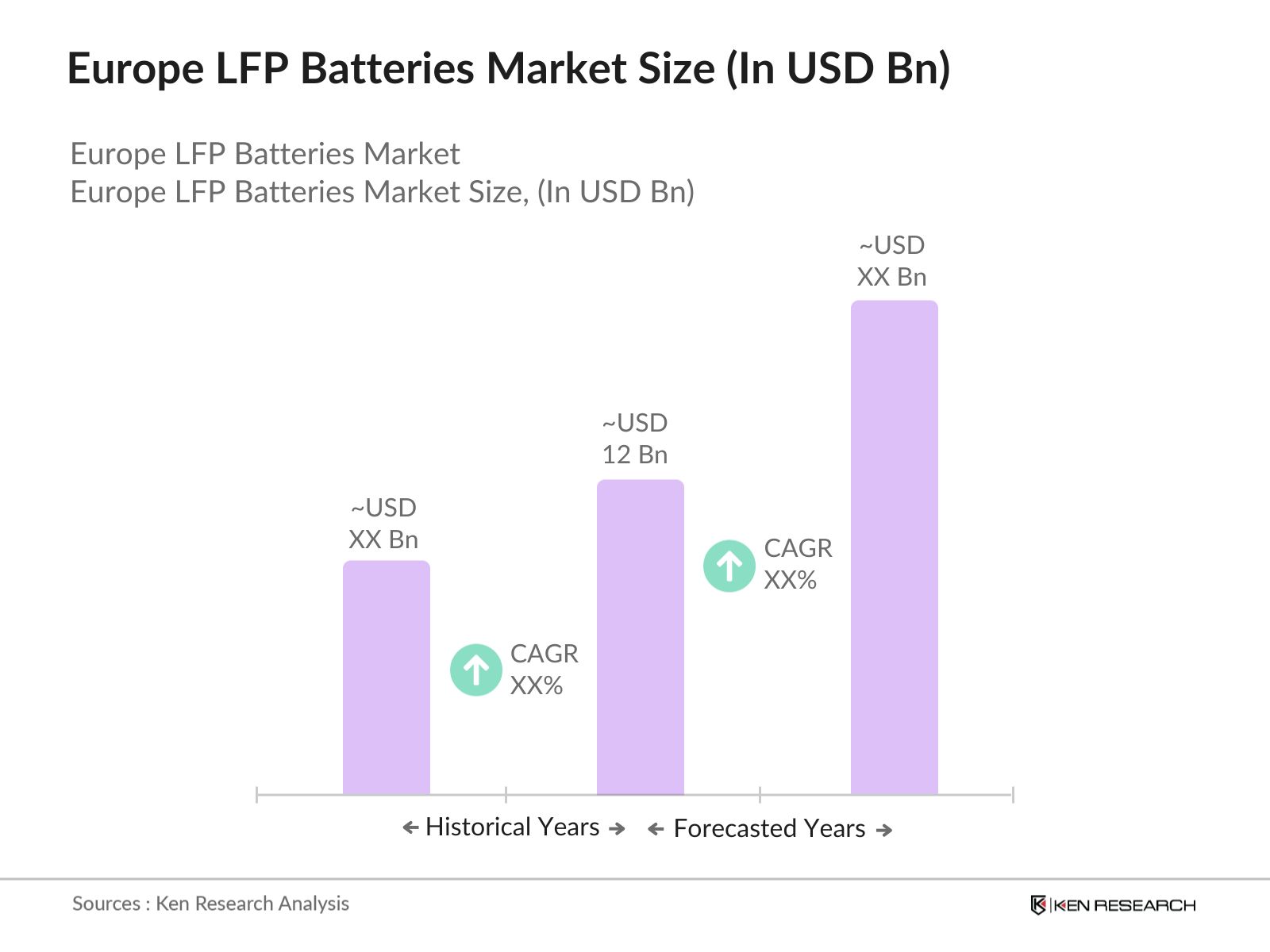

Over the next five years, the Europe LFP battery market is expected to witness substantial growth, driven by increasing investments in electric vehicle (EV) infrastructure and renewable energy projects. Governments across Europe are promoting the adoption of EVs, leading to a significant rise in demand for efficient and cost-effective batteries like LFP. Additionally, advancements in battery technology, including innovations in energy density and fast charging, are likely to further boost market expansion. As companies continue to scale production and improve battery performance, the LFP battery market is positioned to experience steady growth.

|

By Battery Capacity |

Below 40 kWh 40 kWh to 80 kWh Above 80 kWh |

|

By Application |

Electric Vehicles Energy Storage Systems Commercial Vehicles Grid Storage Solutions |

|

By Component |

Anode Cathode Electrolyte Separator |

|

By Vehicle Type |

Passenger Vehicles Commercial Trucks Electric Buses |

|

By Region |

West East North South |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Shift to Sustainable Energy (Electric Vehicles and Energy Storage Systems)

3.1.2 Lower Cost and Safety of LFP over Nickel and Cobalt Batteries

3.1.3 Increasing Government Incentives for Electric Vehicle Adoption

3.1.4 Local Manufacturing and Supply Chain Development

3.2 Market Challenges

3.2.1 Competition from Alternative Battery Technologies

3.2.2 Dependence on Raw Materials (Lithium, Phosphate)

3.2.3 Limited Fast-Charging Capabilities

3.2.4 Recycling and End-of-Life Management of Batteries

3.3 Opportunities

3.3.1 Expansion into Energy Storage for Renewable Power Systems

3.3.2 Innovations in Cell-to-Pack Technology

3.3.3 European Investments in Battery Gigafactories

3.3.4 Growing Demand in Commercial Vehicles and Buses

3.4 Trends

3.4.1 Adoption of LFP in Heavy-Duty Vehicles

3.4.2 Integration of Batteries with Renewable Energy Systems

3.4.3 Use of Prismatic Cell Designs for Higher Energy Density

3.4.4 Deployment of Battery-as-a-Service Models

3.5 Government Regulation

3.5.1 European Green Deal and Emission Targets

3.5.2 Battery Recycling Regulations and Compliance

3.5.3 Electric Vehicle Battery Safety Standards

3.5.4 Public-Private Partnerships in Battery Infrastructure

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

4.1 By Battery Capacity (in Value %)

4.1.1 Below 40 kWh

4.1.2 40 kWh to 80 kWh

4.1.3 Above 80 kWh

4.2 By Application (in Value %)

4.2.1 Electric Vehicles (EVs)

4.2.2 Energy Storage Systems

4.2.3 Commercial Vehicles

4.2.4 Grid Storage Solutions

4.3 By Component (in Value %)

4.3.1 Anode

4.3.2 Cathode

4.3.3 Electrolyte

4.3.4 Separator

4.4 By Vehicle Type (in Value %)

4.4.1 Passenger Vehicles

4.4.2 Commercial Trucks

4.4.3 Electric Buses

4.5 By Region (in Value %)

4.5.1 Western Europe

4.5.2 Eastern Europe

4.5.3 Northern Europe

4.5.4 Southern Europe

5.1 Detailed Profiles of Major Companies

5.1.1 BYD Company Ltd.

5.1.2 Contemporary Amperex Technology Co. Ltd. (CATL)

5.1.3 SK Innovation Co. Ltd.

5.1.4 Morrow Batteries

5.1.5 Vehicle Energy Japan Inc.

5.1.6 ElevenEs

5.1.7 Stellantis N.V.

5.1.8 Northvolt AB

5.1.9 LG Energy Solution

5.1.10 Renault Group

5.1.11 Saft Group SA

5.1.12 Siemens AG

5.1.13 Samsung SDI Co., Ltd.

5.1.14 Hitachi Chemical Co., Ltd.

5.1.15 Svolt Energy Technology Co. Ltd.

5.2 Cross Comparison Parameters (Headquarters, Employees, Revenue, Product Portfolio, Market Penetration, R&D Spending, Partnerships, Patents)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Emission Standards for EV Batteries

6.2 Recycling and Disposal Regulations

6.3 Certification Processes for Safety and Efficiency

6.4 Local Content Requirements

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Battery Capacity (in Value %)

8.2 By Application (in Value %)

8.3 By Component (in Value %)

8.4 By Vehicle Type (in Value %)

8.5 By Region (in Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsThe initial phase involves constructing a comprehensive ecosystem map of the Europe LFP Batteries Market. This includes extensive desk research and secondary data collection from proprietary databases to identify critical variables influencing the market.

During this phase, we analyze historical data on market penetration, manufacturing capacities, and the supply-demand ratio. This is complemented by data on technological advancements and regulatory frameworks that shape the market landscape.

Market hypotheses are validated through interviews with industry experts and stakeholders from leading companies in the battery sector. These consultations provide operational insights and help refine market estimates.

The final stage involves synthesizing all data, including inputs from primary and secondary sources. This step ensures the accuracy of market projections and insights, culminating in a well-rounded analysis of the Europe LFP Batteries Market.

The Europe LFP Batteries Market is valued at USD 12 billion, driven by the rise in demand for electric vehicles and energy storage systems.

Challenges in the Europe LFP Batteries Market include reliance on raw material imports, competition from alternative battery chemistries, and evolving regulatory standards.

Key players in the Europe LFP Batteries Market include BYD Company Ltd., CATL, LG Energy Solution, Northvolt AB, and ElevenEs. These companies lead due to their technological advancements and production capacity.

The growth of the Europe LFP Batteries Market is driven by increasing government incentives for EV adoption, advances in battery technology, and the demand for sustainable energy solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.