Europe Naval Vessels Market Outlook to 2030

Region:Belgium

Author(s):Shambhavi

Product Code:KROD5056

Region:Belgium

Author(s):Shambhavi

Product Code:KROD5056

December 2024

89

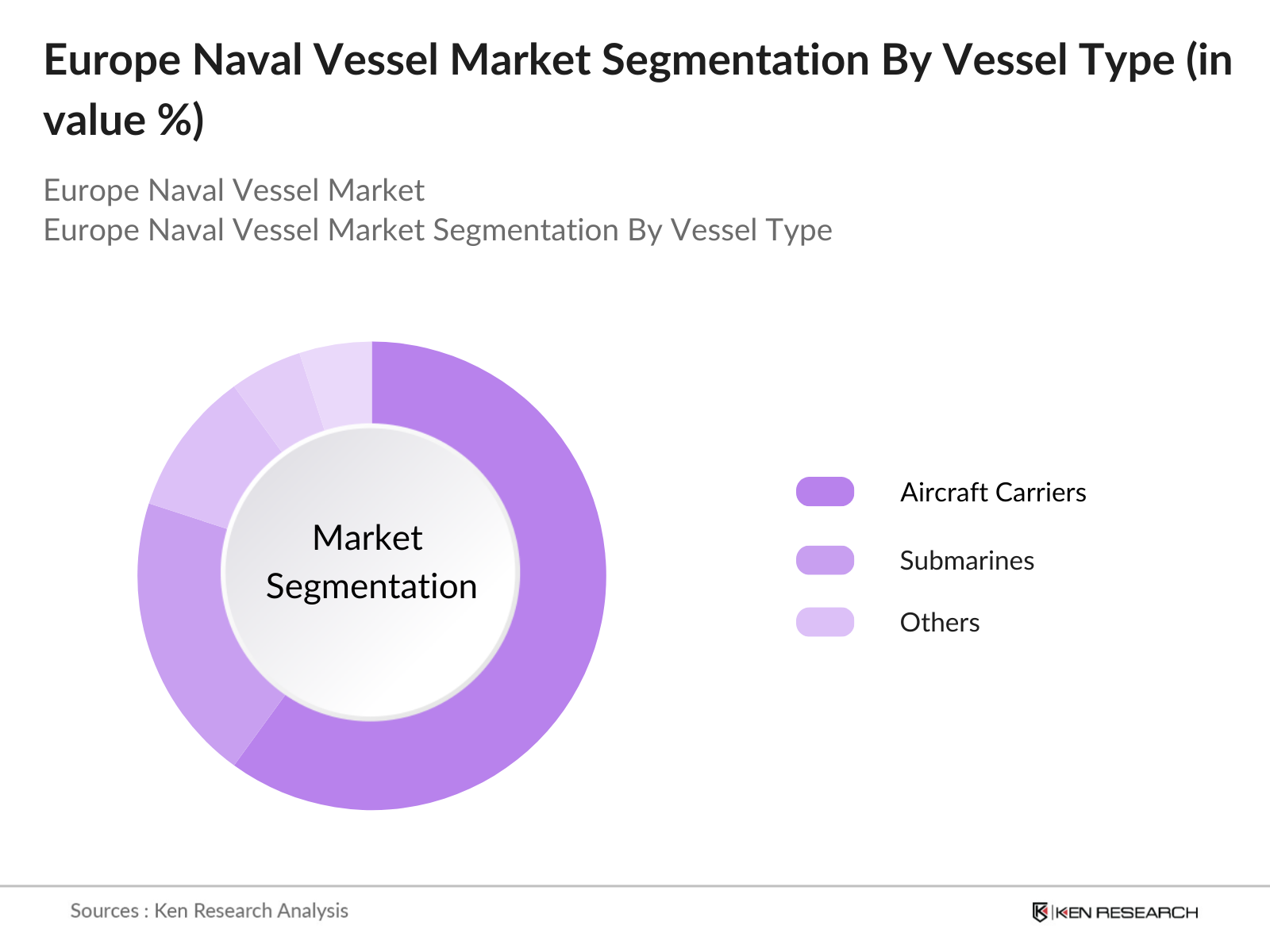

By Vessel Type: The Europe naval vessels market is segmented by vessel type into aircraft carriers, submarines and others. Recently, frigates and destroyers have a dominant market share under this segmentation, as they offer versatility in both defensive and offensive operations. These vessels are equipped with advanced missile systems, anti-submarine warfare capabilities, and are increasingly integrated with cutting-edge stealth technology, making them crucial to modern naval warfare strategies in Europe.

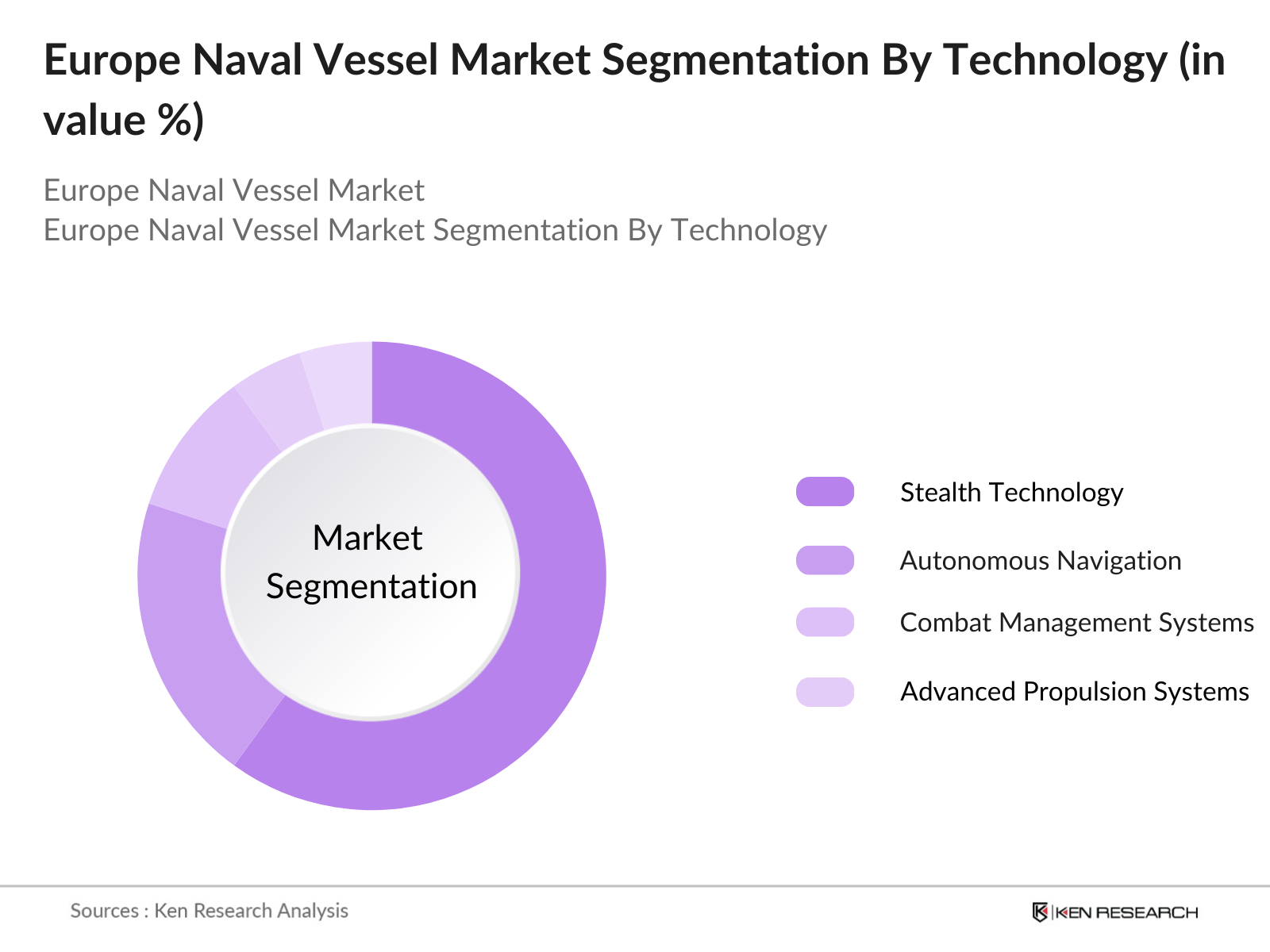

By Technology: The market is segmented by technology into stealth technology, autonomous navigation, combat management systems, and advanced propulsion systems. Stealth technology has seen significant dominance due to the increasing demand for low-detectability naval vessels. Many European countries are heavily investing in stealth capabilities to enhance their defense and deterrence measures, especially against emerging threats. The adoption of radar-absorbing materials, as well as innovative hull designs, has made stealth technology critical in the procurement of new naval vessels.

The European naval vessels market is dominated by a combination of established domestic players and international defense contractors. The consolidation of major players in this market has intensified due to increased government contracts and technological innovations. European defense manufacturers, with their long-standing naval engineering expertise, continue to lead the market, while non-European firms have sought strategic partnerships to expand their presence.

The European naval vessels market is expected to continue its upward trajectory over the next five years. This growth is primarily driven by the continuous increase in defense budgets, strategic modernization of naval fleets, and advancements in naval warfare technologies. Additionally, geopolitical tensions in Europe, particularly surrounding maritime boundaries, are expected to further increase the demand for advanced naval vessels. European countries are likely to enhance collaboration through the European Defence Fund, aiming to boost cross-border innovation in defense technologies, which will also contribute to market expansion.

|

By Vessel Type |

Aircraft Carriers Submarines Frigates and Destroyers Corvettes Amphibious Ships |

|

By Technology |

Stealth Technology Autonomous Navigation Combat Management Systems Advanced Propulsion Systems |

|

By Application |

Naval Warfare Surveillance and Reconnaissance Mine Countermeasures Coastal Defense |

|

By Material |

Steel Aluminum Composites |

|

By Region |

Western Europe Eastern Europe Northern Europe Southern Europe |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Increased Defense Spending, Geopolitical Tensions, Technological Advancements)

3.1.1. Regional Security Initiatives

3.1.2. Modernization of Naval Fleets

3.1.3. Government and NATO Collaboration

3.2. Market Challenges (Budget Constraints, Lengthy Procurement Processes, Environmental Compliance)

3.2.1. High Costs of Advanced Technology

3.2.2. Delays in Shipbuilding and Delivery

3.2.3. Stringent Environmental Regulations

3.3. Opportunities (Export Potential, Naval Vessel Customization, Multi-Mission Capabilities)

3.3.1. Cross-Border Partnerships

3.3.2. Expansion of Shipyards in Emerging Markets

3.3.3. Growing Demand for Coastal Security Vessels

3.4. Trends (Autonomous Vessels, Stealth Technology, Hybrid Propulsion Systems)

3.4.1. Integration of Unmanned Surface Vehicles (USVs)

3.4.2. Cybersecurity Enhancements

3.4.3. Development of Modular Naval Platforms

3.5. Government Regulation (Defense Procurement Policies, Environmental Certifications, Export Regulations)

3.5.1. EU Naval Standards and Compliance

3.5.2. Emission Control Areas (ECA) Rules

3.5.3. Defense Offset Policies

3.6. SWOT Analysis

3.7. Naval Stake Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Vessel Type (In Value %)

4.1.1. Aircraft Carriers

4.1.2. Submarines

4.1.3. Frigates and Destroyers

4.1.4. Corvettes

4.1.5. Amphibious Ships

4.2. By Technology (In Value %)

4.2.1. Stealth Technology

4.2.2. Autonomous Navigation

4.2.3. Combat Management Systems

4.2.4. Advanced Propulsion Systems

4.3. By Application (In Value %)

4.3.1. Naval Warfare

4.3.2. Surveillance and Reconnaissance

4.3.3. Mine Countermeasures

4.3.4. Coastal Defense

4.4. By Material (In Value %)

4.4.1. Steel

4.4.2. Aluminum

4.4.3. Composites

4.5. By Region (In Value %)

4.5.1. Western Europe

4.5.2. Eastern Europe

4.5.3. Northern Europe

4.5.4. Southern Europe

5.1 Detailed Profiles of Major Companies

5.1.1. BAE Systems

5.1.2. Fincantieri

5.1.3. Navantia

5.1.4. Naval Group

5.1.5. Damen Shipyards Group

5.1.6. Thales Group

5.1.7. Lockheed Martin

5.1.8. Saab AB

5.1.9. Leonardo S.p.A

5.1.10. Rolls-Royce Holdings

5.1.11. Rheinmetall AG

5.1.12. ThyssenKrupp Marine Systems

5.1.13. Lrssen Werft

5.1.14. Austal

5.1.15. General Dynamics

5.2 Cross Comparison Parameters (Shipyard Capacity, Revenue, Fleet Modernization Contracts, R&D Investments, Export Capabilities, Workforce Size, Production Timeframe, Technological Expertise)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Environmental Standards (Emission Norms, Sustainable Shipbuilding)

6.2 Defense Procurement Rules (National Security, Offset Requirements)

6.3 Certification Processes (Safety, NATO Standards)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Vessel Type (In Value %)

8.2 By Technology (In Value %)

8.3 By Application (In Value %)

8.4 By Material (In Value %)

8.5 By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first phase involved constructing an ecosystem map encompassing all key stakeholders within the Europe Naval Vessels Market. Extensive desk research was conducted to identify the critical variables influencing the market, such as technological innovations, defense policies, and procurement strategies.

In this phase, historical data related to naval vessel procurement and shipyard capabilities was compiled and analyzed. The analysis focused on the penetration of shipbuilders, technological advancements, and their corresponding revenue streams, ensuring accurate estimations of market trends.

Market hypotheses were validated through consultations with industry experts, including naval shipbuilders, defense contractors, and government officials. These consultations were crucial in verifying market trends, technological developments, and procurement strategies.

The final phase involved direct engagement with shipbuilders and defense ministries to obtain detailed insights on product segments, technological adoption, and procurement timelines. The results were synthesized to produce a comprehensive and validated analysis of the Europe Naval Vessels Market.

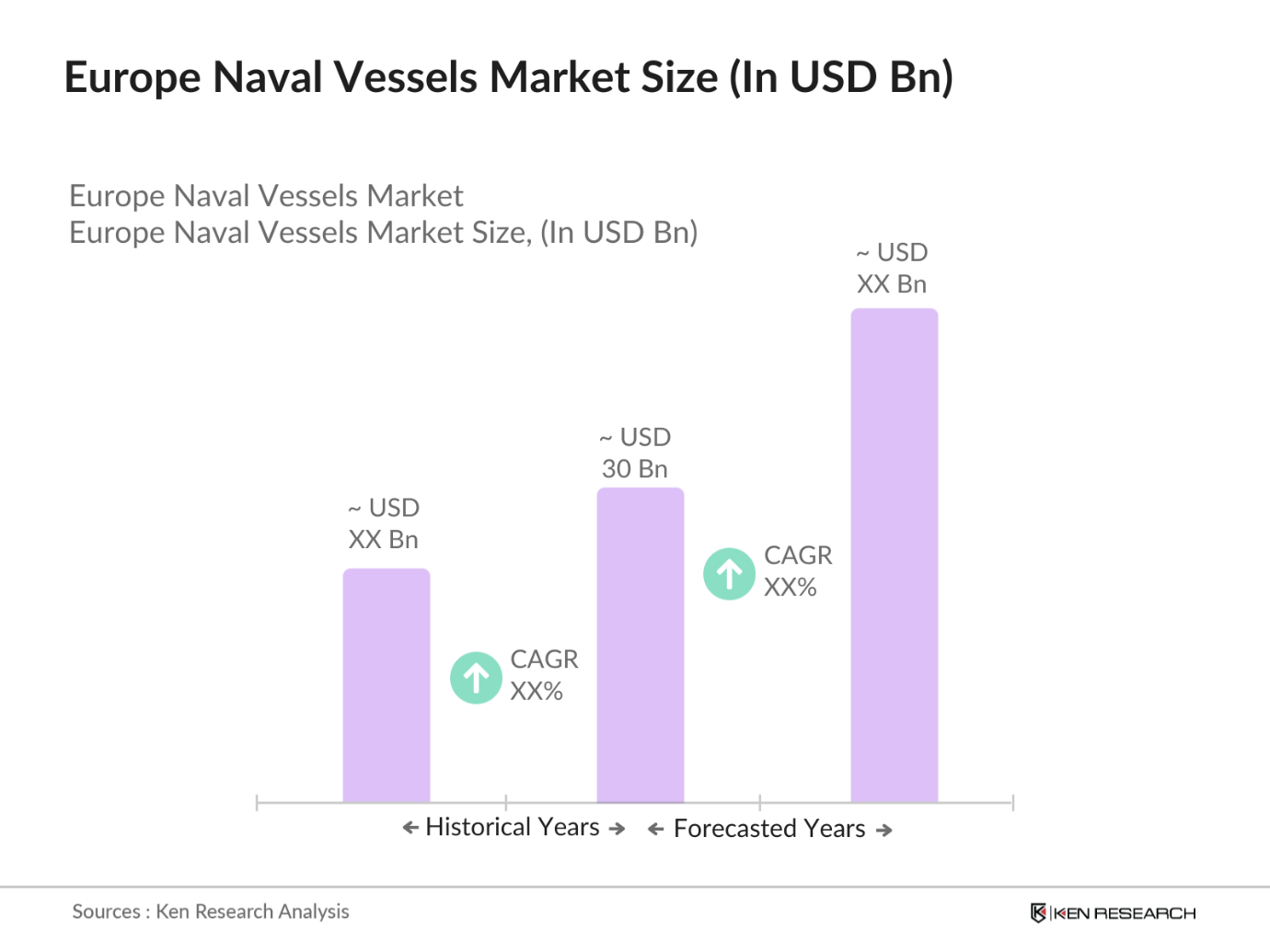

The Europe naval vessels market was valued at USD 30 billion in 2023, driven by increasing defense budgets, fleet modernization, and maritime security concerns.

High costs of advanced naval technologies, delays in shipbuilding due to supply chain disruptions and labor shortages, and budget constraints affecting modernization efforts are the major challanges in the Europe naval vessels market.

BAE Systems, Fincantieri, Navantia, Naval Group, and Damen Shipyards Group are some of the major players of the Europe naval vessels market.

The major growth driver of Europe naval vessels market are regional security initiatives, modernization of naval fleets, NATO and government collaborations, and the increasing adoption of stealth and autonomous naval technologies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.