Europe Pharmaceutical Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD3701

Region:Global

Author(s):Sanjna

Product Code:KROD3701

November 2024

81

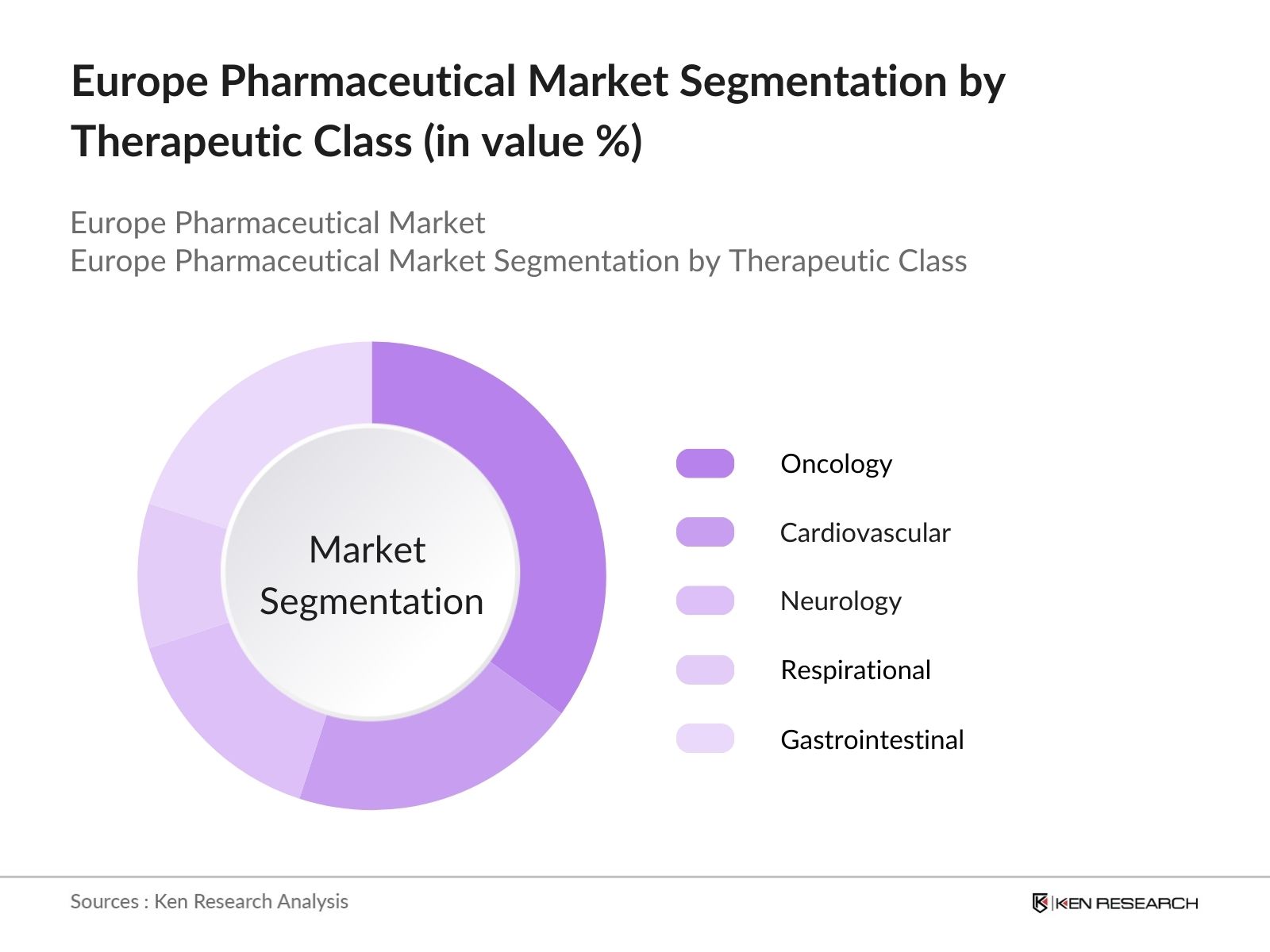

By Therapeutic Class: The Europe Pharmaceutical market is segmented by therapeutic class into oncology, cardiovascular, neurology, respiratory, and gastrointestinal drugs. Oncology drugs have a dominant market share due to the increasing prevalence of cancer, extensive research and innovation in cancer therapies, and the introduction of biologics and biosimilars in oncology treatments. Additionally, substantial funding and public awareness campaigns about cancer screening contribute to the dominance of this segment.

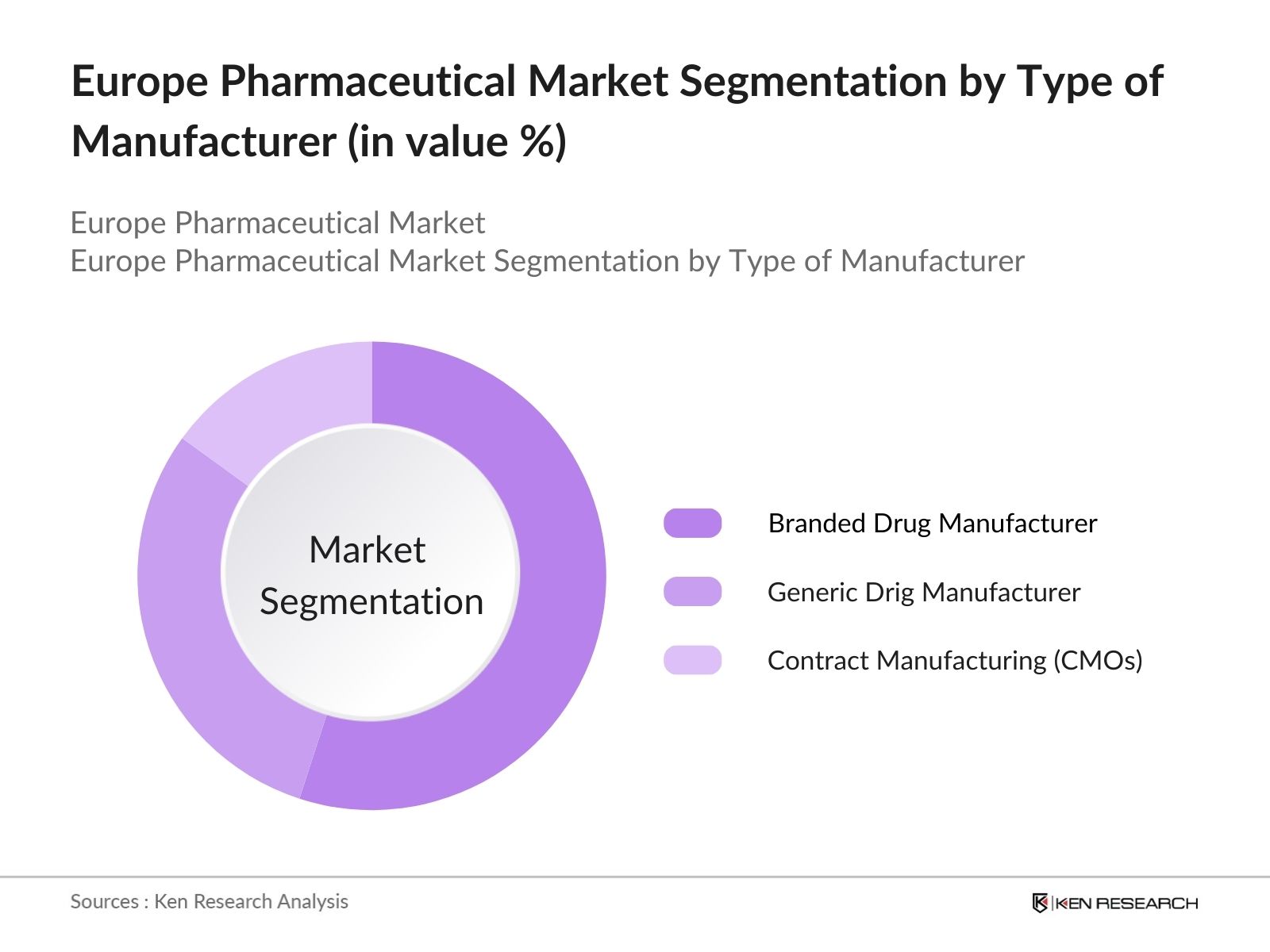

By Type of Manufacturer: The Europe Pharmaceutical market is segmented by type of manufacturer into branded drug manufacturers, generic drug manufacturers, and contract manufacturing organizations (CMOs). Branded drug manufacturers hold the largest market share due to their strong brand presence, high R&D investment, and exclusive patent rights that protect their products from generic competition. Major companies like Roche and Novartis are significant contributors to this segment's leadership.

The Europe Pharmaceutical market is dominated by several leading companies, including both European and global players. These companies have established themselves through significant R&D investments, innovative product pipelines, and extensive distribution networks across Europe. The market remains highly competitive, with consolidation occurring through mergers and acquisitions. The companies listed below play a critical role in shaping the competitive landscape.

|

Company Name |

Establishment Year |

Headquarters |

Revenue |

R&D Investment |

Market Focus |

Therapeutic Specialization |

Number of Patents |

Global Presence |

|

Roche |

1896 |

Basel, Switzerland |

- |

- |

- |

- |

- |

- |

|

Novartis |

1996 |

Basel, Switzerland |

- |

- |

- |

- |

- |

- |

|

Sanofi |

1973 |

Paris, France |

- |

- |

- |

- |

- |

- |

|

GlaxoSmithKline (GSK) |

2000 |

Brentford, UK |

- |

- |

- |

- |

- |

- |

|

Pfizer |

1849 |

New York, USA |

- |

- |

- |

- |

- |

- |

Over the next five years, the Europe Pharmaceutical Market is expected to show significant growth driven by continuous innovation in drug development, a growing demand for biopharmaceuticals, and the expansion of personalized medicine. The aging population across Europe, coupled with increasing healthcare investments, will support the markets upward trajectory. Biopharmaceutical advancements and the integration of digital health tools into pharmaceutical solutions are likely to drive industry transformation.

|

Segment |

Sub-Segment |

|

Therapeutic Class |

Oncology |

|

Cardiovascular |

|

|

Neurology |

|

|

Respiratory |

|

|

Gastrointestinal |

|

|

Type of Manufacturer |

Branded Drug Manufacturers |

|

Generic Drug Manufacturers |

|

|

Contract Manufacturing Organizations |

|

|

Drug Type |

Biologics |

|

Small Molecule Drugs |

|

|

Distribution Channel |

Hospital Pharmacies |

|

Retail Pharmacies |

|

|

Online Pharmacies |

|

|

Country |

France |

|

Germany |

|

|

United Kingdom |

|

|

Sweden |

|

|

Italy |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (CAGR, Market Drivers, Regional Contributions)

1.4. Market Segmentation Overview (Therapeutic Classes, Regions, Distribution Channels, Types of Manufacturers, Drug Development Stages)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Aging Population and Rising Chronic Diseases

3.1.2. Growth of Biologics and Biosimilars

3.1.3. Advancements in Personalized Medicine

3.1.4. Increasing Healthcare Expenditure in Europe

3.2. Market Challenges

3.2.1. Regulatory Complexity and Stringent Approval Processes

3.2.2. High Research & Development Costs

3.2.3. Patent Expiry and Generic Competition

3.2.4. Market Fragmentation Across European Countries

3.3. Opportunities

3.3.1. Expansion of Biosimilars Market

3.3.2. Growing Adoption of AI in Drug Discovery

3.3.3. Digital Health and Telemedicine Integration

3.3.4. Mergers and Acquisitions for Market Consolidation

3.4. Trends

3.4.1. Focus on Orphan Drugs for Rare Diseases

3.4.2. Development of Biopharmaceuticals

3.4.3. Integration of Digital Therapeutics in Pharmaceuticals

3.4.4. Shift Toward Value-Based Healthcare Systems

3.5. Government Regulation

3.5.1. EMA Approval Processes

3.5.2. Good Manufacturing Practices (GMP) Standards

3.5.3. European Union Clinical Trial Regulations

3.5.4. Pharmaceutical Pricing Controls and Reimbursement Policies

3.6. SWOT Analysis

3.7. Stake Ecosystem (Manufacturers, CROs, Regulators)

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4.1. By Therapeutic Class (In Value %)

4.1.1. Oncology

4.1.2. Cardiovascular

4.1.3. Neurology

4.1.4. Respiratory

4.1.5. Gastrointestinal

4.2. By Type of Manufacturer (In Value %)

4.2.1. Branded Drug Manufacturers

4.2.2. Generic Drug Manufacturers

4.2.3. Contract Manufacturing Organizations (CMOs)

4.3. By Drug Type (In Value %)

4.3.1. Biologics

4.3.2. Small Molecule Drugs

4.4. By Distribution Channel (In Value %)

4.4.1. Hospital Pharmacies

4.4.2. Retail Pharmacies

4.4.3. Online Pharmacies

4.5. By Country (In Value %)

4.5.1. France

4.5.2. Germany

4.5.3. United Kingdom

4.5.4. Sweden

4.5.5. Italy

5.1. Detailed Profiles of Major Companies

5.1.1. Roche

5.1.2. Novartis

5.1.3. Sanofi

5.1.4. GlaxoSmithKline (GSK)

5.1.5. AstraZeneca

5.1.6. Pfizer

5.1.7. Bayer AG

5.1.8. Boehringer Ingelheim

5.1.9. Merck Group

5.1.10. Novo Nordisk

5.1.11. Teva Pharmaceuticals

5.1.12. UCB

5.1.13. Ipsen

5.1.14. Servier

5.1.15. STADA Arzneimittel AG

5.2. Cross Comparison Parameters (Revenue, Number of Patents, Therapeutic Specialization, Geographical Presence, R&D Investment, Market Share, Clinical Trials Portfolio, Pipeline Drugs)

5.3. Market Share Analysis (Top 10 Companies by Revenue and Market Share)

5.4. Strategic Initiatives (Collaborations, Licensing, Joint Ventures)

5.5. Mergers and Acquisitions (Recent M&A Activity)

5.6. Investment Analysis (Key Investments, Areas of Focus)

5.7. Venture Capital and Private Equity Funding

5.8. Partnerships with Academic Institutions and Research Organizations

6.1. European Medicines Agency (EMA) Approval Process

6.2. Good Manufacturing Practices (GMP) Compliance

6.3. Clinical Trial Regulations and Compliance

6.4. Patent Laws and Data Exclusivity

6.5. Pharmaceutical Pricing and Reimbursement Policies

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (R&D Innovations, Biosimilars, Digital Therapeutics)

8.1. By Therapeutic Class (In Value %)

8.2. By Type of Manufacturer (In Value %)

8.3. By Drug Type (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Country (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segmentation and Profiling

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Europe Pharmaceutical Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

In this phase, we will compile and analyze historical data pertaining to the Europe Pharmaceutical Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

The final phase involves direct engagement with multiple pharmaceutical manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Europe Pharmaceutical Market.

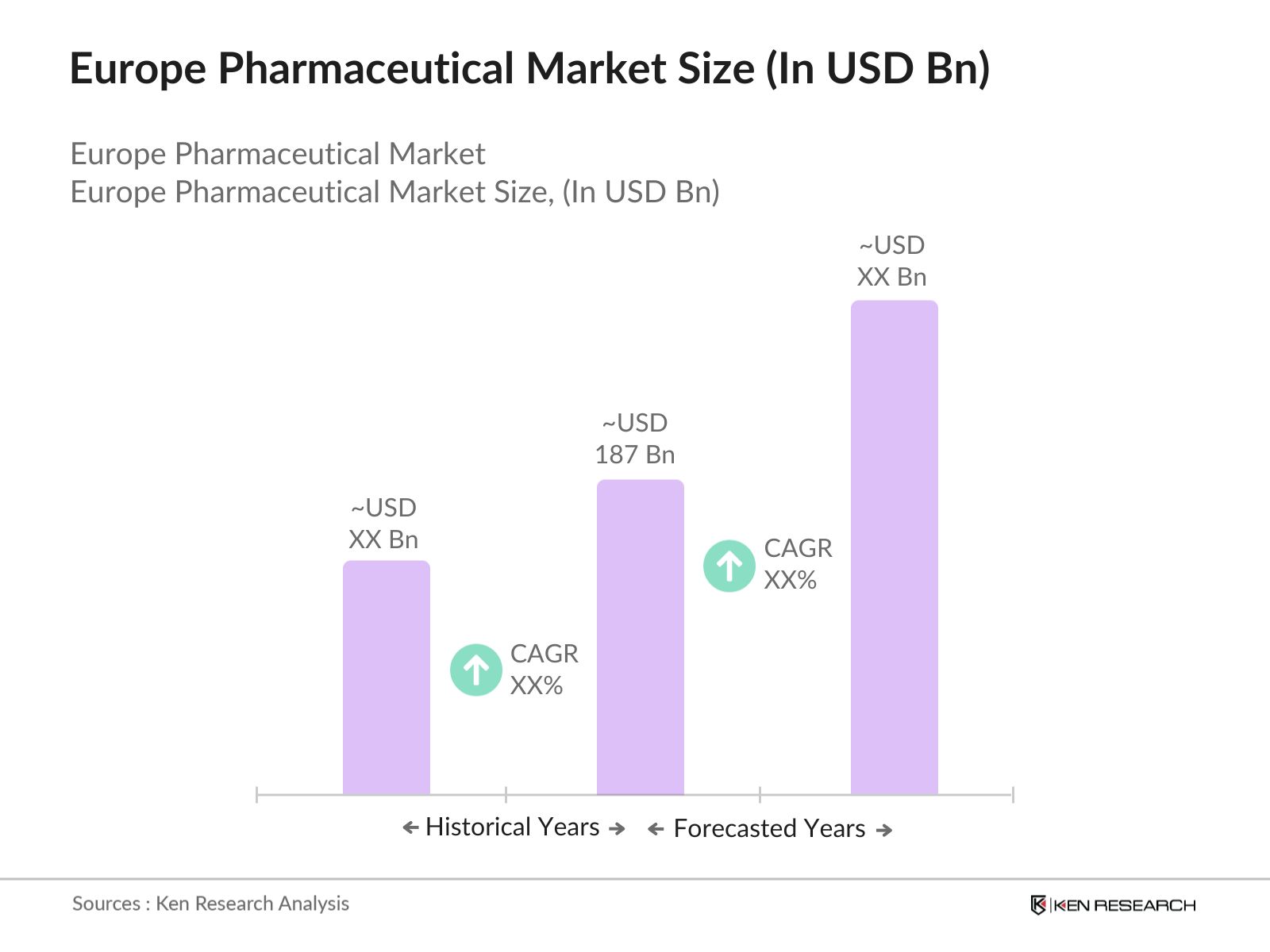

The Europe Pharmaceutical Market is valued at USD 188 billion, driven by high R&D investment, an aging population, and the growing demand for biopharmaceuticals and personalized medicines.

Challenges include regulatory complexity, high R&D costs, and increasing competition from generic drugs. Furthermore, patent expiry and the slow regulatory approval process create additional hurdles for market players.

Key players in the market include Roche, Novartis, Sanofi, GlaxoSmithKline (GSK), and Pfizer. These companies dominate due to their strong R&D investments, extensive product portfolios, and global presence.

The market is driven by the growing elderly population, the increasing prevalence of chronic diseases, advancements in biopharmaceuticals, and personalized medicine. Strong healthcare systems and R&D support also contribute to market growth.

Key trends include the rise of biopharmaceuticals, the increasing adoption of digital health tools, the development of orphan drugs for rare diseases, and the integration of AI in drug discovery and development.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.