Europe Polyisobutylene Market Outlook to 2030

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD2705

October 2024

83

About the Report

Europe Polyisobutylene Market Overview

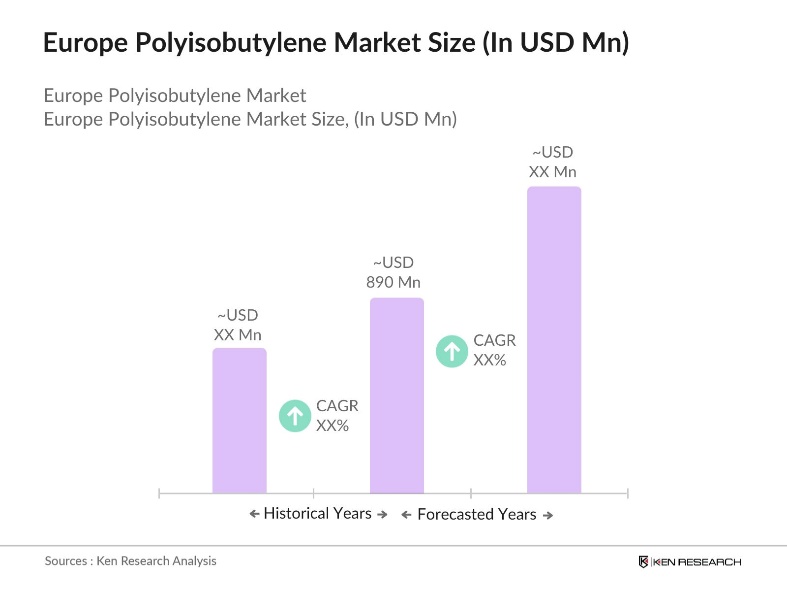

- The Europe Polyisobutylene market is valued at USD 890 Million, driven by the increasing demand across various industries, including automotive, adhesives & sealants, and lubricants. This growth is supported by the materials diverse applications, such as in automotive components, industrial lubricants, and packaging, where its superior thermal and oxidative stability plays a critical role. The markets growth is primarily driven by technological advancements in the production process, which enhance product performance and sustainability.

- The leading countries dominating the Europe Polyisobutylene market include Germany, France, and the UK. Germany, with its strong automotive and industrial manufacturing sectors, leads the market due to high demand for polyisobutylene in automotive parts and lubricants. France and the UK also play significant roles, with a high consumption of adhesives and sealants, especially in the construction and packaging industries. These nations dominate due to well-established manufacturing infrastructure and strong end-user demand.

- BASF launched OPPANOL C, a new form of PIB, in February 2021, designed for easier processing and faster production. Additionally, there has been significant innovation in high molecular weight PIB due to its increased elasticity and resilience, making it suitable for applications like lubricants, adhesives, and stretch films. These innovations are supported by Europes ongoing push towards greener industrial processes and materials.

Europe Polyisobutylene market Segmentation

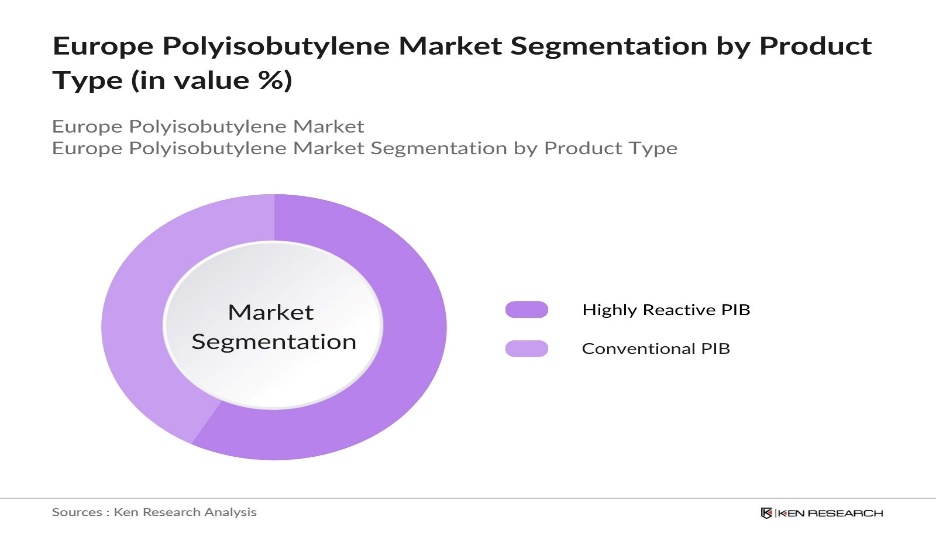

By Product Type: The Europe Polyisobutylene market is segmented by product type into Conventional PIB and Highly Reactive PIB (HR-PIB). Highly Reactive PIB dominates the market due to its extensive use in the automotive sector, specifically in fuel additives, and the growing demand for environmentally friendly products in the transportation industry. The increased use of HR-PIB in high-performance applications, including lubricants and adhesives, has also fueled its dominance in the market.

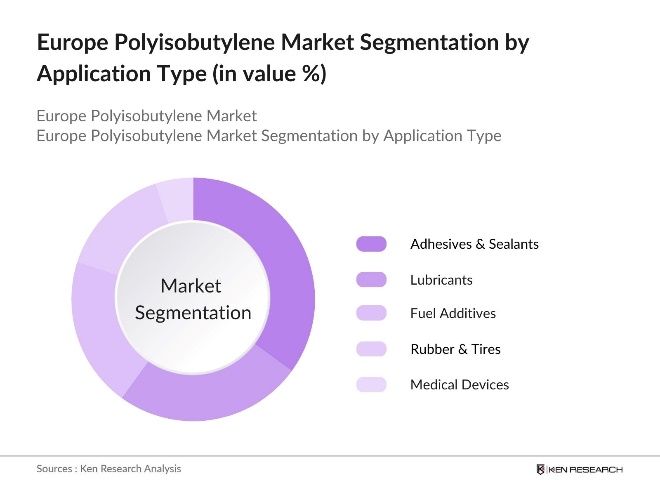

By Application: The market is segmented by application into Adhesives & Sealants, Lubricants, Fuel Additives, Rubber & Tires, and Medical Devices. Adhesives & Sealants dominate the market, driven by the high consumption in construction, packaging, and automotive sectors. The growing infrastructure development across Europe and the shift towards lightweight, durable materials in packaging further enhance the demand for polyisobutylene in adhesives & sealants applications.

Europe Polyisobutylene market Competitive Landscape

The Europe Polyisobutylene market is dominated by both global and regional players who compete based on product innovation, manufacturing capacity, and strategic partnerships. The key companies are involved in R&D activities to develop advanced products with enhanced properties and sustainability, catering to the evolving consumer demands.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD) |

Employees |

R&D Expenditure |

Production Capacity |

Sustainability Initiatives |

Geographical Reach |

|

BASF SE |

1865 |

Ludwigshafen, Germany |

||||||

|

INEOS Group |

1998 |

London, UK |

||||||

|

Lubrizol Corporation |

1928 |

Wickliffe, USA |

||||||

|

TPC Group |

1980 |

Houston, USA |

||||||

|

Chevron Phillips Chemical Company |

2000 |

Texas, USA |

Europe Polyisobutylene market Analysis

Growth Drivers

- Increasing Demand in Automotive Sector: Polyisobutylene (PIB) is seeing rising demand in Europes automotive sector due to its use in applications like fuel additives, lubricants, and sealants. European automobile production was 10.9 million units in 2022, and this number remains steady as of 2024, reflecting the consistent demand for components that use PIB, such as automotive adhesives and sealants. European countries like Germany and France are leading producers of vehicles, and PIBs importance as a key material in making fuel-efficient engines aligns with the European Union's push for reducing CO2 emissions from passenger cars to 95 g/km .

- Rising Applications in Adhesives & Sealants: The adhesives and sealants industry is a significant contributor to the rising PIB demand, especially in packaging and construction. According to Eurostat, the EU produced 142.2 million metric tons of packaging materials in 2023, highlighting the vast potential for PIB applications in the packaging industry. In construction, PIB-based sealants are critical for creating weatherproof joints, which are essential in modern green building initiatives in Germany, the Netherlands, and the Nordic countries. PIBs role in enhancing adhesive performance under varying temperatures makes it a key material for high-performance applications .

- Growing Demand in the Lubricants Industry: The increasing demand from the automotive and manufacturing sectors heavily rely on lubricants for the efficient operation of machinery, reducing friction, and extending the lifespan of equipment. Additionally, the shift towards bio-based and eco-friendly lubricants, driven by stricter environmental regulations, is pushing market growth as industries seek sustainable solutions. Europes focus on reducing energy consumption and emissions further boosts demand for advanced, high-performance lubricants.

Challenges

- Price Volatility of Raw Materials (Isobutylene, Butadiene): The prices of key raw materials for PIB, including isobutylene and butadiene, are highly susceptible to fluctuations in global oil prices. In 2023, the Brent crude oil price averaged around $85 per barrel, influencing the cost of petrochemical derivatives like butadiene and isobutylene, which are vital to PIB production. Europe, which is heavily reliant on oil imports, especially after sanctions on Russian oil, faces heightened risks of price volatility. This creates challenges for PIB manufacturers, as they struggle to maintain stable production costs .

- Stringent Environmental Regulations: Europes stringent environmental regulations, particularly those aimed at reducing carbon emissions and limiting the use of hazardous chemicals, pose challenges for the PIB industry. The European Green Deal and the EU's REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) framework enforce stringent rules on chemical production and usage. PIB manufacturers must ensure compliance, which increases production costs and complicates supply chains. For example, under REACH, producers must account for the full lifecycle impact of their materials, including potential environmental harm .

Europe Polyisobutylene market Future Outlook

Over the next five years, the Europe Polyisobutylene market is expected to show significant growth driven by continuous technological advancements, increasing demand for environmentally sustainable materials, and the expansion of applications in diverse industries such as automotive, packaging, and pharmaceuticals. The rise of electric vehicles and green packaging solutions will further propel the demand for polyisobutylene in Europe.Innovations in bio-based polyisobutylene and the development of high-performance applications in fuel additives and adhesives are key factors expected to drive the market forward. Additionally, growing environmental regulations in Europe will encourage the adoption of more sustainable polyisobutylene solutions, supporting market expansion.

Market Opportunities

- Development of Bio-based Polyisobutylene: The rising demand for sustainable alternatives to petrochemical-based products has created opportunities for the development of bio-based polyisobutylene (bio-PIB). With Europes renewable energy sector growing rapidly (the EU generated 1,298 terawatt-hours of electricity from renewable sources in 2022), bio-PIB is expected to gain traction as part of eco-friendly material solutions. As governments push for green innovations, countries like Germany and the Netherlands are investing in research and development (R&D) for bio-based polymers, which could drive future demand for bio-PIB .

- Expansion in Eastern Europe and Emerging Markets: Eastern Europe represents a burgeoning market for PIB, as the region experiences rapid industrialization and infrastructural development. Countries like Poland, Hungary, and Romania, which collectively saw GDP growth of over 4% in 2023, are investing heavily in infrastructure and automotive manufacturing. This presents opportunities for PIB manufacturers to tap into new demand streams, especially in applications like sealants for construction and lubricants for industrial machinery. Additionally, as emerging markets like Turkey continue to grow, PIB could see increased demand across multiple sectors .

Scope of the Report

|

By Product Type |

Conventional PIB Highly Reactive PIB (HR-PIB) |

|

By Application |

Adhesives & Sealants Lubricants Fuel Additives Rubber & Tires Medical Devices |

|

By Grade |

Low Molecular Weight PIB Medium Molecular Weight PIB High Molecular Weight PIB |

|

By Molecular Weight |

<20,000 Da 20,000 60,000 Da >60,000 Da |

Products

Key Target Audience

Automotive Component Manufacturers

Adhesives & Sealants Manufacturers

Lubricants Suppliers

Rubber & Tire Manufacturers

Medical Device Manufacturers

Packaging Material Suppliers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (REACH, European Green Deal)

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players mentioned in the report:

BASF SE

Kemat Polybutenes

INEOS Group

Lubrizol Corporation

TPC Group

Chevron Phillips Chemical Company

ExxonMobil Corporation

Braskem S.A.

Daelim Industrial Co. Ltd.

Lanxess AG

Reliance Industries Limited

Nippon Chemical Industrial Co., Ltd.

Kothari Petrochemicals

Shandong Hongrui Petrochemical Co., Ltd.

Panjin Heyun Group

Table of Contents

1.Europe Polyisobutylene Market Overview

1.1Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Annual Growth Rate, Volume Growth)

1.4. Market Segmentation Overview (Product Type, Application, Grade, Molecular Weight, End-User)

2.Europe Polyisobutylene Market Size (In USD Bn)

2.1 Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones (Industry Regulations, Technological Advancements)

3. Europe Polyisobutylene Market Analysis

3.1 Growth Drivers

3.1.1. Increasing Demand in Automotive Sector

3.1.2. Rising Applications in Adhesives & Sealants

3.1.3. Growing Demand in Lubricants Industry

3.1.4. Expanding Use in Medical and Pharmaceutical Sectors

3.2 Market Challenges

3.2.1. Price Volatility of Raw Materials (Isobutylene, Butadiene)

3.2.2. Stringent Environmental Regulations

3.2.3. Fluctuating Demand in End-Use Industries (Automotive, Manufacturing)

3.3 Opportunities

3.3.1. Development of Bio-based Polyisobutylene

3.3.2. Expansion in Eastern Europe and Emerging Markets

3.3.3. Increasing Use in Eco-Friendly Applications (Sustainable Packaging, Renewable Energy)

3.4 Trends

3.4.1. Adoption of High-Molecular Weight Polyisobutylene

3.4.2. Innovations in Manufacturing Process (Butyl Rubber, PIB Resins)

3.4.3. Integration of PIB in Green Building Materials

3.5 Government Regulation

3.5.1. REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals)

3.5.2. EU Circular Economy Action Plan

3.5.3. European Green Deal

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Raw Material Suppliers, Manufacturers, Distributors, End Users)

3.8. Porters Five Forces (Supplier Power, Buyer Power, Threat of Substitution, Industry Rivalry)

3.9. Competition Ecosystem (Market Penetration, Regional Expansion)

4. Europe Polyisobutylene Market Segmentation

4.1 By Product Type (In Value %)

4.1.1. Conventional PIB

4.1.2. Highly Reactive PIB (HR-PIB)

4.2 By Application (In Value %)

4.2.1. Adhesives & Sealants

4.2.2. Lubricants

4.2.3. Fuel Additives

4.2.4. Rubber & Tires

4.2.5. Medical Devices

4.3 By Grade (In Value %)

4.3.1. Low Molecular Weight PIB

4.3.2. Medium Molecular Weight PIB

4.3.3. High Molecular Weight PIB

4.4 By Molecular Weight (In Value %)

4.4.1. <20,000 Da

4.4.2. 20,000 60,000 Da

4.4.3. >60,000 Da

4.5 By End-User (In Value %)

4.5.1. Automotive

4.5.2. Construction

4.5.3. Packaging

4.5.4. Pharmaceuticals

4.5.5. Manufacturing

5. Europe Polyisobutylene Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. BASF SE

5.1.2. Kemat Polybutenes

5.1.3. INEOS Group

5.1.4. Lubrizol Corporation

5.1.5. TPC Group

5.1.6. Chevron Phillips Chemical Company

5.1.7. ExxonMobil Corporation

5.1.8. Braskem S.A.

5.1.9. Daelim Industrial Co. Ltd.

5.1.10. Lanxess AG

5.1.11. Reliance Industries Limited

5.1.12. Nippon Chemical Industrial Co., Ltd.

5.1.13. Kothari Petrochemicals

5.1.14. Shandong Hongrui Petrochemical Co., Ltd.

5.1.15. Panjin Heyun Group

5.2 Cross Comparison Parameters (Revenue, Market Share, Product Portfolio, R&D Investments, Production Capacity, Geographical Reach, Pricing Strategy, Sustainability Practices)

5.3. Market Share Analysis (Top Players, Regional Dominance)

5.4. Strategic Initiatives (Product Launches, Partnerships, Joint Ventures)

5.5. Mergers and Acquisitions (Industry Consolidation, Impact on Market Share)

5.6. Investment Analysis (Private Equity, Institutional Investments)

5.7. Venture Capital Funding (Start-up Investments in Bio-based Polyisobutylene)

5.8. Government Grants (EU Funding for Research and Development)

5.9. Private Equity Investments (Infrastructure Expansion, Technological Advancements)

6. Europe Polyisobutylene Market Regulatory Framework

6.1Environmental Standards (EU Emission Directives, VOC Regulations)

6.2. Compliance Requirements (Safety Data Sheets, REACH Compliance)

6.3. Certification Processes (ISO Standards, Industry Certifications)

7. Europe Polyisobutylene Future Market Size (In USD Bn)

7.1Future Market Size Projections (Volume and Revenue Forecast)

7.2. Key Factors Driving Future Market Growth (Demand for Green Technologies, Sustainable Materials)

8. Europe Polyisobutylene Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By Grade (In Value %)

8.4 By Molecular Weight (In Value %)

8.5 By End-User (In Value %)

9. Europe Polyisobutylene Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives (Targeted Campaigns for Key End-Users)

9.4. White Space Opportunity Analysis (Untapped Applications, Niche Markets)

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

In this phase, the research team maps out all major stakeholders within the Europe Polyisobutylene Market. This process includes extensive desk research, sourcing data from proprietary databases and secondary research to determine critical factors influencing market trends.

Step 2: Market Analysis and Construction

The analysis stage involves compiling historical data on the markets penetration and revenue generation. Key metrics, including service quality and performance, are evaluated to provide an accurate estimation of market size and future growth.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through expert consultations with industry practitioners and stakeholders. These insights help to refine and corroborate market data, ensuring the accuracy of the final analysis.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with manufacturers and end-users to gain detailed insights into product performance, preferences, and sales data. This approach validates the bottom-up analysis and guarantees a comprehensive view of the market.

Frequently Asked Questions

1. How big is the Europe Polyisobutylene Market?

The Europe Polyisobutylene Market is valued at USD 890 million, driven by its wide range of applications in automotive, lubricants, and packaging industries.

2. What are the challenges in the Europe Polyisobutylene Market?

Challenges include price volatility of raw materials such as isobutylene, stringent environmental regulations, and fluctuating demand in the automotive and manufacturing industries.

3. Who are the major players in the Europe Polyisobutylene Market?

Major players include BASF SE, INEOS Group, Lubrizol Corporation, TPC Group, and Chevron Phillips Chemical Company, with strong market positioning due to their technological advancements and expansive distribution networks.

4. What are the growth drivers of the Europe Polyisobutylene Market?

The market is propelled by factors such as growing demand in the automotive sector, advancements in production technology, and the rising application of polyisobutylene in environmentally friendly products.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.