Europe Semiconductor Market

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD1990

Region:Europe

Author(s):Paribhasha Tiwari

Product Code:KROD1990

November 2024

83

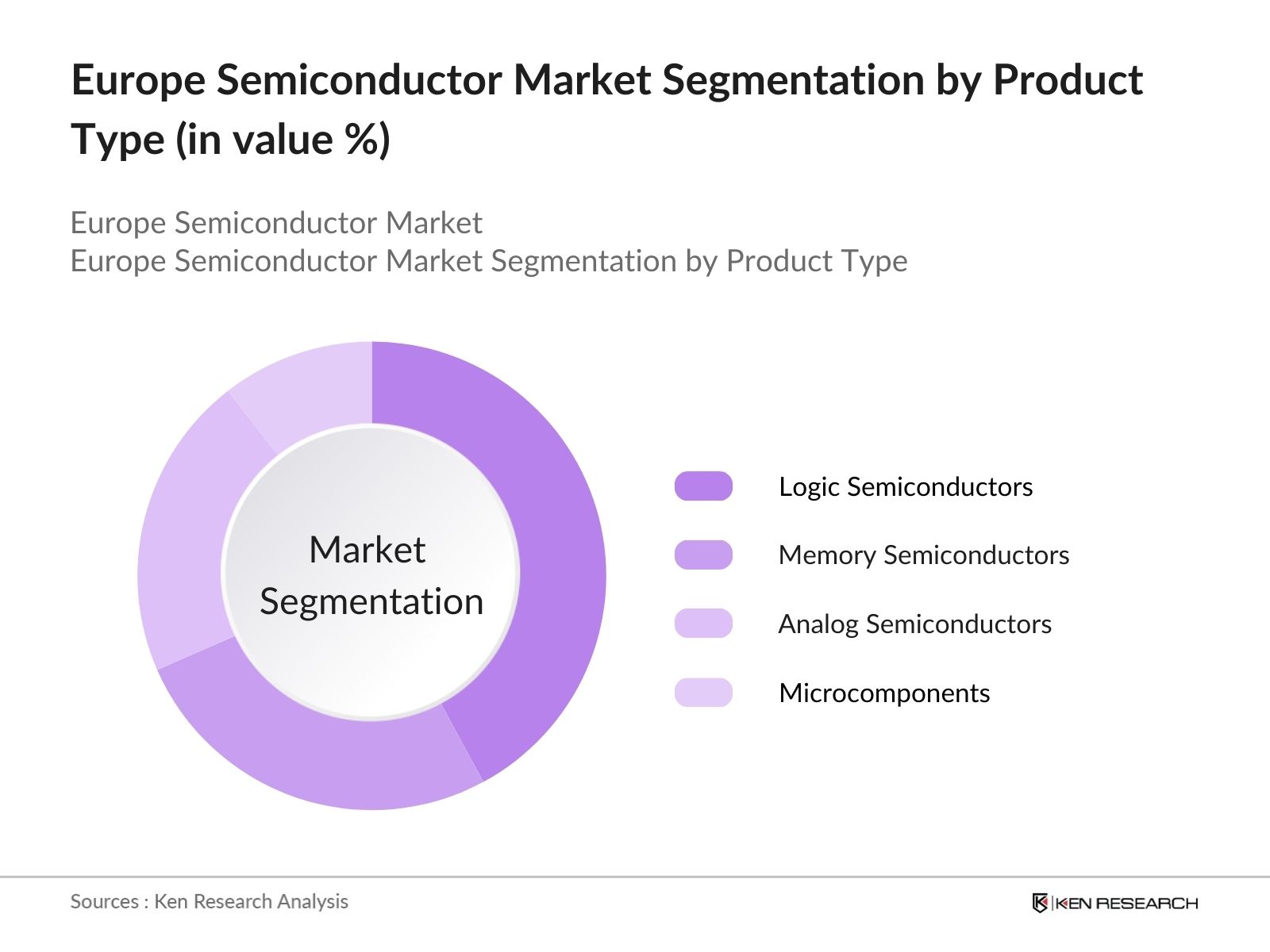

By Product Type: The Europe Semiconductor Market is segmented by product type into logic semiconductors, memory semiconductors, analog semiconductors, and microcomponents. Logic semiconductors hold a dominant market share, driven by their critical role in computing and consumer electronics. Logic semiconductors are essential for performing various computational tasks and are widely used in devices ranging from smartphones to data centers. Major tech companies such as Intel and AMD have propelled the demand for these products, leveraging cutting-edge fabrication technologies to deliver increasingly powerful and efficient processors.

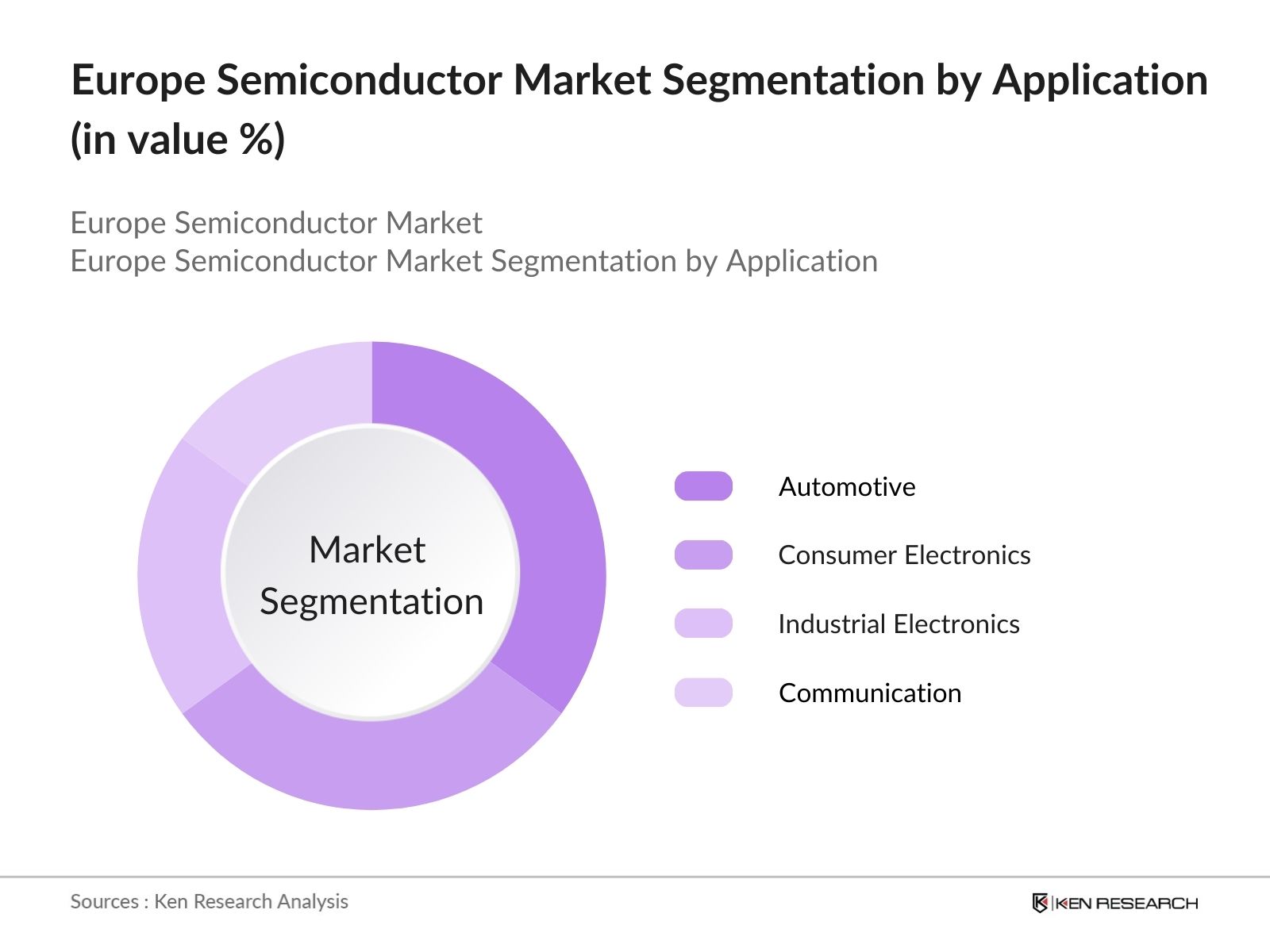

By Application: The market is segmented by application into automotive, consumer electronics, industrial electronics, and communication infrastructure. The automotive segment dominates due to the increasing integration of semiconductors in electric vehicles (EVs), autonomous driving systems, and smart vehicle technologies. The demand for semiconductor components such as sensors, microcontrollers, and power management chips has surged in the automotive industry. This trend is further supported by Europes strong focus on environmental sustainability and the rise of EV production, with companies like Tesla and Volkswagen leading the charge.

The Europe Semiconductor Market is dominated by a few key players who control a significant portion of the market. These companies include large multinational corporations that have established their presence through extensive R&D investments, strategic partnerships, and acquisitions. The competitive landscape is characterized by innovation in semiconductor fabrication processes, with companies focusing on advanced nodes and specialized semiconductor manufacturing equipment.

|

Company |

Established |

Headquarters |

Revenue |

Number of Employees |

Fab Locations |

R&D Investment |

Technology Portfolio |

Market Share (%) |

|---|---|---|---|---|---|---|---|---|

|

Intel Corporation |

1968 |

USA |

- | - | - | - | - | - |

|

STMicroelectronics |

1987 |

Switzerland |

- | - | - | - | - | - |

|

Infineon Technologies AG |

1999 |

Germany |

- | - | - | - | - | - |

|

NXP Semiconductors |

2006 |

Netherlands |

- | - | - | - | - | - |

|

ASML Holding N.V. |

1984 |

Netherlands |

- | - | - | - | - | - |

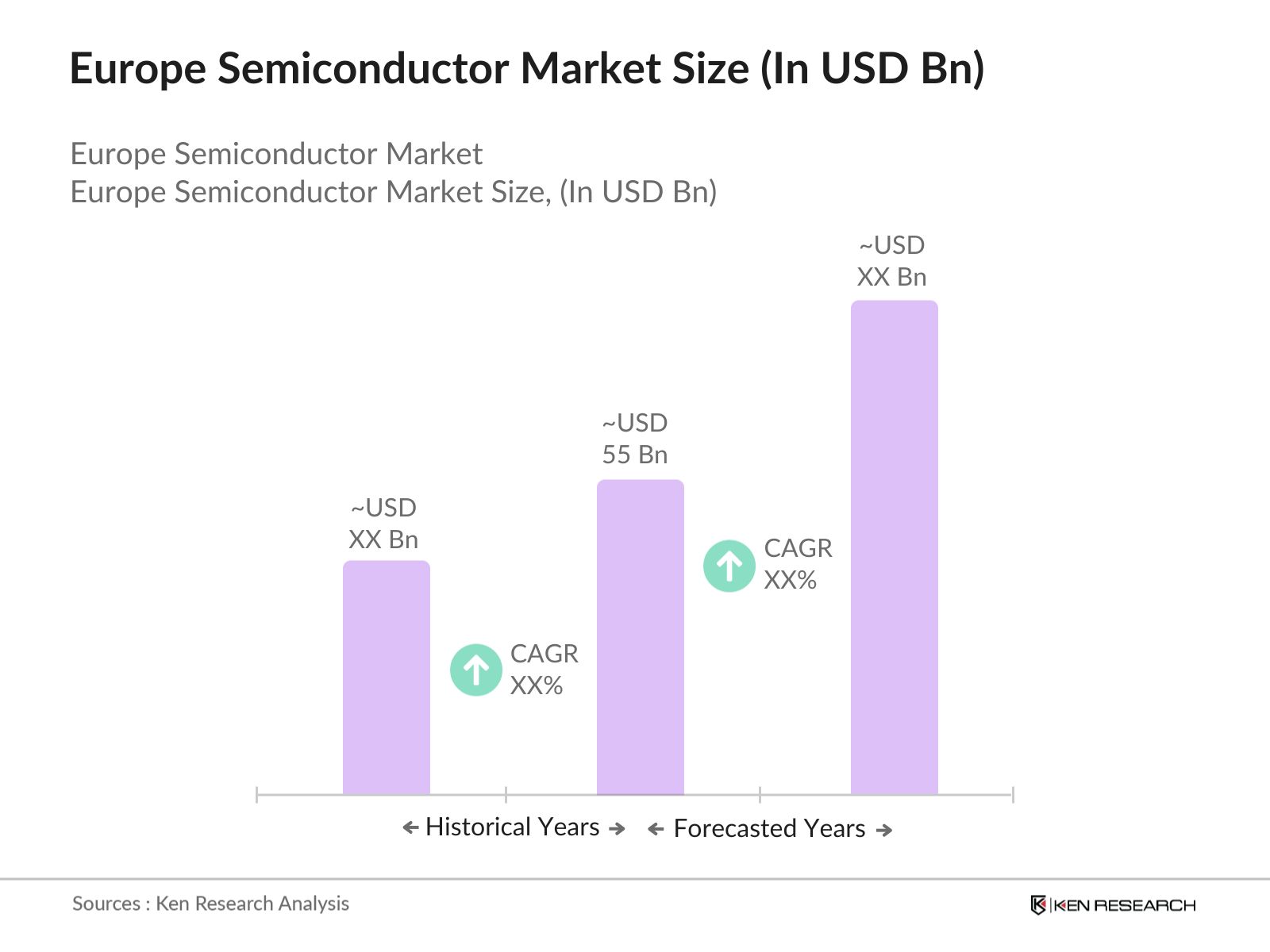

Over the next five years, the Europe Semiconductor Market is expected to witness strong growth due to the increasing integration of semiconductors in various industries, such as automotive, telecommunications, and industrial applications. The rise in electric vehicle production, driven by stringent EU regulations for reducing carbon emissions, will further boost semiconductor demand. The introduction of advanced manufacturing technologies, such as 5nm and below nodes, will continue to drive innovation in the semiconductor industry. The continued investment in semiconductor R&D by governments and private organizations will also play a crucial role in shaping the future of the market.

|

By Product Type |

Logic Semiconductors Memory Semiconductors Analog Semiconductors Microcomponents |

|

By Application |

Automotive Consumer Electronics Industrial Electronics Communication Infrastructure |

|

By Technology Node |

5nm and Below 10nm to 6nm 16nm to 10nm 28nm and Above |

|

By Region |

West Central East North South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand for Consumer Electronics

3.1.2. Expansion of 5G Networks

3.1.3. Growth in Electric Vehicle (EV) Production

3.1.4. Advancements in AI and Machine Learning

3.2. Market Challenges

3.2.1. Semiconductor Supply Chain Disruptions

3.2.2. High Capital Expenditure Requirements

3.2.3. Geopolitical Trade Tensions

3.2.4. Environmental and Sustainability Concerns

3.3. Opportunities

3.3.1. Development of Advanced Packaging Technologies

3.3.2. Growth in IoT Applications

3.3.3. Increasing Semiconductor Demand in Automotive Sector

3.3.4. Expansion of Cloud Computing Infrastructure

3.4. Trends

3.4.1. Rising Adoption of Advanced Node Manufacturing

3.4.2. Semiconductor Foundry Consolidation

3.4.3. Growing Focus on Energy Efficiency and Power Management

3.4.4. Semiconductor Innovation in Quantum Computing

3.5. Government Regulation

3.5.1. EU Chip Act and Strategic Autonomy

3.5.2. Incentives for Semiconductor Manufacturing in Europe

3.5.3. Environmental Compliance Regulations (RoHS, REACH)

3.5.4. Trade Agreements and Export Controls

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem Analysis

3.8. Porters Five Forces

3.9. Competitive Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Logic Semiconductors

4.1.2. Memory Semiconductors

4.1.3. Analog Semiconductors

4.1.4. Microcomponents (MCUs, MPUs, DSPs)

4.1.5. Discrete Semiconductors

4.2. By Application (In Value %)

4.2.1. Automotive

4.2.2. Consumer Electronics

4.2.3. Industrial Electronics

4.2.4. Communications Infrastructure

4.2.5. Healthcare Devices

4.3. By Technology Node (In Value %)

4.3.1. 5nm and Below

4.3.2. 10nm to 6nm

4.3.3. 16nm to 10nm

4.3.4. 28nm and Above

4.4. By Region (In Value %)

4.4.1. Western Europe

4.4.2. Central & Eastern Europe

4.4.3. Northern Europe

4.4.4. Southern Europe

5.1. Detailed Profiles of Major Competitors

5.1.1. Intel Corporation

5.1.2. STMicroelectronics

5.1.3. Infineon Technologies AG

5.1.4. NXP Semiconductors

5.1.5. ASML Holding N.V.

5.1.6. Arm Holdings

5.1.7. GlobalFoundries Inc.

5.1.8. Bosch Sensortec GmbH

5.1.9. Micron Technology, Inc.

5.1.10. Texas Instruments Incorporated

5.1.11. TSMC (Taiwan Semiconductor Manufacturing Company)

5.1.12. Analog Devices, Inc.

5.1.13. Renesas Electronics Corporation

5.1.14. AMS-OSRAM AG

5.1.15. ON Semiconductor Corporation

5.2. Cross Comparison Parameters (Revenue, Headquarters, Number of Employees, Inception Year, Fab Locations, Market Share in Europe, Product Portfolio, R&D Investment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Joint Ventures and Partnerships

5.7. Investment Analysis

5.8. Venture Capital and Private Equity Involvement

6.1. Environmental Standards (RoHS, REACH, EU Ecodesign Directive)

6.2. Compliance and Certification Processes (ISO, CE)

6.3. Semiconductor Trade Policies in Europe

6.4. Industry Standards (JEDEC, IEC, ESCC)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology Node (In Value %)

8.4. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Entry Strategies

9.4. White Space Opportunity Analysis

The research process begins with mapping the entire semiconductor ecosystem in Europe, focusing on key stakeholders, including manufacturers, suppliers, and regulators. A combination of secondary research from proprietary databases and public sources is used to identify the critical variables that affect market dynamics, such as government policies, technological advancements, and industry demand.

In this phase, historical data from reliable sources is analyzed to assess the market size, industry growth, and penetration of semiconductors across various industries. Data such as production volumes, consumption rates, and pricing models are compiled to understand the market structure and generate accurate revenue estimates.

The data is further refined through consultations with industry experts, including semiconductor manufacturers, researchers, and supply chain managers. This step involves interviews and discussions to validate market trends, growth drivers, and technological innovations, ensuring that the insights reflect on-ground realities.

The final stage consolidates all the findings, verified by engaging with manufacturers and industry participants. This stage ensures that market forecasts, segmentation data, and competitive analysis are accurate and comprehensive, giving stakeholders a clear understanding of market trends and opportunities.

The Europe Semiconductor Market is valued at USD 55 billion, driven by rising demand from the automotive and consumer electronics sectors.

Challenges in the Europe Semiconductor Market include supply chain disruptions, high capital expenditure, and geopolitical trade tensions affecting the availability of raw materials and equipment.

Key players in the Europe Semiconductor Market include Intel Corporation, STMicroelectronics, Infineon Technologies AG, NXP Semiconductors, and ASML Holding N.V.

The Europe Semiconductor Market is driven by the growing demand for advanced technologies such as electric vehicles, 5G networks, and artificial intelligence applications.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.