Europe Tuna Fish Market Outlook to 2030

Region:Europe

Author(s):Sanjna Verma

Product Code:KROD7048

December 2024

93

About the Report

Europe Tuna Fish Market Overview

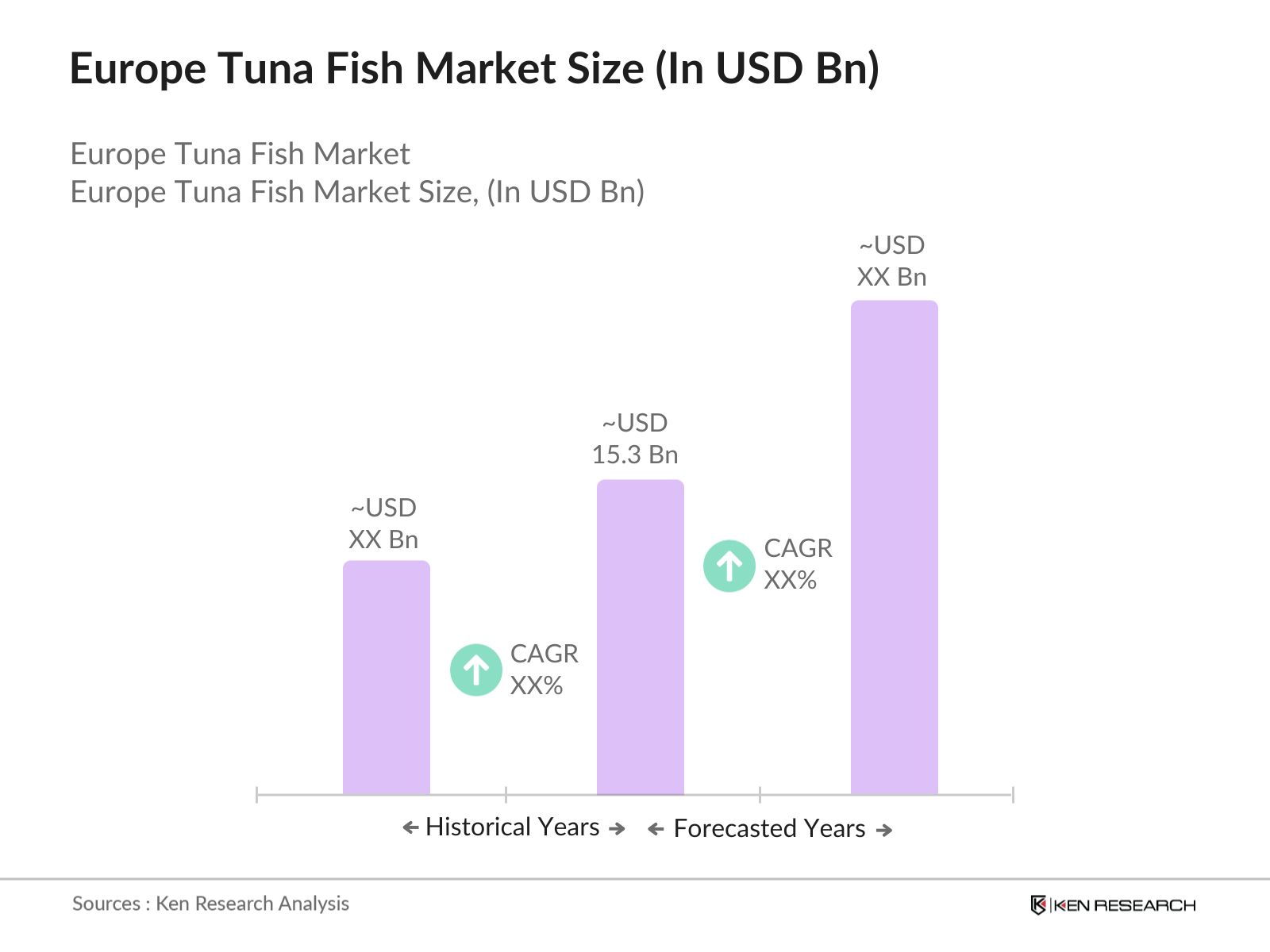

- The Europe Tuna Fish market is valued at USD 15.3 billion, driven by increasing demand for canned and frozen tuna across key European countries. The market has witnessed steady growth over the past five years due to the rising consumer preference for sustainable and certified products. Furthermore, the demand for value-added tuna products like tuna fillets and ready-to-eat meals has been a crucial driver for market growth, particularly in the foodservice industry.

- Spain, Italy, and France dominate the Europe Tuna Fish market due to their long-established fishing industries and favorable geographical locations that provide access to abundant tuna resources. These countries have developed robust supply chains, advanced fishing fleets, and processing capabilities, which allow them to meet both domestic and export demand. Additionally, their regulatory frameworks supporting sustainable fishing practices have further solidified their position in the market.

- The EU Common Fisheries Policy (CFP) is a key regulatory framework that governs the fishing activities of EU member states. It includes stringent measures for conserving fish stocks, including tuna, by setting fishing quotas and promoting sustainable practices. In 2023, the CFP allocated USD 1.09 billion for fisheries conservation and sustainable development initiatives, with a significant portion focused on tuna stocks in the Mediterranean and Atlantic regions.

Europe Tuna Fish Market Segmentation

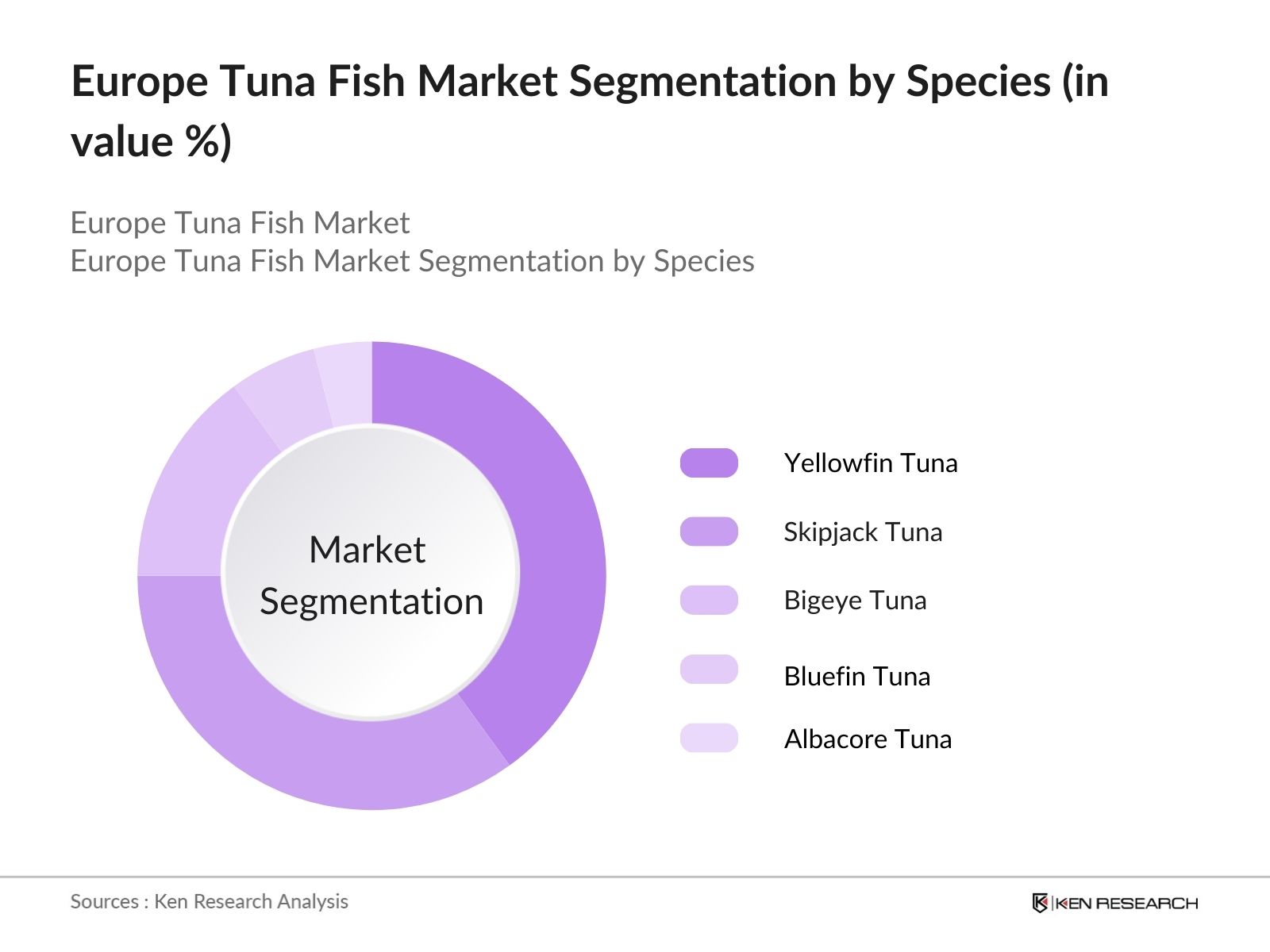

By Species: Europe Tuna Fish market is segmented by species into Yellowfin Tuna, Skipjack Tuna, Bigeye Tuna, Bluefin Tuna, and Albacore Tuna. Yellowfin tuna holds the dominant market share due to its widespread use in both canned and fresh tuna products. Yellowfin tuna is particularly popular because of its versatility in the culinary world and its ability to meet the growing consumer demand for sustainable seafood. The species is commonly used in high-end restaurants and sushi bars, contributing to its strong market presence.

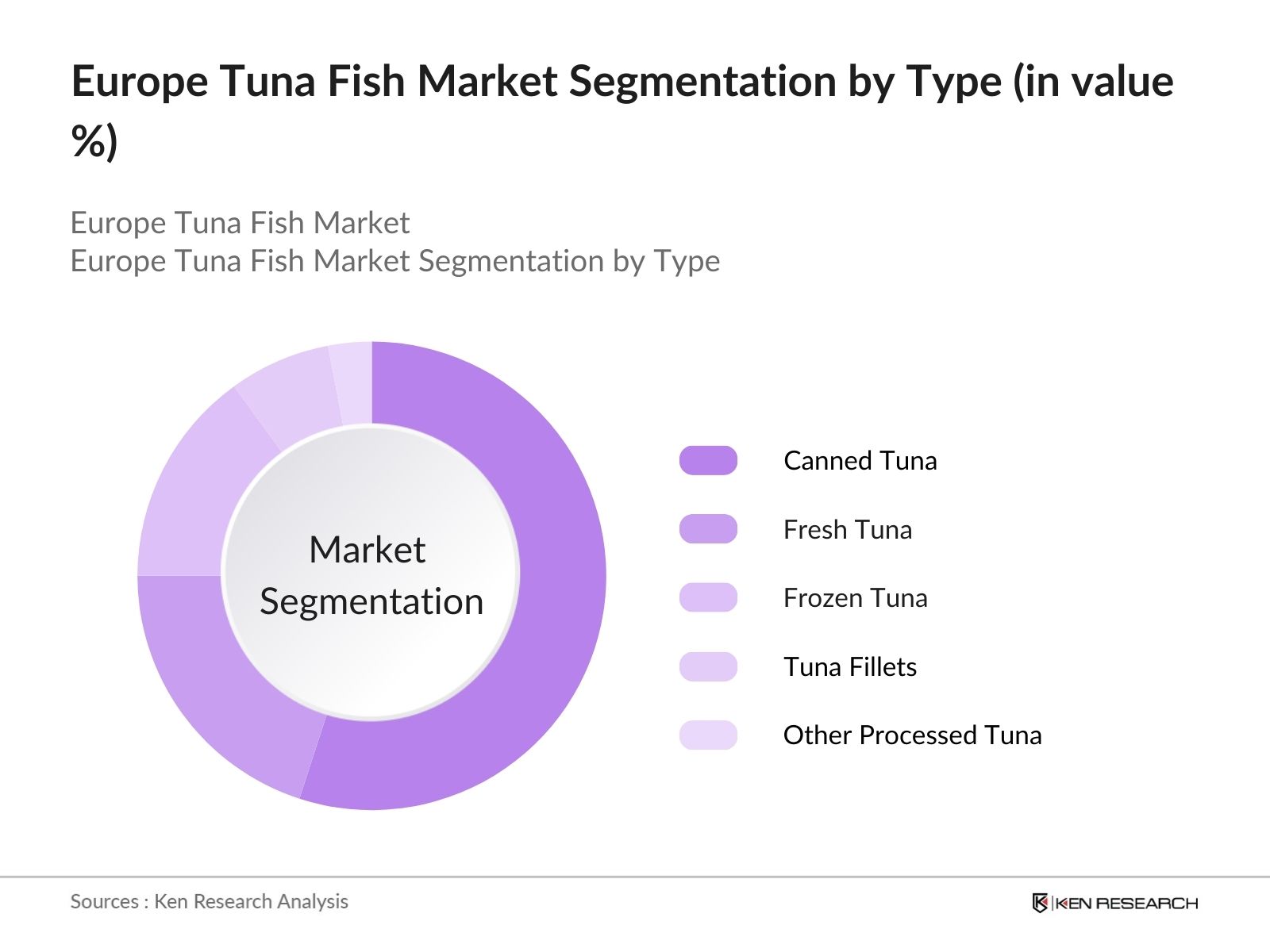

By Type: Europe Tuna Fish market is segmented by type into Fresh Tuna, Frozen Tuna, Canned Tuna, Tuna Fillets, and Other Processed Tuna. Canned Tuna has a dominant market share due to its convenience, affordability, and long shelf life. Canned tuna remains a staple food item in many European households, driven by its use in salads, sandwiches, and ready-to-eat meals. Additionally, advancements in packaging and sustainable certifications have contributed to the growing trust among consumers toward canned tuna products.

Europe Tuna Fish Market Competitive Landscape

The Europe Tuna Fish market is dominated by major players who have established strong supply chains, advanced fishing technologies, and sustainable certifications. The consolidation in the industry highlights the influence of these companies in both domestic and international markets. These firms focus on sustainability, innovation, and premium product segments to maintain their competitive edge.

|

Company Name |

Establishment Year |

Headquarters |

Number of Fishing Vessels |

Sustainability Certifications |

Tuna Processing Facilities |

Revenue (in USD Bn) |

Tuna Exports (% of Total Revenue) |

Market Penetration |

|

Thai Union Group PCL |

1977 |

Thailand |

- |

- |

- |

- |

- |

- |

|

Bumble Bee Foods LLC |

1899 |

USA |

- |

- |

- |

- |

- |

- |

|

Frinsa del Noroeste S.A. |

1961 |

Spain |

- |

- |

- |

- |

- |

- |

|

Bolton Group S.A. |

1949 |

Italy |

- |

- |

- |

- |

- |

- |

|

Grupo Calvo |

1940 |

Spain |

- |

- |

- |

- |

- |

- |

Europe Tuna Fish Market Analysis

Growth Drivers

- Sustainable Fishing Initiatives: Sustainable fishing initiatives in Europe are driving the growth of the tuna fish market, particularly due to strong enforcement of the European Union's regulations on fishing practices. According to data from the EU Commission, over 85% of EU-managed fish stocks, including tuna, are fished sustainably as of 2024, enhancing the quality and availability of tuna in the market. These initiatives are crucial in maintaining the long-term availability of tuna, with governments enforcing compliance to reduce overfishing and protect marine biodiversity.

- Increased Demand for Tuna in Canned Fish Segment: The demand for canned tuna remains robust, particularly in export markets. According to the European Market Observatory for Fisheries and Aquaculture (EUMOFA), in 2022, the EU produced approximately416,100 tonsof "prepared or preserved skipjack and Atlantic bonito tuna," driven by increased consumption of canned tuna due to its convenience and affordability.

- Growth of Aquaculture and Fisheries: Aquaculture plays a significant role in supporting the EUs tuna supply. According to recent reports, the total aquaculture production in the EU for 2022 was approximately1.08 million tonnes. The expansion of tuna farms, particularly in Spain and Italy, is crucial for meeting rising demand, with investments in sustainable practices like cage farming and hatchery programs. This growth aligns with the EUs Common Fisheries Policy, which emphasizes sustainable aquaculture growth to supplement traditional wild capture.

Challenges

- Illegal, Unreported, and Unregulated (IUU) Fishing: IUU fishing remains a significant challenge for the European tuna market. According to the European Fisheries Control Agency, IUU fishing results in an estimated loss of around USD 10.98 billion annually across the EUs fishing sector, directly affecting the tuna industry. The EU has increased its surveillance measures to reduce IUU fishing in the Mediterranean and Atlantic, yet enforcement remains a challenge due to limited resources and the vast geographical scope of tuna habitats.

- Climate Change Impact on Tuna Stocks: Climate change is increasingly affecting tuna stocks in European waters. The European Environmental Agency reported that rising ocean temperatures are shifting tuna migration patterns, with some stocks moving further north. These changes make it harder for European fleets to predict and harvest tuna. In 2023, there was a recorded 10% decrease in tuna catches in the Mediterranean due to warmer sea temperatures, highlighting the growing risk posed by climate change.

Europe Tuna Fish Market Future Outlook

Europe Tuna Fish market is expected to see significant growth driven by consumer demand for sustainable and premium-quality seafood. The increasing awareness of the environmental impact of overfishing has led to a rise in demand for sustainably sourced tuna products. Additionally, advancements in processing technologies, coupled with expanding product lines in premium and ready-to-eat tuna segments, will further contribute to market growth.

Market Opportunities

- Growth in Premium and Organic Tuna Markets: The premium and organic tuna markets in Europe are growing, driven by consumer demand for high-quality, sustainably sourced seafood. According to the EU Market Observatory for Fisheries and Aquaculture Products (EUMOFA), premium tuna, including organic varieties, accounted for approximately 15% of total tuna sales in the EU in 2023. Markets such as Germany, France, and the Netherlands are seeing increased demand for organic tuna, supported by the availability of MSC (Marine Stewardship Council) certified tuna products.

- Rising Popularity of Sustainable Tuna Certifications: Sustainable certifications, such as those provided by the MSC, are becoming more important for consumers across Europe. In 2023, over 60% of canned tuna sold in Europe carried some form of sustainability certification, according to EUMOFA. The rise in certified sustainable products has opened up new opportunities for European tuna producers, particularly in markets like Scandinavia and Western Europe, where consumers are increasingly prioritizing sustainability in their purchasing decisions.

Scope of the Report

|

By Segments |

Sub-segments |

|

By Species |

Yellowfin Tuna |

|

Skipjack Tuna |

|

|

Bigeye Tuna |

|

|

Bluefin Tuna |

|

|

Albacore Tuna |

|

|

By Type |

Fresh Tuna |

|

Frozen Tuna |

|

|

Canned Tuna |

|

|

Tuna Fillets |

|

|

Other Processed Tuna |

|

|

By Fishing Method |

Purse Seining |

|

Longlining |

|

|

Pole and Line |

|

|

Handline Fishing |

|

|

By End User |

Retail |

|

Foodservice |

|

|

Industrial Processing |

|

|

By Country |

Spain |

|

Italy |

|

|

France |

|

|

Germany |

|

|

United Kingdom |

Products

Key Target Audience

Tuna Fishing Companies

Tuna Processing and Canning Companies

Seafood Exporters

Foodservice Chains and Retailers

Environmental and Sustainability Organizations

Logistics and Cold Storage Providers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (European Union, Marine Stewardship Council)

Companies

Players Mentioned in the Report

Thai Union Group PCL

Bumble Bee Foods LLC

Frinsa del Noroeste S.A.

Bolton Group S.A.

Grupo Calvo

American Tuna Inc.

Century Pacific Food Inc.

Ocean Brands GP

Sea Value PLC

Alliance Select Foods International Inc.

Table of Contents

1. Europe Tuna Fish Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Europe Tuna Fish Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Europe Tuna Fish Market Analysis

3.1. Growth Drivers

3.1.1. Sustainable Fishing Initiatives

3.1.2. Increased Demand for Tuna in Canned Fish Segment

3.1.3. Growth of Aquaculture and Fisheries

3.1.4. EU Fishing Regulations

3.2. Market Challenges (Illegal Fishing, Climate Change, High Operation Costs)

3.2.1. Illegal, Unreported, and Unregulated (IUU) Fishing

3.2.2. Climate Change Impact on Tuna Stocks

3.2.3. Rising Operational and Regulatory Costs

3.2.4. Competition from Other Seafood Products

3.3. Opportunities (Premium Tuna Segments, Sustainable Certification)

3.3.1. Growth in Premium and Organic Tuna Markets

3.3.2. Rising Popularity of Sustainable Tuna Certifications

3.3.3. Expansion into Non-traditional European Markets

3.3.4. Advancements in Tuna Fishing Technology

3.4. Trends (Sustainability, Value-Added Products)

3.4.1. Shift Toward Sustainable Tuna Fishing Practices

3.4.2. Increasing Demand for Frozen Tuna Products

3.4.3. Growth of Tuna-Based Ready-to-Eat Meals

3.4.4. Value Addition and Processed Tuna Products

3.5. Government Regulations (Fishing Quotas, EU Common Fisheries Policy)

3.5.1. European Union Common Fisheries Policy (CFP)

3.5.2. Fishing Quotas for Tuna Species

3.5.3. Regulations on Tuna Trade and Exports

3.5.4. National Environmental and Marine Protection Laws

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Europe Tuna Fish Market Segmentation

4.1. By Species (In Value %)

4.1.1. Yellowfin Tuna

4.1.2. Skipjack Tuna

4.1.3. Bigeye Tuna

4.1.4. Bluefin Tuna

4.1.5. Albacore Tuna

4.2. By Type (In Value %)

4.2.1. Fresh Tuna

4.2.2. Frozen Tuna

4.2.3. Canned Tuna

4.2.4. Tuna Fillets

4.2.5. Other Processed Tuna

4.3. By Fishing Method (In Value %)

4.3.1. Purse Seining

4.3.2. Longlining

4.3.3. Pole and Line

4.3.4. Handline Fishing

4.4. By End User (In Value %)

4.4.1. Retail

4.4.2. Foodservice

4.4.3. Industrial Processing

4.5. By Country (In Value %)

4.5.1. Spain

4.5.2. Italy

4.5.3. France

4.5.4. Germany

4.5.5. United Kingdom

5. Europe Tuna Fish Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Thai Union Group PCL

5.1.2. Bumble Bee Foods LLC

5.1.3. Frinsa del Noroeste S.A.

5.1.4. Bolton Group S.A.

5.1.5. American Tuna Inc.

5.1.6. Grupo Calvo

5.1.7. Century Pacific Food Inc.

5.1.8. Alliance Select Foods International Inc.

5.1.9. Sea Value PLC

5.1.10. Ocean Brands GP

5.2. Cross Comparison Parameters (Fisheries Certifications, Revenue, Tuna Catches, Sustainability Initiatives, Fishing Fleet Size, Market Share, Geographical Presence, Product Range)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Support Programs

5.8. Industry Collaborations

6. Europe Tuna Fish Market Regulatory Framework

6.1. Environmental Standards

6.2. EU Compliance Regulations

6.3. Fisheries Management and Quota Systems

6.4. Marine Sustainability Certification Requirements

7. Europe Tuna Fish Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Europe Tuna Fish Future Market Segmentation

8.1. By Species (In Value %)

8.2. By Type (In Value %)

8.3. By Fishing Method (In Value %)

8.4. By End User (In Value %)

8.5. By Country (In Value %)

9. Europe Tuna Fish Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Product Portfolio Optimization

9.3. Market Entry Strategies

9.4. White Space Opportunity Analysis

Disclaimer

Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins by mapping the entire ecosystem of stakeholders in the Europe Tuna Fish market. This step involves extensive secondary research to gather data from proprietary and public sources such as government databases, trade associations, and industry reports. The aim is to identify key variables such as fishing quotas, export regulations, and sustainability certifications.

Step 2: Market Analysis and Construction

Historical data on the Europe Tuna Fish market is compiled to analyze current trends in product types, market segments, and end-user applications. This includes tracking the tuna catch volumes, processing capacity, and demand from various consumer segments such as foodservice and retail. The goal is to evaluate market structure and revenue generation trends.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses on market dynamics, product preferences, and consumer behavior are validated through in-depth interviews with industry experts and tuna fishing companies. This helps to refine market estimates, and the insights gathered directly from industry participants add depth to the quantitative data.

Step 4: Research Synthesis and Final Output

In the final stage, tuna fish companies and stakeholders are consulted to verify findings and collect specific insights on market opportunities, consumer preferences, and upcoming regulatory changes. The data collected is synthesized to provide a comprehensive overview of the Europe Tuna Fish market.

Frequently Asked Questions

01. How big is the Europe Tuna Fish Market?

The Europe Tuna Fish market is valued at USD 4.8 billion, driven by strong demand for canned and frozen tuna products, especially in Spain, Italy, and France, where consumption of seafood is a key dietary component.

02. What are the challenges in the Europe Tuna Fish Market?

Challenges in the Europe Tuna Fish market include illegal fishing activities, the high operational costs of sustainable fishing, and climate change impacting tuna stocks. These factors create difficulties in maintaining consistent tuna supply.

03. Who are the major players in the Europe Tuna Fish Market?

Key players in the Europe Tuna Fish market include Thai Union Group, Bumble Bee Foods, Frinsa del Noroeste, Bolton Group, and Grupo Calvo. These companies dominate the market due to their advanced fishing fleets, sustainability certifications, and extensive processing capacities.

04. What are the growth drivers of the Europe Tuna Fish Market?

Growth drivers in Europe Tuna Fish market include increasing consumer demand for sustainable seafood, rising awareness of environmental issues, and the expanding popularity of value-added tuna products like ready-to-eat meals. Regulatory support for sustainable fishing practices also contributes to market expansion.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.